Real estate investors routinely overpay on taxes because standard depreciation rules force them to write off entire properties over 27.5 years (residential) or 39 years (commercial). Yet many building components (specialty electrical, flooring, land improvements, appliances) legally qualify for 5-, 7-, or 15-year depreciation schedules, unlocking first-year deductions that can equal 20%–40% or more of a property's cost.

This guide covers two complementary tax strategies that maximize those deductions: cost segregation and bonus depreciation. Cost segregation is an engineering-based study that reclassifies building components into shorter depreciation categories. Bonus depreciation is the IRS provision that lets you immediately deduct those short-life assets in year one. As of July 4, 2025, it is restored to 100% under the One Big Beautiful Bill Act (OBBBA) for qualifying property with an acquisition date of January 19, 2025 or later.

You'll learn how each strategy works, how they interact, what changed under the OBBBA, which properties qualify, and how to implement both to reduce or eliminate federal taxes and accelerate portfolio growth.

TL;DR: Cost Segregation & Bonus Depreciation at a Glance

- Cost segregation reclassifies building components into 5-, 7-, and 15-year property instead of 27.5 or 39 years through an engineering-based study

- Bonus depreciation allows 100% immediate deduction of those short-life assets in year one, permanently restored under P.L. 119-21 for property with an acquisition date of January 19, 2025 or later

- Together, they convert 20–40% or more of a property's cost basis into first-year tax deductions

- Cost segregation identifies eligible assets; bonus depreciation sets the deduction rate. Understanding both is what turns a study into immediate cash flow

What Are Cost Segregation and Bonus Depreciation?

What Is a Cost Segregation Study?

Cost segregation is a tax strategy that uses engineering analysis to break down a real estate purchase price into individual asset components, each assigned a MACRS recovery period based on its function rather than treating the building as a single depreciable asset.

Under standard IRS rules, residential rental properties depreciate over 27.5 years and commercial properties over 39 years. A cost segregation study identifies components' electrical fixtures, specialty plumbing, flooring, land improvements that qualify for 5-, 7-, or 15-year MACRS schedules instead.

Who performs the study: Qualified cost segregation professionals use engineering-based methodology that includes blueprints, site inspections, contractor records to document and support each reclassification. The IRS Cost Segregation Audit Techniques Guide states that studies conducted by individuals with engineering or construction backgrounds are more reliable than those without such expertise.

Seneca Cost Segregation's engineering team employs a comprehensive methodology that includes:

- Physical or virtual site inspections with detailed photography and measurements

- Blueprint and construction document review

- Contractor record analysis and cost allocation using R.S. Means data

- Engineering quantity take-offs for precise component measurement

- Legal classification using the Whiteco six-factor test

- Detailed 20-30 page reports with IRS-compliant documentation

With over 10,200 properties studied nationwide and an average first-year deduction of $171,243, Seneca's studies produce results supported by their AuditDefense guarantee.

What Is Bonus Depreciation?

Bonus depreciation (IRC §168(k)) is an additional first-year depreciation allowance. It lets taxpayers deduct a specified percentage of qualifying property costs — property with a MACRS recovery period of 20 years or less in the year it is placed in service, rather than spreading that deduction over the full recovery period.

Historically, only new property qualified. The Tax Cuts and Jobs Act (TCJA) expanded eligibility to include used property, and the OBBBA preserves this expansion. Used property must clear three acquisition tests:

- Cannot have been used by the taxpayer previously

- Cannot be acquired from a related party

- Cannot carry a carryover basis

How Cost Segregation and Bonus Depreciation Work Together

Cost segregation creates the inventory of short-life assets (5-, 7-, 15-year property). Bonus depreciation then allows you to deduct up to 100% of those reclassified assets in year one instead of spreading the deduction across the shorter schedule. Without a cost segregation study, most of the property remains on a 27.5- or 39-year schedule and does not qualify for bonus depreciation at all.

