Introduction

Most real estate agents operate as 1099 independent contractors — not W-2 employees — which means the IRS treats them as self-employed business owners responsible for their own tax planning, estimated payments, and deductions. This classification offers real flexibility and the freedom to build a business on your own terms, but it also carries a hidden cost that catches many agents off guard during their first profitable year.

Without a proactive strategy, agents can lose a significant portion of commission income to self-employment tax (15.3% on every dollar of net profit), income tax (ranging from 10% to 37% depending on your bracket), and missed deductions that could have legally reduced taxable income by thousands.

The difference between an agent who treats tax planning as a year-end scramble and one who implements strategic deductions, entity structuring, and depreciation can easily exceed $20,000 annually — and considerably more for top producers.

This guide covers the tax strategies that matter most for 1099 real estate agents:

- Choosing the right business structure to reduce self-employment tax

- Maximizing often-overlooked deductions

- Managing quarterly estimated payments without penalties

- Using retirement contributions for tax deferral

- Amplifying savings through investment property depreciation and cost segregation

TLDR:

- 1099 agents pay 15.3% self-employment tax plus income tax, but can deduct 50% of SE tax and claim business expenses on Schedule C

- S-Corp election saves thousands once net profit exceeds $40,000–$60,000 by splitting income between salary and distributions

- Top deductions include vehicle expenses, home office, health insurance premiums, and the Augusta Rule for rental income

- Cost segregation studies on investment properties can generate six-figure first-year depreciation deductions

- Real Estate Professional Status lets rental losses offset commission income directly

What Being a 1099 Real Estate Agent Really Means for Your Taxes

Operating as a 1099 independent contractor fundamentally changes your tax obligations compared to W-2 employees. Every dollar you earn in commission income gets reported on Schedule C (Form 1040), where you calculate net profit by subtracting ordinary business expenses. That net profit then faces two layers of federal taxation: self-employment tax and income tax.

Self-employment tax hits first: You owe 15.3% on all net earnings, consisting of 12.4% for Social Security and 2.9% for Medicare. For 2026, the Social Security portion applies to the first $184,500 of net earnings. Unlike W-2 employees whose employer absorbs half the payroll tax burden, 1099 agents pay the full amount — both the employee and employer share.

There is one immediate upside: you can deduct 50% of your self-employment tax on Form 1040 (Schedule 1, line 15) as an above-the-line adjustment to income. This reduces your adjusted gross income regardless of whether you itemize. For an agent with $100,000 in net profit — SE tax of roughly $15,300 — that deduction alone saves $7,650 in taxable income.

Income tax applies on top: After the SE tax deduction, your remaining income is subject to federal income tax at progressive rates (10% to 37%) and potentially state income tax. Combined, the effective tax burden on net profit can easily reach 35-45% for agents in higher brackets.

Two more rules catch agents off guard:

- Report all commissions, even without a 1099-NEC — the IRS expects every dollar declared, and underreporting triggers audit risk and penalties.

- Pay quarterly estimates using Form 1040-ES. For the 2026 tax year, due dates fall on April 15, June 15, September 15, and January 15, 2027. Missing them triggers underpayment penalties even if your annual return is filed on time.

Choosing the Right Business Structure to Reduce Self-Employment Tax

By default, 1099 real estate agents operate as sole proprietors, which is the simplest structure but also the most expensive from a tax perspective. Every dollar of net profit is subject to the full 15.3% self-employment tax, and as commission income grows, that bill compounds fast. An agent earning $80,000 in net profit pays roughly $12,240 in SE tax; at $150,000, the bill jumps to over $21,000.

The S-Corp Election Strategy

Forming an LLC (or Professional Association in some states) and electing S-Corporation taxation allows agents to split income between a W-2 salary and profit distributions. Only the salary portion is subject to SE tax — distributions are not. This distinction can save thousands annually.

For example, an agent with $100,000 in net profit who pays themselves a $60,000 salary and takes $40,000 as distributions only pays SE tax on the $60,000, saving approximately $6,120 compared to sole proprietorship treatment.

