This guide walks through IRS-sanctioned tax strategies designed specifically to reward real estate investment: deductions for operating expenses, depreciation acceleration through cost segregation, capital gains deferral via 1031 exchanges, and advanced techniques like Real Estate Professional Status and the Short-Term Rental loophole. These aren't loopholes—they're incentives Congress built into the tax code to encourage capital investment in real property.

TLDR

- Deduct operating expenses like mortgage interest, insurance, repairs, and property management fees to reduce taxable rental income

- Accelerate depreciation deductions by 5-10x using cost segregation and 100% bonus depreciation on qualifying properties

- Defer capital gains taxes indefinitely with 1031 exchanges — or eliminate them through stepped-up basis at death

- Offset W-2 income with rental losses via Real Estate Professional Status or the Short-Term Rental exception

- Stack additional benefits like the QBI deduction, Opportunity Zones, and long-term capital gains treatment

Start With the Basics: What Expenses Can You Deduct?

Rental property owners can deduct ordinary and necessary expenses tied to managing their investment. The IRS allows these deductions on Schedule E, covering the actual costs of operating income-producing property throughout the tax year.

Common deductible expenses include:

- Mortgage interest on loans used to acquire or improve the property

- Property taxes paid to state and local governments (no SALT cap applies to investment properties)

- Landlord insurance premiums

- Repairs and maintenance that keep the property in good working condition

- Property management fees and commissions

- Advertising costs to attract tenants

- Professional fees for accountants, attorneys, and tax advisors

- Utilities paid by the landlord

- Travel expenses for property inspections and maintenance

The distinction between repairs and improvements trips up many investors. Repairs are fully deductible in the year incurred—fixing a broken window, patching a roof leak, or repainting a room. Improvements must be capitalized and depreciated over time because they result in a betterment, restore the property to like-new condition, or adapt it to a new use. Installing a new HVAC system, adding a deck, or renovating a kitchen are improvements.

The IRS Tangible Property Regulations offer three safe harbors worth knowing:

- De minimis: Deduct expenditures up to $2,500 per invoice without capitalizing them

- Routine maintenance: Expense recurring activities that keep property in efficient operating condition

- Small taxpayer: Qualifying owners can expense repairs and improvements if total annual costs don't exceed the lesser of 2% of the property's unadjusted basis or $10,000

The IRS requires documentation for every deduction you claim. Records must be kept until the statute of limitations expires for the year you dispose of the property—not just three years from filing. That means holding onto receipts, invoices, bank statements, and depreciation schedules for the entire ownership period plus several years beyond sale.

Depreciation and Cost Segregation: The Biggest Tax-Saving Tool in Real Estate

Standard depreciation lets property owners recover the cost of a building (not land) over 27.5 years for residential rentals and 39 years for commercial properties.

For a $400,000 residential property, the annual depreciation deduction is approximately $14,545 ($400,000 ÷ 27.5). At a 35% combined tax rate, that saves $5,091 per year—roughly $140,000 over the full depreciation life.

Cost segregation dramatically accelerates these deductions by breaking the building into component asset classes with shorter depreciation schedules.

How Cost Segregation Works

A cost segregation study is an engineering-based analysis that reclassifies building components into 5-year, 7-year, and 15-year property categories instead of lumping everything into the 27.5 or 39-year building class. Components eligible for reclassification include:

- 5-year property: Carpet, vinyl flooring, appliances, decorative light fixtures

- 7-year property: Furniture, office equipment, certain fixtures

- 15-year property: Landscaping, parking lots, sidewalks, site utilities, land improvements

Industry studies show cost segregation typically reclassifies 20-40% of a property's depreciable basis into these shorter-life categories.

Bonus Depreciation Amplifies the Benefit

Once cost segregation identifies short-life assets, bonus depreciation lets you write off those components in year one. The One Big Beautiful Bill Act (OBBBA) reinstated 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025.

For property acquired before that date but placed in service in 2025, bonus depreciation remains at 40% (60% for long production period property).

This creates massive front-loaded deductions. For that same $400,000 property, cost segregation might identify $150,000 in short-life assets. With 100% bonus depreciation, you write off the entire $150,000 in year one instead of spreading it over 27.5 years—a first-year deduction of $150,000 versus roughly $14,545 under straight-line depreciation.

Paper Losses That Increase Cash Flow

Cost segregation creates "paper losses" that reduce taxable income without affecting actual cash flow. If your rental property generates $30,000 in net operating income but cost segregation produces $150,000 in depreciation deductions, you show a $120,000 tax loss while still depositing $30,000 in cash. For cash-flow-positive investors, this means the IRS effectively subsidizes growth that was already generating real returns.

The bonus depreciation phase-down schedule makes acting now critical. For properties placed in service after January 19, 2025, the 100% rate applies. But this benefit diminishes in future years, making 2025 and early 2026 a strategic window for maximizing first-year deductions.

Seneca Cost Segregation

Investors looking to capture these deductions can work with Seneca Cost Segregation, an engineering-based firm that has completed over 10,200 studies across all 50 states. Seneca delivers an average first-year deduction of $171,243, with studies typically finished within 2-4 weeks.

