Introduction

Most real estate investors face a familiar frustration: you buy a $2 million property, but the IRS makes you wait 27.5 or 39 years to claim the full tax benefit — even though the appliances, flooring, and HVAC systems wear out far sooner. That slow depreciation schedule locks up valuable deductions for decades, forcing higher tax bills while other investors find ways to accelerate their savings.

Cost segregation solves this problem. It's an IRS-approved, engineering-based strategy that reclassifies property components into shorter depreciation schedules of 5, 7, or 15 years instead of 27.5 or 39, legally reducing taxable income and improving cash flow in the early years of ownership.

With 100% bonus depreciation reinstated for properties acquired and placed in service after January 19, 2025, investors who combine both strategies can write off a significant portion of a property's cost in year one rather than spreading it across decades.

This article explains what a cost segregation study is, how the process works step by step, who benefits most, and when it makes financial sense to pursue one.

TLDR

- Cost segregation reclassifies building components into 5-, 7-, or 15-year depreciation categories, rather than the standard 27.5 or 39 years

- Bonus depreciation was reinstated at 100% under the One Big Beautiful Bill for assets acquired and placed in service on or after January 19, 2025; the TCJA phase-down applies to assets acquired before that date

- Investors average $171,243 in first-year deductions across 10,200+ completed studies

- Strongest ROI on properties with a $300K+ depreciable basis owned five or more years

- IRS Form 3115 allows retroactive claims without amending prior returns

What Is a Cost Segregation Study?

A cost segregation study is a detailed tax and engineering analysis that breaks a property into its individual components, each with its own IRS-recognized depreciable life, rather than treating the entire building as a single asset on a slow straight-line schedule. The result: property owners front-load depreciation deductions into the early years of ownership, freeing up capital when it's most useful.

The Baseline: Standard Depreciation

Under the Modified Accelerated Cost Recovery System (MACRS), real property defaults to slow depreciation schedules. Residential rental properties (where 80% or more of gross rental income comes from dwelling units) depreciate over 27.5 years. Commercial properties (office buildings, stores, warehouses) depreciate over 39 years. Cost segregation accelerates that timeline by reclassifying eligible components into shorter depreciation categories.

The Core Reclassification

Cost segregation identifies components that qualify for accelerated depreciation:

5-Year Property:

- Carpeting and flooring

- Appliances (refrigerators, dishwashers, ranges)

- Specialty electrical connections dedicated to equipment

- Decorative millwork and wall coverings

7-Year Property:

- Office furniture and fixtures

- Decorative lighting not part of the building structure

- Movable partitions

15-Year Property:

- Landscaping and site improvements

- Parking lots and paving

- Outdoor lighting and security systems

- Sidewalks, fences, and retaining walls

Legal Foundation and IRS Compliance

This is not a tax loophole. Cost segregation methodology is grounded in the 1997 Tax Court ruling Hospital Corporation of America v. Commissioner (109 T.C. 21), which validated engineering-based segregation of tangible personal property from structural components. The IRS subsequently issued its Cost Segregation Audit Techniques Guide (Publication 5653), establishing 13 quality standards for defensible studies.

The guide explicitly warns against "rule of thumb" approaches that rely on fixed percentages. A defensible study must include:

- Preparation by qualified engineers

- Detailed methodology descriptions

- Physical site inspections

- Engineering "take-offs" (quantity and cost measurements)

- Reconciliation of allocated costs to total actual costs

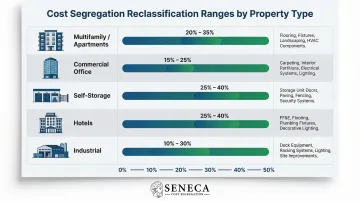

Typical Reclassification Ranges by Property Type

Based on engineering study data across property types, reclassification ranges follow consistent patterns:

| Property Type | Typical Reclassification | Key Components |

|---|---|---|

| Multifamily / Apartments | 20-35% | Appliances, carpeting, cabinetry, parking lots |

| Commercial Office | 15-25% | Specialty lighting, electrical systems, fixtures |

| Self-Storage | 25-40% | Unit partitions, roll-up doors, security systems |

| Hotels | 25-40% | FF&E, decorative finishes, pools |

| Industrial | 10-30% | Heavy machinery installations, dedicated HVAC |

Self-storage and hotels consistently land at the higher end because their builds include extensive site improvements, specialized fixtures, and personal property that separates cleanly from the structural shell.

