Introduction

Ultra-high-net-worth individuals (typically defined as those with $30 million or more in investable assets) face a specific challenge: their real estate holdings generate enormous tax exposure, yet many fail to deploy the layered strategies those portfolios make available.

Standard tax planning addresses single properties or isolated transactions. UHNW portfolios require something different — a coordinated approach that simultaneously manages income tax on rental operations, capital gains on appreciating assets, and estate tax across holdings that may span multiple states and property types.

The tax pressures at this wealth level are substantial:

- High ordinary income rates on rental operations

- Capital gains exposure on decades of appreciation

- The 3.8% Net Investment Income Tax surcharge for high earners

- Estate tax on portfolios valued in the tens or hundreds of millions

- Heightened IRS scrutiny: audit rates for taxpayers reporting $10 million or more in income exceeded 11% in recent years

The complexity of multi-entity structures, cross-jurisdictional holdings, and overlapping tax regimes means generic tax advice leaves millions unrealized.

What follows is a practical roadmap through the strategy categories every UHNW real estate investor should deploy: accelerated depreciation to front-load deductions, capital gains deferral and elimination mechanisms, income tax mitigation through strategic status elections, and wealth transfer structures that reduce or eliminate estate tax across generations.

TLDR:

- UHNW real estate portfolios create amplified tax exposure and amplified opportunity—strategies scaled across large holdings generate millions in savings

- Cost segregation with bonus depreciation reclassifies 20-30% of property value into front-loaded deductions

- Serial 1031 exchanges and Opportunity Zone investments defer or eliminate capital gains, compounding equity tax-free

- Real estate professional status unlocks unlimited loss deductions against ordinary income, while QBI deductions reduce pass-through income by up to 20%

- Dynasty Trusts, FLP valuation discounts, and GRATs remove appreciation from taxable estates across generations

What Sets UHNW Real Estate Tax Planning Apart

The defining feature of UHNW real estate tax planning is scale. When you control multiple properties across commercial, multi-family, and high-value residential asset classes—often in different states—each tax strategy produces exponentially greater results than it would for a single-property investor. A cost segregation study that saves $50,000 on one building saves $500,000 when applied to ten. A 1031 exchange that defers $200,000 in capital gains on a single sale defers $2 million when used across a portfolio disposition cycle.

That scale creates a compounding problem: every transaction touches three distinct tax burdens at once.

Three Simultaneous Tax Burdens

UHNW investors must manage three overlapping exposures:

- Income tax on rental receipts and business income from property operations

- Capital gains tax on accumulated appreciation when properties are sold or transferred

- Estate and gift taxes on the total value of holdings at death or during lifetime transfers

Standard tax planning addresses these in isolation—filing annual returns, planning individual sales, drafting wills. UHNW planning integrates all three simultaneously, recognizing that a decision in one area (such as accelerating depreciation through cost segregation) directly impacts the others (increasing recapture liability at sale, but creating offsetting losses that reduce estate size).

Regulatory Scrutiny and Compliance Burden

High-income taxpayers face a materially higher audit probability than the average filer. The IRS closes over 500,000 audits annually and recommends $29 billion in additional tax, with large real estate portfolios drawing disproportionate scrutiny.

The compliance burden at this level spans several distinct areas:

- Passive activity loss rules and material participation documentation

- The 3.8% Net Investment Income Tax on investment income above $250,000 for married filers

- Defensible valuations for entity structures and elections

Every tax position must be documented and supported by qualified professionals. At portfolio scale, audit exposure is a structural reality, not a remote risk.

Cost Segregation and Bonus Depreciation: The Front-Loaded Advantage

Standard depreciation methods treat commercial real property as a single asset recovered over 39 years, and residential rental property over 27.5 years. This approach underutilizes the deductible value of the property by ignoring the reality that buildings contain distinct components—electrical systems, plumbing, HVAC, flooring, fixtures, landscaping, parking lots—with much shorter useful lives.

Cost segregation is the engineering-based methodology that reclassifies these components into 5-, 7-, and 15-year asset classes under the Modified Accelerated Cost Recovery System (MACRS). Industry benchmarks show that 20-30% of a commercial property's depreciable basis can be reclassified, with an average of 16.3% moved to 5-year property and 11.4% to 15-year property.

