This guide covers what capital gains tax on investment property actually means, how it's calculated (including the often-overlooked depreciation recapture), the current rate brackets, and the legitimate strategies investors use to reduce or defer what they owe. It's written for rental property owners, multi-family investors, commercial real estate holders, and short-term rental operators who want to make informed decisions before selling.

TLDR: Capital Gains Tax on Investment Property at a Glance

- Profits from selling investment property are taxed as short-term gains (up to 37%) or long-term gains (0%, 15%, or 20%) depending on your hold period and income

- Your taxable gain is based on adjusted cost basis (not just purchase price), so improvements and depreciation both affect what you owe

- Depreciation recapture is taxed separately at up to 25%, and is often the most overlooked part of the tax bill

- High earners face an extra 3.8% Net Investment Income Tax on top of standard capital gains rates

- Legal deferral options include 1031 exchanges, opportunity zone investments, and installment sales

What Is Capital Gains Tax on Investment Property?

Capital gains tax is the tax owed on the profit made when selling a capital asset, in this case an investment property. The IRS treats investment properties (rentals, multi-family, commercial, short-term rentals) differently from primary residences for tax purposes.

Two holding periods determine your tax rate:

- Short-term gains (property held under one year): taxed as ordinary income at rates up to 37%

- Long-term gains (property held over one year): taxed at preferential rates of 0%, 15%, or 20%

This distinction directly determines how much tax you owe, often by tens of thousands of dollars.

Unlike a primary residence, where married couples can exclude up to $500,000 of gain under Section 121, investment properties are generally not eligible for the home sale exclusion. One exception applies when a rental is converted to a primary residence and meets strict IRS requirements, but depreciation recapture still applies even then.

Short-Term vs. Long-Term Capital Gains Tax Rates for Investment Property

Short-Term Capital Gains

Any property sold within one year of purchase is taxed as ordinary income. The profit is added to the investor's total income and taxed at their marginal federal rate, which can be as high as 37% for 2025.

Example: An investor earning $150,000 who sells a flip for a $100,000 profit now has $250,000 in taxable income, pushing them into a higher tax bracket.

For 2025, the top federal ordinary income tax rate of 37% applies to taxable income over $626,351 for Single filers and $751,601 for Married Filing Jointly.

Long-Term Capital Gains

Holding a property beyond one year changes the tax picture considerably. Instead of ordinary income rates, investors qualify for preferential long-term rates based on taxable income:

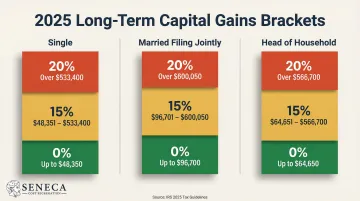

2025 Long-Term Capital Gains Brackets:

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $48,350 | $48,351 to $533,400 | Over $533,400 |

| Married Filing Jointly | Up to $96,700 | $96,701 to $600,050 | Over $600,050 |

| Head of Household | Up to $64,750 | $64,751 to $566,700 | Over $566,700 |

Net Investment Income Tax (NIIT)

The NIIT is a 3.8% surtax that applies to investment income, including capital gains from real estate, for taxpayers whose modified adjusted gross income (MAGI) exceeds certain thresholds:

- Single/Head of Household: $200,000

- Married Filing Jointly: $250,000

The IRS explicitly includes gain from the sale of investment real estate in Net Investment Income. For high-income earners, the effective maximum combined federal long-term capital gains rate is 23.8% (20% base + 3.8% NIIT).

Why the One-Year Holding Period Matters

Illustrative Comparison on a $200,000 Gain:

- Short-term (under 1 year): Taxed as ordinary income at 32% marginal rate = $64,000 tax

- Long-term (over 1 year): Taxed at 15% preferential rate = $30,000 tax

- Savings from holding over one year: $34,000

This example assumes a middle-income investor without NIIT exposure. For high earners subject to the 3.8% NIIT, the gap widens further: short-term rates can reach 37% federal alone, versus a 23.8% combined long-term rate.

