Yet according to a Government Accountability Office report, 53% of individual taxpayers with rental real estate activity misreport their activities, leaving billions in legitimate deductions on the table. Many investors either fail to claim depreciation entirely or miss advanced strategies that could multiply their tax savings.

This guide covers everything you need to know: how depreciation works, eligibility requirements, step-by-step calculation methods, advanced strategies like cost segregation and bonus depreciation, and the depreciation recapture tax trap that catches unprepared sellers. Whether you're a first-time landlord or a seasoned investor, understanding these rules can mean the difference between mediocre returns and exceptional cash flow.

TLDR

- Depreciation spreads the building's cost over 27.5 years for residential rentals, generating annual deductions with no out-of-pocket cost

- You must claim depreciation; the IRS assumes you took it and will trigger recapture tax on sale regardless

- Cost segregation reclassifies 20–40% of property costs into 5-, 7-, or 15-year categories, sharply accelerating your deductions

- The 2025 One Big Beautiful Bill Act (OBBBA) restored 100% bonus depreciation for qualifying property acquired after January 19, 2025

- Depreciation recapture taxes prior deductions at up to 25% when you sell; however, 1031 exchanges defer this liability

What Is Rental Property Depreciation and Who Qualifies?

Depreciation is the IRS's recognition that buildings wear out over time. Rather than deducting the entire purchase price in year one, the tax code allows you to recover the cost of the structure (not the land) through annual deductions spread over the property's useful life.

Your rental property's roof, foundation, and systems all deteriorate with use, and the tax code reflects that reality. Each year, you claim a portion of the building's cost as a business expense, reducing your taxable rental income.

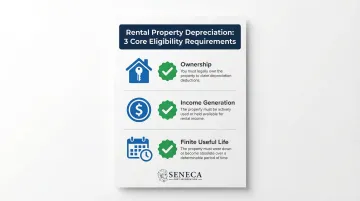

Three Core Eligibility Requirements

According to IRS Publication 527 and Publication 946, your property must meet three specific criteria:

- You own it: Direct ownership qualifies, including properties with an active mortgage

- It generates income: Used in a trade, business, or held for income production (rental use qualifies)

- It has a finite useful life: Expected to last more than one year and subject to wear, decay, or obsolescence

Land never qualifies because it doesn't wear out or become obsolete. You can only depreciate the building and improvements.

The Critical "Allowed or Allowable" Rule

Here's the part most investors miss: depreciation is not optional. Under IRC §1016(a)(2), the IRS calculates depreciation recapture upon sale based on what you could have claimed, even if you didn't take the deduction.

This creates a costly trap for investors who skip the deduction. If you fail to claim $87,000 in depreciation over 10 years, you lose that annual tax benefit entirely. Then when you sell, the IRS still taxes you on that $87,000 at up to 25% — meaning you pay the recapture tax without ever having received the deduction benefit.

The good news: missed deductions are recoverable. File Form 3115 (Application for Change in Accounting Method) to claim omitted depreciation as a Section 481(a) adjustment in the current tax year, with no amended returns required.

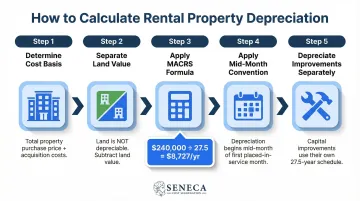

How to Calculate Rental Property Depreciation Step by Step

Calculating your annual depreciation deduction requires five distinct steps. Most investors can complete this process themselves, though complex properties benefit from professional guidance.

Step 1: Determine Your Cost Basis

Your depreciable basis isn't just the purchase price. According to IRS Publication 551, start with the purchase price and add:

- Abstract fees and legal fees

- Recording fees and surveys

- Transfer taxes and title insurance

- Owner's title insurance

- Capitalized improvements made before placing the property into service

Do not include: Points, mortgage interest, appraisal fees for obtaining financing, or other loan-related costs. These are handled separately on Schedule E as financing costs.

Step 2: Separate Land Value from Building Value

The GAO report identified approximately 166,000 taxpayers who illegally depreciated non-depreciable land, a primary IRS audit trigger. You must allocate your total basis between land (non-depreciable) and building (depreciable).

