Introduction

Real estate investors forfeit significant tax savings each year by defaulting to standard depreciation schedules and missing strategic deductions. Most property owners treat their annual tax bill as fixed. It's not. With the right planning, it's highly controllable.

Investment property creates three distinct tax obligations (rental income tax, depreciation recapture up to 25%, and capital gains), each requiring a different reduction strategy. Most investors discover these liabilities only at sale, when options have already narrowed.

Decisions made at acquisition and throughout the holding period determine 80% of your lifetime tax exposure. The earlier you plan, the more you control.

This guide covers ownership-phase and exit-phase tax reduction strategies for landlords, buy-and-hold investors, short-term rental (STR) owners, and commercial property owners. You'll learn how to legally minimize what you owe through IRS-approved methods including accelerated depreciation, cost segregation, strategic timing, and deferral vehicles.

TL;DR

- Investment property generates three tax layers: rental income, depreciation recapture (up to 25%), and capital gains

- Cost segregation plus 100% bonus depreciation turns 20–40% of property cost into immediate first-year deductions

- The IRS taxes depreciation as "allowed or allowable" at sale, so skipping deductions doesn't avoid recapture

- REPS or the STR 7-day rule unlocks passive losses that can offset W-2 income

- 1031 exchanges, installment sales, and Qualified Opportunity Zones defer or eliminate capital gains at exit

How Investment Property Taxes Accumulate

Investment property creates a three-layer tax structure that compounds over time. Understanding how these layers interact is the first step toward reducing them.

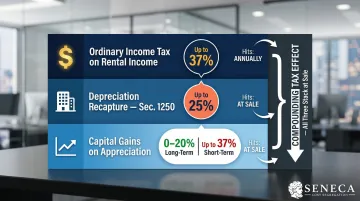

The Three Tax Layers

| Tax Layer | When It Hits | Rate |

|---|---|---|

| Ordinary income tax on net rental income | Each year during ownership | Up to 37% |

| Depreciation recapture (Sec. 1250) | At sale | Up to 25% |

| Capital gains on appreciation | At sale | 0–20% (long-term); up to 37% (short-term) |

Layer 1, Rental Income Tax: Taxable rental income equals gross rents minus operating expenses and depreciation. Rental income is passive, so it avoids self-employment (FICA) taxes. The trade-off: passive loss rules restrict how losses can offset other income, which is why timing deductions strategically matters.

Layer 2, Depreciation Recapture: When you sell, the IRS recaptures all depreciation you claimed and taxes it at up to 25% as unrecaptured Section 1250 gain. The IRS applies this to depreciation that was "allowed or allowable"—meaning you owe the tax even if you never claimed the deduction. Skipping depreciation doesn't eliminate recapture; it just means you paid tax twice on the same income.

Layer 3, Capital Gains: Property appreciation is taxed as a capital gain. Hold longer than one year and you qualify for long-term rates (0%, 15%, or 20% depending on income). Sell within a year and you pay ordinary income rates up to 37%.

The Phantom Income Problem

Depreciation creates a timing mismatch. During ownership, depreciation reduces your taxable income—potentially creating paper losses that shelter other income. At sale, mandatory recapture creates a concentrated tax hit. Example: You buy a $1 million property ($800,000 building, $200,000 land) and depreciate it over 27.5 years. You claim $29,091 annually in depreciation for 10 years ($290,910 total). At sale, you owe 25% recapture tax on that $290,910 ($72,728) plus capital gains on appreciation—regardless of whether you actually took those deductions.

Key Tax Drivers That Inflate Your Bill

Four controllable variables determine most of your tax liability. Ignoring them at acquisition compounds costs for years.

| Tax Driver | Default Impact | Optimized Outcome |

|---|---|---|

| Holding Period | Short-term rates up to 37% | Long-term rates 0%, 15%, or 20% |

| Depreciation Structure | 27.5/39-year straight-line | Accelerated 5-, 7-, or 15-year via cost segregation |

| Investor Status | Passive losses restricted to passive income | Nonpassive losses offset W-2 or business income |

| Property Classification | Undifferentiated building depreciation | Optimized land/building allocation and component classification |

Holding Period

Short-term capital gains (property held ≤1 year) are taxed at ordinary income rates up to 37%. Long-term capital gains (held >1 year) are taxed at 0%, 15%, or 20%. This single decision can cut your tax rate on gains by half or more.