Every study includes AuditDefense with a money-back guarantee and IRS-compliant documentation. The veteran-owned team coordinates directly with CPAs to integrate findings into tax filings—and a 95% client referral rate reflects how that process holds up in practice.

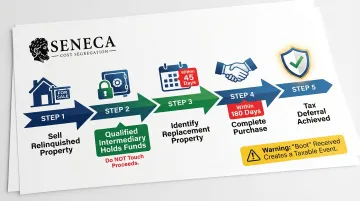

The 1031 Exchange: How to Defer Capital Gains When You Sell

A 1031 exchange lets you defer capital gains taxes and depreciation recapture when you sell an investment property — as long as you reinvest the proceeds into like-kind real property of equal or greater value. The deferred tax doesn't disappear; it rolls into your replacement property's basis. But deferral means the full sale proceeds compound in your next investment rather than shrinking by 20-25% on day one.

The Compounding Power of Tax Deferral

Sell a property for $800,000 with a $300,000 gain, and you'd normally owe $45,000-$60,000 in federal capital gains tax (15-20% rate) plus depreciation recapture tax at up to 25%. A 1031 exchange lets you reinvest the entire $800,000 instead of $740,000, giving you an extra $60,000 working in your next deal. Repeat this across three or four exchanges over a decade, and each deferred tax bill stays in circulation — building equity instead of going to the IRS.

When a 1031-exchanged property is eventually passed to heirs, they receive a stepped-up cost basis to fair market value under IRC Section 1014, potentially eliminating the deferred gain entirely.

Strict Rules and Timelines

To qualify for tax deferral, you must follow precise IRS requirements:

Critical deadlines:

- 45-day identification window: Identify replacement property in writing within 45 days of closing on the relinquished property

- 180-day exchange window: Complete the purchase by the earlier of 180 days after sale or the due date of your tax return (including extensions)

Qualified Intermediary requirement: You cannot take control of sale proceeds. A Qualified Intermediary must hold the funds between sale and purchase. Touching the money disqualifies the exchange and triggers immediate taxation.

Equal or greater value rule: The replacement property must match or exceed the relinquished property's value, and you must reinvest all net proceeds. Any cash you pocket — called "boot" — is immediately taxable.

Debt replacement rule: If you paid off $200,000 in debt on the sale, you must replace that debt with new financing or additional cash equity in the replacement property. Failing to do so creates taxable boot equal to the unmatched debt.

Depreciation Recapture Still Deferred

A 1031 exchange defers both capital gains and depreciation recapture. Depreciation recapture — taxed at up to 25% — applies when you eventually sell without exchanging. For investors who've claimed years of depreciation deductions (especially those accelerated through a cost segregation study), the recapture liability can actually exceed the capital gains tax. Deferring both through a 1031 exchange keeps that combined tax bill out of the picture until you're ready to cash out — or pass the asset to heirs and potentially eliminate it altogether.

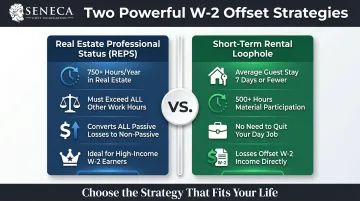

Real Estate Professional Status and the Short-Term Rental Loophole: How to Offset W-2 Income

The IRS classifies most rental activity as "passive," meaning losses can only offset other passive income—not W-2 wages or active business income. This limitation prevents high earners from using depreciation losses to reduce their employment taxes. Two strategies work around this restriction.

Real Estate Professional Status (REPS)

Qualifying as a Real Estate Professional under IRC §469(c)(7) converts passive rental losses into non-passive losses that can offset any income source, including W-2 wages and business profits.

Two requirements must be met annually:

- Spend more than 750 hours per year on real estate activities (development, construction, acquisition, conversion, rental, management, leasing, or brokerage)

- Spend more hours on real estate than in any other profession or business

REPS is especially powerful for high earners—doctors, attorneys, business owners—when combined with cost segregation. A physician earning $500,000 in W-2 income who generates $200,000 in rental losses through cost segregation can offset their entire practice income if they qualify, potentially saving $70,000–$100,000 in federal taxes in a single year.

IRS Documentation Requirement: Keep contemporaneous time logs recording activities, dates, hours, and descriptions. Vague estimates won't survive audit scrutiny.

The Short-Term Rental (STR) Loophole

The STR exception offers a path for investors who don't meet REPS requirements. Under Treasury Regulation §1.469-1T(e)(3)(ii)(A), an activity is not treated as a "rental activity" if the average guest stay is 7 days or fewer—reclassifying the STR as a non-passive business rather than a passive rental.

To unlock non-passive treatment, you must also meet material participation under one of seven IRS tests. The most common threshold: 500+ hours annually in the STR business. Qualifying activities include:

- Managing bookings and guest communication

- Overseeing maintenance and repairs

- Setting and adjusting pricing

- Handling property operations day-to-day

Key advantage: You don't need to quit your day job. A full-time software engineer who actively manages three Airbnb properties and logs 500+ hours can use STR losses to offset their W-2 income, even without REPS.

