2026 presents a particularly powerful window. The One Big Beautiful Bill Act permanently restored 100% bonus depreciation for qualifying property acquired after January 19, 2025, eliminating the phase-down schedule that was reducing this benefit through 2025. Combined with cost segregation, STR owners can now front-load massive deductions and offset W-2 and business income—without needing Real Estate Professional Status.

This guide covers the two-part strategy: (1) qualifying your STR under the IRS's non-passive classification rules, and (2) combining cost segregation with 100% bonus depreciation to create immediate, defensible deductions that materially reduce your tax burden in year one.

TLDR

- 100% bonus depreciation was permanently restored for property acquired after January 19, 2025—no phase-down

- STRs with average guest stays of 7 days or fewer are non-passive under IRC §469, so losses can offset W-2 and business income when you materially participate

- Cost segregation reclassifies 20–40% of property components into shorter depreciation schedules, making them eligible for immediate first-year write-off

- Properties above $300,000 typically generate first-year tax savings that far exceed study costs

- Prior-year properties qualify via look-back studies using IRS Form 3115—no amended returns required

Why Short-Term Rentals Get Unique Tax Treatment in 2026

Under IRC §469, rental income is normally classified as passive, meaning losses can only offset other passive income—not W-2 wages or active business income. STRs with average stays of 7 days or fewer are explicitly excepted from this classification, meaning their losses function like active business losses when you meet material participation requirements.

The Permanent 100% Bonus Depreciation Window

The One Big Beautiful Bill Act (Public Law 119-21) permanently restored 100% bonus depreciation for qualifying property acquired and placed in service after January 19, 2025. This means STR owners are no longer racing against a phase-down schedule. The full first-year write-off of qualifying components is now a stable, long-term planning tool.

You Don't Need Real Estate Professional Status

This is the most common misconception among STR investors: many assume they need REPS to unlock these benefits. They don't.

The STR exception under IRC §469 is a separate legal path from REPS entirely. Here's how the two compare:

- REPS: Requires 750+ hours annually in real estate activities, plus more time in real estate than any other activity — a bar most W-2 employees can't clear

- STR exception: Requires average guest stays of 7 days or fewer and material participation — no 750-hour threshold

Meet those STR conditions, and your losses become non-passive regardless of REPS status.

The "Paper Loss" Advantage

Accelerated depreciation creates large deductions without actual cash outflows. A property generating positive cash flow can simultaneously show a significant "paper loss" that reduces taxable income. The IRS built this into the tax code as a capital timing mechanism — not a workaround.

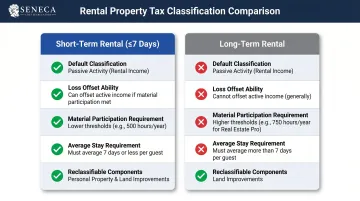

Comparison: STR vs. Long-Term Rental

| Dimension | Short-Term Rental (≤7 days) | Long-Term Rental |

|---|---|---|

| Average Stay Requirement | 7 days or fewer | N/A |

| Default Classification | Non-passive (if materially participating) | Passive |

| Loss Offset Ability | Can offset W-2 and business income | Only offsets other passive income (unless REPS) |

| Material Participation Requirement | Yes (500 hours, or 100 hours + no one else does more) | Requires REPS (750 hours + more than any other activity) |

| Typical Reclassifiable Components | 20–40% (furnishings, appliances, outdoor amenities) | Lower (typically unfurnished) |

The 7-Day Rule and Material Participation Requirements

Calculating Your Average Period of Customer Use

The IRS formula: total rental days ÷ total number of rental periods = average stay. If the result is 7 days or fewer, the property qualifies under the short-term exception.

This must be recalculated every tax year. If the average exceeds 7 days in any given year, the activity reverts to passive treatment and losses become restricted. The booking platform (Airbnb, VRBO, direct) is irrelevant—the IRS evaluates stay length from booking records alone.

30-Day Exception: If the average stay is between 8 and 30 days AND significant personal services are provided (daily cleaning, concierge, meals), the property may still qualify. Most investors structure under the 7-day rule rather than rely on this harder-to-document path.