Depreciation Structure

Most investors default to straight-line depreciation over 27.5 years (residential) or 39 years (commercial) simply because they don't know alternatives exist. That default choice leaves years of accelerated deductions on the table. Cost segregation can shift a substantial portion of those deductions into years one through five instead.

Investor Status

The IRS classifies rental income as passive by default, meaning losses can only offset other passive income. Qualifying for Real Estate Professional Status (REPS) converts those passive losses to nonpassive. The short-term rental loophole achieves the same result. Either path allows losses to offset W-2 or business income directly.

Property Classification

Three decisions made at closing directly shape your annual deductions:

- How you separate land value from building value

- Whether you elect bonus depreciation

- How you classify components (5-year vs. 15-year vs. 27.5-year property)

Get these wrong at acquisition and you're locked into suboptimal depreciation for the entire holding period.

Strategies to Reduce Taxes During Ownership

The greatest tax leverage in real estate comes from strategies applied while actively holding the property. Decisions made after closing—not just at purchase—determine the bulk of your annual tax exposure.

Maximize Deductions and Depreciation

Operating Deductions Available to All Investors:

- Mortgage interest

- Property taxes

- Insurance premiums

- Management fees

- Maintenance and repairs

- Advertising and marketing

- Professional fees (legal, accounting, property management)

- Depreciation

Accurate recordkeeping is required to defend each deduction. The IRS allows you to deduct ordinary and necessary expenses for managing, conserving, or maintaining rental property.

Repair vs. Capital Improvement: The Critical Distinction

The IRS applies the BAR test (Betterment, Adaptation, or Restoration) to determine whether an expense is a currently deductible repair or a capital improvement that must be depreciated:

- Repairs (deductible now): Keeps property in ordinarily efficient operating condition (fixing a broken window, patching a roof leak, repainting)

- Improvements (capitalized and depreciated): Results in betterment, adaptation to new use, or restoration of the property (new roof, room addition, HVAC replacement)

Safe Harbors to Simplify Compliance:

- De Minimis Safe Harbor: Deduct up to $2,500 per invoice or item (for taxpayers without an applicable financial statement)

- Routine Maintenance Safe Harbor: Deduct recurring activities expected to be performed more than once during a 10-year period

Optimize Building vs. Land Value at Acquisition

Land is not depreciable. The IRS requires you to separate land value from building value at purchase. Many investors accept the property tax assessor's allocation without question, which often understates building value. Documentation from a CPA and appraiser can support a reasonable allocation that maximizes depreciable basis.

Accelerate Savings with Cost Segregation and Bonus Depreciation

Standard straight-line depreciation is a baseline, not an optimal strategy. Cost segregation combined with bonus depreciation allows you to front-load decades of write-offs into the first year of ownership.

How Cost Segregation Works

A cost segregation study reclassifies building components from 27.5- or 39-year property into shorter-lived asset classes:

- 5-year property: Appliances, carpets, furniture in residential rentals

- 7-year property: Office furniture and fixtures

- 15-year property: Land improvements (parking lots, fencing, landscaping, sidewalks)

Studies commonly identify 20-40% of property value eligible for accelerated depreciation. This converts a portion of your purchase price into large first-year deductions instead of spreading them across decades.

The Power of 100% Bonus Depreciation

The One Big Beautiful Bill Act (P.L. 119-21), enacted July 4, 2025, restored 100% bonus depreciation for qualified property with an acquisition date of January 19, 2025 or later. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline:

| Period | Bonus Depreciation Rate |

|---|---|

| September 27, 2017 – December 31, 2022 | 100% |

| January 1, 2023 – December 31, 2023 | 80% |

| January 1, 2024 – December 31, 2024 | 60% |

| January 1, 2025 – January 18, 2025 | 40% |

| January 19, 2025 – December 31, 2030 (acquisition date January 19, 2025 or later) | 100% |

If acquisition date is before January 19, 2025:

- 40% bonus depreciation applies in 2025

- 20% bonus depreciation applies in 2026

When combined with a cost segregation study, investors can deduct a substantial portion of a property's cost in year one rather than spreading it across decades.

Example Impact:

| Property Placed in Service | Bonus Depreciation Rate | First-Year Deduction on $200K of Reclassified Assets |

|---|---|---|

| January 1-19, 2025 | 40% | $80,000 |

| After January 19, 2025 | 100% | $200,000 |

Seneca Cost Segregation has delivered an average first-year deduction of $171,243 across more than 10,200 properties nationwide. Every study is backed by an AuditDefense guarantee and completed within 2-4 weeks.

