Introduction

Cost segregation can generate hundreds of thousands of dollars in first-year tax deductions, but the ability to use those deductions depends on a factor most investors overlook: their tax classification with the IRS.

Two investors can own identical properties, commission identical cost segregation studies, and produce identical depreciation deductions, yet walk away with completely different tax outcomes. Whether one qualifies as a Real Estate Professional (REP) determines everything. For the REP, a $200,000 depreciation loss might eliminate their entire tax bill. For the non-REP, that same $200,000 sits in suspension, unusable against their W-2 income.

This article explains what REP status is, how it unlocks or limits cost segregation savings, the qualification requirements, and what non-REPs can do to still benefit from accelerated depreciation.

TLDR

- Cost segregation accelerates depreciation, but passive loss rules often prevent those deductions from offsetting W-2 wages

- REP status reclassifies rental activity as active, allowing depreciation losses to offset any income type immediately

- Qualification requires 750+ hours in real estate activities AND more than 50% of total working time in real estate

- Non-REPs can still benefit through the short-term rental loophole or passive income offset strategies

- Detailed time logs and a material participation election are what make or break an IRS audit of REP status

The Passive Loss Problem: Why Cost Segregation Doesn't Always Pay Off Immediately

The IRS draws a sharp line between active and passive income. Active income covers wages, salaries, and business profits from activities where you materially participate. Passive income covers rental income and activities where you're not materially involved.

For most rental property owners, the IRS automatically classifies rental activities as passive, regardless of how much time you spend managing the property. Losses from those activities, including accelerated depreciation deductions from a cost segregation study, can only offset other passive income. They cannot touch W-2 wages or business profits.

When Passive Losses Get Suspended

When passive losses exceed passive income, the excess becomes "suspended" and carried forward to future tax years. This delays the full tax benefit of a cost segregation study, sometimes by years or even decades.

Example: You commission a study that generates $180,000 in first-year depreciation. Your rental property produces $30,000 in net income before depreciation. After applying the depreciation, you have a $150,000 loss. If you have no other passive income and don't qualify as a REP, that $150,000 loss sits in suspension rather than reducing your current year's tax bill.

The $25,000 Exception (That Doesn't Help Most Investors)

The IRS does provide a small carve-out: taxpayers who actively participate in rental activities and earn under $100,000 in adjusted gross income (AGI) can deduct up to $25,000 in passive losses against ordinary income. This allowance phases out completely at $150,000 AGI, making it effectively useless for the high-income investors who stand to benefit most from cost segregation.

Why This Matters for Cost Segregation

A properly executed cost segregation study can generate $100,000 to $500,000+ in first-year depreciation deductions. But if you're classified as passive, most or all of that benefit sits in suspension rather than reducing the current year's tax bill. The deduction isn't lost forever. It carries forward and becomes available when you sell the property in a taxable transaction, but the immediate cash flow benefit disappears.

In short:

- Passive investors defer the benefit until a future sale or passive income event

- REP-qualified investors can apply those deductions against ordinary income now

- The difference in timing can mean years of delayed tax savings

What It Takes to Qualify as a Real Estate Professional

REP status is the IRS classification that removes rental activities from the passive category, allowing depreciation losses to offset any income type in the year they're generated.

The Two Primary IRS Tests

To qualify as a REP, you must satisfy both of the following tests during the tax year:

| Test | Requirement |

|---|---|

| 750-Hour Test | You must spend more than 750 hours during the tax year in real estate trades or businesses in which you materially participate |

| 50% Test | More than 50% of your total personal services across all trades or businesses must be in real estate activities |

Both tests must be satisfied. Meeting one but not the other disqualifies you.

Material Participation: The Third Hurdle

Qualifying as a REP at the federal level is not sufficient on its own. You must also materially participate in each individual rental activity (or make a grouping election to treat all rentals as one activity).

The most commonly applied material participation tests include:

| Test | Requirement |

|---|---|

| 500-Hour Threshold | You log more than 500 hours in the rental activity during the year |

| 100-Hour Comparative Test | You exceed 100 hours and no other individual, including employees and contractors, participates more than you |

| Facts-and-Circumstances | You participate on a regular, continuous, and substantial basis for more than 100 hours (risky, as the IRS frequently challenges this one) |

The Spouse Strategy

For married couples filing jointly, only one spouse needs to meet the 750-hour and 50%-of-time requirements. Hours cannot be combined across spouses to satisfy the test, but once one spouse qualifies, the entire household benefits, even if the other works full-time outside real estate.