For a $10 million commercial acquisition with $8 million in depreciable basis, that translates to $1.3 million in 5-year assets and $900,000 in 15-year assets — fully depreciated decades ahead of standard schedules.

Bonus Depreciation Amplifies Results

The true power of cost segregation emerges when combined with bonus depreciation. The One Big Beautiful Bill Act (OBBBA) permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. This means reclassified short-life assets become immediately eligible for first-year write-offs of 100% of their basis.

For UHNW investors, the math is concrete:

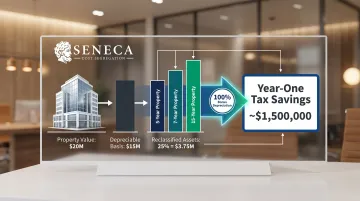

- A $20 million multi-family acquisition with $15 million depreciable basis and 25% reclassification generates $3.75 million in bonus-eligible assets

- At 100% bonus depreciation and the top 37% federal rate plus 3.8% NIIT, that single deduction produces approximately $1.5 million in federal tax savings in year one

Seneca Cost Segregation, which has completed over 10,200 studies nationwide, reports an average first-year deduction of $171,243 across all property types. For large commercial properties and multi-family complexes — where reclassifiable values run into the millions — engineering-based studies routinely surface substantially more than that baseline. Studies are typically completed within 2-4 weeks and include audit defense guarantees.

Qualified Improvement Property (QIP)

The CARES Act corrected a drafting error in the Tax Cuts and Jobs Act, retroactively classifying interior improvements to nonresidential buildings as 15-year property eligible for bonus depreciation. For UHNW investors who actively improve commercial holdings—renovating office lobbies, upgrading retail interiors, modernizing hotel rooms—QIP provides another avenue for immediate write-offs. Improvements made after the building was first placed in service now qualify for accelerated recovery, making value-add acquisition strategies even more tax-efficient.

Depreciation Recapture Planning

Accelerating depreciation today creates a corresponding liability at disposition. Section 1250 recapture taxes prior depreciation claimed at a maximum 25% rate upon property sale — and for UHNW investors who have claimed millions in deductions, that future bill can be significant. Managing it requires forward planning: 1031 exchanges defer recapture along with capital gains, while strategic hold periods can time dispositions against offsetting losses. Cost segregation should never be deployed in isolation — it must integrate into a broader disposition and portfolio management strategy.

Capital Gains Management: 1031 Exchanges and Opportunity Zones

For UHNW investors, capital gains represent one of the largest single tax exposures. Decades of appreciation on multiple properties create embedded gains that, if recognized, trigger the top 20% long-term capital gains rate plus the 3.8% NIIT, for an effective federal rate of 23.8%. State taxes in high-tax jurisdictions push the combined rate above 30%. On a $50 million portfolio with $35 million in embedded gain, an unplanned liquidation could trigger $8.3 million in federal capital gains tax alone.

1031 Like-Kind Exchanges: Indefinite Deferral

The Section 1031 like-kind exchange remains the primary mechanism for deferring capital gains on real property at scale. The mechanics are straightforward: sell an appreciated property, roll proceeds into a replacement property of equal or greater value within strict IRS timelines (45-day identification, 180-day closing), and defer 100% of the gain.

The deferred gain stays embedded in the replacement property's basis, reducing future depreciation but preserving full equity for reinvestment.

For UHNW investors, the true advantage is serial exchange strategies. By executing successive 1031 exchanges over decades, investors continuously upgrade portfolio quality, trading up from smaller assets into institutional-grade commercial or large multi-family holdings, while deferring the embedded gain indefinitely. Academic research estimates that the incremental present value of a 1031 exchange strategy ranges from 8% to 58% (mean 37%) of the deferred tax liability, depending on hold period and reinvestment assumptions. The Joint Committee on Taxation estimated that $9.9 billion in tax revenue was deferred in 2019 due to like-kind exchanges.

Key considerations for UHNW portfolios:

- Use qualified intermediaries to manage compliance and segregate exchange proceeds

- Plan identification strategies carefully when upgrading into larger assets

- Coordinate with property management and leasing teams to avoid boot (taxable cash or debt relief)

- Time exchanges to align with portfolio rebalancing and liquidity needs

Opportunity Zone Investments

Qualified Opportunity Zones (QOZ) offer a complementary strategy for UHNW investors with large realized capital gains from any source, not just real estate. By reinvesting gains into a Qualified Opportunity Fund (QOF) within 180 days, investors defer the original gain until December 31, 2026, or an earlier inclusion event. After a 10-year hold, the investor can elect to step up the basis of the QOF investment to fair market value, permanently excluding all appreciation on the QOF investment from capital gains tax.