Engineering-based studies differ from software-only approaches by including on-site inspections, detailed engineering drawings, and component-level analysis by licensed professional engineers. That documentation is what makes deductions defensible under IRS scrutiny.

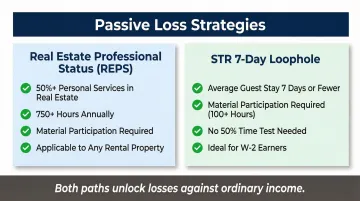

Unlock the Real Estate Professional Status (REPS) or the Short-Term Rental Loophole

Passive loss rules normally suspend rental losses from offsetting ordinary W-2 or business income. Two strategies remove this limitation.

Real Estate Professional Status (REPS)

Qualifying as a Real Estate Professional removes the passive classification and allows losses to offset any income type. Requirements under IRC §469(c)(7):

- More than 50% of your personal services during the year must be performed in real property trades or businesses

- You must perform more than 750 hours of services in those real property trades or businesses

Critical: REPS must be paired with material participation in your specific rental activities to be effective. Qualifying for REPS only removes the automatic passive designation—you must also meet one of the seven material participation tests (such as participating for more than 500 hours) to deduct losses against ordinary income.

For investors who can't meet the REPS time requirements, the short-term rental classification offers an alternative path.

The Short-Term Rental (STR) Loophole

Properties with an average rental period of 7 days or fewer are not classified as passive rental activities under IRC §469. With material participation, losses generated from these properties can offset ordinary income without requiring full REPS qualification.

Key considerations:

- You must track and document average guest stay length

- Material participation still required (typically 100+ hours if you're the primary participant)

- Providing substantial hotel-like services (daily cleaning, meals) may trigger self-employment taxes

This loophole is often the most viable path for W-2 employees to generate nonpassive real estate losses, since the >50% time test for REPS is difficult to meet with a full-time job.

REPS vs. STR Loophole: Comparison

| Feature | Real Estate Professional Status (REPS) | STR Loophole |

|---|---|---|

| Primary Requirement | >50% personal services in real property + >750 hours | Average rental period ≤7 days |

| Material Participation Required | Yes | Yes |

| Losses Offset | Any income type | Ordinary income |

| Practical for W-2 Employees | Difficult (50% time test) | More viable path |

| IRS Code | IRC §469(c)(7) | IRC §469 |

Strategies to Reduce Taxes at Sale or Exit

Capital gains exposure at sale is predictable and plannable. Investors who wait until closing to think about taxes miss strategies that require advance preparation. Timing and structure are the primary levers.

Capital Gains Timing and Offset Strategies

Hold for Long-Term Treatment

The simplest tax reduction decision: hold the property for more than one year. Long-term capital gains rates for 2025 are far below short-term rates:

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | $0–$48,350 | $48,351–$533,400 | Over $533,400 |

| Married Filing Jointly | $0–$96,700 | $96,701–$600,050 | Over $600,050 |

Short-term gains (≤1 year holding period) are taxed at ordinary income rates up to 37%.

Tax-Loss Harvesting

Sell underperforming investments in the same tax year to offset gains from the property sale. The IRS allows you to use capital losses to offset capital gains dollar-for-dollar. If losses exceed gains, you can deduct up to $3,000 per year against ordinary income, with unlimited carryforward for excess losses.

Release Suspended Passive Losses

If you've accumulated suspended passive losses from the property over the years (losses that couldn't be used due to passive activity rules), a fully taxable sale to an unrelated party releases all suspended losses. These can offset the capital gains and depreciation recapture generated by the sale.

Offsetting gains is one side of the equation. The other is deferring or eliminating the tax liability at sale entirely.

Tax Deferral and Elimination Strategies

1031 Like-Kind Exchange

IRC §1031 allows investors to defer capital gains taxes entirely by reinvesting sale proceeds into like-kind replacement property. The Tax Cuts and Jobs Act limited exchanges strictly to real property held for investment or productive use in a trade or business.

Strict IRS timelines:

- 45 days: Identify replacement property in writing to your Qualified Intermediary

- 180 days: Close on replacement property (or tax return due date, whichever is earlier)

Requirements for total deferral:

- Replacement property must be equal or greater value than relinquished property

- All equity must be reinvested (no cash taken out)

- Debt on replacement property must equal or exceed debt on relinquished property

Receiving cash or non-like-kind property ("boot") triggers taxable gain to the extent of the boot received. A 1031 exchange defers tax—it does not eliminate it. The deferred gain carries forward until a future non-exchanged sale.

