Introduction

Short-term rental owners face a critical challenge: how to offset the significant tax burden that comes with rental income while managing high upfront investment costs. Many STR investors struggle to find tax strategies powerful enough to reduce their taxable income meaningfully, especially when their rental generates strong cash flow.

Cost segregation offers a solution specifically designed for this problem. It's an IRS-compliant tax strategy that allows STR owners to reclassify property components (flooring, appliances, landscaping, hot tubs) for accelerated depreciation, dramatically reducing taxable income in the early years of ownership when cash flow matters most.

While cost segregation is widely used in commercial real estate, STR owners have access to a unique additional benefit: the ability to offset active income like W-2 wages, not just passive rental income.

Under Treasury Regulation §1.469-1T(e)(3)(ii)(A), properties with average guest stays of seven days or fewer qualify as active business activity under IRS rules. That distinction makes this strategy particularly powerful for high earners.

This guide covers everything you need to apply cost segregation to your STR property — from how the mechanics work to the specific rules that determine whether you qualify.

TL;DR

- Cost segregation reclassifies STR components (furniture, appliances, landscaping) into 5, 7, or 15-year depreciation schedules instead of 39 years

- The "Seven-Day Rule" classifies STRs with average stays of 7 days or fewer as active business activity, unlocking loss deductions unavailable to passive rental owners

- Owners must meet IRS material participation requirements (typically 100+ hours annually) to offset W-2 wages with STR losses

- 100% bonus depreciation applies to property acquired and placed in service on or after January 19, 2025; for property acquired before January 19, 2025, the TCJA phase-down remains in effect, with average first-year deductions reaching $171,243

- A properly documented cost segregation study is your first line of defense if the IRS audits your depreciation claims

What Is Cost Segregation for Short-Term Rentals?

Cost segregation is an IRS-compliant, engineering-based tax study that reclassifies a property's components into shorter depreciation categories (5-year, 7-year, and 15-year) instead of treating the entire building as a single 39-year asset.

This accelerates when you claim deductions, reducing taxable income when cash flow matters most and freeing up capital for reinvestment or property improvements.

How It Differs from Standard Depreciation:

Standard depreciation spreads deductions evenly across decades. If you purchase a $750,000 STR property with a $600,000 building basis (excluding land), standard depreciation gives you roughly $15,385 annually over 39 years.

This approach accelerates depreciation by identifying and separating:

- Furniture, appliances, specialty fixtures, window treatments, and decorative lighting (5-year personal property)

- Patios, landscaping, parking areas, fencing, and outdoor entertainment features (15-year land improvements)

- Structural components that stay on the standard 39-year building schedule

By reclassifying 20-35% of the building value into faster depreciation schedules, you can generate $60,000-$150,000+ in first-year deductions instead of $15,000. Combined with bonus depreciation, this front-loading effect is especially powerful for STR owners who qualify for active participation treatment.

Why STRs Have a Unique Tax Advantage: The Seven-Day Rule

Short-term rentals operate under completely different tax rules than traditional long-term rentals. This distinction is what allows high-income earners to bypass the passive activity loss limitations that normally restrict rental property deductions.

The Seven-Day Rule Exception

Under normal IRS rules, rental income is passive. This means depreciation losses can only offset other passive income, not wages, business profits, or self-employment income.

Short-term rentals break this rule under a specific IRS exception. Treasury Regulation §1.469-1T(e)(3)(ii)(A) states that an activity is not a rental activity if "the average period of customer use for such property is seven days or less."

Once an STR qualifies as active business activity—similar to operating a hotel—depreciation losses from cost segregation can offset W-2 wages, self-employment income, and business profits directly. This is the core of what's commonly called the "short-term rental loophole."

The 39-Year Depreciation Problem for STRs

Here's a misconception many STR owners and even some CPAs get wrong: most short-term rentals are not depreciated over 27.5 years like long-term residential rentals.

Under IRC §168(e)(2)(A) and IRS Publication 946, the 27.5-year schedule only applies if 80%+ of gross rental income comes from dwelling units—and the statute explicitly excludes transient-use properties like hotels. Because most STRs have average guest stays under 30 days, they fall into that transient category.

