This scenario plays out for thousands of real estate investors every year. The passive activity loss (PAL) rules under IRC Section 469 create a wall between rental losses and active income—but there are two key doors through that wall: the $25,000 special allowance for active participants and Real Estate Professional (REP) status. Understanding these rules determines whether your rental losses provide immediate tax relief or accumulate for years.

This article explains how PAL rules work in 2026, who qualifies for the $25,000 allowance and REP status, how suspended losses accumulate and when they're released, and actionable strategies to maximize your deductions.

TLDR

- The IRS treats most rental real estate as passive by default—losses offset only other passive income, not W-2 wages or active business profits

- Active participants with MAGI under $100,000 can deduct up to $25,000 in rental losses against non-passive income; the allowance phases out fully at $150,000

- Real estate professionals who meet the 750-hour and 50%-of-time tests can deduct unlimited losses against any income type

- Suspended losses carry forward indefinitely and release fully when you sell a property in a fully taxable transaction

- The 2026 PAL rules are unchanged from 2025—the One Big Beautiful Bill Act (July 2025) expanded depreciation but left the $25,000 threshold and REP requirements intact

What Are Passive Activity Loss Rules for Real Estate?

Congress enacted the passive activity loss (PAL) rules in 1986 to stop high-income taxpayers from using paper real estate losses (primarily from depreciation) to shelter W-2 wages and active business income. Before 1986, investors could buy rental properties, claim large depreciation deductions, and offset salary income with those losses, even when properties generated positive cash flow.

The Three-Bucket Income Framework

The IRS now divides all income into three buckets:

- Active income: Wages, salaries, and business profits where you materially participate

- Passive income: Rental activities and businesses where you do not materially participate

- Portfolio income: Dividends, interest, and capital gains

The core rule: Losses from one bucket generally cannot offset income from another bucket.

Why Rental Real Estate Is Passive by Default

Even if you spend significant hours managing your properties (screening tenants, coordinating repairs, collecting rent), the IRS treats rental activities as passive unless you qualify as a real estate professional — a designation that requires meeting specific hour thresholds and material participation tests beyond ordinary landlord duties.

According to IRS Publication 925, rental real estate is automatically classified as passive under IRC Section 469(c)(2) regardless of participation level, unless the taxpayer meets the real estate professional (REP) exception.

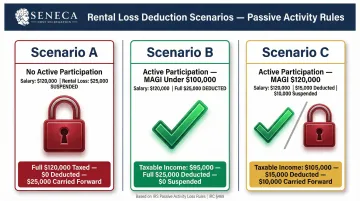

Practical Impact: A Concrete Example

Consider an investor earning $120,000 in salary with a $25,000 rental loss:

- Scenario A (Does not meet active participation threshold): The $25,000 loss is suspended. It cannot offset the $120,000 salary. The investor pays tax on the full $120,000.

- Scenario B (Meets active participation, MAGI under $100,000): The investor can deduct the full $25,000 loss, reducing taxable income to $95,000.

- Scenario C (Meets active participation, MAGI of $120,000): The allowable deduction is reduced. The phase-out calculation limits the deduction to $15,000, leaving $10,000 suspended.

Those suspended losses don't disappear — they carry forward to offset future passive income or free up entirely when you sell the property.

The $25,000 Special Allowance: Who Qualifies and How It Phases Out

Active Participation: What It Means and Who Qualifies

Active participation is a lower standard than material participation. It requires meaningful involvement in management decisions—approving tenants, setting rental terms, authorizing repairs, and similar activities. You can hire a property manager and still qualify as long as you retain final decision-making authority.

Key restrictions:

- You must own at least a 10% interest in the rental activity (by value)

- Limited partners are generally excluded

- Only individuals can actively participate—corporations and most trusts do not qualify

How the MAGI Phase-Out Works

The full $25,000 allowance is available to active participants with Modified Adjusted Gross Income (MAGI) of $100,000 or less. For every dollar of MAGI above $100,000, the allowance is reduced by $0.50. At $150,000 MAGI, the allowance is fully eliminated.

For PAL purposes, MAGI is calculated as adjusted gross income without passive activity income/loss, deductible IRA contributions, Social Security benefits, student loan interest deductions, and certain other exclusions. See IRS Publication 925 for the complete list.

To see how these thresholds play out in practice, consider a common mid-income scenario:

Phase-Out Calculation Example

Scenario: Single taxpayer with $130,000 MAGI and a $31,000 rental loss

Step-by-step calculation:

- Excess MAGI over threshold: $130,000 – $100,000 = $30,000

- Reduction amount: $30,000 × 50% = $15,000

- Adjusted allowance: $25,000 – $15,000 = $10,000

- Suspended loss: $31,000 – $10,000 = $21,000 carried forward

This investor can deduct $10,000 against non-passive income this year. The remaining $21,000 is suspended and tracked on Form 8582.