Three acceptable methods:

- Property tax assessment - Use the ratio from your county's assessment (if building is assessed at 80% and land at 20%, apply those percentages to your purchase price)

- Professional appraisal - Hire a licensed appraiser to allocate values

- Purchase agreement allocation - If your contract separately states land and building values

Step 3: Apply the MACRS Calculation

Residential rental properties use the Modified Accelerated Cost Recovery System (MACRS) with a 27.5-year recovery period under the General Depreciation System (GDS).

Formula: Depreciable Basis ÷ 27.5 Years = Annual Deduction

Example:

- Purchase price: $300,000

- Land value: $60,000

- Depreciable basis: $240,000

- Annual deduction: $240,000 ÷ 27.5 = $8,727 per year

Step 4: Account for the Mid-Month Convention

Under IRC §168(d)(2), residential rental property follows the mid-month convention. The IRS treats your property as placed in service at the midpoint of the month it became ready and available for rent.

This affects year one and the final year of depreciation:

- Property placed in service in July: You claim 5.5 months of depreciation in year one (July 15 - December 31)

- Year one deduction: $8,727 × (5.5 ÷ 12) = $4,000

- Years 2-27: Full $8,727 annual deduction

- Final year (year 28): Remaining 6.5 months = $4,727

Step 5: Depreciate Improvements Separately

Once a property is in service, any improvements made afterward don't roll into the original depreciation schedule. Capital improvements must be depreciated as separate assets with their own placed-in-service dates and recovery periods. Examples include:

- New roof installation

- HVAC system replacement

- Room additions or structural modifications

- Kitchen or bathroom renovations

Repairs and maintenance are deducted immediately in the year incurred. Examples include:

- Repainting existing surfaces

- Fixing broken appliances

- Patching roof leaks

- Replacing broken windows

A $15,000 roof repair is deducted immediately; a $15,000 roof replacement must be depreciated over 27.5 years. That single classification decision can shift thousands of dollars between this year's tax bill and the next 27.

Types of Depreciation Methods for Rental Property

Not all depreciation follows the same schedule. The IRS provides multiple methods, each with specific applications and requirements.

Straight-Line Depreciation (GDS)

The General Depreciation System is the default method for residential rental properties. It spreads equal annual deductions across 27.5 years, providing predictable, consistent tax benefits. Most rental property owners use GDS: it's simple, requires no special elections, and delivers the maximum annual deduction under standard rules.

Alternative Depreciation System (ADS)

ADS extends the recovery period to 30 years for residential property placed in service after December 31, 2017 (40 years for property placed in service earlier). This results in smaller annual deductions.

When ADS is required:

- Properties used predominantly outside the United States

- Tax-exempt use properties

- Properties owned by electing real property trade or business under TCJA §163(j)

- Farming properties with certain elections

How the two compare on a $240,000 depreciable basis:

| Method | Recovery Period | Annual Deduction ($240,000 basis) |

|---|---|---|

| GDS | 27.5 years | $8,727 |

| ADS | 30 years (post-Dec 31, 2017) | $8,000 |

If you're not required to use ADS, GDS consistently produces the larger deduction. ADS becomes relevant primarily when TCJA §163(j) elections are in play.

Component Depreciation for Personal Property

Not everything in your rental follows the 27.5-year schedule. Personal property and land improvements qualify for much shorter recovery periods:

| Recovery Period | Property Examples |

|---|---|

| 5-year property | Appliances (refrigerators, stoves, dishwashers); Carpeting and flooring; Furniture used in the rental |

| 7-year property | Office furniture and equipment; Decorative elements not permanently attached |

| 15-year property | Landscaping and fencing; Parking lots and driveways; Swimming pools and outdoor structures |

These shorter schedules generate larger near-term deductions. A $5,000 appliance package depreciated over 5 years provides $1,000 annually, compared to just $182 if treated as part of the building's 27.5-year schedule.

This component-level thinking leads directly into cost segregation, the most powerful depreciation strategy available to real estate investors.