The Multiplier Effect

Here's the sequence:

- Purchase a property → $2 million depreciable basis

- Commission a cost segregation study → identifies 25% ($500,000) as short-life assets

- Apply 100% bonus depreciation → deduct the full $500,000 in year one

- Result: A $500,000 first-year deduction that can offset passive income or, for qualifying real estate professionals, active income

Without cost segregation, that $2 million property would generate only ~$72,727 in annual depreciation (27.5-year schedule). With cost segregation and bonus depreciation, you capture $500,000 upfront which is nearly 7× the standard deduction.

Cost segregation is a study methodology (not a tax provision itself), while bonus depreciation is a statutory provision under IRC §168(k). Either can be used independently, but combining them produces significantly higher first-year deductions than either tool delivers alone.

Qualified Improvement Property (QIP)

Interior improvements to nonresidential buildings placed in service after the building itself qualify for a 15-year recovery period under the CARES Act technical correction and are therefore eligible for bonus depreciation. This is especially relevant for investors who renovate commercial spaces or complete tenant buildouts.

Key QIP considerations for investors:

- Retroactive claims allowed: Rev. Proc. 2020-25 lets taxpayers recover missed bonus depreciation on QIP placed in service after December 31, 2017, via Form 3115

- Tenant buildouts qualify: Interior improvements completed after the building's placed-in-service date typically meet the 15-year QIP threshold

- Documentation matters: Proper asset classification across personal property, site improvements, and QIP determines how much bonus depreciation you can actually claim

Seneca's engineering-based studies are built to identify and document each of these asset classes accurately, so nothing eligible gets left on the table.

Which Property Types and Assets Qualify?

Property Types That Benefit Most

Cost segregation studies provide the greatest tax benefit for:

- Residential rentals: Single-family, multi-family, apartments

- Commercial properties: Office, retail, industrial

- Short-term rentals (STRs)

- Owner-occupied business properties

- Newly constructed or substantially renovated buildings

Minimum threshold: Properties with a depreciable cost basis of at least $300,000 (excluding land) justify the study cost, though $450,000–$500,000+ represents the optimal range where savings significantly outweigh fees.

STR owners have a particular incentive: short-term rentals may allow you to bypass passive activity loss (PAL) limitations entirely, provided you meet material participation requirements that includes an average guest stay of 7 days or fewer with regular, ongoing involvement in operations.

Common Asset Classes by Recovery Period

| Recovery Period | Example Assets |

|---|---|

| 5-year property | Specialty electrical and decorative lighting; Carpeting and vinyl flooring; Appliances and cabinetry; Certain technology infrastructure |

| 7-year property | Office furniture and fixtures; Movable partitions; Communications equipment |

| 15-year property | Parking lots and sidewalks; Fencing and landscaping; Exterior pole lighting |

| 27.5/39-year property (structural components) | Foundation and load-bearing walls; Roof and whole-building HVAC; Plumbing serving the entire building |

Industry benchmarks show approximately 20–30% of a property's basis is typically reclassified to shorter recovery periods, though this varies by property type. Manufacturing facilities can reach 30–60%, while warehouses typically reclassify only 10–17%.

Eligibility Rules for Bonus Depreciation

Understanding which asset classes fall into 5-, 7-, and 15-year buckets sets the stage for bonus depreciation, but not every reclassified asset automatically qualifies. To be eligible, each asset must:

- Have a MACRS recovery period of 20 years or less

- Be placed in service within the applicable statutory timeframe

- Meet original-use or used-property acquisition requirements

- Be acquired after the relevant legislative effective dates

Each asset is evaluated individually. A cost segregation study produces the asset-level documentation the IRS requires to substantiate bonus depreciation claims, and that same documentation serves as your primary defense in the event of an audit.

Bonus Depreciation Rules, Phase-Outs, and the OBBBA Update

Phase-Out History Under the TCJA

Bonus depreciation was introduced in 2002 at 30%, varied between 30–50% for the following decade, and was raised to 100% under the Tax Cuts and Jobs Act of 2017 for property placed in service from September 27, 2017 through December 31, 2022.