For UHNW families deploying capital from business sales, stock liquidations, or real estate dispositions into long-term development projects or distressed community investments, QOZ offers permanent elimination of gain on the reinvested capital, provided the investment is held for a decade and the fund performs.

Independent fund viability assessment is critical. The tax benefit should complement, not replace, fundamental investment diligence.

Stepped-Up Basis at Death: The Ultimate Elimination

Under IRC §1014, heirs inherit property at fair market value as of the date of death, erasing all embedded capital gain and depreciation recapture. For UHNW families, the decision of when to sell versus hold through the estate carries significant tax consequences.

Consider: a property with $10 million in embedded gain and $5 million in recapture exposure transfers to heirs with a fresh $15 million basis, eliminating $3.6 million in federal tax (23.8% on gain, 25% on recapture).

The interplay between stepped-up basis, 1031 exchanges, and estate planning is complex. Exchanges preserve capital for growth during life; strategic holding through death eliminates the deferred tax entirely. Key timing factors include:

- Estate tax exposure and current exemption thresholds

- Near-term liquidity needs across the portfolio

- The investor's age, health, and generational transfer goals

Tax-Loss Harvesting in Real Estate Portfolios

UHNW investors with diversified holdings can strategically dispose of properties that have declined in value relative to adjusted basis, generating losses that offset gains elsewhere in the portfolio. Unlike publicly traded securities, real estate loss harvesting requires actual disposition (no wash-sale rule applies to real property), but the losses can offset both capital gains and, in some cases, ordinary income when combined with real estate professional status.

Income Tax Mitigation Through Real Estate

Beyond capital gains, UHNW real estate portfolios generate substantial rental and business income subject to ordinary income tax rates. Three IRS provisions—real estate professional status, the Qualified Business Income deduction, and Net Investment Income Tax planning—create powerful levers to reduce or eliminate this tax exposure.

Real Estate Professional Status (REPS)

Under IRC §469(c)(7), a taxpayer qualifies as a real estate professional by meeting two thresholds:

- More than 750 hours of services in real property trades or businesses during the year

- More than 50% of personal services performed in all trades or businesses are in real property

When these thresholds are met, real estate losses become non-passive and can offset ordinary income without limitation. For UHNW individuals with high W-2 income, business income, or investment income, this election unlocks enormous deduction capacity, especially when combined with cost segregation-driven paper losses.

Example: A UHNW investor with $5 million in W-2 income and $3 million in rental properties generates $1.2 million in first-year depreciation through cost segregation. Without REPS, this loss is passive and can only offset passive income. With REPS qualification (achieved by spending 751+ hours managing properties and real estate investments, and ensuring real estate represents the majority of working time), the $1.2 million loss offsets the $5 million W-2 income. That reduces taxable income to $3.8 million and saves approximately $490,000 in federal tax in year one.

REPS is particularly valuable for:

- UHNW spouses who dedicate full-time effort to managing the family's real estate portfolio

- Investors transitioning from active business careers into full-time real estate management

- Families with substantial cost segregation-driven losses and high-income earners

Qualified Business Income (QBI) Deduction

The Section 199A QBI deduction allows pass-through entities, including rental real estate structured as trades or businesses, to deduct up to 20% of qualified business income. For 2025, the deduction phases out at $394,600 for married filing jointly and $197,300 for single filers. The OBBBA made the QBI deduction permanent for taxable years beginning after December 31, 2025, adding a minimum $400 deduction for taxpayers with at least $1,000 of QBI.

For UHNW investors whose rental activities qualify as trades or businesses, the QBI deduction can reduce effective tax rates substantially. A portfolio generating $2 million in net rental income may qualify for a $400,000 deduction, saving $148,000 in federal tax at the top 37% rate. Meeting safe harbor requirements for hours of service and maintaining separate books are prerequisites.