The W-2 Employee Challenge

Full-time W-2 employees in non-real-estate fields face an uphill battle. If you work 2,000 hours per year in another profession, you would need to spend more than 2,000 hours in real estate activities to satisfy the 50%-of-time test.

In Warren v. Commissioner, the Tax Court ruled that a taxpayer who worked 1,913 hours at Lockheed Martin failed the REP test because he only logged 1,628 hours in real estate. To pass the 50% test, his real estate hours had to strictly exceed his W-2 hours.

For most W-2 employees, clearing that bar realistically requires stepping back from traditional employment, or having a qualifying spouse who manages the portfolio full-time.

REP Status + Cost Segregation: The Real Tax Math

The difference between REP and non-REP status isn't theoretical. It's measured in tens of thousands of dollars of tax savings.

The Scenario

Consider an investor who purchases a $1.5 million residential rental property. After allocating 20% to land ($300,000), the depreciable basis is $1.2 million.

A cost segregation study reclassifies 25% of that building basis ($300,000) into 5-, 7-, and 15-year asset classes. With 100% bonus depreciation available for property placed in service after January 19, 2025, the study generates a $300,000 first-year depreciation deduction.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate |

|---|---|

| September 27, 2017 – December 31, 2022 | 100% |

| January 1, 2023 – December 31, 2023 | 80% |

| January 1, 2024 – December 31, 2024 | 60% |

| January 1, 2025 – January 18, 2025 | 40% |

| January 19, 2025 – December 31, 2030 | 100% (if acquisition date is January 19, 2025 or later) |

If acquisition date is before January 19, 2025:

- 40% bonus depreciation applies in 2025

- 20% bonus depreciation applies in 2026

Non-REP Scenario: Suspended Losses

Here's how the same numbers play out under each classification:

| Non-REP Investor | REP Investor | |

|---|---|---|

| W-2 Income | $200,000 | $200,000 |

| Depreciation Deduction | $300,000 | $300,000 |

| Loss Classification | Passive (suspended) | Active (deductible) |

| Year-One Tax Offset | $0 | $111,000 federal |

| With State Taxes | No change | $130,000+ total savings |

Without REP status, the $300,000 loss sits in suspension, carried forward but unavailable until the investor generates passive income or sells the property. With REP status, that same deduction offsets W-2 income directly, producing a real return on the cost of the study in year one.

Real-World Data

Seneca Cost Segregation clients achieve an average first-year deduction of over $171,243. The full value of that deduction against active income is only realizable when the investor qualifies as a REP or uses one of the alternative strategies described below.

The Compounding Advantage

That gap compounds over time. Depreciation deductions taken immediately can be reinvested or deployed into additional properties, while passive losses that stay suspended produce nothing in the meantime. Over a 10-year investment horizon, an investor who consistently offsets active income with cost segregation deductions can acquire additional assets years ahead of a comparable investor waiting to unlock those same losses.

If You Don't Qualify as a REP: Strategies That Still Work

Not qualifying as a REP doesn't mean cost segregation is worthless. Several alternative strategies can still deliver real tax savings.

| Strategy | Key Condition | Income Offset |

|---|---|---|

| Short-Term Rental (STR) Loophole | Average guest stay of 7 days or fewer; material participation required | Active income |

| Passive Income Offset | Other passive income sources available | Passive income only |

| Release on Sale | Property sold in a taxable transaction | Capital gain offset |

The Short-Term Rental (STR) Loophole

Rental properties with an average guest stay of 7 days or fewer are not classified as rental activities under IRC §469. They're treated as business activities, meaning cost segregation depreciation losses can potentially offset active income if the investor materially participates, without requiring REP status.

Key requirements:

- Average guest stay must be 7 days or fewer

- You must materially participate in the activity (most commonly satisfied by the 100-hour test: you spend 100+ hours managing the property and no one else spends more time than you)

Example: A nurse earning $150,000 annually purchases a $750,000 short-term rental in a mountain town. A cost segregation study identifies $180,000 in accelerated depreciation. Because the average stay is under 7 days and the nurse spends 120 hours managing the property (more than the cleaning service), the $180,000 loss offsets nursing income directly, potentially saving $66,000+ in taxes.

