Introduction

High-income W-2 professionals and investors in the 37% federal tax bracket face a brutal tax reality: standard deductions don't scale with income. A physician earning $500,000 pays the same standard deduction as someone earning $150,000, leaving high earners with minimal tax relief. Meanwhile, the Net Investment Income Tax (NIIT) adds another 3.8% on passive rental income above threshold limits, compounding the burden.

Real estate is one of the few areas of the tax code that rewards high earners with legal, substantial deductions. The catch: passive activity loss rules trap most of those benefits unless you qualify under specific IRS classifications. Most rental property advice ignores this barrier entirely — which is why it fails high earners.

This guide covers Real Estate Professional Status (REPS), the Short-Term Rental (STR) strategy, 1031 exchanges, and cost segregation. Executed correctly, these strategies eliminate current-year tax liability outright. Not just defer it.

TL;DR

- Real estate offers high earners rare access to deductions that can offset W-2 and business income, not just passive gains

- The passive activity loss rule blocks most rental deductions unless you qualify for REPS or use the STR loophole

- REPS requires 750+ hours and >50% of total work time in real estate; the spouse strategy makes this accessible to dual-income couples

- Cost segregation front-loads depreciation deductions, creating $150,000–$200,000+ first-year write-offs on million-dollar properties

- Stacking REPS, cost segregation, and 1031 exchanges can produce six-figure annual tax reductions for disciplined investors

Why High-Income Earners Face a Steeper Tax Challenge

The Passive Activity Loss Trap

The Tax Reform Act of 1986 introduced the passive activity loss (PAL) rule, classifying rental real estate as "passive." Under IRC §469, passive losses can only offset passive income — not W-2 wages or business income.

A $25,000 active participation exception exists, but it phases out completely at $150,000 modified adjusted gross income (MAGI). For physicians, executives, and entrepreneurs earning well above that threshold, this exception provides no relief.

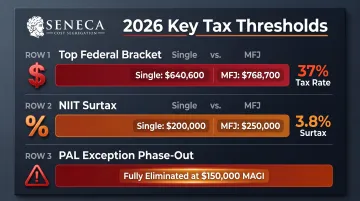

Key PAL thresholds for 2026:

- Top federal bracket: 37% on income over $640,600 (single) or $768,700 (married filing jointly)

- NIIT surtax: 3.8% on investment income above $200,000 (single) or $250,000 (MFJ)

- $25,000 PAL exception: Fully phased out at $150,000 MAGI

Once your income clears these thresholds, rental property losses become "suspended passive losses" — trapped on your return until you sell the property in a fully taxable transaction.

The NIIT Compounds the Problem

High earners also face the Net Investment Income Tax of 3.8% on passive rental income once AGI exceeds IRS thresholds. Rental income many investors assume is sheltered ends up taxed at combined rates exceeding 40%.

Why Standard Rental Advice Fails

The conventional wisdom — "buy a rental property and deduct losses" — assumes you can use those deductions immediately. For high earners, that assumption doesn't hold. Suspended losses accumulate on your return with no current-year benefit. When you eventually sell, they offset capital gains, not the ordinary income driving your tax bill in the first place.

Real Estate Tax Strategies That Actually Move the Needle

The strategies below work because they either reclassify rental activity (making losses non-passive) or defer capital gains at sale. Both create immediate, measurable tax relief.

Real Estate Professional Status (REPS)

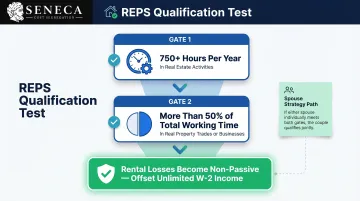

To qualify for REPS under IRC §469(c)(7), you must meet two tests:

- Spend more than 750 hours per year in real estate activities

- Spend more than 50% of total working time on real property trades or businesses

When qualified, rental losses become non-passive and can offset unlimited W-2 or business income.

REPS is effectively off the table for full-time W-2 professionals working 2,000+ hours annually. For married couples filing jointly, however, either spouse can satisfy the requirements. The qualifying spouse's status applies to the joint return, allowing the high earner's income to be offset.

A cardiologist earning $550,000 annually works 2,200 hours in medicine. But if their spouse dedicates 800 hours to managing the couple's rental portfolio—and performs no other work exceeding those 800 hours—the spouse qualifies. The couple's joint return can now use rental losses to offset the physician's W-2 income.