That classification puts STRs in nonresidential real property territory, depreciated over 39 years, the same schedule as hotels and office buildings.

Reclassifying 20–35% of property components into 5, 7, or 15-year assets through cost segregation directly offsets this slower base depreciation rate, making the strategy particularly impactful for STR owners.

Bonus Depreciation Amplifies the Seven-Day Rule Benefit

When components are reclassified through cost segregation, they qualify for bonus depreciation—meaning immediate, full expensing in year one rather than spreading deductions across decades. The rate you can claim depends on when the property was placed in service.

The One, Big, Beautiful Bill Act (OBBBA) restored 100% bonus depreciation for qualified property acquired and placed in service on or after January 19, 2025, per IRS Notice 2026-11. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline:

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | — |

| January 1, 2023 – December 31, 2023 | 80% | — |

| January 1, 2024 – December 31, 2024 | 60% | — |

| January 1, 2025 – January 18, 2025 | 40% | — |

| January 19, 2025 – December 31, 2030 | 100% | Acquisition date must be January 19, 2025 or later |

| 2025 (if acquired before January 19, 2025) | 40% | TCJA phase-down applies |

| 2026 (if acquired before January 19, 2025) | 20% | TCJA phase-down applies |

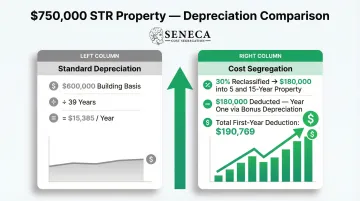

Illustrative Example: The Combined Impact

Consider a $750,000 STR property purchase with $150,000 allocated to land and $600,000 to the building.

Standard depreciation approach:

- Annual deduction: $600,000 ÷ 39 years = $15,385

Cost segregation approach:

- Engineering study identifies 30% ($180,000) as 5-year and 15-year property

- With 100% bonus depreciation: $180,000 deducted in year one

- Remaining $420,000 depreciated over 39 years: $10,769 annually

- Total first-year deduction: $190,769

At a 35% effective tax rate, this generates approximately $66,769 in first-year tax savings compared to $5,385 under standard depreciation, a difference of $61,384.

Note: Individual results vary based on property composition, tax bracket, and specific circumstances. Consult your tax advisor for property-specific projections.

How a Cost Segregation Study Works for STR Properties

A qualified cost segregation firm conducts an engineering-based analysis of the property, separates assets into appropriate depreciation classes, and produces an IRS-compliant report filed with your tax return.

Studies on existing properties (look-back studies) can capture missed deductions from prior years without amending returns, using IRS Form 3115 to claim a catch-up adjustment in the current year.

Step 1: Property Analysis and Asset Identification

The process begins with a detailed engineering review of the property, including blueprints, purchase documents, and a site inspection to identify every depreciable component.

For STRs, this includes:

- Structural shell: Building frame, roof, windows, primary HVAC, plumbing

- Personal property: Furniture, appliances, specialty lighting, hot tubs, decorative fixtures, window treatments, kitchenware

- Land improvements: Decking, patios, landscaping, driveways, fencing, outdoor entertainment features

The IRS Cost Segregation Audit Techniques Guide strongly emphasizes the necessity of site visits, stating that quality studies "include a site visit, as well as photographic evidence, to assist in identifying the assets and in determining the allocations of values or costs."

The thoroughness of this step directly determines the size of your deduction. STR properties with elaborate furnishings, hot tubs, and outdoor amenities often yield particularly strong results, typically reclassifying 25–35% of building value.

Step 2: Reclassification and Depreciation Assignment

Each identified component is assigned to its appropriate depreciation class based on IRS asset classification rules:

| Asset Class | STR Examples | Recovery Period |

|---|---|---|

| 5-Year Property | Appliances, carpeting, furniture, window treatments, decorative lighting, hot tubs | 5 years |

| 7-Year Property | Readily removable interior walls, certain office equipment | 7 years |

| 15-Year Property | Paving, parking lots, landscaping, fences, patios, decks, site lighting | 15 years |

| 39-Year Property | Building shell, roof, windows, primary HVAC, structural components | 39 years |

STR-specific assets like guest amenity packages, high-turnover furnishings, and outdoor entertainment features often qualify for the shortest recovery periods.

