Material participation determines whether rental losses are "active" and immediately deductible or "passive" and trapped behind IRS barriers. For investors who've commissioned cost segregation studies that reclassify 20–40% or more of their property's cost into accelerated depreciation, understanding this distinction isn't academic—it's the difference between unlocking $100,000+ in immediate tax savings and watching those deductions sit idle for years.

The stakes doubled in 2013 when the 3.8% Net Investment Income Tax (NIIT) took effect, adding another layer of tax exposure to passive rental income. Establishing material participation isn't just about deducting losses—it's also about avoiding an additional surtax on rental profits.

TLDR

- Material participation requires regular, continuous, substantial involvement in your rental activity, measured by seven IRS tests

- Rentals are passive by default; only material participation or Real Estate Professional status unlocks losses against W-2 and business income

- Without material participation, cost segregation losses are suspended until you generate passive income or sell the property

- The IRS and Tax Court routinely reject retroactive hour logs, particularly from full-time W-2 employees claiming real estate professional status

What Is Material Participation in Real Estate and Why It Matters

Material participation is a legal standard under IRC Section 469 requiring involvement in a rental or business activity on a "regular, continuous, and substantial basis." This isn't subjective—the IRS defines seven specific tests, and you must satisfy at least one.

The Passive Activity Loss Trap

Under Section 469, rental activities are presumed passive by default, regardless of how actively involved you are. This means rental losses can only offset other passive income—not your W-2 wages, not your business income, not any "active" earnings.

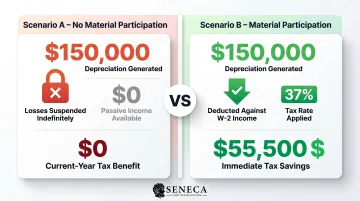

Scenario A (No Material Participation): You complete a cost segregation study that generates $150,000 in first-year depreciation. You have no other passive income. Result: The entire $150,000 loss is suspended and carries forward to future years. Current-year tax benefit: $0.

Scenario B (With Material Participation): Same $150,000 depreciation deduction. You've established material participation (or Real Estate Professional Status + material participation). Result: You immediately deduct the full $150,000 against your W-2 income. At a 37% tax rate, that's $55,500 in immediate tax savings.

Three Levels of Participation

The IRS recognizes three tiers:

- Passive: No meaningful involvement; losses suspended

- Active: Making management decisions, but still subject to passive loss rules (with limited $25,000 allowance)

- Material: Highest standard; converts rental losses to fully deductible non-passive losses

Reaching the material participation tier doesn't just unlock loss deductions—it also affects how your rental income is taxed.

The NIIT Factor

Since 2013, the 3.8% Net Investment Income Tax applies to passive rental income for taxpayers above certain income thresholds. Establishing material participation exempts rental income from this surtax under Treasury Reg. §1.1411-4(g)(7), which provides a safe harbor for real estate professionals who participate more than 500 hours per year.

The 7 IRS Material Participation Tests

You need to satisfy only ONE of seven tests to establish material participation for the year. Each test has specific thresholds and documentation requirements.

Test 1: The 500-Hour Test

You participate in the activity for more than 500 hours during the tax year — roughly 10 hours per week for 50 weeks.

This is the most common and defensible path. Qualifying activities include:

- Tenant screening and lease negotiations

- Property inspections and maintenance coordination

- Financial management and bookkeeping

- Coordinating repairs and renovation oversight

- Vendor management and contract negotiations

- Marketing and advertising vacant units

Example: An investor with three single-family rentals spends 6 hours per week on property management tasks (responding to tenant requests, coordinating repairs, reviewing financials, conducting quarterly inspections). Over 50 weeks, that's 300 hours — falling short of Test 1. Add renovation oversight on one property (an extra 5 hours per week for 40 weeks = 200 hours) and they reach 500 hours total and qualify.

Tests 2 and 3: Substantially All Participation and the 100-Hour Threshold

Test 2 requires that your participation constitutes substantially all participation in the activity by all individuals, including non-owners.

Test 3 requires that you participated more than 100 hours AND at least as much as any other individual.

Test 3 is particularly useful for co-owned properties or when using a property manager. Your hours must equal or exceed those of any other individual — including the property manager.

Planning tip: If your property manager logs 120 hours annually handling routine maintenance calls and rent collection, but you log 125 hours managing renovations, approving capital expenditures, and handling lease negotiations, you satisfy Test 3.

Test 4: Prior 5-Year Aggregate Participation

You participated in the activity for more than 500 hours in aggregate during any 5 of the 10 preceding tax years. The years don't need to be consecutive.

This test is valuable for investors who ramped up involvement early in a property's life — even if current-year hours have declined, prior participation history can carry the qualification.

Tests 5 and 6: Historical Participation Safe Harbors

Test 5 applies if you materially participated in the activity for any 5 of the preceding 10 tax years. Test 6 applies if you materially participated in a personal service activity for any 3 prior years.