Key requirements:

- 250+ hours of rental services per year

- Contemporaneous time logs and documentation

- Separate books and records for each rental activity

- Coordination with REPS election and material participation standards

Net Investment Income Tax (NIIT) Planning

The 3.8% NIIT applies to passive investment income for taxpayers exceeding MAGI thresholds ($250,000 MFJ, $200,000 single). Rental income from passive activities is generally subject to NIIT, adding nearly 4% to the effective tax rate on rental operations.

NIIT can be reduced or eliminated through:

- REPS election: Real estate professionals who participate more than 500 hours in rental activities can exclude rental income from NII

- Active participation structures: Materially participating in rental trades or businesses reclassifies income as non-passive

- Entity classification elections: Structuring rental activities to meet trade or business standards removes them from NIIT exposure

For UHNW investors with $10 million in net rental income, eliminating NIIT saves $380,000 annually. That figure alone justifies a thorough review of entity structure and participation status before year-end.

Entity Structuring and Wealth Transfer Strategies for UHNW Real Estate

UHNW real estate portfolios are rarely held in individual names. Multi-entity structures serve dual purposes: liability protection (isolating risk at the property level) and tax efficiency (controlling how income flows to owners, allocating depreciation, and managing transfer tax treatment).

Entity Structure Fundamentals

Typical structures include:

- LLCs: Provide liability protection, flexible ownership, and pass-through taxation; most common for individual properties

- Limited Partnerships (LPs): Allow centralized management with general partner control and limited partner passive ownership; ideal for family wealth transfers

- S Corporations: Enable REPS election for active shareholders and limit self-employment tax on distributions; less common but useful in specific contexts

The choice determines how income flows, how deductions are allocated among partners, and—critically—what transfer tax treatment applies when interests are gifted or inherited.

Family Limited Partnerships (FLPs) and Family LLCs

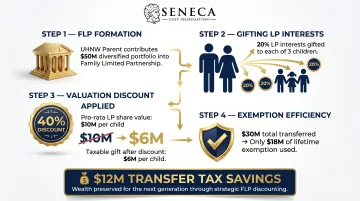

FLPs and Family LLCs are wealth transfer accelerants. By transferring limited partnership interests (or non-managing LLC membership interests) to heirs, UHNW families apply valuation discounts for lack of control and lack of marketability. A 40% combined discount is common; some appraisals support 50% or higher.

How it works: A UHNW parent holds a $50 million real estate portfolio in an FLP. The parent gifts 20% limited partnership interests (non-controlling, non-marketable) to three children. Each 20% interest has a pro-rata value of $10 million, but after applying a 40% combined discount, the taxable gift value is only $6 million per child. Over three gifts, $30 million in value transfers using only $18 million of lifetime exemption—a $12 million transfer tax savings.

Critical compliance requirements:

- Qualified independent appraisals prepared by credentialed appraisers

- Documented business purpose beyond tax avoidance

- Arm's-length management and distributions

- Avoid commingling personal and entity assets

Grantor Retained Annuity Trusts (GRATs)

GRATs allow a UHNW grantor to transfer appreciation on real property holdings to heirs with minimal gift tax. The grantor contributes property to the trust and receives a fixed annuity payment for a term of years. At the end of the term, remaining assets pass to beneficiaries.

The tax advantage: The value of the gift is calculated as the contributed property value minus the present value of the annuity payments (using the IRS Section 7520 rate). If the property appreciates faster than the 7520 rate, the excess appreciation transfers to heirs gift-tax-free.

Example: A grantor transfers a $10 million commercial property into a 10-year GRAT. The annuity payments (calculated at the 7520 rate of 5.6%) are structured to "zero out" the gift value. If the property appreciates at 8% annually, the grantor receives back the original $10 million value plus 5.6% growth via annuity payments, and the beneficiaries receive the 2.4% annual excess—approximately $2.7 million—free of gift and estate tax.

GRATs are best suited when:

- The contributed asset has strong near-term appreciation potential

- Current 7520 rates are low (making the hurdle rate easier to clear)

- The grantor has a long enough time horizon to survive the trust term

Intentionally Defective Grantor Trusts (IDGTs)

IDGTs allow a grantor to sell appreciating property to an irrevocable trust in exchange for a promissory note, freezing the estate value while transferring future growth to beneficiaries.

The trust is "defective" for income tax purposes—the grantor pays income tax on trust earnings—but fully respected for estate tax purposes, removing those assets from the taxable estate.