The $25,000 Passive Loss Allowance

If neither REPS nor the STR loophole fits your situation, there's still a fallback. Investors can deduct up to $25,000 in passive rental losses against ordinary income if they actively participate in managing the property and their Modified Adjusted Gross Income (MAGI) is under $100,000. The allowance phases out at 50 cents per dollar of MAGI above $100,000 and disappears entirely at $150,000.

Active participation is a lower bar than material participation—making management decisions like approving tenants, setting rental terms, and approving repairs is typically sufficient.

Other Real Estate Tax Strategies Worth Stacking

The QBI Deduction (Section 199A)

The Qualified Business Income deduction allows eligible taxpayers to deduct up to 20% of qualified business income from pass-through entities like LLCs, S-Corps, and sole proprietorships. Rental real estate can qualify if you meet specific requirements under Revenue Procedure 2019-38.

Safe harbor requirements:

- Maintain separate books and records for each rental enterprise

- Perform 250+ hours of rental services annually (repairs, maintenance, rent collection, tenant management)

- Keep contemporaneous records documenting hours, activities, dates, and personnel

2025 income thresholds:

- Married filing jointly: Phase-in begins at $394,600, complete phase-out at $494,600

- Single/other filers: Phase-in begins at $197,300, complete phase-out at $247,300

Below these thresholds, you can claim the full 20% deduction regardless of business type. Above them, W-2 wage and qualified property limitations kick in — especially restrictive for specified service businesses. The QBI deduction is scheduled to sunset after December 31, 2025, making this the last year for this benefit unless Congress extends it.

Opportunity Zones

Investing in a Qualified Opportunity Fund (QOF) lets you defer capital gains from any source — not just real estate — by reinvesting them within 180 days of the gain's recognition date.

For legacy investments, the deferred gain must be recognized by December 31, 2026. The One Big Beautiful Bill Act permanently renewed the Opportunity Zone program, with new designation cycles starting July 1, 2026.

Key benefit: If you hold the QOF investment for at least 10 years, you can step up the basis to fair market value on the date of sale, permanently excluding all post-investment appreciation from federal capital gains tax.

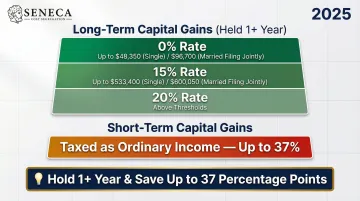

Long-Term Capital Gains vs. Short-Term

Holding a property for more than one year before selling qualifies the gain for long-term capital gains rates—0%, 15%, or 20% depending on income—compared to ordinary income rates (up to 37%) for properties sold within one year.

2025 long-term capital gains brackets:

- 0% rate: Up to $48,350 (single) / $96,700 (married filing jointly)

- 15% rate: Up to $533,400 (single) / $600,050 (married filing jointly)

- 20% rate: Above these thresholds

Primary Residence Exclusion (Section 121)

Taxpayers can exclude gain on the sale of a principal residence if they owned and used it as their main home for at least 2 of the 5 years before selling:

- Single filers: Exclude up to $250,000 of gain

- Married filing jointly: Exclude up to $500,000 of gain

Converting investment property to a primary residence: Two rules reduce — but don't eliminate — the exclusion. First, gain allocated to periods of "nonqualified use" after 2008 is not excludable. Second, depreciation claimed after May 6, 1997 triggers unrecaptured Section 1250 gain taxed at 25%. If you're planning a conversion, timing the move carefully and tracking your depreciation history can preserve a meaningful portion of the exclusion.

Frequently Asked Questions

How to use real estate to reduce your taxes?

Own investment property to generate legal tax deductions through operating expenses, depreciation, and cost segregation that reduce taxable income. Use 1031 exchanges to defer capital gains, and if you qualify for REPS or the STR loophole, offset W-2 income with rental losses.

Can you offset W-2 income with real estate depreciation?

Yes, but only under two conditions: qualifying as a Real Estate Professional (750+ hours/year in real estate, exceeding all other work) or using the Short-Term Rental loophole (average stay of 7 days or fewer with material participation). Both convert passive losses into active deductions against W-2 income.

What is the $250,000 / $500,000 home sale exclusion?

This exclusion applies to a primary residence: single filers can exclude up to $250,000 in gain, and married couples filing jointly can exclude up to $500,000, provided they owned and lived in the home for at least 2 of the last 5 years before selling.

Does buying a house give you a bigger tax return?

Buying a primary residence adds deductions (mortgage interest, property taxes) that may increase your itemized total, but doesn't guarantee a bigger refund. Investment properties offer far greater benefits through depreciation and expense deductions that cut taxable income directly.

Is real estate a good investment for tax purposes?

Yes—real estate is one of the most tax-advantaged asset classes in the U.S. tax code. Depreciation, expense deductions, preferential capital gains rates, 1031 exchanges, and cost segregation give investors more legal tools to reduce taxes than almost any other investment type.

Is there a way to make property taxes lower?

Investors can appeal a property's assessed value with the local tax assessor if they believe it's overvalued, especially after a market decline. Property taxes on investment properties are fully deductible as a business expense on Schedule E, reducing the after-tax cost of the bill.