The TCJA then scheduled a 20% annual phase-down:

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | |

| January 1, 2023 – December 31, 2023 | 80% | |

| January 1, 2024 – December 31, 2024 | 60% | |

| January 1, 2025 – January 18, 2025 | 40% | |

| January 19, 2025 – December 31, 2030 | 100% | Acquisition date must be January 19, 2025 or later |

| 2025 (placed in service) | 40% | If acquisition date is before January 19, 2025 |

| 2026 (placed in service) | 20% | If acquisition date is before January 19, 2025 |

Even at reduced rates, cost segregation studies remained valuable because accelerated depreciation still outpaced straight-line treatment. But the full first-year deduction was reduced significantly.

Example comparison for a $2M property with $500K reclassified:

| Bonus Rate | Year-One Deduction | Remaining Basis Treatment |

|---|---|---|

| 100% bonus | $500,000 | — |

| 60% bonus | $300,000 | Spread remaining $200K over 5–15 years |

| 20% bonus | $100,000 | Spread remaining $400K over 5–15 years |

Permanent Restoration Under P.L. 119-21 (OBBBA)

On July 4, 2025, President Trump signed P.L. 119-21 (the "One Big Beautiful Bill"), which **permanently restores 100% bonus depreciation** for qualified property acquired and placed in service after January 19, 2025. The provision applies to both new and used property. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Transitional election: For the first taxable year ending after January 19, 2025, taxpayers may elect a 40% rate (or 60% for property with longer production periods and certain aircraft) instead of the full 100% rate.

Qualified Production Property (QPP)

For the first time, certain nonresidential real property used as an integral part of a qualified production activity (manufacturing, refining, industrial production) now qualifies for 100% bonus depreciation under the new QPP provision.

Eligibility requirements:

- Construction must begin after January 19, 2025, and before January 1, 2029

- Property must be placed in service before January 1, 2031

- Must be used in manufacturing, agricultural, chemical, or refining activities

Exclusions: Office space, parking, and sales floors are explicitly excluded. If the property ceases to be used for production within 10 years, the depreciation is subject to full §1245 recapture.

Section 179 Increase Under the OBBBA

For investors deploying bonus depreciation through a cost segregation study, Section 179 covers the personal property and equipment that falls outside real property classification. Under the OBBBA, the deduction limit rises to $2.5 million with a $4.0 million phase-out threshold, both indexed for inflation after 2025. Where bonus depreciation applies broadly to qualifying property, Section 179 gives investors a direct, elective write-off for smaller equipment purchases in the same tax year.

Real-World Example: A Real Estate Investor Using Both Strategies

Scenario: An investor acquires a $2 million multi-family property in 2025 (excluding land value).

| Metric | Without Cost Segregation | With Cost Segregation + 100% Bonus Depreciation |

|---|---|---|

| Entire depreciable basis | $2,000,000 | $2,000,000 |

| Depreciation schedule | 27.5 years | 27.5 years |

| Short-life assets identified | — | 25% ($500,000) as 5-, 7-, or 15-year property |

| Bonus depreciation deduction | — | $500,000 in year one |

| Annual deduction | ~$72,727 | Remaining basis ($1,500,000) continues on 27.5-year schedule: ~$54,545/year |

| Total year-one deduction | ~$72,727 | $554,545 |

| Tax savings at 37% federal rate | ~$26,909/year | ~$205,182 |

Year-one comparison:

| Tax Savings | |

|---|---|

| With cost segregation | $205,182 |

| Without cost segregation | $26,909 |

| Incremental benefit | $178,273 in additional year-one cash |

The Reinvestment Advantage

The cash freed up by eliminating or significantly reducing tax liability in year one can be deployed into the next property acquisition faster. That $178,273 deployed into another property with similar returns compresses the acquisition timeline by months, sometimes years. That's the real multiplier effect of pairing cost segregation with bonus depreciation.