State Capital Gains Taxes

State capital gains taxes stack on top of federal rates and vary widely by state. Eight states levy no individual income tax:

- Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, and Wyoming

Most other states tax capital gains as ordinary income. California's top rate hits 13.3%, meaning investors there can face a combined federal and state rate above 36% on long-term gains. Other states range from 2.5% to 10%. Any exit strategy calculation needs to account for state exposure alongside federal liability.

How to Calculate Capital Gains on an Investment Property

The core formula is:

Capital Gain = Sale Price − Selling Costs − Adjusted Cost Basis

Components Defined

Selling costs, including agent commissions, closing costs, transfer taxes, and legal fees, directly reduce the taxable gain.

Adjusted cost basis is where investment property calculations get more complex than most investors expect. The IRS defines it as the original purchase price, plus capital improvements, minus depreciation claimed.

Step-by-Step Calculation Example

Scenario: An investor buys a rental for $400,000, makes $50,000 in improvements, claims $60,000 in depreciation over 10 years, then sells for $600,000 with $30,000 in selling costs.

- Original purchase price: $400,000

- Add capital improvements: +$50,000

- Subtract depreciation taken: −$60,000

- Adjusted cost basis: $390,000

Calculate the gain:

- Sale price: $600,000

- Minus selling costs: −$30,000

- Minus adjusted basis: −$390,000

- Capital gain: $180,000

These figures are illustrative. Work with a tax advisor to apply this to your specific property.

What Qualifies as a Capital Improvement vs. Repair?

Notice the $50,000 in improvements above — whether an expense qualifies as a capital improvement or a repair determines whether it raises your basis at all. The distinction matters far more than most investors realize.

Capital improvements add to your adjusted basis:

- New roof installation

- HVAC system replacement

- Room additions or structural expansions

- Kitchen or bathroom modernization

Repairs and routine maintenance do not add to basis:

- Painting exterior or interior

- Fixing leaks or replacing broken fixtures

- Patching a small section of roof

- Routine maintenance to keep property operational

Keep complete records throughout the holding period: receipts for every capital improvement and depreciation schedules from prior tax returns. If the IRS audits the sale, undocumented improvements cannot be added to basis, meaning a higher taxable gain and a larger tax bill.

Depreciation Recapture: The Hidden Tax Many Investors Miss

When an investor sells a property for more than its depreciated value, the IRS "recaptures" the depreciation deductions previously taken and taxes them at a maximum rate of 25%, separate from and in addition to the standard capital gains tax. This catches many investors by surprise because they assumed they'd only owe the standard long-term capital gains rate on their entire profit.

Here's what that looks like when you run the actual numbers.

How Recapture Works Alongside Capital Gains

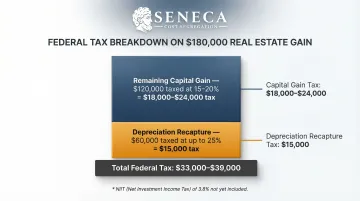

Using the earlier calculation example with a $180,000 gain:

- Depreciation recapture: $60,000 (the depreciation taken) taxed at up to 25% = $15,000 in recapture tax

- Remaining capital gain: $120,000 taxed at 15% or 20% long-term rate = $18,000 to $24,000 in capital gains tax

- Total federal tax: $33,000 to $39,000 (before NIIT)

These taxes layer on top of each other, creating a significantly higher tax bill than many investors anticipate.

Cost Segregation and Depreciation Recapture

Investors who have used accelerated depreciation strategies, such as cost segregation studies, will have taken larger depreciation deductions in earlier years, which means more recapture at sale.

The upfront tax savings from accelerated depreciation provide real cash flow advantages during the holding period. For investors working with a cost segregation firm like Seneca Cost Segregation, those deductions can convert 20–40% of property costs into immediate tax savings, with an average first-year deduction of $171,243 across more than 10,200 completed studies.

Pairing accelerated depreciation with a 1031 exchange allows investors to defer recapture indefinitely, maximizing both in-ownership tax benefits and long-term tax efficiency.

Planning Around Recapture Before You Sell

Depreciation recapture is not avoidable if you've claimed depreciation; it will be owed on sale unless the property is exchanged via a 1031 or held until death (when heirs receive a stepped-up basis). Factoring recapture into your sale projections before going to market prevents the kind of tax-bill surprise that erodes returns you spent years building.