An engineering-based approach produces more defensible reclassifications than a purely accountant-driven percentage allocation. The IRS makes this explicit: "a study by a construction engineer is more reliable than one conducted by someone with no engineering or construction background."

Seneca Cost Segregation's process follows all 13 quality elements outlined in the IRS Audit Techniques Guide, with an AuditDefense guarantee that includes representation at no additional charge and a money-back guarantee if a material issue arises.

Step 3: Filing and Realizing the Deduction

The completed study is delivered to you and your CPA, who incorporates the accelerated depreciation schedule into your tax return. The study should be completed in the same tax year you want to claim the deduction, ideally the same year you materially participate.

Seneca typically delivers studies within 2–4 weeks, making tax-year timing feasible even late in Q4. Across more than 10,200 completed studies nationwide, clients have achieved an average first-year deduction of $171,243.

Material Participation: The Key to Unlocking Non-Passive Losses

The Seven-Day Rule alone does not guarantee active loss treatment. You must also meet at least one of the IRS's material participation tests in the tax year you want to claim the deduction.

Without meeting a material participation test, losses remain passive and can only offset passive income, severely limiting the tax benefit.

The Most Commonly Used Material Participation Tests

According to IRS Publication 925 and Treasury Regulation §1.469-5T, here are the three tests most accessible for STR owners:

| Test | Requirement | Best For | Notes |

|---|---|---|---|

| Test 1: 500-Hour Test | You participate more than 500 hours during the year | Self-managed portfolios or full-time STR operators | Requires approximately 10 hours per week |

| Test 2: Substantially All Participation | Your participation constitutes "substantially all" of the participation by all individuals | Solo operators who handle their own cleaning and maintenance | Fails if you use cleaners or contractors heavily |

| Test 3: 100-Hour / No One More Test | You participate more than 100 hours during the year AND no other individual (including employees) participates more than you | Most common test for STR owners | Requires tracking your hours AND ensuring cleaners, handymen, or managers don't exceed your participation |

What Counts as Qualifying Participation

According to IRS Publication 925, work done in the capacity of an "investor" does not count toward material participation unless you're directly involved in day-to-day management.

| Counts Toward Material Participation | Does NOT Count |

|---|---|

| Guest communication and inquiry responses | Studying financial statements |

| Managing bookings and reservations | Preparing summaries for personal use |

| Coordinating cleaners and maintenance | Monitoring finances in a non-managerial capacity |

| Performing repairs and maintenance yourself | Work done solely to avoid passive loss disallowance |

| Purchasing supplies and amenities | |

| Dynamic pricing management | |

| Property inspections |

Critical documentation requirement: Contemporaneous time logs documenting qualifying tasks are essential documentation. The Tax Court in Pohoski v. Commissioner ruled against taxpayers who could not prove their hours exceeded those of their third-party property managers.

The Joint-Filing Strategy

Married couples filing jointly have a distinct advantage. Under Treasury Regulation §1.469-5T(f)(3), any participation by a spouse counts as participation by the taxpayer, regardless of whether the spouse owns an interest in the activity.

This means cost segregation deductions can reduce the household's combined taxable income even if only one spouse actively manages the STR.

For example: one spouse holds a high-paying W-2 job while the other manages the STR for 100+ hours annually. The couple can use STR losses to offset that W-2 income directly.

Material Participation vs. Real Estate Professional Status

The STR Seven-Day Rule + material participation path is entirely separate from Real Estate Professional Status (REPS) under IRC §469(c)(7).

| Criteria | REPS Requirements | STR Material Participation |

|---|---|---|

| Hours | More than 750 hours in real property trades or businesses | Only 100+ hours required (with no one participating more) |

| Services | More than half of all personal services in real property activities | No requirement that real estate be your main occupation |

| Accessibility | Harder to qualify unless real estate is your primary occupation | Accessible for high-income earners with primary careers |

For most W-2 earners, REPS is out of reach — but the 100-hour material participation test is not. If you're actively managing your STR and keeping time logs, you may already qualify to unlock non-passive loss treatment this tax year.