Beyond Standard Depreciation: Bonus Depreciation and Cost Segregation

Standard depreciation provides steady, predictable deductions. But advanced strategies can multiply your first-year tax savings by 10x or more.

The 2025 OBBBA 100% Bonus Restoration

Bonus depreciation allows investors to immediately expense a percentage of qualifying property rather than spreading deductions over years. The Tax Cuts and Jobs Act established a phase-down from 100% (September 27, 2017 – December 31, 2022) to 80% (2023), 60% (2024), and 40% (early 2025).

Then everything changed. The "One Big Beautiful Bill Act" (OBBBA, P.L. 119-21), enacted July 4, 2025, restored 100% bonus depreciation for qualified property acquired and placed in service on or after January 19, 2025. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | |

| January 1, 2023 – December 31, 2023 | 80% | |

| January 1, 2024 – December 31, 2024 | 60% | |

| January 1, 2025 – January 18, 2025 | 40% | |

| January 19, 2025 – December 31, 2030 | 100% | Acquisition date must be January 19, 2025 or later |

| 2025 (if acquired before January 19, 2025) | 40% | TCJA phase-down still applies |

| 2026 (if acquired before January 19, 2025) | 20% | TCJA phase-down still applies |

This applies to 5-, 7-, and 15-year property components, which is exactly what cost segregation identifies.

Cost Segregation: Engineering Maximum Tax Benefits

Cost segregation breaks your property into component parts, reclassifying them from 27.5- or 39-year assets into 5-, 7-, or 15-year property eligible for accelerated depreciation. An engineering-based study identifies specific components:

| Recovery Period | Component Examples |

|---|---|

| 5-year property | Carpeting and vinyl flooring; Window treatments and blinds; Appliances and kitchen equipment; Decorative lighting fixtures |

| 7-year property | Office furniture and equipment; Movable partitions; Decorative wall coverings |

| 15-year property | Landscaping and site improvements; Parking lots and driveways; Fencing and exterior lighting; Swimming pools and outdoor amenities; Specialty electrical systems; Decorative masonry |

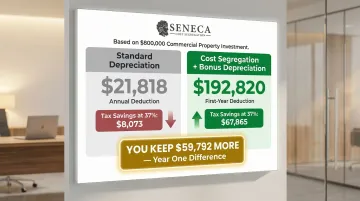

Real-World Impact: The Numbers That Matter

A property that generates $8,727 in annual depreciation under standard MACRS can produce dramatically higher first-year deductions through cost segregation and bonus depreciation.

Seneca Cost Segregation, which has assessed over 10,200 properties across all 50 states, reports an average first-year deduction of $171,243 for clients combining cost segregation with bonus depreciation. This represents 20-40% of most property costs converted into immediate tax savings.

Example scenario:

- Purchase price: $800,000

- Land value: $200,000

- Depreciable basis: $600,000

- Standard depreciation: $21,818 annually

- After cost segregation: $192,820 first-year deduction

- Tax savings at 37% rate: $67,865

That gap comes from reclassifying $350,000 of basis into shorter-life components, and how much benefit you capture depends heavily on the property type.

Which Properties Benefit Most?

Cost segregation delivers the highest returns for properties with significant personal property components or specialized improvements:

| Benefit Level | Reclassification Rate | Property Types |

|---|---|---|

| Highest benefit | 30–60% | Short-term rentals with furnishings and appliances; Multi-family properties with extensive amenities; Commercial properties with specialized systems; Properties with recent renovations or improvements |

| Moderate benefit | 20–30% | Standard residential rentals; Office buildings; Retail properties |

| Lower benefit | 10–20% | Warehouses with minimal improvements; Basic industrial buildings |

A minimum depreciable basis of $300,000 is the threshold where study costs (typically $5,000 to $15,000 depending on property complexity) are justified by the tax savings.

IRS Compliance and Audit Defensibility

The IRS Cost Segregation Audit Techniques Guide explicitly warns against "rule of thumb" or software-only estimates. The IRS strongly prefers a "detailed engineering approach" performed by qualified professionals involving:

- On-site physical inspections

- Blueprint and construction document review

- Component-by-component cost allocation

- Detailed engineering documentation

A properly conducted engineering-based study is fully IRS-compliant and can withstand audit scrutiny. Seneca Cost Segregation backs every study with an audit defense guarantee, demonstrating confidence in their methodology's defensibility.