Qualifying for REPS removes the "per se passive" label from rental activities, but material participation in each property still must be proven. Common thresholds include:

- 500-hour test across all properties (requires a grouping election)

- 100-hour test for individual properties, provided your hours exceed anyone else's

The Short-Term Rental (STR) Loophole

Properties where the average guest stay is seven days or fewer are not classified as rental real estate under Treasury Regulation §1.469-1T(e)(3)(ii)(A). Instead, they're treated as business activities, falling outside passive activity rules entirely.

A W-2 professional can generate non-passive losses from an STR by meeting material participation—most commonly the 100-hour test (100+ hours AND more hours than anyone else managing the property).

Critical Restrictions:

- Property manager hours count against you: Hiring a full-service manager whose hours exceed yours will fail the test

- Owner-use days don't count: Personal use days and repair days are excluded from the seven-day average calculation

- Time logs are mandatory: Contemporaneous records showing dates, hours, property addresses, and specific activities performed

In Lucero v. Commissioner (T.C. Memo. 2020-136), the Tax Court denied material participation because taxpayers failed to prove their hours exceeded their property manager's hours.

One additional risk: providing "substantial services" like daily cleaning, meals, or concierge assistance converts income from Schedule E to Schedule C, subjecting it to 15.3% self-employment tax. Basic services—utilities, trash, cleaning between stays—do not trigger this reclassification.

The 1031 Exchange: Deferring Capital Gains at Sale

A 1031 exchange under IRC §1031 allows investors to sell an investment property and defer capital gains tax by reinvesting proceeds into a "like-kind" property within strict IRS timeframes:

- 45-day identification window: Identify replacement property within 45 days of sale

- 180-day closing window: Complete the exchange within 180 days

A qualified intermediary (QI) must hold funds between transactions. Direct receipt of sale proceeds disqualifies the exchange entirely.

Both capital gains and depreciation recapture (taxed at 25%) are deferred—not eliminated. Many investors manage this through continued exchanges or holding until death, when IRC §1014 provides a step-up in basis and permanently eliminates the deferred taxes.

Cost Segregation: The Multiplier That Amplifies Every Strategy

What Cost Segregation Does

Cost segregation is an engineering-based tax study that reclassifies building components from 27.5-year (residential) or 39-year (commercial) depreciation into shorter recovery periods:

- 5-year property: Carpeting, appliances, decorative lighting, specialized cabinetry

- 7-year property: Office furniture and equipment

- 15-year property: Fences, roads, landscaping, parking structures

This front-loads depreciation deductions, creating large paper losses in early ownership years rather than spreading them over decades.

Bonus Depreciation Supercharges the Strategy

The "One Big Beautiful Bill" (P.L. 119-21), enacted July 4, 2025, permanently restored 100% bonus depreciation for qualified property placed in service after January 19, 2025. Components reclassified through cost segregation can now be deducted in full in year one.

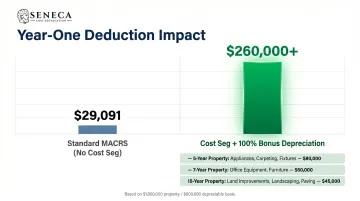

$1,000,000 Property Example:

Assuming $800,000 depreciable basis (20% allocated to land) and cost segregation reclassifying 30% of basis:

| Scenario | First-Year Deduction |

|---|---|

| Standard MACRS (no bonus) | ~$29,091 |

| Cost seg + 100% bonus (post-Jan 19, 2025) | ~$260,000+ |

Why Cost Segregation Is the Multiplier

Cost segregation doesn't stand alone—it generates the large paper losses that make REPS and STR strategies powerful. Without sufficient depreciation, even qualifying for REPS may produce modest savings. With cost segregation, first-year deductions can reach five to six figures per property.

Depreciation Recapture: The Trade-Off

When a property is sold, the IRS recaptures accelerated depreciation as ordinary income (up to 25% rate). However, this can be deferred through 1031 exchanges or reduced through long-term holds. The time-value of money consistently makes front-loaded deductions more valuable than spreading them out, even accounting for eventual recapture.

Choosing the Right Cost Segregation Study

Study quality matters — especially for high earners whose large first-year deductions are more likely to draw IRS scrutiny. Seneca Cost Segregation's ASCSP-certified engineering team has completed studies on over 10,200 properties nationwide, delivering an average first-year deduction of $171,243. Studies are completed in 2–4 weeks and include AuditDefense backed by a money-back guarantee. For investors combining cost segregation with REPS or STR status, that audit protection is worth factoring into the decision.