The "Reasonable Salary" Requirement:

The IRS requires the salary to reflect fair market compensation for the agent's actual work. Artificially low salaries designed to minimize payroll tax trigger audits and penalties. In David E. Watson, P.C. v. United States, the court recharacterized a $24,000 salary as unreasonably low for a professional, assessing FICA taxes on the distributions. The IRS examines factors such as training, experience, time devoted to the business, comparable salaries for similar roles, and the ratio of salary to distributions.

Document your compensation position thoroughly: maintain market wage surveys, board minutes approving salary, and time logs showing hours worked. This paper trail is your first line of defense in an audit.

Conservative practitioners often recommend a salary of 40-60% of total net income for active service providers like real estate agents. The right percentage depends on your production volume, time commitment, and local market rates.

Break-Even Point for S-Corp Elections

The documentation and compliance requirements above are real costs — which is why the math only works at a certain income level. Practitioner guidance generally suggests that S-Corp tax savings outweigh the added costs when net profit reaches approximately $40,000 to $60,000 annually. Below this threshold, the administrative burden and compliance expenses often exceed the SE tax savings.

Practical Trade-Offs to Consider:

- Payroll setup and ongoing processing: Running payroll every pay period, withholding FUTA/SUTA taxes, and filing quarterly 941 forms

- Separate entity tax return: S-Corps file Form 1120-S annually, adding $800-$2,000+ in tax preparation fees

- State-specific costs: Some states charge annual franchise taxes or LLC fees regardless of income

- Recordkeeping complexity: Stricter separation of personal and business finances, formal shareholder meetings, and corporate formalities

Form 2553 Filing Deadline:

S-Corp elections must generally be filed no later than 2 months and 15 days after the beginning of the tax year (March 15 for calendar-year entities). Late election relief is available under Rev. Proc. 2013-30 if reasonable cause exists, but timely filing avoids complications.

Use the $40,000-$60,000 net profit threshold as your starting point: if you're consistently above it, run the numbers with a tax professional. If you're below it, sole proprietorship or single-member LLC treatment keeps things simple while you scale.

The Top Tax Deductions 1099 Real Estate Agents Shouldn't Miss

Maximizing deductions directly reduces taxable income, lowering both self-employment and income tax. Yet many agents leave thousands on the table by failing to track eligible expenses. Use this section as a checklist to audit your own spending.

Vehicle Expenses

Agents can choose between the IRS standard mileage rate or the actual expense method. For 2026, the standard mileage rate is 72.5 cents per mile. This method is simpler and must be elected in the first year the vehicle is available for business use. Track every business mile with a contemporaneous mileage log showing the date, destination, miles driven, and business purpose.

The actual expense method allows deducting depreciation, gas, repairs, insurance, and loan interest based on the percentage of business use. For heavy vehicles with a GVWR over 6,000 lbs, this method unlocks larger first-year deductions through Section 179 or bonus depreciation.

For 2026, the Section 179 deduction limit is $2,560,000, though heavy SUVs are capped at $32,000. The One Big Beautiful Bill Act permanently restored 100% bonus depreciation for qualified property acquired after January 19, 2025, allowing immediate full expensing of the business-use portion.

Home Office Deduction

If a portion of your home is used regularly and exclusively for business, you can deduct a proportional share of rent, mortgage interest, utilities, insurance, and depreciation. The exclusive-use test is strict: the space must serve no personal function and must be your principal place of business or where you regularly meet clients.

Simplified method: $5 per square foot, up to 300 square feet (maximum $1,500 deduction). This method avoids depreciation recapture when selling your home.

Actual expense method: Calculate the percentage of your home used for business and apply that percentage to total home expenses. This method typically yields higher deductions for expensive homes or those with significant utility and maintenance costs.