6 Strategies to Reduce or Defer Capital Gains Tax on Investment Property

1. 1031 Exchange (Like-Kind Exchange)

A 1031 exchange allows investors to defer all capital gains tax and depreciation recapture by reinvesting the sale proceeds into a "like-kind" replacement property of equal or greater value within strict IRS timelines:

- 45 days to identify replacement properties in writing

- 180 days to close on the replacement property

This is a deferral, not an elimination, but investors can continue rolling gains forward indefinitely. For that reason, it's the strategy most tax advisors evaluate first before any investment property sale.

2. Tax-Loss Harvesting

Capital losses from other investments (stocks, other properties sold at a loss) can be used to offset capital gains from the investment property sale, reducing the net taxable gain. This requires strategic timing and works best when coordinated with a tax advisor.

3. Installment Sale

Instead of receiving the full sale price upfront, investors can structure a seller-financed installment sale, spreading the gain (and tax liability) over multiple years. This can help keep the investor in a lower tax bracket each year and delay some of the tax hit.

One key limitation: depreciation recapture is fully taxable in the year of sale, regardless of when payments are received.

4. Opportunity Zone Investment

Investors can defer (and potentially partially reduce) capital gains by rolling proceeds into a Qualified Opportunity Fund (QOF) within 180 days of the sale. Gains deferred into a QOF are recognized in 2026 under current law, and investments held 10+ years in the fund may qualify for tax-free appreciation on the new investment.

5. Convert to Primary Residence

Investors who move into a rental property and live in it as a primary residence for at least 2 out of the 5 years before selling may qualify for the Section 121 exclusion ($250,000 for single filers, $500,000 for married filing jointly). That said, depreciation taken during rental periods is still subject to recapture, and any gain must be prorated for periods of nonqualified use after December 31, 2008.

6. Cost Segregation: Accelerate Deductions During Ownership

Unlike the strategies above, cost segregation works during the holding period rather than at the point of sale. It front-loads depreciation deductions to significantly reduce taxable income in the years you own the property. When paired with a 1031 exchange to defer recapture at sale, the two strategies work together — larger deductions during ownership, deferred tax liability at exit.

Seneca Cost Segregation has completed over 10,200 property studies, with an average first-year deduction of $171,243. For many investors, that front-loaded savings frees capital to reinvest before the next acquisition — not after.

Frequently Asked Questions

How much capital gains do I pay on investment property?

The rate depends on how long you held the property. Short-term gains (under 1 year) are taxed as ordinary income (up to 37%); long-term gains (over 1 year) are taxed at 0%, 15%, or 20%, plus a potential 3.8% NIIT for high earners. Depreciation recapture is taxed separately at up to 25%.

How are capital gains calculated on an investment property?

Sale Price minus Selling Costs minus Adjusted Cost Basis equals the capital gain. The adjusted cost basis accounts for the original purchase price plus capital improvements minus depreciation claimed, so keeping thorough records throughout ownership is critical.

How do you avoid capital gains on investment property?

Outright avoidance is rare, but deferral and reduction are achievable through strategies like a 1031 exchange, opportunity zone investment, installment sales, or tax-loss harvesting. Holding until death transfers the property with a stepped-up basis, which can eliminate accumulated gains for heirs.

What is the $250,000/$500,000 home sale exclusion?

This Section 121 exclusion applies to primary residences only — single filers can exclude up to $250,000 in gains; married joint filers up to $500,000 — provided the home was their primary residence for at least 2 of the last 5 years. Investors who convert a rental to a primary residence may partially qualify, but depreciation recapture still applies.

What is the depreciation recapture tax rate on investment property?

Depreciation recapture (Section 1250 gain) is taxed at a maximum federal rate of 25%, separate from and in addition to long-term capital gains rates. The exact amount subject to recapture equals the total depreciation deductions claimed during the ownership period.

Do I have to pay capital gains tax if I do a 1031 exchange?

A properly executed 1031 exchange defers (not eliminates) capital gains tax and depreciation recapture. As long as the investor rolls proceeds into a qualifying like-kind replacement property within IRS deadlines, no tax is owed at the time of sale. The deferred gain carries forward to the replacement property's basis.