Both tests give investors flexibility when participation history is already established. Once you satisfy Test 5, you're deemed to materially participate even if current-year hours drop below 500.

Strategic application: Investors who materially participated during property renovations or initial lease-up can benefit from Test 5 even after transitioning to lighter management roles.

Test 7: Facts and Circumstances (Most Restrictive)

You participated on a regular, continuous, and substantial basis — with a 100-hour minimum floor.

Critical restriction: Management activities don't count if any other person was compensated to manage the activity or spent more management hours than you.

This makes Test 7 nearly impossible for investors using professional property managers. Courts have consistently rejected Test 7 claims when property managers are involved — making Test 1 the far stronger option for most investors.

Spousal Participation Rule

Under IRS Temporary Regulations, hours performed by a spouse count toward material participation — even if the spouse has no ownership interest in the property. This applies regardless of whether you file jointly or separately.

Planning opportunity: If you log 300 hours and your spouse logs 250 hours managing the same rental activity, your combined 550 hours satisfy Test 1.

Material Participation vs. Active Participation

Most rental property owners default to active participation — but understanding how it differs from material participation determines whether your losses are capped or fully deductible.

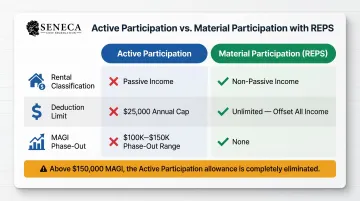

Active participation is a lower standard than material participation, but it comes with strict limits.

Active Participation Requirements

- Own at least 10% of the rental property

- Make bona fide management decisions (approve tenants, set lease terms, authorize repairs)

- Cannot be a limited partner

- No specific hour requirement

The $25,000 Loss Allowance

The benefit: IRC §469(i) allows up to $25,000 of rental losses to offset non-passive income for taxpayers who actively participate.

The catch: This allowance phases out completely between $100,000 and $150,000 in Modified Adjusted Gross Income (MAGI). For every $2 above $100,000, you lose $1 of the allowance. At $150,000 MAGI, the benefit disappears entirely.

Direct Comparison

| Standard | Rental Classification | Deduction Limit | MAGI Phase-Out |

|---|---|---|---|

| Active Participation | Remains passive | Up to $25,000 annually | $100K–$150K |

| Material Participation + REPS | Non-passive | Unlimited against all income | None |

Active participation limits deductions to $25,000 — and phases that out entirely above $150,000 MAGI. Material participation combined with Real Estate Professional Status removes the passive classification altogether, making losses fully deductible against any income with no cap.

Real Estate Professional Status (REPS) and Material Participation

This is where most investors get tripped up: Qualifying as a Real Estate Professional does NOT automatically make rental losses non-passive. REPS only removes the statutory presumption that rentals are passive. You must also materially participate in each rental activity.

The Two REPS Tests

To qualify as a Real Estate Professional under IRC §469(c)(7), you must satisfy both:

- More than 50% test: More than half of all personal services performed during the year are in real property trades or businesses in which you materially participate

- 750-hour test: You perform more than 750 hours in those real property trades or businesses

Hours as an employee don't count unless you own more than 5% of the employer.

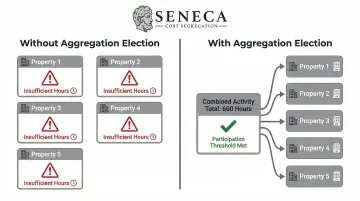

The Aggregation Election: Critical for Multiple Properties

Treasury Reg. §1.469-9(g) allows qualifying real estate professionals to elect to treat all rental real estate interests as a single activity for material participation purposes. For investors with multiple properties, this election is often the difference between qualifying and not.

Without aggregation, you must prove material participation separately for each rental property — meaning five properties could require hundreds of documented hours per property. With the aggregation election, hours combine across all properties. Your 600 total hours across five properties satisfy the material participation threshold for the aggregated activity.

Filing requirements:

- Must be formally filed with your original tax return

- Binding for all future years

- Can be made late under Rev. Proc. 2011-34

- Has specific implications when you dispose of individual properties

REPS for Married Couples

Only the hours of the spouse seeking REPS status count toward the 750-hour and more-than-half tests — you cannot combine spousal hours to qualify for REPS itself. Once one spouse qualifies, however, both spouses' hours can be combined to establish material participation in the underlying rental activities.

Example:

- Spouse A works full-time in software (2,000 hours) and logs 200 real estate hours

- Spouse B works part-time in real estate, logging 900 professional hours plus 500 hours managing the couple's rentals

Result: Spouse B qualifies for REPS (900 real estate hours > 750, and more than half of 1,400 total personal service hours). The couple can then combine both spouses' rental management hours (200 + 500 = 700 hours) to establish material participation in their aggregated rental activity.

