Introduction

Most real estate investors treat 1031 exchanges and cost segregation as separate tactics—but combining them correctly is where the real leverage lives, and where most mistakes happen. A 1031 exchange defers capital gains taxes when you sell and reinvest in like-kind property. Cost segregation accelerates depreciation on that replacement property. Used together, these strategies compound tax savings: you defer taxes on the back end while generating fresh deductions on the front end.

The challenge is basis mechanics. After a 1031 exchange, your replacement property carries both a carryover basis (from the relinquished property) and an excess basis (any additional capital you deploy). By default, cost segregation and bonus depreciation only apply to the excess basis. A specific IRS election can change that, allowing you to treat the full combined basis as newly placed in service.

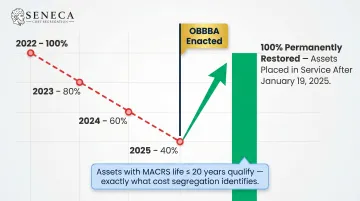

With the One Big Beautiful Bill Act (OBBBA) restoring 100% bonus depreciation permanently for properties placed in service after January 19, 2025, that election is now worth significantly more to investors who get it right.

TL;DR

- A 1031 exchange defers capital gains taxes; cost segregation accelerates depreciation—together, they multiply tax efficiency in a single transaction

- Your replacement property's basis has two parts: only the excess basis qualifies for bonus depreciation by default, but an IRS election opens the full basis to cost segregation

- OBBBA permanently restored 100% bonus depreciation for qualified assets acquired after January 19, 2025, enabling 100% first-year write-offs on qualifying assets

- Personal property identified in cost segregation studies is mostly treated as real property under final IRS regulations—so a cost seg study rarely invalidates a 1031 exchange

- Coordinating the 1031 timeline, cost segregation study, and your CPA before filing is essential to capturing the full benefit

What Are Cost Segregation and 1031 Exchanges?

A 1031 exchange is an IRS-sanctioned mechanism under IRC Section 1031 that allows real estate investors to defer capital gains taxes, depreciation recapture, and net investment income tax by selling investment property and reinvesting the proceeds into like-kind replacement property. You have 45 days to identify the replacement property and 180 days to close from the date you transfer the relinquished property.

Cost segregation is an engineering-based study that reclassifies building components from long-life real property (27.5 or 39 years) into shorter MACRS categories—typically 5, 7, or 15 years. With 100% bonus depreciation now restored under OBBBA, qualifying assets identified through cost segregation can be deducted entirely in year one, rather than spread over decades.

Together, these two strategies work on opposite ends of the same transaction. The 1031 exchange preserves capital by deferring taxes on the sale, while cost segregation generates immediate deductions on the acquisition. You defer taxes on gains from the relinquished property and simultaneously create new depreciation deductions on the replacement property—compressing two rounds of tax savings into a single deal.

Why Real Estate Investors Use Both Strategies Together

The Compounding Effect

A 1031 exchange keeps deferred gains working in your portfolio. Cost segregation on the replacement property generates fresh depreciation that can offset other income—including W-2 income if you qualify as a real estate professional. The result is compounding tax efficiency: you roll equity forward tax-free and immediately create new deductions that reduce your taxable income from multiple income streams.

What You Lose by Using Only One Strategy

Consider a $3,000,000 commercial property depreciated straight-line over 39 years. Annual depreciation under standard MACRS is $76,923—helpful, but modest relative to the asset value. That's where the compounding advantage of combining both strategies becomes concrete.

Now apply cost segregation with 100% bonus depreciation. Industry benchmarks indicate 20-40% of a property's depreciable basis can be reclassified to 5-, 7-, or 15-year property. On a $3,000,000 property:

- $600,000 deducted in year one at 20% reclassification

- $1,200,000 deducted in year one at 40% reclassification

That's $600,000 to $1,200,000 in first-year deductions versus $76,923 spread over 39 years. Capital you would have waited decades to access becomes available in year one—ready for your next acquisition.

Real Estate Professional Status Angle

Investors who qualify as real estate professionals under IRC §469(c)(7) can use accelerated depreciation from cost segregation to offset active income—not just passive rental income. To qualify, investors must meet three tests:

- More than 50% of personal services in real property trades or businesses

- More than 750 hours of services in those businesses annually

- Material participation in the rental activity (typically 500+ hours)

For qualifying investors, the combined strategy becomes particularly powerful: 1031 exchanges preserve equity, and cost segregation generates deductions usable against W-2 income, business income, or other non-passive sources.