Married Filing Separately: A Major Disadvantage

For married taxpayers filing separately, the special allowance drops to $12,500 and the phase-out begins at $50,000 MAGI—not $100,000. If both spouses lived together at any time during the year, the allowance is zero. For most rental property owners, the MFS status effectively eliminates this benefit—making joint filing the stronger choice unless other tax factors outweigh it.

Real Estate Professional Status: The Path to Unlimited Deductions

The Two-Part Qualification Test

To bypass passive loss limits entirely, you must qualify as a Real Estate Professional under IRC Section 469(c)(7). This requires meeting two separate tests:

Test 1: More than 750 hours

You must perform more than 750 hours of personal service during the tax year in real property trades or businesses in which you materially participate.

Test 2: More than 50% of personal services

Those real estate hours must exceed 50% of your total personal services performed in all trades or businesses during the year.

Qualifying real property trades or businesses include:

- Real property development

- Construction or reconstruction

- Acquisition or conversion

- Rental or leasing

- Operations or management

- Brokerage

Exclusions to know:

- Employee hours in real estate don't count unless you own more than 5% of the employer

- A spouse's hours do not count toward the REP test (though they do count for material participation)

- Investor-type activities like reviewing financial statements do not count

Material Participation Inside REP Status

Qualifying as a real estate professional is not enough on its own. You must also materially participate in each rental activity. The IRS provides seven tests for material participation, but the most commonly used are:

- 500-hour test: Participating for more than 500 hours during the year

- Substantially-all test: Your participation accounts for substantially all participation across all individuals involved in the activity

- 100-hours/no one more test: Participating for more than 100 hours, and no one else participates more

The Aggregation Election

A qualifying REP can elect under Treasury Regulation 1.469-9(g) to treat all rental real estate interests as a single activity. This makes it easier to meet material participation thresholds across a portfolio.

Important: This election is binding and generally cannot be reversed without IRS consent. Work with a tax advisor before making this call — it has long-term consequences for your entire portfolio.

Documentation: The IRS Places the Burden on You

Once you've made the aggregation election — or chosen to track activities separately — your records become your defense. The IRS requires contemporaneous documentation to substantiate REP status. In Moss v. Commissioner, the Tax Court rejected "ballpark guesstimates" and post-event reconstructions. In Zarrinnegar v. Commissioner, by contrast, the court accepted REP status based on credible daily time logs proving over 1,000 hours — the difference was documentation quality.

What counts as operational work:

- Property showings and tenant meetings

- Coordinating repairs and maintenance

- Marketing and advertising properties

- Negotiating leases

- Direct property management tasks

What does NOT count (investor-type work):

- Reviewing financial statements

- Studying market reports

- Monitoring investment performance

Your recordkeeping baseline: Maintain detailed time logs, calendar entries, emails, and contractor invoices — and keep them current. Reconstructing records after an audit notice is a losing strategy.

How Suspended Passive Losses Accumulate and When You Can Use Them

How Losses Accumulate Over Time

When passive losses exceed passive income and any allowable deduction, the excess is "suspended" and tracked on Form 8582. These losses carry forward indefinitely, building up on your tax return until a qualifying event releases them.

Example: An investor with $160,000 MAGI cannot access the $25,000 allowance. Their rental generates a $20,000 annual loss. After five years, they have $100,000 in suspended losses sitting on their tax return—a potential future asset.

When Suspended Losses Are Released

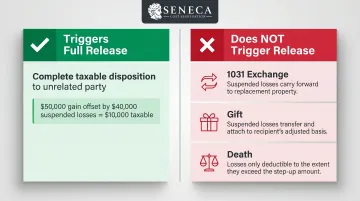

Complete Disposition Triggers Full Release

The primary trigger for releasing suspended losses is a complete disposition of the property in a fully taxable transaction to an unrelated party. Under IRC Section 469(g)(1), all suspended losses from that property become immediately deductible in the year of sale. These losses can offset the capital gain, reducing or eliminating taxable gain.

Example: You sell a rental property for a $50,000 gain and have $40,000 in accumulated suspended losses. The suspended losses offset the gain, leaving only $10,000 in taxable gain.

What Does NOT Trigger Release

Three common transactions do not trigger release:

- 1031 exchanges — Suspended losses carry over to the replacement property; no release occurs at exchange.