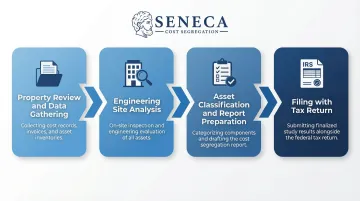

How a Cost Segregation Study Works: The Step-by-Step Process

Step 1: Property Review and Data Gathering

The study begins with collecting construction records, blueprints, purchase agreements, and cost documentation. Essential documents include:

- Closing statement (HUD-1) establishing purchase price and acquisition date

- Property appraisal separating land value from building value

- Construction contracts and AIA forms G-702/G-703 showing itemized costs

- Renovation receipts and contractor invoices

If original cost records are unavailable, engineers use estimation techniques based on current-cost databases and industry benchmarks, though this increases study costs and reduces precision.

Step 2: Engineering Site Analysis

A qualified engineer physically inspects and documents the property, identifying every component and its cost basis. This site visit differentiates a full engineering-based study from a "rule of thumb" approach.

Why engineering matters: The IRS explicitly favors engineering-based studies because they provide itemized quantity takeoffs, photographic documentation, and component-level cost allocations. Studies without physical inspections face higher audit risk and a greater chance of IRS adjustments.

The engineer catalogs:

- Building systems (HVAC, plumbing, electrical)

- Interior finishes (flooring, cabinetry, fixtures)

- Site improvements (parking, landscaping, fencing)

- Specialty equipment and installations

Step 3: Asset Classification and Report Preparation

Each identified component is assigned to the correct IRS asset class (5-, 7-, 15-year, or structural 27.5/39-year). The final report includes:

- Executive summary of findings and tax impact

- Detailed asset lists with cost allocations

- Engineering methodology and supporting calculations

- Photographic documentation

- Reconciliation to total purchase price

- IRS authority references (Revenue Procedures, case law)

This comprehensive documentation serves as audit defense if the IRS questions the reclassification.

Step 4: Filing with Your Tax Return

Once the report is complete, depreciation adjustments are applied on Form 4562 (Depreciation and Amortization), typically in the year the property is placed in service. For properties already owned, changes are made via IRS Form 3115 (detailed in a later section).

Seneca Cost Segregation follows this same framework with CCSP-certified professionals and licensed engineers who adhere to the IRS Cost Segregation Audit Techniques Guide. Their proprietary technology supports compliance while keeping study timelines to 2-4 weeks. With over 10,200 studies completed nationwide, the firm has built a process that pairs thoroughness with efficiency.

Key Tax Benefits of a Cost Segregation Study

Accelerated Depreciation Deductions

By moving a portion of a property's cost basis into 5-, 7-, and 15-year classes, investors claim significantly larger deductions in the first few years of ownership rather than spreading them evenly over decades.

Bonus Depreciation Amplifies the Effect

Assets with a depreciable life of 20 years or less generally qualify for bonus depreciation under IRC §168(k). The bonus depreciation percentage applicable to qualifying assets has changed over time under the Tax Cuts and Jobs Act (TCJA) and subsequent legislation:

| Period | Bonus Depreciation Rate |

|---|---|

| September 27, 2017 – December 31, 2022 | 100% |

| January 1, 2023 – December 31, 2023 | 80% |

| January 1, 2024 – December 31, 2024 | 60% |

| January 1, 2025 – January 18, 2025 | 40% |

| January 19, 2025 – December 31, 2030 | 100% (if acquisition date is January 19, 2025 or later) |

The One Big Beautiful Bill (H.R.1, enacted July 4, 2025) permanently restored 100% bonus depreciation for assets acquired and placed in service after January 19, 2025.

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

This means qualifying components identified through cost segregation with an acquisition date of January 19, 2025 or later can be written off entirely in year one.

Example: Residential Property Placed in Service in 2024

Assuming someone placed a residential property with the following details in service in 2024: Purchase: $1,000,000 Improvements made: $50,000 Land value: $150,000 Cost basis: $900,000 (Purchase + Improvements – Land value)

If you were to depreciate the property using standard straight-line depreciation, you'd allocate the $900,000 linearly over 27.5 years, giving you a per-year depreciation of $32,727.27.

Now, assume we do a cost segregation study on the property and find that 12% of the cost basis is personal property, 16% is site improvements, and 72% is real property.