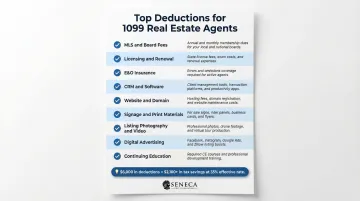

Marketing, Licensing, and Professional Costs

Deductible expenses include:

- MLS dues and board fees

- State licensing and renewal fees

- Errors & Omissions insurance

- CRM and transaction management software subscriptions

- Website hosting, design, and domain registration

- Signage, business cards, and promotional materials

- Photography and videography for listings

- Advertising on Zillow, Facebook, or other platforms

- Continuing education courses and designations

An agent spending $6,000 annually on these categories reduces taxable income by the full amount, saving $2,100+ in combined taxes at a 35% effective rate.

Health Insurance Premiums

Self-employed agents—including S-Corp shareholders owning more than 2% of the company—can deduct 100% of health, dental, and vision insurance premiums for themselves and their families as an above-the-line deduction under IRC §162(l). This deduction is disallowed for any month you're eligible to participate in a subsidized health plan maintained by your employer or your spouse's employer.

For S-Corp owners, the premiums must be paid or reimbursed by the S-Corp and reported as wages in Box 1 of the W-2 (but not subject to payroll taxes). An agent paying $800/month in premiums who overlooks this deduction leaves nearly $10,000 in above-the-line deductions unclaimed each year.

The Augusta Rule (Section 280A)

Under IRC §280A(g), if you rent your personal residence for fewer than 15 days during the taxable year, that rental income is excluded from your gross income entirely. Meanwhile, a business entity (such as your S-Corp or LLC) can deduct the rent as an ordinary and necessary expense if paid at fair market value.

How agents can use this:

- Host quarterly team meetings or annual planning retreats at your home

- Conduct client appreciation events or broker opens

- Use your property for business training sessions or strategy workshops

Essential documentation:

- Written rental agreement specifying dates, purpose, and rate

- Comparable rental rates for similar properties in your area (Airbnb, VRBO, local event venues)

- Meeting agendas, attendee lists, and photos documenting the business use

- Payment from the business entity to you at the documented fair market rate

For an agent renting their home for 10 days at $500/day, the business deducts $5,000, while you receive $5,000 tax-free—an effective $10,000 tax advantage from a single event.

Managing Quarterly Estimated Tax Payments

The IRS requires 1099 agents to prepay taxes four times per year to avoid underpayment penalties. For the 2026 tax year, the general quarterly due dates are April 15, June 15, September 15, and January 15, 2027. If a due date falls on a weekend or legal holiday, the payment is due the next business day.

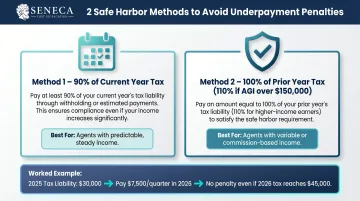

Two Safe Harbor Methods

To avoid the underpayment penalty, you must meet one of the following safe harbors:

- Pay 90% of the current year's expected tax liability, or

- Pay 100% of the prior year's total tax (110% if prior-year adjusted gross income exceeded $150,000)

Example: An agent whose 2025 tax liability was $30,000 can use the prior-year method and pay $30,000 in quarterly installments ($7,500 per quarter) throughout 2026. Even if 2026 income spikes and the actual tax liability reaches $45,000, no underpayment penalty applies—the agent simply pays the $15,000 balance when filing the return. This method provides predictability for agents with variable commission income.

The penalty is calculated based on the amount of the underpayment, the period it was underpaid, and the published quarterly interest rate. For Q1 2026, the underpayment interest rate is 7%, meaning underpayments compound quickly over multiple quarters.

Practical Cash-Flow Tip

Those compounding penalties make proactive saving non-negotiable. Set aside a fixed percentage of every commission check into a dedicated tax savings account the moment it clears.

Most tax professionals recommend setting aside 25%–35% of net income to cover federal and state liabilities. That range accounts for self-employment tax (15.3%) plus income tax (10%–37% depending on your bracket).