Software-only approaches lack that documentation and engineering foundation. Without a qualified professional's sign-off and component-level cost allocation, the IRS has documented grounds to disallow deductions, meaning the study cost is the least of your concerns if it triggers an audit.

Depreciation Recapture: What Happens When You Sell

Depreciation provides powerful tax benefits during ownership. But the IRS eventually reclaims a portion of that benefit when you sell.

Understanding Section 1250 Recapture

Under IRC §1(h)(6) and Publication 544, when you sell a depreciated rental property at a gain, the portion of your long-term capital gain attributable to straight-line depreciation is classified as "unrecaptured section 1250 gain" and taxed at a maximum rate of 25%.

This applies whether you actually claimed the depreciation or not, which is another reason the "allowed or allowable" rule matters.

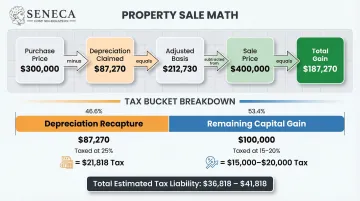

10-Year Hold Example

Let's make the math concrete:

Property details:

- Purchase price: $300,000

- Land value: $60,000

- Depreciable basis: $240,000

- Annual depreciation: $8,727

- Hold period: 10 years

Cumulative depreciation: $8,727 × 10 years = $87,270

At sale:

- Sale price: $400,000

- Adjusted basis: $300,000 - $87,270 = $212,730

- Total gain: $400,000 - $212,730 = $187,270

Tax breakdown:

- Depreciation recapture: $87,270 × 25% = $21,818

- Remaining capital gain: $100,000 × 15-20% (depending on income) = $15,000-$20,000

- Total tax liability: $36,818-$41,818

The Installment Sale Liquidity Trap

Many sellers use owner financing (installment sales) to spread payments over years. But there's a severe liquidity trap few anticipate.

Under IRC §453(i), any depreciation recapture must be recognized as ordinary income in the year of disposition, even if you receive zero cash upfront. You owe the 25% recapture tax immediately, regardless of payment structure.

Note: When structuring seller financing, a down payment large enough to cover the immediate recapture tax liability is needed at closing. In the example above, at least $21,818 cash at closing is required to cover the IRS liability.

Two Strategies to Manage Recapture

Strategy 1: 1031 Like-Kind Exchange

An IRC §1031 exchange allows you to defer both capital gains and depreciation recapture by rolling proceeds into a replacement property of equal or greater value.

Requirements:

- Both properties must be held for investment or business use

- Exchange must be completed within strict timelines (45 days to identify, 180 days to close)

- Must use a qualified intermediary

- Replacement property must equal or exceed relinquished property value

1031 exchanges defer 100% of depreciation recapture indefinitely, until you eventually sell without exchanging.

Strategy 2: Installment Sales

Despite the recapture trap covered above, installment sales remain useful for managing the remaining capital gain. That portion can be spread across multiple years through installment reporting, which doesn't reduce total tax owed but can keep you in lower brackets each year. This strategy works best when:

- Your capital gain is large relative to your annual income

- You expect to stay in a lower tax bracket in future years

- You've already secured enough cash at closing to cover the recapture tax

The Strategic Takeaway

Because recapture is owed regardless of whether depreciation was claimed, taking the full annual deduction avoids these outcomes. Failing to claim it means:

- You lose the annual tax benefit (reduced cash flow during ownership)

- You still pay the 25% recapture tax when you sell

- You've effectively donated money to the IRS for no reason

The recapture math warrants review with a qualified tax advisor before any sale is structured, especially seller financing or a 1031 exchange. The timing and structure of the exit matters as much as the depreciation claimed.

Common Mistakes Rental Property Owners Make with Depreciation

Even experienced investors make costly depreciation errors. Three common pitfalls include:

Depreciating Land Value

The GAO identified 166,000 taxpayers who improperly included land in their depreciable basis. This is one of the IRS's primary audit triggers for rental property owners.

