Introduction

Rental income looks attractive on paper, until you factor in mortgage payments, property taxes, insurance, repairs, management fees, and unexpected maintenance costs. Many landlords watch their margins erode and assume it's the market. More often, it's missed deductions. The difference between a profitable rental portfolio and one that barely breaks even often comes down to knowing which expenses the IRS allows you to deduct, and claiming them correctly.

The tax code offers landlords substantial advantages across more categories than most realize. Depreciation alone can offset tens of thousands in taxable income annually. Add in mortgage interest, repairs, management fees, and professional services, and the deductible total can easily exceed what most landlords ever claim. The shortfall isn't usually a legal problem. It's a documentation and awareness problem.

This guide covers the full range of rental property tax deductions: major property-level write-offs, operating expenses, professional service costs, and the distinctions that keep you compliant. We'll also walk through passive loss rules, recordkeeping requirements, and how to report everything on Schedule E.

TLDR: Key Rental Property Tax Deductions at a Glance

- Landlords can deduct most ordinary operating expenses, including mortgage interest, property taxes, insurance, repairs, management fees, utilities, travel, and professional services

- Depreciation is usually the biggest deduction (27.5-year schedule for residential rentals); cost segregation can accelerate 20–40% of property value into year-one deductions

- Capital improvements, land value, and personal-use expenses are not immediately deductible

- Passive loss rules cap annual rental loss deductions at $25,000, phasing out completely above $150,000 modified AGI

- Accurate recordkeeping and correct Schedule E filing are essential for audit protection

Major Property-Level Tax Deductions

These deductions stem from owning the property itself and typically represent the largest dollar amounts you can write off each year.

Depreciation: Your Largest and Most Powerful Deduction

The IRS allows you to deduct the cost of a residential rental building over 27.5 years using straight-line depreciation. Land value is always excluded. Only the structure and improvements qualify. This is a non-cash deduction, meaning you write off an asset you already own without spending additional money each year.

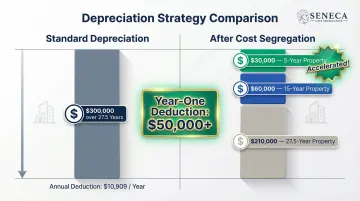

Standard depreciation example: A $400,000 property with $100,000 in land value leaves $300,000 of depreciable basis. Under standard depreciation, you'd deduct $10,909 annually ($300,000 ÷ 27.5 years) for the next 27.5 years.

Cost segregation accelerates this timeline. Instead of depreciating the entire building over 27.5 years, an engineering-based cost segregation study reclassifies components such as flooring, appliances, fixtures, landscaping, and electrical systems into shorter 5-, 7-, or 15-year depreciation schedules. The result: deductions that would have trickled in over decades get pulled forward into year one.

Seneca Cost Segregation has completed over 10,200 engineering-based studies nationwide, with clients averaging a $171,243 first-year deduction, often by converting 20–40% or more of a property's cost into accelerated write-offs.

Cost segregation example: That same $300,000 depreciable basis might break down as follows after a study:

- $30,000 reclassified to 5-year property (appliances, carpets)

- $60,000 reclassified to 15-year property (landscaping, fencing, site improvements)

- $210,000 remaining as 27.5-year property

With 100% bonus depreciation (available for property acquired and placed in service after January 19, 2025), the $30,000 in 5-year property generates an immediate $30,000 deduction in year one. The 15-year property accelerates significantly as well. Instead of $10,909 in year-one depreciation, you might claim $50,000 or more, depending on bonus depreciation rates and study findings.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate |

|---|---|

| September 27, 2017 – December 31, 2022 | 100% bonus depreciation |

| January 1, 2023 – December 31, 2023 | 80% bonus depreciation |

| January 1, 2024 – December 31, 2024 | 60% bonus depreciation |

| January 1, 2025 – January 18, 2025 | 40% bonus depreciation |

| January 19, 2025 – December 31, 2030 | 100% bonus depreciation if acquisition date is January 19, 2025 or later |

If acquisition date is before January 19, 2025:

- 40% bonus depreciation applies in 2025

- 20% bonus depreciation applies in 2026

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Mortgage Interest and Property Taxes

Mortgage interest on rental property loans is fully deductible as a rental expense on Schedule E. Unlike the mortgage interest deduction for primary residences (which is limited), rental property interest has no cap. For many landlords, this is the second-largest deduction after depreciation.

Property taxes on your rental are also fully deductible in the year paid, and they bypass the $10,000 SALT cap that limits personal residence deductions on Schedule A. Tracking rental property taxes separately from personal home taxes ensures each deduction lands in the correct place on the return.

Insurance Premiums

Premiums for landlord insurance, liability coverage, fire insurance, and flood insurance are fully deductible. If you use the property personally for part of the year, only the portion covering the rental period qualifies, and expenses must be prorated based on rental vs. personal use days.