- Gifts — Losses are not released. They transfer to the recipient by being added to their basis.

- Death — Losses become deductible on the decedent's final return, but only to the extent they exceed the step-up in basis the heir receives.

Death example: A property with $60,000 in suspended losses and a $400,000 fair market value at death receives a stepped-up basis to $400,000. If the original basis was $350,000, the step-up eliminates $50,000 of the suspended losses ($400,000 – $350,000). Only $10,000 of suspended losses remain deductible on the final return.

Passive Income Offset Method

Disposition isn't the only way to unlock suspended losses. As you generate passive income in future years—from additional rental properties, limited partnership interests, or other qualifying passive activities—those suspended losses offset that income dollar for dollar. This gives investors a practical path to use accumulated losses without ever selling a property.

Strategies to Maximize Real Estate Tax Deductions in 2026

Timing and Income Strategies

Investors near the $100,000–$150,000 phase-out range can preserve or expand their $25,000 allowance by timing income events:

- Defer year-end bonuses to the following year

- Maximize retirement contributions (401(k), traditional IRA) to reduce MAGI

- Accelerate deductible expenses into the current year

If you have suspended losses, evaluate whether generating passive income through new acquisitions or other passive investments can unlock them in the near term.

Disposition Planning

When selling a property, choosing a fully taxable sale (rather than a 1031 exchange) strategically releases all accumulated suspended losses at once. If the sale generates a capital gain, the suspended losses can directly offset it.

Tradeoff to consider with a tax advisor:

- 1031 exchange: Defer capital gains tax, but carry suspended losses forward to the replacement property

- Fully taxable sale: Pay capital gains tax now, but unlock suspended losses immediately to offset the gain and potentially other income

Cost Segregation and Accelerated Depreciation

Cost segregation studies accelerate depreciation by reclassifying 20%–40% or more of a property's cost from 27.5- or 39-year schedules to 5-, 7-, or 15-year schedules. This front-loads deductions into the early years of ownership.

Critical planning consideration: These larger deductions are most powerful when combined with REP status or sufficient passive income to absorb them. Without either, accelerated depreciation simply creates larger suspended losses.

For context, investors who do qualify — through REP status or adequate passive income — have identified an average of $171,243 in first-year deductions through engineering-based cost segregation studies (Seneca Cost Segregation's internal data across 10,200+ properties). Knowing your PAL situation first determines whether accelerated depreciation pays off now or is better timed for when you have the income or status to absorb it.

Frequently Asked Questions

What are the passive loss rules for real estate?

Under IRC Section 469, most rental real estate is treated as a passive activity, meaning losses can only offset passive income. The two main exceptions are the $25,000 special allowance for active participants with MAGI under $150,000 and full non-passive treatment for qualifying real estate professionals.

What are the passive activity loss limitations for 2026?

The core PAL rules are unchanged for 2026: the $25,000 allowance phases out between $100,000 and $150,000 MAGI, and REP requirements (750 hours, 50% of time) remain the same. The One Big Beautiful Bill Act (P.L. 119-21) (July 4, 2025) expanded Section 1245 property definitions but left passive loss thresholds intact.

What are the passive activity loss limitations for 2025?

The 2025 rules are identical to 2026: $25,000 allowance phasing out between $100,000 and $150,000 MAGI, with REP status as the path to unlimited deductions. Returns filed in 2026 for tax year 2025 use Form 8582 to calculate and track passive loss limitations.

What is the capital loss limitation for 2026?

The capital loss limitation under IRC Section 1211(b) remains at $3,000 per year ($1,500 for married filing separately) for losses exceeding capital gains. This is separate from passive loss rules—when selling a rental, capital losses are subject to this limit, while suspended passive losses from that property are released separately in full.

Can I deduct rental property losses if I have a W-2 job?

Yes, up to $25,000 may be deductible if you actively participate in the rental and have MAGI below $100,000. Above $150,000, losses are suspended unless you qualify as a real estate professional. Between $100,000 and $150,000, the allowance phases out by 50% of the excess MAGI.

What happens to suspended passive losses when I sell a rental property?

When a rental property is sold in a fully taxable transaction to an unrelated party, all suspended passive losses from that property become deductible in the year of sale under IRC Section 469(g)(1). These losses can offset the gain on sale, so tracking suspended losses each year directly affects your tax outcome at closing.

Next Step: If your rental losses are suspended due to MAGI limits, a cost segregation study can accelerate depreciation deductions—creating passive income offsets or supporting a REP qualification strategy. Consult a qualified tax advisor to determine which approach fits your situation.