When it's time to pay, note that the IRS is phasing out legacy options:

- IRS Direct Pay — free, no enrollment required, pay directly from a bank account

- IRS Online Account — the replacement for EFTPS as of late 2025; individual EFTPS enrollments have sunsetted

- Check irs.gov for the most current payment options, as the transition continues through 2026

Retirement Contributions as a Tax Strategy

For self-employed agents, retirement accounts are one of the most powerful tools available — contributions reduce taxable income now while building long-term wealth. Two options are worth knowing in detail.

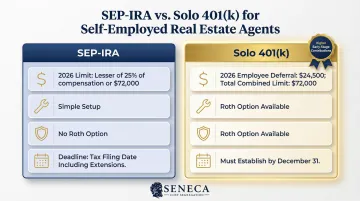

SEP-IRA

For 2026, the maximum contribution to a SEP-IRA is the lesser of 25% of compensation or $72,000. Contributions are made pre-tax, directly reducing taxable income, and can be made as late as the tax filing deadline including extensions—giving agents flexibility to assess their year-end tax position before committing funds.

Example: An agent with $150,000 in net self-employment income can contribute up to $37,500 to a SEP-IRA (25% of net SE income after the SE tax deduction). This contribution reduces taxable income by $37,500, saving roughly $13,125 in taxes at a 35% effective rate.

Solo 401(k)

Agents operating without employees can open a Solo 401(k), which allows both an employee contribution and an employer contribution. For 2026, the employee elective deferral limit is $24,500, and the total combined contribution limit is $72,000.

Solo 401(k) advantages over a SEP-IRA:

- Enables higher total contributions at the same income level — the employee deferral is calculated on gross income, not net SE income

- Higher deferral ceiling than SEP-IRA alone

- Roth option available for post-tax contributions with tax-free withdrawals in retirement

Setup deadline: Solo 401(k) plans must be established by December 31 of the tax year, though contributions can be made until the tax filing deadline (including extensions).

Hire Your Children Strategy

Agents operating as sole proprietors or single-member LLCs can employ their minor children for legitimate, age-appropriate tasks, such as:

- Social media posting and content organization

- Filing, scheduling, and administrative support

- Data entry or photography assistance

Payments to a child under age 18 are exempt from Social Security and Medicare (FICA) taxes — a meaningful savings on top of the wage deduction.

For 2026, the standard deduction for a dependent child is limited to the greater of $1,350 or the individual's earned income plus $450 (up to the regular standard deduction). By paying your child up to the standard deduction limit, the wages are a deductible business expense for you and tax-free income for the child.

Requirements: The work must be legitimate, age-appropriate, and compensated at reasonable market rates. Maintain timesheets, job descriptions, and payment records to support the deduction if audited.

How Owning Investment Property Amplifies Your Tax Savings

Many real estate agents leverage their market expertise to invest in rental properties—and ownership opens an entirely different layer of tax benefits that can dwarf the deductions available from your 1099 business alone. The key advantage is depreciation: a non-cash deduction that can create "paper losses" offsetting other income.

Real Estate Professional Status (REPS)

Rental activities are generally passive under IRS rules, meaning losses cannot offset active commission income. However, agents who spend more than 750 hours annually in real property trades or businesses and meet the "more than half your working time" test may qualify for Real Estate Professional Status (REPS).

Why REPS matters: Qualifying allows rental property losses to offset active 1099 commission income rather than being trapped as passive losses subject to the $25,000 special allowance (which phases out for MAGI between $100,000 and $150,000).

How active agents qualify: Brokerage and agent activities count toward the REPS tests. If you're already logging 1,500+ hours annually in licensed real estate activities (showing properties, marketing listings, negotiating contracts), you naturally meet the 750-hour threshold. The "more than half" test requires that real estate activities constitute more than 50% of your total working time across all trades or businesses during the year.

Documentation is critical: Maintain contemporaneous time logs tracking hours spent in real estate activities and hours spent in any other business. Detailed calendars, appointment records, and activity logs are highly recommended to survive audit scrutiny.

Cost Segregation: The Tool to Maximize Depreciation

Standard residential rental property depreciation spreads a property's cost over 27.5 years under MACRS. For a $500,000 building (excluding land), annual depreciation is roughly $18,182. Cost segregation accelerates this timeline by identifying building components that qualify for shorter depreciation periods.