Deductible insurance types include:

- Landlord/dwelling fire policies

- General liability coverage

- Flood and earthquake insurance

- Loss of rental income riders

- Umbrella policies (rental-use portion)

Operating and Management Expense Deductions

Day-to-day costs of running a rental property make up a large share of annual expenses, and the IRS allows most of these to be deducted in the year paid.

Repairs vs. Capital Improvements: A Critical Distinction

The IRS draws a sharp line between repairs and improvements:

| Type | IRS Treatment | Examples |

|---|---|---|

| Repairs | Restore property to working condition; immediately deductible in the year paid | Fixing a leaky faucet, repainting walls, replacing broken windows |

| Capital Improvements | Add value, prolong useful life, or adapt property to new use; must be capitalized and depreciated over time | Adding a new HVAC system, replacing the entire roof, renovating a kitchen |

Common mistakes include trying to deduct a full kitchen renovation or new roof as a repair. The IRS will reclassify these as improvements during an audit.

Two elections can simplify this analysis for smaller purchases:

| Safe Harbor | Details |

|---|---|

| De minimis safe harbor | Expense items up to $2,500 per invoice or item ($5,000 with an applicable financial statement). This election is claimed by attaching a statement titled "Section 1.263(a)-1(f) de minimis safe harbor election" to a timely filed return. |

| Routine maintenance safe harbor | Recurring activities performed more than once over a 10-year period — like repainting every few years — qualify as deductible maintenance rather than improvements. |

Property Management, Advertising, and Tenant-Related Costs

Fully deductible operating expenses include:

- Property management fees paid to third-party managers

- Advertising costs (online listings, signage, professional photography)

- Tenant screening and background check fees

- Legal fees for lease drafting or eviction proceedings

- Accounting fees for rental-related bookkeeping

All of these go on Schedule E. Receipts and invoices organized throughout the year make filing straightforward.

Utilities, Supplies, and Travel

If you pay utilities on behalf of tenants (water, trash, gas, electric), those costs are fully deductible. So are office supplies tied to managing the rental: printer paper, postage, and software subscriptions.

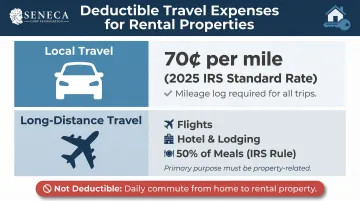

Travel expenses to inspect, manage, or maintain rental properties are deductible:

| Travel Type | Deductible Amounts |

|---|---|

| Local mileage | The IRS standard mileage rate applies (70 cents per mile for 2025, up from 67 cents in 2024) |

| Long-distance travel | Flights, hotels, and 50% of meals for out-of-town properties qualify, as long as the trip's primary purpose is property-related |

Detailed mileage logs and receipts support these deductions. Travel between your home and a rental property is generally nondeductible commuting unless your home qualifies as your principal place of business.

Professional and Business Expense Deductions

Running rental property involves professional costs that the IRS treats as legitimate business expenses.

Professional Services: Legal, Accounting, and Tax Prep

Fees paid to attorneys, CPAs, and tax preparers specifically for rental property matters are deductible. This includes:

- Legal fees for lease drafting, eviction proceedings, or tenant disputes

- Accounting fees for rental bookkeeping and financial statements

- Tax preparation fees allocated to preparing Schedule E (not personal tax filing)

- Tax software costs for rental income reporting

Note: Legal fees paid to defend or acquire title to property must be capitalized and added to the property's basis, not deducted currently.

Home Office Deduction

Landlords who use a dedicated space in their home exclusively and regularly to manage rental activities may qualify for the home office deduction. The space must be your principal place of business for rental management.

That means no other fixed location where you conduct substantial administrative work for your rentals.

Two calculation methods:

| Method | Details |

|---|---|

| Simplified method | $5 per square foot, up to 300 square feet maximum ($1,500 deduction) |

| Actual expense method | Allocate a percentage of actual home expenses (mortgage interest, property taxes, utilities, insurance, depreciation) based on square footage |

Landlords report this deduction using the worksheet in IRS Publication 587, not Form 8829 (which is for Schedule C filers).

Employee and Independent Contractor Wages

Wages paid to employees (like a resident manager) or independent contractors (plumbers, landscapers, handymen) for rental property work are deductible.

For contractors, the following Form 1099-NEC rules apply:

| Rule | Details |

|---|---|

| Threshold | Issue a 1099-NEC to any contractor paid $600 or more during the calendar year |

| Filing deadline | File with the IRS and furnish to the contractor by January 31 |

| Exceptions | Payments to corporations are generally exempt, except attorney fees, which must always be reported |

What Is Not Deductible and How Passive Loss Rules Affect You

Understanding what you cannot deduct is just as important as knowing what qualifies.