12% of $900,000 = $108,000 16% of $900,000 = $144,000 72% of $900,000 = $648,000

Because you placed the property in service in 2024, it qualifies for 60% bonus depreciation, and the treatment is as follows:

$108,000 x 60% = $64,800. The remaining 40% comes in over the next 5 years. $144,000 x 60% = $86,400. The remaining 40% comes in over the next 15 years. Real Property / 27.5 years = $648,000 / 27.5 = $23,563.64 every year until Year 28

The total 1st year deduction = $64,800 + $86,400 + $23,563.64 = $174,763.64

The Additional First Year Depreciation Deduction = $174,763.64 – $32,727.27 = $142,036.37

You'll then get a tax deduction of $142,036.37 instead of $32,727.27. At a 37% federal tax rate, this nets a check from the IRS for $52,553.46.

Reduced Taxable Income and Improved Cash Flow

Larger upfront deductions lower taxable income, reducing current-year tax liability. This keeps more cash in hand to:

- Reinvest into the next property acquisition

- Fund renovations or capital improvements

- Pay down debt faster

- Cover operating expenses without drawing reserves

Rather than sending money to the IRS and waiting decades to recoup it, investors use those funds immediately.

Partial Asset Disposition

When segregated short-lived components (roofing, HVAC, flooring) are replaced, investors can write off the remaining undepreciated basis of the old component rather than continuing to depreciate an asset that no longer exists.

Example: If you replace a $30,000 HVAC system after 10 years, you can immediately deduct the remaining $15,000 undepreciated basis rather than continuing to depreciate it over the next 20+ years. Every major replacement over your holding period is another opportunity to accelerate deductions.

Strategic Sale Planning (Purchase Price Allocation)

Because a cost-segregated property is treated as a "basket of assets," sellers can strategically allocate less value to shorter-lived assets at sale, minimizing ordinary income from depreciation recapture and maximizing lower-taxed capital gains treatment.

Understanding how recapture works at sale helps you plan the allocation strategically:

Recapture rules:

- Section 1245 property (5- and 7-year assets): Taxed as ordinary income

- Section 1250 property (real property): Unrecaptured gain capped at 25%

- Capital gains: Taxed at preferential long-term rates

Proper allocation planning with your CPA can meaningfully reduce the tax exposure when you eventually sell.

Who Should Get a Cost Segregation Study?

Property Types and Ownership Scenarios

Cost segregation delivers the strongest ROI for:

Property types:

- Commercial buildings (office, retail, industrial)

- Multi-family apartment complexes

- Short-term rentals (Airbnb, VRBO)

- Single-family rentals

- Hotels and hospitality properties

- Self-storage facilities

- Owner-occupied businesses

Timing scenarios:

- Newly purchased properties

- Recently completed construction or renovation projects

- Properties acquired within the past 10 years (retroactive studies)

Minimum Property Value Threshold

Most specialists recommend a depreciable basis of $300,000 to $500,000 before the study ROI makes economic sense. Below this threshold, professional fees ($5,000 to $15,000 typically) may exceed the net present value of accelerated tax benefits.

For commercial properties with 39-year depreciation schedules, the recommended minimum is closer to $750,000 due to the longer baseline depreciation period.

Holding Period Matters

Investors planning to hold a property for at least 5 years tend to benefit most. Those planning to sell quickly may face depreciation recapture that offsets savings, though strategic planning can mitigate this.

Real estate professional status is another factor worth flagging. Investors who meet the IRS definition — 750+ hours per year in real property trades with material participation — can use cost segregation losses to offset non-passive income like W-2 wages, which substantially boosts those savings.

When It May Be Less Beneficial

Not every property or investor is a strong candidate. Cost segregation may not make sense for:

- Investors planning to sell within 1-2 years without a recapture strategy

- Properties where most depreciation has already been fully claimed

- Properties with inadequate documentation requiring expensive estimation work

- Depreciable basis below $300K–$500K, where fees may outweigh the tax benefit

A quick assessment from a qualified cost segregation specialist can clarify whether the numbers work for a given property situation.

Is a Cost Segregation Study Worth It?

Addressing the "Timing Difference" Concern

Some investors hesitate because cost segregation accelerates deductions now but depreciation recapture taxes apply when the property is sold. This concern is real, but the time-value of money typically makes it worthwhile.