How it works: A cost segregation study, guided by Rev. Proc. 87-56 class lives, reclassifies components into 5-year, 7-year, or 15-year property. Common reclassified items include:

- Flooring and fixtures

- Landscaping and site improvements

- Electrical systems and HVAC

- Appliances and specialty components

For residential rentals, typical reclassification percentages range from 20% to 40% of total building cost.

Bonus depreciation multiplier: The One Big Beautiful Bill Act restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. This allows reclassified 5-year, 7-year, and 15-year assets to be fully expensed in year one, front-loading deductions into early years when they have the most impact.

Example: An agent buys a $600,000 rental property ($500,000 building, $100,000 land). A cost segregation study identifies $200,000 in 5-year and 15-year assets eligible for 100% bonus depreciation. The first-year depreciation jumps from $18,182 (standard) to $218,182 (with cost segregation and bonus depreciation). For an agent in the 35% effective tax bracket who qualifies for REPS, that $200,000 increase in deductions translates to $70,000 in immediate tax savings.

Seneca Cost Segregation has completed over 10,200 studies nationwide, with an average first-year deduction of $171,243 across completed studies. Every analysis follows IRS guidelines and includes an AuditDefense guarantee — with a money-back promise if a material issue arises. For agents who own investment properties, Seneca's engineering-based studies are delivered in 2-4 weeks with full IRS compliance documentation.

The 1031 Exchange

When an agent sells an investment property, a 1031 like-kind exchange lets you defer capital gains taxes by rolling proceeds into a replacement property. Taxpayers must identify replacement property within 45 days of transferring the relinquished property and complete the acquisition within 180 days.

Why this matters for high-income agents: In upper tax brackets (where long-term capital gains are taxed at 15-20% plus the 3.8% net investment income tax), a 1031 exchange defers a tax bill that could otherwise reach 23.8%. For a $300,000 gain, deferring taxes preserves $71,400 for reinvestment — compounding wealth over multiple property cycles.

Frequently Asked Questions

How to pay less taxes as a 1099 contractor?

The most impactful moves are electing S-Corp taxation to reduce self-employment tax once net profit exceeds $40,000–$60,000, maximizing deductions (home office, vehicle, health insurance, retirement contributions), and making quarterly estimated payments to avoid penalties. A CPA familiar with real estate can pinpoint which combination applies to your situation.

What is the 80/20 rule for realtors?

In real estate, the 80/20 rule means roughly 20% of agents close 80% of total sales volume. From a tax standpoint, those top producers in higher brackets have the most to gain from advanced strategies like S-Corp elections and cost segregation studies on investment properties.

Do 1099 real estate agents need to pay quarterly estimated taxes?

Yes, the IRS requires self-employed agents to pay estimated taxes four times per year (April, June, September, and January). Failing to do so can result in underpayment penalties and interest even if you pay the full balance when filing your return.

What is the best business structure for a 1099 real estate agent?

For newer or lower-income agents, a sole proprietorship or single-member LLC is the simplest starting point. An S-Corp election typically makes sense once net commissions consistently exceed $40,000–$60,000 per year, when the SE tax savings outweigh the added compliance costs.

Can a 1099 real estate agent deduct vehicle expenses?

Yes, agents can deduct vehicle expenses using either the standard mileage rate (70 cents per mile for 2025 — verify the current rate annually with the IRS) or actual expenses (depreciation, gas, repairs, insurance). Heavy vehicles over 6,000 lbs GVWR may qualify for accelerated depreciation under Section 179 or bonus depreciation—but you must maintain a contemporaneous mileage log to support the deduction.

Can real estate agents qualify for Real Estate Professional Status (REPS)?

Yes, active agents are often well-positioned to qualify for REPS because their licensed real estate activities count toward the 750-hour threshold. Qualifying allows rental property losses to offset commission income, making property ownership even more tax-efficient. Keep detailed time logs to document your hours — you'll need them to satisfy both the material participation test and the requirement that real estate activities make up more than half your working time.