Non-deductible items:

| Non-Deductible Item | Treatment |

|---|---|

| Land value | Never depreciable under any circumstances |

| Capital improvements | Not immediately deductible, though recovered through depreciation over time |

| Personal-use expenses | If you live in the property part of the year, expenses must be prorated |

| Mixed-purpose travel | Travel costs exceeding the rental business purpose are not deductible |

Passive Activity Loss Rules

Rental activities are classified as passive income under IRS rules, meaning losses can generally only offset other passive income. Two exceptions allow certain landlords to deduct losses against ordinary income.

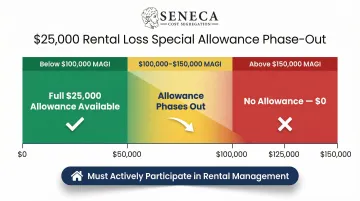

The $25,000 Special Allowance

Landlords who actively participate in managing their rental (approving tenants, making repair decisions) and have a modified adjusted gross income (MAGI) under $100,000 can deduct up to $25,000 in rental losses against ordinary W-2 wages. This allowance phases out between $100,000 and $150,000 MAGI, dropping to zero at the $150,000 threshold.

$25,000 Special Allowance Phase-Out

| MAGI | Allowable Rental Loss Deduction Against Ordinary Income |

|---|---|

| Under $100,000 | Up to $25,000 |

| $100,001 – $149,999 | Phases out proportionally |

| $150,000 or more | $0 (no allowance) |

The Real Estate Professional Exception

If you work 750+ hours per year in real estate activities and this exceeds time spent in any other profession, you can treat rental losses as non-passive and deduct them fully against any income. This requires meeting strict IRS tests annually and making a formal grouping election for multiple properties.

Use Form 8582 (Passive Activity Loss Limitations) to calculate your allowable losses under either exception and track unused losses carried forward.

How to Claim and Track Your Rental Property Deductions

Rental income and expenses are reported on Schedule E (Form 1040), Supplemental Income and Loss. Each property gets its own column (A, B, or C). If you own more than three rentals, attach additional Schedule E pages and combine totals on a master schedule.

Depreciation calculated on Form 4562 carries over to line 18 of Schedule E, while operating expenses, mortgage interest, property taxes, and management fees each have their own designated lines. Keeping those entries organized starts with solid recordkeeping.

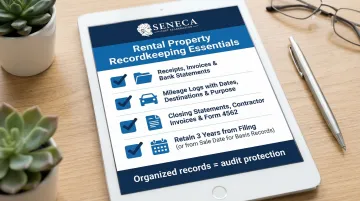

Recordkeeping best practices:

| Records to Maintain | Details |

|---|---|

| Receipts, invoices, bank statements, and lease agreements | Required documentation |

| Contemporaneous mileage logs (with dates, destinations, and business purpose) | Support deduction claims |

| Closing statements, contractor invoices, and Forms 4562 | Required for depreciation tracking |

| All tax records | At least 3 years from filing date (or 3 years from sale date for property basis records) |

Partial personal use adds another layer to watch. If you rent a property for fewer than 15 days per year, rental income is tax-free, but no expenses are deductible.

If you rent for 15+ days and personal use exceeds the greater of 14 days or 10% of rental days, you must prorate deductions between rental and personal use. Your rental deductions cannot exceed gross rental income in this scenario.

Frequently Asked Questions

What expenses are deductible on a rental property?

You can deduct mortgage interest, property taxes, depreciation, insurance, repairs, property management fees, professional services (legal, accounting), travel, utilities, and advertising: any ordinary and necessary expense for managing the rental property.

What is not deductible as a rental expense?

Land value, capital improvements (which are depreciated rather than expensed), personal-use expenses, and costs unrelated to the rental activity cannot be deducted. Capital improvements are recovered over time through depreciation schedules.

What is the $25,000 rental loss allowance?

Landlords who actively participate in managing their rental can deduct up to $25,000 in rental losses against ordinary income, subject to modified AGI phase-out limits. The allowance begins phasing out at $100,000 MAGI and disappears completely at $150,000.

How can I maximize my tax return on a rental property?

Several strategies together produce the biggest results:

- Tracking every eligible expense throughout the year—rather than reconstructing at tax time—produces more accurate results

- Full use of depreciation, including a cost segregation study for accelerated deductions, reduces taxable income

- Detailed records ensure deductions hold up under scrutiny

- A tax professional who specializes in real estate can support accurate filing

What is the most overlooked tax deduction for rental property owners?

Depreciation, and specifically accelerated depreciation through cost segregation, is frequently underutilized. Many landlords are unaware they can front-load deductions on components like flooring, appliances, fixtures, and landscaping into the first year rather than spreading them over 27.5 years.

Are rental properties a good tax write-off?

Yes. Rental properties offer depreciation (a non-cash deduction), deductions for nearly all operating expenses, and the potential to offset taxable income significantly. These are advantages few other investments match.