Stacking Strategies for Maximum Tax Reduction

The Power of Combination

The real tax reduction comes from stacking strategies deliberately:

Example scenario:

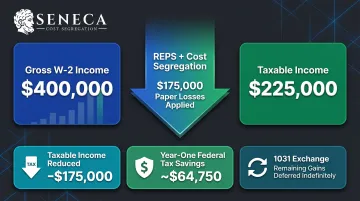

A tech executive earning $400,000 whose spouse qualifies for REPS owns three rental properties. Cost segregation generates $175,000 in year-one paper losses across the portfolio. Key outcomes:

- Taxable income drops from $400,000 to $225,000 after REPS offsets W-2 earnings directly

- Federal tax savings reach approximately $64,750 in year one (37% bracket)

- 1031 exchange on sale defers capital gains and depreciation recapture, letting wealth compound tax-deferred indefinitely

Which Strategies for Which Investors

Investor profile mapping:

- Full-time W-2 professional with limited time: STR loophole + cost segregation

- Couple where one spouse can dedicate 750+ hours: REPS + cost segregation + 1031 exchanges

- Long-term portfolio builder: 1031 exchange chains + cost segregation

- All profiles: Cost segregation as the base layer

Legal but Not Simple

Stacking these strategies requires proactive annual tax planning, not reactive filing. Several rules interact in ways that can produce unexpected results without careful coordination:

- Passive income rules determine which losses can offset active W-2 income

- Recapture timelines affect how depreciation is taxed on sale

- Grouping elections influence how the IRS treats multiple properties under REPS

- Material participation thresholds must be documented and met annually

Work with a cost segregation specialist alongside your CPA before filing — not after.

Documentation and Compliance: Protecting Your Deductions

IRS Scrutiny Is Real

Large real estate deductions—especially from REPS, STR loophole, and cost segregation—draw IRS attention. Contemporaneous time logs are essential: specific dates, hours, property addresses, and activities performed.

Generic entries like "property management" have repeatedly failed in Tax Court. In Moss v. Commissioner (135 T.C. 365), the court rejected reconstructed logs and ballpark estimates.

Good documentation is only part of the picture. These compliance gaps catch high earners off guard even when their deductions are legitimate:

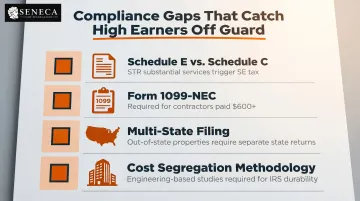

Compliance Touchpoints High Earners Overlook

- Schedule E vs. Schedule C: STRs with substantial services may shift your filing from Schedule E to Schedule C

- Form 1099-NEC: Required for any contractor paid $600+ annually under IRC §6041

- Multi-state filing: Out-of-state properties trigger separate filing requirements in each jurisdiction

- Cost segregation methodology: Engineering-based studies hold up under IRS review; software-only tools frequently don't

IRS Audit Technique Guides

The IRS publishes Audit Technique Guides (ATGs) for "Passive Activity Losses" and "Cost Segregation." These guides lay out exactly how examiners approach each issue — including REPS hour verification, property classification disputes, and material participation challenges. Knowing what auditors look for is the first step to making sure your records can answer their questions.

Frequently Asked Questions

What are the best tax strategies for high earners who invest in real estate?

Cost segregation, REPS, the STR loophole, and 1031 exchanges are the most effective strategies. The optimal approach stacks multiple strategies based on your income type, time availability, and property mix for maximum tax reduction.

Is real estate a good investment for high income earners?

Real estate offers depreciation deductions unavailable in stocks or bonds and provides passive income with potential tax shelter. With the right structure, it can convert paper losses into real tax savings against high W-2 income.

Can real estate losses offset W-2 income?

Generally, no—passive losses cannot offset W-2 income under IRC §469. The two main exceptions are qualifying for REPS or meeting material participation in a short-term rental property, both of which convert passive losses to non-passive.

What is the passive activity loss rule and why does it matter for high earners?

The 1986 PAL rule blocks rental losses from offsetting active income. The $25,000 exception phases out completely at $150,000 MAGI, leaving rental property tax benefits inaccessible to most high earners. REPS or the STR loophole are the primary workarounds.

How much can I save with a cost segregation study?

Savings depend on property value, asset mix, and your ability to use the resulting losses through REPS or STR qualification. A professional engineering-based study on a qualifying property can identify $150,000 to $200,000+ in accelerated first-year deductions.

Do I have to be a real estate professional to benefit from these tax strategies?

REPS is the most powerful strategy but not required. The STR loophole is accessible to busy W-2 professionals who meet material participation, and cost segregation with 1031 exchanges provide value regardless of professional status.