Passive Income Offset

Investors with other passive income sources, such as interests in passive partnerships, rental properties generating net income, or royalties, can use suspended passive losses from cost segregation to offset those passive gains.

This approach won't offset W-2 or active business income, but it does reduce overall tax liability and frees up cash flow that would otherwise go to the IRS.

Key situations where this applies:

- Passive partnership distributions subject to tax

- Net rental income from other long-term rentals

- Royalty income classified as passive under IRC §469

Release on Sale

Passive losses are fully released and deductible in the year a property is sold in a taxable sale. A non-REP investor can still benefit from carried-forward cost segregation losses at the point of sale, sometimes delivering a concentrated deduction that offsets a significant portion of the capital gain recognized.

Protecting Your REP Status: Documentation the IRS Will Accept

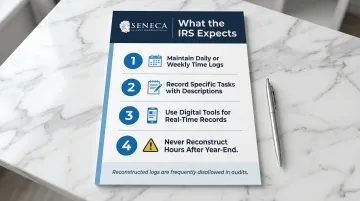

REP status is one of the most frequently audited tax positions for real estate investors. The tax benefits are substantial, and the IRS scrutinizes claims carefully. Documentation is not optional. It's essential.

What the IRS Expects

The IRS expects a contemporaneous time log that records the date, hours spent, and specific activities performed for each real estate task. After-the-fact reconstructions are generally viewed unfavorably and may be disallowed entirely during an audit.

| Case | Court Finding |

|---|---|

| Moss v. Commissioner | The Tax Court ruled that the regulations "do not allow a postevent 'ballpark guesstimate.'" |

| Manalo v. Commissioner | The court rejected a taxpayer's revised logs created years after the fact, calling them "uncorroborated and unreliable." |

Best practices:

- A daily or weekly time log maintained throughout the year provides a contemporaneous record

- Specific task descriptions (e.g., "reviewed lease agreements," "coordinated with contractor on HVAC repair," "toured property with prospective tenant") support log accuracy

- Digital tools (calendar apps, time-tracking software) generate real-time records

- Time logs reconstructed at year-end are more likely to be challenged or disallowed during an audit

The Grouping Election

Time logs protect your hours, but if you own multiple rentals, how those properties are structured matters just as much. Investors who own multiple rental properties can make an IRC §469(c)(7)(A) election to group all rental activities as a single activity. This simplifies material participation tracking and prevents a scenario where you qualify as a REP at the federal level but still fail to materially participate in each individual property.

The filing mechanics are straightforward:

- The election is made by filing a statement with the original income tax return

- If you missed the deadline, the IRS provides relief for late elections under Revenue Procedure 2011-34

- Once made, the grouping election applies to all future years unless revoked

Frequently Asked Questions

Do you have to be a real estate professional to do cost segregation?

No, REP status is not required to commission a cost segregation study. Any property owner can benefit from one. However, without REP status, depreciation losses may be suspended as passive losses and cannot immediately offset active income like W-2 wages.

Can cost segregation losses offset W-2 income without REP status?

Under standard passive activity rules, cost segregation losses from long-term rental properties cannot directly offset W-2 income for most investors. The exception is the STR loophole: short-term rentals with average stays of 7 days or fewer and material participation can allow active income offsets without REP qualification.

Can my spouse qualify as the real estate professional for our household?

Yes. In a married filing jointly household, only one spouse needs to satisfy the 750-hour and 50%-of-time tests. Once that threshold is met, the entire household gains access to REP tax treatment, a significant advantage when one spouse works full-time in real estate.

What happens to my suspended passive losses when I sell a rental property?

Passive losses carried forward from prior cost segregation deductions are fully released and deductible in the year of a taxable sale of the property. This means non-REP investors can still realize the tax benefit of a cost segregation study, with the full benefit unlocked at disposition.

How does REP status interact with bonus depreciation?

Bonus depreciation accelerates the size of the first-year deduction; REP status determines whether that deduction can offset active income immediately. For REPs, combining both strategies in a single tax year produces the largest possible reduction in taxable income.

How many hours do I need to document to prove REP status to the IRS?

The IRS requires 750+ hours in real estate activities, representing more than 50% of total working time. A contemporaneous log with dates, tasks, and durations is the standard for IRS documentation, as reconstructed records are frequently challenged during audits.