Advantages:

- The sale is not a taxable event (grantor and trust are the same taxpayer for income tax)

- The grantor pays income tax on trust income, allowing the trust assets to grow without tax erosion

- Future appreciation escapes estate tax entirely

Example: A UHNW investor sells a $20 million multi-family portfolio to an IDGT in exchange for a 10-year, 5% promissory note. The trust pays annual interest and principal from rental income. Over 10 years, the property appreciates to $35 million. The $15 million appreciation is removed from the grantor's estate, saving approximately $6 million in estate tax (at 40% rate). The grantor continues to pay income tax on rental income, further reducing the taxable estate.

Dynasty Trusts

Dynasty Trusts hold assets across multiple generations while avoiding estate and generation-skipping transfer (GST) taxes at each generational shift. Established in favorable jurisdictions (South Dakota, Nevada, Delaware, Alaska), dynasty trusts can persist for hundreds of years or in perpetuity.

Mechanics:

- The grantor funds the trust with real estate or other assets, using lifetime GST exemption to shelter the transfer

- The trust holds and manages assets for the benefit of multiple generations

- At each generation, no estate or GST tax is due; assets remain in trust

- For 2025, the GST exemption is $13,990,000; the OBBBA increased it to $15,000,000 for 2026, indexed thereafter

Why this matters: A UHNW family that funds a dynasty trust with $15 million in real estate in 2026 (using the full GST exemption) and achieves 6% annual appreciation will hold $103 million after 30 years, $243 million after 50 years—all free of estate and GST tax. That tax-free compounding gap widens with every decade the trust remains intact, which is the entire point.

Step-Up in Basis and Estate Planning Integration

The entity structures and trusts above focus on transferring assets efficiently—but the basis reset available at death changes the math on when to transfer versus when to hold.

For UHNW families who have accumulated significant depreciation deductions (including cost segregation write-offs), the stepped-up basis at death resets the heir's cost basis to current market value. This eliminates embedded capital gains and wipes out depreciation recapture liability.

In practice, it rewards families for holding appreciated property through death rather than selling during life.

Strategic implication: The decision of when to sell versus when to hold becomes a high-stakes timing question. If a UHNW investor expects to live another 10-20 years, holding property through death may eliminate $10 million in embedded gain and $3 million in recapture exposure, saving heirs $3.3 million in federal tax—more than compensating for any estate tax due (particularly if estate planning tools like FLPs and GRATs have reduced the taxable estate).

Building a Coordinated UHNW Real Estate Tax Strategy

None of these strategies works in isolation. The most effective UHNW real estate tax planning stacks complementary tools into an integrated, multi-year strategy that compounds savings across income tax, capital gains, and estate tax domains.

Hypothetical 10-Year Strategy Sequence

Year 1-2: Acquire $30 million multi-family portfolio. Commission cost segregation studies, reclassify $7.5 million into bonus-eligible assets, claim $7.5 million in first-year depreciation. Qualify for REPS, offset $4 million in ordinary income from business interests, saving $1.5 million in federal tax. Establish Family LLC to hold properties.

Year 3-4: Gift 30% non-managing LLC interests to three children using FLP valuation discounts. $9 million pro-rata value reduced to $5.4 million taxable gift (40% discount). Fund GRAT with appreciated property, zero out gift value, begin annuity payments.

Year 5-7: Execute 1031 exchange, sell original $30 million portfolio (now worth $40 million), roll proceeds into $45 million institutional-grade commercial property. Defer $10 million capital gain and $2.5 million depreciation recapture. Commission new cost segregation study on replacement property, generate $9 million in new first-year deductions.

Year 8-10: Establish Dynasty Trust in South Dakota, contribute $15 million in appreciated real estate using lifetime GST exemption. Trust holds assets for grandchildren and future generations, avoiding estate tax at each generational transition. Grantor continues to pay income tax on trust earnings, reducing taxable estate by $500,000 annually.

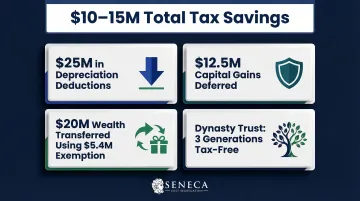

Net result over 10 years:

- $25 million in depreciation deductions offsetting high-bracket income

- $12.5 million in capital gains and recapture deferred indefinitely

- $20 million in wealth transferred out of the taxable estate using only $5.4 million of exemption

- A dynasty trust positioned to grow tax-free for three generations

Total tax savings: conservatively $10–15 million in present value terms.