How Cost Segregation Works After a 1031 Exchange

The Basis Problem

When you acquire property through a 1031 exchange, the tax basis splits into two components:

- Carryover basis: The adjusted basis from the relinquished property

- Excess basis: Any additional funds paid above the relinquished property's value

These components are treated differently for depreciation and cost segregation purposes under Treasury Regulation §1.168(i)-6.

Option 1 — Default Method

Under default rules, the carryover basis continues depreciating over the remaining recovery period of the relinquished property using the same method and convention. Only the excess basis is treated as newly placed in service—meaning cost segregation and bonus depreciation apply only to the excess basis.

When this option is preferable:

- The relinquished property is near the end of its tax life

- You have minimal carryover basis and significant excess basis

- You want to minimize complexity and avoid making an election

Option 2 — Simplified Method Election (Best When Carryover Basis Is Large)

Under Treas. Reg. §1.168(i)-6(i)(1), you can elect to treat both the carryover basis and excess basis as newly placed in service on the date you acquire the replacement property. This means the full depreciable basis—carryover plus excess—is eligible for cost segregation reclassification.

Bonus depreciation constraint: Bonus depreciation is only available on the excess basis unless the replacement property is brand new and unused (purchased directly from a builder). The carryover basis does not qualify for bonus depreciation on used property under either option.

Numeric Example

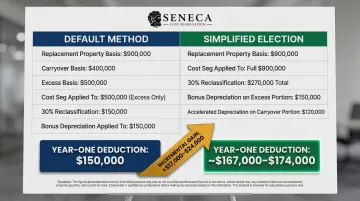

Scenario: You sell a property with a $400,000 adjusted basis and buy a $900,000 replacement property.

- Carryover basis: $400,000

- Excess basis: $500,000 (assumes $500,000 in new capital or debt)

- Total depreciable basis: $900,000 (excluding land)

Under the default method:

- Cost segregation applies to the $500,000 excess basis only

- Assuming 30% reclassification to 5-7 year property: $150,000 eligible for bonus depreciation

- Year-one bonus deduction: $150,000 (at 100% OBBBA rate)

The simplified election changes that calculus significantly by unlocking the full basis for reclassification.

Under the simplified election:

- Cost segregation applies to the full $900,000 depreciable basis

- Assuming 30% reclassification: $270,000 eligible for accelerated depreciation

- However, only the $150,000 from the excess basis qualifies for bonus depreciation

- The remaining $120,000 from the carryover basis is depreciated over 5-7 years (not bonus-eligible)

- Year-one bonus deduction: $150,000 + first-year depreciation on the $120,000 (approximately $17,000–$24,000 depending on method)

- Total first-year deduction under simplified method: approximately $167,000–$174,000

The simplified election increases the cost segregation benefit by allowing the full basis to be reclassified, even though bonus depreciation remains limited to the excess basis.

Seneca Cost Segregation works directly with investors and their CPAs to analyze which depreciation option maximizes benefit before the study is commissioned. This prevents the overstated or understated projections that arise when 1031 basis math is skipped at the outset.

Key Rules That Govern the Combination

Bonus Depreciation Under the OBBBA

The One Big Beautiful Bill Act (OBBBA) restored 100% bonus depreciation permanently for qualifying assets placed in service after January 19, 2025. Assets with a MACRS depreciable life of 20 years or less—exactly the assets identified by cost segregation (5-, 7-, 15-year property)—qualify for full immediate expensing.

This makes a post-1031 cost segregation study dramatically more impactful than under the phased-out bonus depreciation rates that preceded OBBBA. Before OBBBA, bonus depreciation had stepped down to 80%, 60%, 40%, and 20% in successive years.

The 15% Incidental Personal Property Rule

That increase in deduction power makes it critical to understand what can flow through a 1031 exchange without triggering problems. Treasury Regulation §1.1031(k)-1(g)(7)(iii) provides a safe harbor: personal property can be included in a 1031 exchange transaction without invalidating it if:

- It is typically transferred alongside real property in standard commercial transactions, and

- It does not exceed 15% of the fair market value of the replacement real property

Important: Even if the exchange remains valid, personal property received may still be treated as boot and trigger taxable gain.

Example: You acquire a $2,000,000 office building with $250,000 in furniture and equipment (12.5% of the real property value). The furniture meets the safe harbor, so the qualified intermediary safe harbor is not violated. However, the $250,000 in personal property is non-like-kind property—you will recognize gain to the extent of that boot.