Common Misconceptions and Pitfalls

Misconception 1: "My STR depreciates over 27.5 years like a regular rental"

Reality: Most STR properties with average stays under 30 days are classified as 39-year nonresidential property under the IRS's transient use rule, not 27.5-year residential rental property.

According to IRC §168(e)(2)(A), the definition of "residential rental property" explicitly excludes "a unit in a hotel, motel, or other establishment more than one-half of the units in which are used on a transient basis."

Many tax professionals get this wrong, which affects the accuracy of depreciation calculations and the strategy's expected benefit. A CPA experienced in STR taxation can verify the property's classification.

Misconception 2: "Cost segregation is only for large commercial properties"

Reality: Any STR property with sufficient depreciable basis can benefit from a study. Industry consensus suggests properties with depreciable basis (excluding land) of $500,000–$750,000 or more justify the engineering fees.

That said, STR properties often carry a disproportionately high share of fast-depreciating assets compared to long-term rentals. A beachfront vacation home with elaborate furnishings, hot tubs, outdoor kitchens, and specialty lighting may reclassify 30–35% of building value, making the strategy worthwhile even for properties that seem modestly sized.

According to the American Society of Cost Segregation Professionals, typical studies reclassify 15–30% of a building's depreciable basis into shorter tax categories, with returns on investment typically ranging from 10–25:1.

Misconception 3: "I can skip material participation because I hired a property manager"

Delegating day-to-day tasks to a property manager does not satisfy material participation requirements.

Under Treasury Regulation §1.469-5T(b)(2)(ii), management activities do not count if another person receives compensation for managing the activity or spends more hours managing it than you do. If you use a full-service property manager who handles guest communication, cleaning coordination, and maintenance, they will almost certainly exceed your participation hours, which disqualifies you from the 100-hour test.

The property manager trap: In Pohoski v. Commissioner, the Tax Court ruled against taxpayers claiming the 100-hour test because they failed to introduce evidence of the actual time spent by their third-party property management company.

Solution: If you use a property manager, you must either:

- Participate more than 500 hours yourself (Test 1), OR

- Track both your hours and the manager's hours to prove you participate more (Test 3), OR

- Qualify under Real Estate Professional Status

Without meeting one of these thresholds, STR losses cannot offset active income. Courts have rejected claims where investors could not produce contemporaneous time records.

Frequently Asked Questions

Can you cost segregate a short-term rental?

Yes, any STR property placed in service for rental income is eligible for a cost segregation study. STRs often yield particularly strong results due to their higher proportion of personal property (furniture, appliances, hot tubs) and land improvements (patios, landscaping, outdoor entertainment features) that qualify for accelerated depreciation, typically reclassifying 25-35% of building value.

Do short-term rentals depreciate over 27.5 or 39 years?

Most STRs with average guest stays under 30 days are classified as 39-year nonresidential property under the IRS's transient use rule, not 27.5-year residential rental property. This classification makes cost segregation even more valuable, as reclassifying components into 5, 7, and 15-year schedules provides greater acceleration compared to the slower 39-year baseline.

What is the 80/20 rule for Airbnb?

The 80/20 rule refers to IRC §168(e)(2)(A), which states that a building qualifies as "residential rental property" (27.5-year depreciation) only if 80% or more of its gross rental income comes from dwelling units. However, properties used on a transient basis (average stays under 30 days) are excluded from this definition, which is why most STRs default to 39-year depreciation regardless of this threshold.

What is the 75-55 rule for Airbnb?

The "75-55 rule" is an internet myth with no basis in the IRS tax code. It's likely a misreading of IRC §280A, which limits rental deductions when personal use exceeds 14 days or 10% of rental days, and excludes properties rented fewer than 15 days annually from claiming any rental deductions.

How much can I save with a cost segregation study on my short-term rental?

Savings depend on property value, asset composition, tax bracket, and bonus depreciation eligibility. Seneca's clients average a $171,243 first-year deduction, with typical ROI of 10-25:1. On a $750,000 STR, first-year savings often reach $50,000-$75,000 or more. Request a free assessment at senecacostseg.com or call 530-797-6539 for a property-specific estimate.