Why it still pays:

- A dollar of tax saved today is worth more than a dollar of tax paid later

- Reinvesting those savings generates compounding returns

- Many investors use 1031 exchanges to defer recapture indefinitely

- The difference between 25% recapture rate and current ordinary income rates often favors acceleration

ROI Benchmark: Real-World Performance

Seneca Cost Segregation has achieved an average first-year deduction of $171,243 across more than 10,200 studies nationwide. This benchmark illustrates the substantial upfront savings available for investors across property types, though individual results depend on property characteristics, cost basis, and holding strategy.

Case study snapshot:

- Retail center ($13.5M basis): $1,168,876 first-year tax savings, 95.5:1 ROI

- Multifamily portfolio ($390M basis): $90M reclassified, $36M first-year cash benefit

- Commercial office ($15M basis): $2.6M first-year savings on $20K study fee (13,000% ROI)

Results vary by property type, cost basis, and holding strategy, but across 10,200+ studies, the pattern is consistent: engineering-based reclassification delivers meaningful first-year cash benefits.

Audit Protection as a Key Consideration

Strong ROI numbers only hold up if the study itself is IRS-defensible. A professionally prepared, engineering-based study with comprehensive documentation is your strongest protection if the IRS questions a reclassification. Characteristics of a qualified provider include:

- CCSP-certified professionals

- Licensed engineers on staff

- IRS-compliant methodology following the Audit Techniques Guide

- Explicit audit defense commitment with money-back guarantees

- Flat-fee pricing (not contingency-based fees, which signal to the IRS that results may be inflated)

Seneca Cost Segregation backs every study with an AuditDefense guarantee, meaning if the IRS challenges a reclassification, their team responds on your behalf at no additional cost.

How to Claim Missed Deductions: IRS Form 3115

Investors who did NOT perform a cost segregation study in the year they acquired a property can still capture those missed deductions by filing a change in accounting method using IRS Form 3115.

The Catch-Up Mechanism

Form 3115 allows a Section 481(a) adjustment: all the accelerated depreciation that should have been claimed in prior years is taken as a single deduction in the current tax year, without amending prior returns.

This is a legitimate, IRS-approved process, yet most real estate investors don't know it exists until years of deductions have already slipped by.

Timeline Example

- Property purchased: 2022

- No cost segregation performed at acquisition

- Study completed: 2025

- Result: All missed depreciation from 2022-2024 is claimed as a catch-up deduction on the 2025 return

Optimal Timing

The study is most impactful on properties acquired, built, or substantially renovated within the past several years. While you can go back up to 10 years, the time value of money favors acting sooner rather than later.

Filing Requirements

Form 3115 requires filing a duplicate copy with the IRS in Ogden, UT, alongside the original attached to your timely filed tax return. Errors in this process (missed deadlines, incorrect attachments, or miscalculated adjustments) can result in IRS rejection of the entire catch-up deduction. Most DIY platforms do not handle Form 3115 correctly.

Frequently Asked Questions

How does cost segregation work?

An engineering team identifies and reclassifies individual property components into 5-, 7-, or 15-year depreciation categories (rather than 27.5 or 39 years), allowing investors to claim much larger tax deductions in the early years of ownership through accelerated depreciation and bonus depreciation.

Is it worth it to do cost segregation?

For most investors holding a property worth $300K+ in depreciable basis for 5+ years, the upfront tax savings typically far outweigh the cost of the study. The reinvestment opportunity from improved cash flow adds further long-term value, and the advantage compounds when paired with 100% bonus depreciation.

Can you do a cost segregation on a rental property?

Yes. Both residential rental properties (single-family, multi-family) and commercial properties qualify. The strategy applies to any income-producing real estate, including short-term and long-term rentals, as long as the property meets the minimum depreciable basis threshold.

Can you take bonus depreciation on cost segregation study?

Yes. Assets identified through cost segregation with a useful life of 20 years or less generally qualify for bonus depreciation. 100% bonus depreciation has been reinstated for qualifying assets acquired and placed in service after January 19, 2025 under the One Big Beautiful Bill. The TCJA phase-down is still in effect; if a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Do you have to pay back cost segregation?

Cost segregation does not need to be "paid back" directly, but when a property is sold, depreciation recapture taxes apply to the accelerated deductions taken. Real property recapture is typically taxed at 25%, while personal property faces ordinary income rates — a key reason to factor in your exit strategy and 1031 exchange options before selling.

What is IRS Form 3115 used for?

Form 3115 (Application for Change in Accounting Method) lets property owners retroactively apply cost segregation to a property they already own, capturing all missed accelerated depreciation as a single catch-up deduction in the current tax year — no amended returns required.