Installment Sale (Seller Financing)

Spreading sale proceeds over multiple years lets you control how much gain you recognize annually, which can keep you below the 20% threshold each year. You structure the sale so the buyer pays you over time, and you report gain proportionally as payments arrive.

Considerations:

- You'll collect interest income (taxable)

- You carry default risk if the buyer defaults

- Spreading recognition across years can also reduce your exposure to the 3.8% Net Investment Income Tax

Qualified Opportunity Zone (QOZ) Funds

Investors can defer capital gains by reinvesting them into a Qualified Opportunity Fund within 180 days of sale. The One Big Beautiful Bill Act made the QOZ program permanent and established a rolling five-year deferral for investments made after December 31, 2026.

Key benefits:

- Only the capital gain amount needs to be invested (not the entire proceeds)

- Applies to any capital gain (stocks, business sales, real estate)

- Gains on the QOZ investment itself may be eliminated if held 10+ years

QOZ vs. 1031 Exchange:

| Feature | 1031 Exchange | QOZ Fund |

|---|---|---|

| Eligible Gains | Real estate only | Any capital gain |

| Reinvestment Window | 45/180 days | 180 days |

| Capital Required | Entire proceeds | Only the gain amount |

| Tax Elimination | Defers only | Eliminates post-investment appreciation after 10 years |

Both QOZ and 1031 strategies involve strict eligibility rules and sequencing requirements that must be in place before closing, not after.

Conclusion

Most investors overpay on taxes not because they ignored the rules, but because they never had a plan. Understanding where each layer of tax originates, and applying the right strategy at the right time, is what separates investors who build wealth from those who hand it to the IRS by default.

The most effective approach combines multiple strategies across both ownership and exit phases:

- Maximize operating deductions and optimize depreciation structure at acquisition

- Use cost segregation and bonus depreciation to front-load deductions

- Use REPS or the STR loophole to activate passive loss deductions

- Plan exit timing and structure to minimize capital gains exposure

- Use 1031 exchanges, installment sales, or QOZ funds when appropriate

This requires proactive planning rather than reactive filing. Qualified professionals in cost segregation, tax strategy, and real estate law are positioned to implement these strategies correctly. Firms like Seneca Cost Segregation combine engineering-based cost segregation studies with complimentary tax strategy assessments, so you can identify the full scope of savings available before you file, not after.

Frequently Asked Questions

How can I avoid paying taxes on investment property?

Completely avoiding taxes isn't realistic, but you can sharply reduce them through depreciation deductions, cost segregation, 1031 exchanges, and qualifying for Real Estate Professional Status. Combining strategies across both ownership and sale phases, with professional guidance, produces the greatest results.

What is the $250,000 / $500,000 capital gains exclusion for homeowners?

Under IRC Section 121, homeowners who have lived in a property as their primary residence for at least 2 of the past 5 years can exclude up to $250,000 (single) or $500,000 (married filing jointly) in capital gains from taxes. This exclusion does not automatically apply to investment properties but can be accessed if you convert a rental to your primary residence.

What is depreciation recapture and how does it affect investment property taxes?

When a depreciated property is sold, the IRS "recaptures" previously claimed depreciation deductions by taxing them at up to 25%. This applies whether or not you actually took depreciation, making it critical to claim depreciation properly during ownership and plan for this tax at exit.

What is a 1031 exchange and how does it reduce capital gains taxes?

A 1031 exchange defers capital gains taxes by reinvesting full sale proceeds into like-kind property within IRS-mandated timelines (45-day identification, 180-day closing). The tax isn't eliminated; it's deferred until a future non-exchanged sale, allowing that capital to compound in the new investment.

Can I use cost segregation on a single-family rental property?

Cost segregation can be applied to single-family rentals, but it typically delivers its greatest benefit on multi-family, commercial, and higher-value properties with a depreciable basis of at least $300,000 (excluding land). A cost segregation specialist can confirm whether the study cost is justified by expected deductions.

What is the difference between short-term and long-term capital gains on investment property?

Properties sold within one year are taxed at ordinary income rates (up to 37%); hold longer than one year and you qualify for long-term capital gains rates of 0%, 15%, or 20%. Waiting at least 12 months before selling is one of the simplest tax reduction decisions an investor can make.