Meeting the Material Participation Tests

You need to meet only one of three practical tests under Treasury Regulation §1.469-5T:

- 500+ hours in the rental activity during the tax year

- 100+ hours AND no other individual spends more time on the activity than you

- Substantially all participation in the activity is performed by you

What counts as qualifying hours:

- Guest communications and booking management

- Pricing strategy and listing optimization

- Maintenance coordination and vendor management

- Financial review and bookkeeping

- Property inspection and oversight

Contemporaneous Documentation Is Critical

Participation logs must be recorded at the time activities occur—not reconstructed later. In Moss v. Commissioner (135 T.C. 365, 2010), the Tax Court rejected a summary of time spent on rental properties prepared years later, stating that regulations "do not allow a postevent 'ballpark guesstimate.'"

That standard held in Lucero v. Commissioner (T.C. Memo 2020-136), where the court rejected a log created during IRS Appeals to reconstruct hours using invoices and receipts. The IRS consistently treats after-the-fact documentation as unreliable, regardless of how well it is supported by secondary records.

Start a dedicated time-tracking method from day one of ownership. Record the date, hours, and a brief activity description for each entry.

Personal Use Limit Under IRC §280A

Material participation qualifies you to deduct losses—but personal use of the property introduces a separate constraint. Under IRC §280A, vacation home rules apply when personal use exceeds the greater of:

- 14 days per year, or

- 10% of total rental days

Once triggered, these rules can limit or eliminate deductible losses. STR owners who also use the property personally must track and segregate rental versus personal days from the start of each tax year to keep the strategy intact.

Cost Segregation + 100% Bonus Depreciation: The Full Strategy

How a Cost Segregation Study Works

A cost segregation study is an engineering-based analysis that identifies which property components can be reclassified from the standard 27.5-year (residential) or 39-year (nonresidential) depreciation schedule into 5-, 7-, or 15-year schedules.

The process:

- Engage a certified cost segregation provider – Look for CCSP certification from the American Society of Cost Segregation Professionals, which requires 7,000 hours of direct experience and passing a rigorous exam.

- Supply property records – Purchase documents, architectural plans, contractor invoices, and settlement statements.

- Engineering analysis and site review – The engineering team identifies reclassifiable components through detailed property inspection.

- Asset reclassification – Components are moved into accelerated schedules based on IRS asset classification rules.

- Delivery of compliant study report – The report integrates directly into your tax return via your CPA.

- Bonus depreciation election – Your CPA files the election to take 100% first-year deduction on reclassified assets.

To see what these six steps produce in practice, consider a typical STR acquisition. Seneca Cost Segregation's studies — completed in 2–4 weeks with AuditDefense and a money-back guarantee — average a first-year deduction of $171,243 across 10,200+ properties nationwide.

Illustrative Example: $750,000 STR Acquisition

- Land value: $150,000 (not depreciable)

- Building basis: $600,000

Standard depreciation:

- $600,000 ÷ 27.5 years = $21,818/year

After cost segregation (30% reclassified):

- Reclassified assets: $180,000 (5-, 7-, 15-year property)

- Remaining building: $420,000 (27.5-year property)

With 100% bonus depreciation:

- First-year deduction on reclassified assets: $180,000

- First-year building depreciation: $15,273 ($420,000 ÷ 27.5)

- Total first-year deduction: $195,273

Tax savings at 35% combined rate: $68,346 in year one

Illustrative only — actual results vary by property characteristics, component mix, and state conformity.

Look-Back Studies and Prior-Year Properties

STR owners who purchased properties in prior years can still access this strategy. A look-back cost segregation study using IRS Form 3115 (Change in Accounting Method) allows all missed accelerated depreciation from prior years to be claimed as a single catch-up deduction in the current tax year — without amending prior returns.

For a property held five or more years, that catch-up can dwarf a single year's standard deduction.