The fix: Land value is separated from building value using property tax assessments, professional appraisals, or documented purchase allocations. If your property tax statement shows land at 20% and improvements at 80%, those percentages are applied to the purchase price.

Using the full purchase price as the depreciable basis is an automatic red flag.

Using the Wrong Placed-in-Service Date

Depreciation begins when the property is "ready and available" for rent, not when a tenant moves in or when you close on the purchase.

Wrong: Using the date your first tenant's lease begins Right: Using the date the property was ready to rent (renovations complete, utilities connected, listing active)

If you purchased July 1, completed renovations August 15, and got your first tenant September 1, your placed-in-service date is August 15. Starting depreciation later means losing deductions you're entitled to claim.

Confusing Repairs with Improvements

This is where misclassification costs investors the most. Under Treas. Reg. §1.263(a)-3, you must capitalize (depreciate) expenses that result in:

- Betterment: corrects a pre-existing defect or enlarges the property

- Restoration: replaces a substantial structural component

- Adaptation: converts the property to a new or different use

| Category | Tax Treatment | Examples |

|---|---|---|

| Repairs | Deduct immediately | Repainting existing surfaces; Fixing broken appliances; Patching roof leaks; Replacing broken windows |

| Improvements | Must depreciate | Complete roof replacement; HVAC system replacement; Room additions; Kitchen/bathroom renovations |

The numbers tell the story: a $20,000 expense deducted immediately reduces current-year taxes by $7,400 (at the 37% rate). Depreciated over 27.5 years, that same expense yields only $269 annually, or $996 in year-one tax savings. That's a $6,404 difference riding on a single classification call.

The IRS scrutinizes this line closely. If you're unsure how a major expense should be classified, document your reasoning before filing, as misclassification is one of the fastest routes to a rental property audit.

Frequently Asked Questions

How many years do you depreciate a rental property?

Residential rental properties are depreciated over 27.5 years under the General Depreciation System (GDS/MACRS) or 30 years under the Alternative Depreciation System (ADS). Commercial properties follow a 39-year schedule.

What is the most common depreciation method for rental property?

The straight-line method under the General Depreciation System (GDS/MACRS) is the standard approach, spreading equal deductions across 27.5 years for residential properties. ADS applies in specific situations, such as properties used outside the US or certain tax-exempt use cases.

Can I claim 100% depreciation on my rental property?

Standard depreciation spreads deductions over 27.5 years, but through cost segregation and bonus depreciation, investors can accelerate a significant portion into year one. Under the 2025 OBBBA, properties acquired after January 19, 2025, qualify for 100% bonus depreciation on 5-, 7-, and 15-year components.

Do you have to pay back depreciation on a rental property?

Yes. When you sell, the IRS taxes the amount previously depreciated at up to 25% under Section 1250 recapture rules. This applies whether or not you actually claimed the deductions, making it critical to take the annual depreciation benefit.

Is it worth claiming depreciation on a rental property?

Yes, and skipping it is a costly mistake. Depreciation reduces taxable income during ownership without any cash outlay, and the IRS applies recapture tax upon sale regardless of whether you claimed it. Not taking the deduction means paying the tax without ever receiving the benefit.

What are the main types of depreciation for rental property?

The main types are straight-line depreciation under GDS (27.5-year residential), ADS (30-year), and accelerated component depreciation through cost segregation, which reclassifies parts of the property into 5-, 7-, or 15-year asset categories eligible for bonus depreciation.

Ready to maximize your rental property tax deductions? Seneca Cost Segregation has helped real estate investors across all 50 states achieve an average of $171,243 in first-year deductions through engineering-based cost segregation studies. With over 10,200 properties assessed and a 95% client referral rate, the team brings 12+ years of specialized expertise and full audit defense protection.

Beyond cost segregation, Seneca provides complimentary tax assessments to identify additional savings opportunities across your entire portfolio—with 70% of clients discovering tax benefits they hadn't previously considered. Contact Seneca Cost Segregation at 530-797-6539 or visit their website to get your free savings estimate today.