Cost Segregation on the Relinquished Property

If you performed a cost segregation study on the property you're now selling in a 1031 exchange, fully depreciated personal property components are at risk of ordinary income recapture under Section 1245 if not matched by equivalent personal property classifications in the replacement property.

How to avoid recapture: If the replacement property's cost segregation study identifies at least equal value of like-kind personal property, you can defer recapture. This is a key reason to commission a cost segregation study on the replacement property when the relinquished property also had one.

Real Property vs. Personal Property Under Sec. 1031 Final Regulations

IRS final Sec. 1031 regulations (T.D. 9935) confirmed that most building components identified as 5- and 7-year property in a cost segregation study are still classified as real property under Sec. 1031. This surprises many investors who assume shorter depreciation lives signal personal property status.

The reason: real property classification for exchange purposes follows state law and structural permanence tests, not MACRS depreciation lives. Performing a cost segregation study on a property involved in a 1031 exchange does not generally invalidate the exchange.

Common Pitfalls, Misconceptions, and When Not to Use Both

Misconception — "Cost segregation on a 1031 property is too complicated or risky"

Many investors fear that performing a cost segregation study on a replacement property jeopardizes the 1031 exchange. With final regulations in place, this concern is largely unfounded. The real risk is failing to align basis calculations with your cost segregation firm before the study is ordered. Skipping that step produces inaccurate savings projections — not the study itself.

Pitfall — Mismatched Property Classifications Across Exchanges

If you accelerated personal property depreciation in the relinquished property (via a prior cost segregation study) but the replacement property has fewer or no equivalent personal property components, ordinary income recapture is triggered even in an otherwise fully deferred exchange.

Solution: Analyze replacement property composition before closing. Request preliminary cost segregation estimates on candidate properties during the 45-day identification window — before you commit.

When Not to Use Both

The combination adds little value in these scenarios:

- Little to no excess basis — cost segregation applies to only a small slice of the property's value

- Depreciation life is nearly exhausted — the simplified election offers no meaningful uplift over what's already scheduled

- Passive losses are already maxed out — if you have no passive income to offset and carryforwards are capped, accelerated deductions won't move the needle near-term

These are situations to pause and evaluate with your CPA—not blanket reasons to avoid the strategy.

Frequently Asked Questions

Can you do a cost segregation study on a 1031 exchange?

Yes. A cost segregation study can be performed on a replacement property acquired through a 1031 exchange. Final Sec. 1031 regulations confirm most cost-seg-identified components are still real property under state law and structural tests. The key is working with a firm that understands 1031 basis calculations before the study is commissioned.

What are the 3-property rule, 95%, 200%, and 5-year rules in a 1031 exchange?

Treas. Reg. §1.1031(k)-1(c)(4) establishes three identification rules: the 3-property rule (up to 3 properties, any value), the 200% rule (any number of properties if total value stays under 200% of the relinquished property's FMV), and the 95% rule (any number of properties if you actually acquire at least 95% of their total value). The 5-year rule under IRC §121(d)(10) blocks the primary residence exclusion if the home was acquired in a prior 1031 exchange within the last five years.

Does a 1031 exchange reset depreciation on the replacement property?

Under default rules, depreciation does not restart—the carryover basis continues on the old schedule. However, you can elect the simplified method under Treas. Reg. §1.168(i)-6(i)(1) to treat the full basis as newly placed in service, which resets depreciation and enables full cost segregation on the combined basis.

What is the 15% incidental personal property rule in a 1031 exchange?

The IRS permits personal property to be included in a 1031 exchange without invalidating it, as long as it is customarily transferred alongside real property and does not exceed 15% of the replacement property's fair market value. That said, it may still be treated as boot and trigger partial taxable gain.

What happens to accelerated depreciation if I sell a property without doing another 1031 exchange?

Accelerated depreciation taken through cost segregation is subject to recapture. Section 1245 personal property recaptures at ordinary income rates (up to 37%), and Section 1250 real property recaptures at 25%. Subsequent 1031 exchanges can defer this recapture indefinitely — with proper advance planning.

What is the simplified method election and when should I use it in a 1031 exchange?

This IRS election under Treas. Reg. §1.168(i)-6(i)(1) treats the full depreciable basis of the replacement property — carryover plus excess — as newly placed in service, making the entire amount eligible for cost segregation reclassification. It delivers the most value when carryover basis is substantial and maximizing first-year deductions is the priority.