Material Participation and Cost Segregation Depreciation

Cost segregation studies reclassify building components into 5-, 7-, and 15-year property classes, creating front-loaded depreciation. According to the IRS Cost Segregation Audit Techniques Guide, this typically accelerates 20–40% or more of a commercial property's depreciable basis.

The catch: those accelerated deductions generate rental losses, which are subject to passive activity loss rules.

The Unlock Scenario

Without Material Participation:

- Cost segregation study generates $200,000 in first-year depreciation

- You have $50,000 in W-2 income and no other passive income

- Result: The $200,000 loss is suspended under IRC §469(b)

- Losses carry forward until you generate passive income or dispose of the property

With Material Participation (or REPS + Material Participation):

- Same $200,000 depreciation deduction

- You've established REPS and materially participate in the rental

- You immediately apply the $200,000 loss against your W-2 income — at 37% federal rate, that's $74,000 in current-year tax savings

Real-World Impact

Seneca Cost Segregation's completed studies average a $171,243 first-year deduction. For investors who've confirmed material participation status before commissioning the study, this means immediate access to the full tax benefit — rather than waiting years for suspended losses to free up.

That timing distinction matters more than most investors realize. Evaluating your participation status before ordering a study determines whether those deductions work for you now or sit idle.

Strategic timing: If you can't establish material participation in the current year, consider:

- Increasing your involvement to meet the 500-hour test

- Coordinating with your spouse to combine hours

- Timing the study for a year when you qualify for REPS

Documenting Your Material Participation

The IRS doesn't require contemporaneous daily time logs, but the burden of proof is on you. Treasury Reg. §1.469-5T(f)(4) states that taxpayers may use "reasonable means" including appointment books, calendars, email trails, and narrative summaries.

Critical reality: Courts consistently reject retroactive "ballpark guesstimates" unsupported by contemporaneous evidence.

Case Law Lessons

Claims that failed:

Moss v. Commissioner (135 T.C. 365, 2010) — Post-audit guesstimates ruled insufficient; counting "on call" hours also rejected.

Hassanipour v. Commissioner (T.C. Memo 2013-88) — A full-time W-2 employee (1,936 employer-logged hours) claimed only 32–35 hours per week in real estate to satisfy the REPS 50% test. The court called his reconstructed calendar "not credible" and "inherently improbable."

Pourmirzaie v. Commissioner (T.C. Memo 2018-26) — No records kept; hours reconstructed from memory after an exam notice arrived. The court rejected the reconstruction and imposed a 20% accuracy-related penalty.

A claim that barely survived:

- Birdsong v. Commissioner (T.C. Memo 2018-148) — No contemporaneous logs, but detailed spreadsheets, receipts, and invoices backed credible testimony. The court accepted it as "reasonable means" while explicitly cautioning the taxpayers to keep strictly contemporaneous records going forward.

Actionable Documentation Strategy

Maintain a running log throughout the year:

- Date of activity

- Specific task description

- Property identifier (if multiple rentals)

- Exact hours spent

Supplement with corroborating evidence:

- Email timestamps with tenants and contractors

- Contractor bids and invoices

- Inspection notes and photos

- Lease documents and tenant applications

- Travel records for property visits

- Calendar entries and appointment confirmations

Special scrutiny for W-2 employees: The IRS closely scrutinizes taxpayers who work full-time in non-real estate roles yet claim they spent more hours on real estate. If you're claiming REPS while working a 40-hour-per-week job, your documentation must be thorough, contemporaneous, and verifiable.

Frequently Asked Questions

What is considered material participation in real estate?

Material participation means involvement in a real estate activity on a regular, continuous, and substantial basis as defined by one of seven IRS tests. The most common is the 500-hour test: participating more than 500 hours in the activity during the tax year.

What is the 100 hour rule for material participation?

The 100-hour threshold appears in Test 3: you must participate more than 100 hours AND at least as much as any other individual involved in the activity, including non-owners like property managers. This test applies when multiple people contribute hours — it rewards the investor who's most hands-on, even without crossing the 500-hour mark.

What happens if you don't materially participate?

Without material participation, rental losses, including depreciation deductions from cost segregation, are classified as passive and can only offset other passive income. Excess losses are suspended and carried forward until you generate passive income or sell the property, potentially delaying tax benefits for years.

Can I materially participate if I use a property manager?

Yes, but it's harder. Using a property manager doesn't automatically prevent material participation, but under Test 3, your hours must equal or exceed those of any other individual. If the manager logs more hours, you must rely on Test 1 (500+ hours) or another qualifying test instead.

Does my spouse's participation count toward material participation?

Yes. Under IRS regulations, a spouse's participation counts toward the owner's material participation, even if the spouse has no ownership interest and you file separately.

How does material participation affect cost segregation deductions?

Material participation, or Real Estate Professional Status (REPS) combined with material participation, allows accelerated depreciation from a cost segregation study to offset ordinary income immediately. Without it, those losses are passive and suspended, significantly delaying the tax benefit.