The Professional Team

Executing this level of planning requires a coordinated team:

- Tax attorney — Drafts and maintains entity structures (FLPs, GRATs, IDGTs, Dynasty Trusts) and ensures transfer tax compliance and valuation standards

- CPA specializing in real estate taxation — Manages REPS qualification, passive activity tracking, QBI elections, and annual filings; coordinates with cost segregation engineers on study integration

- Cost segregation firm — Provides the engineering analysis, asset classification, and photographic documentation required to support accelerated depreciation claims; Seneca Cost Segregation has completed over 10,200 studies nationwide and backs every study with an audit-defense guarantee

- Wealth advisor — Integrates real estate tax planning with estate planning, liquidity management, and portfolio allocation across the family office or RIA

- Qualified intermediary — Manages 1031 exchange proceeds, identification timelines, and closing coordination to maintain IRS compliance

This team must communicate regularly — quarterly at minimum, and more frequently during acquisition or disposition cycles. A cost segregation decision in January ripples into tax planning in April, entity structure in June, and estate gifting in December. Without that coordination, opportunities are lost and compliance risks compound. The upside when everyone is aligned: every tool reinforces the next.

Frequently Asked Questions

What is considered ultra-high net worth?

Ultra-high-net-worth is generally defined as having $30 million or more in investable assets, excluding primary residence. This distinguishes UHNW from high-net-worth ($1M+ investable assets) and very-high-net-worth ($5M–$30M) classifications, and determines access to advanced tax planning strategies and specialized financial services.

How do ultra-high-net-worth individuals avoid estate taxes?

UHNW individuals reduce estate taxes by using the lifetime estate and gift tax exemption ($13.99 million in 2025, $15 million in 2026 under OBBBA) and transferring assets through Dynasty Trusts and GRATs to remove future appreciation from the taxable estate. FLP valuation discounts reduce taxable gift values further, while the stepped-up basis at death eliminates embedded capital gains and depreciation recapture for heirs.

Do ultra-high-net-worth individuals pay property taxes?

Yes, UHNW individuals pay property taxes on all real estate holdings. These taxes are deductible as a business expense on investment and commercial properties, though personal residences are subject to the $10,000 SALT deduction cap under current law. Strategic ownership structures like LLCs provide liability protection but do not eliminate the property tax obligation.

How does cost segregation benefit large real estate portfolios specifically?

At the UHNW level, cost segregation studies on large commercial or multi-family assets reclassify a greater absolute dollar amount of property value into accelerated depreciation categories, generating larger front-loaded deductions that can offset substantial ordinary income. The ROI on a study is significantly higher for UHNW investors because the reclassified value is proportionately larger and the tax savings apply at the top marginal rates (37% federal plus 3.8% NIIT).

What is the difference between a 1031 exchange and an Opportunity Zone investment for deferring capital gains?

A 1031 exchange defers gains indefinitely by rolling proceeds into like-kind real property, with no limit on the number of successive exchanges. An Opportunity Zone investment defers the original gain by reinvesting into a QOF within 180 days. After a 10-year hold, taxes on the QOF investment's appreciation are eliminated entirely. Opportunity Zones suit investors willing to commit capital long-term who want permanent elimination rather than indefinite deferral.

Can real estate losses offset ordinary income for ultra-high-net-worth investors?

Under standard passive activity rules, real estate losses can only offset passive income. However, UHNW investors who qualify as real estate professionals (750-hour and 50%-of-working-time thresholds under IRC §469(c)(7)) can treat those losses as non-passive. That allows large depreciation-driven losses from cost segregation studies to directly offset ordinary income — wages, business income, or investment income — without limitation.

Coordinated planning is what separates meaningful tax savings from marginal ones at the UHNW level. Combining cost segregation, capital gains deferral, income mitigation, and wealth transfer strategies — executed by a team of attorneys, CPAs, and engineers — can preserve tens of millions across generations. Seneca Cost Segregation brings engineering-based methodology, 10,200+ completed studies, and audit-defense guarantees to that process. To explore how cost segregation fits your portfolio, contact Seneca at 530-797-6539 or visit senecacostseg.com.