State Conformity Caution

Not all states conform to federal bonus depreciation rules. Several states require add-back adjustments or phase deductions differently:

| State | Treatment | Impact |

|---|---|---|

| North Carolina | Add-back 85%; subtract 20%/year for 5 years | Federal benefit spread over 5 years |

| Minnesota | Add-back 80%; subtract 20%/year for 5 years | Federal benefit spread over 5 years |

| Florida | Add-back 100%; subtract 1/7th per year for 7 years | Federal benefit spread over 7 years |

Model state-level impact with your CPA before finalizing acquisition economics or filing.

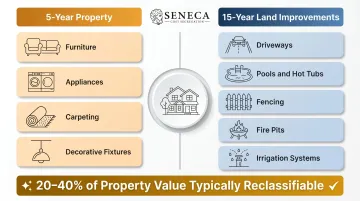

STR Components That Qualify for Accelerated Depreciation

5-Year Property

- Furniture (beds, sofas, dining sets, outdoor furniture)

- Appliances (refrigerators, dishwashers, ranges, microwaves)

- Carpeting and vinyl flooring

- Decorative fixtures and specialty finishes

These assets are the most common starting point for STR cost segregation — and often account for the largest share of reclassified value.

15-Year Land Improvements

- Driveways, walkways, and fencing

- Retaining walls and landscaping

- Pools, hot tubs, and outdoor kitchens

- Fire pits and irrigation systems

Why STRs Qualify More Components

STRs are typically furnished, amenity-rich, and improvement-intensive. Every piece of furniture, appliance, and outdoor feature is a potential accelerated depreciation asset. A comparable unfurnished long-term rental has far fewer qualifying components — which means cost segregation unlocks a larger share of deductions on an STR dollar-for-dollar than on most other residential property types.

Mistakes That Kill Your STR Depreciation Strategy

Skipping the Annual Average Stay Check

Many investors assume their property qualifies at purchase and never verify again. If a shift in booking strategy—longer minimums, seasonal policy changes—pushes the average stay above 7 days in any tax year, the losses revert to passive and cannot offset active income. Export booking records and recalculate the formula each year.

Rebuilding Participation Logs After the Fact

The IRS and Tax Court have disallowed material participation claims specifically because logs were clearly assembled after the fact. A time-tracking app, calendar record, or even a dated spreadsheet maintained in real time is far more defensible than end-of-year recollections.

Overlooking Depreciation Recapture at Sale

Accelerated depreciation shifts when you pay tax — it doesn't eliminate the liability. Upon sale, unrecaptured Section 1250 gain may be taxed at up to 25% federally. Model this before acquisition, and plan your exit strategy—1031 exchange, installment sale, or long-term hold—from day one.

Frequently Asked Questions

Does 100% bonus depreciation apply to STR properties I purchased before January 2025?

The permanent 100% rate applies to qualifying property acquired after January 19, 2025. However, owners of earlier acquisitions can still benefit from accelerated depreciation schedules through a cost segregation look-back study, claiming all missed depreciation in the current tax year via IRS Form 3115.

Do I need Real Estate Professional Status to use the STR depreciation strategy?

No. REPS is not required. The STR exception under IRC §469 is a separate legal path—it requires average stays of 7 days or fewer and material participation, not the 750-hour REPS threshold.

What happens to my accelerated depreciation deductions when I sell my STR?

Depreciation is recaptured upon sale, with unrecaptured Section 1250 gain taxed at up to 25% federally. Common mitigation strategies include a 1031 exchange into like-kind property, installment sale structuring, or a long-term hold plan. Each option carries different tax implications and should be evaluated with your CPA before you close on a property.

How exactly do I calculate my average period of customer use?

Total rental days ÷ total number of rental periods. This must be recalculated annually from actual booking records—the result must be 7 days or fewer each year for the non-passive classification to hold.

Is the STR depreciation strategy legal and audit-defensible?

Yes. The strategy is fully legal and explicitly grounded in IRC §469 and IRS Publication 925. Defensibility depends on accurate average stay documentation, contemporaneous participation logs, and a cost segregation report prepared by a licensed engineer using ASCSP-certified methodology.

What property value threshold makes a cost segregation study financially worthwhile for an STR?

Cost segregation generally makes financial sense for properties valued at $300,000 or above, where first-year tax savings typically deliver a multiple of the study cost. Below that threshold, study fees may consume too much of the benefit to justify the engagement.