The pattern repeats with each acquisition:

- Year-one deductions reduce tax liability immediately

- Freed-up capital funds the next down payment sooner

- Each new property creates another opportunity for accelerated depreciation

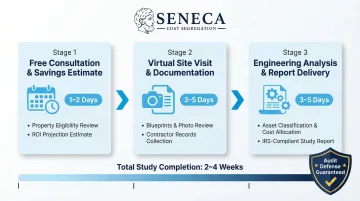

How to Get Started with a Cost Segregation Study

The Process

A professional cost segregation study begins with a property review: documents, blueprints, photos, and a site visit where applicable. From there, an engineering analysis classifies each component, and the process concludes with a detailed report your CPA uses to file accelerated depreciation on your tax return.

Seneca Cost Segregation typically completes studies within 2–4 weeks, compared to the industry standard of 4–8 weeks. The process includes:

| Step | Timeline | Description |

|---|---|---|

| Free consultation and savings estimate | 1–2 days | Property eligibility assessment and preliminary ROI projection |

| Virtual site visit and documentation collection | 3–5 days | Guided property tour via video call or on-site inspection |

| Engineering analysis and report delivery | 3–5 days | Detailed engineering take-offs, cost allocation, asset classification, and IRS-compliant report preparation |

Studies are backed by Seneca's AuditDefense guarantee: if the IRS audits your study and Seneca's analysis is found to be the cause of an issue resulting in greater than 5% adjustment to depreciation, Seneca will refund 100% of the cost segregation services fees.

Timing: Current-Year vs. Look-Back Studies

The ideal time for a cost segregation study is the year a property is placed in service. However, look-back studies can capture missed deductions on properties already owned.

Using Form 3115 (Application for Change in Accounting Method), you can claim all missed depreciation in the current year via a §481(a) catch-up adjustment, typically with no need to amend prior returns. The IRS treats asset reclassification as a change in accounting method, which is exactly what Form 3115 is designed for.

Whether a look-back study makes sense depends on property type, basis, and holding period. Seneca handles Form 3115 preparation and coordinates with your CPA for smooth filing.

Frequently Asked Questions

What is cost segregation and how does it relate to bonus depreciation?

Cost segregation is an engineering study that reclassifies building components into shorter MACRS depreciation categories (5-, 7-, 15-year property). Bonus depreciation is the IRS provision that allows immediate expensing of those shorter-life assets. Combined, they can convert 20%–40% or more of a property's cost basis into deductions in year one.

How is cost segregation different from bonus depreciation?

Cost segregation is a study methodology that identifies which assets qualify for accelerated depreciation, while bonus depreciation is a tax code provision (§168(k)) that determines how much of those assets can be deducted upfront. One prepares the asset inventory; the other determines the deduction rate.

Do you need a cost segregation study to claim bonus depreciation?

Technically no, but without a study, most of a real property's value remains in 27.5/39-year categories ineligible for bonus depreciation. A cost segregation study unlocks the majority of bonus depreciation opportunity for real estate investors.

What property types qualify for cost segregation (for example, commercial or rental property)?

Any depreciable real property with components that can be reclassified into shorter MACRS life categories, including:

- Residential rentals (single-family, multi-family, apartments)

- Commercial properties (office, retail, industrial)

- Short-term rentals

- Owner-occupied businesses

What property or assets qualify for 100% bonus depreciation?

Qualifying assets include:

- MACRS property with a 20-year or shorter recovery period (5-, 7-, 15-year assets)

- Depreciable computer software

- Qualified Improvement Property (QIP)

- Certain Qualified Production Property under the OBBBA

Acquisition and placed-in-service requirements must be met in all cases.

What are the rules, limitations, and phase-out schedule for bonus depreciation through 2026?

The TCJA phase-down (80% in 2023, 60% in 2024, 40% pre-Jan. 19, 2025) was reversed by P.L. 119-21 signed July 4, 2025, restoring 100% bonus depreciation for qualifying property with an acquisition date of January 19, 2025 or later. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.