Introduction: Why Advanced 1031 Strategies Separate Portfolio Builders from One-Time Tax Savers

Most real estate investors complete a 1031 exchange once, defer a single taxable event, and move on — never realizing the same mechanics can be stacked and repeated to systematically defer millions across an entire portfolio. Reverse exchanges, construction exchanges, and DST/721 combinations aren't just alternatives to a standard exchange. Used deliberately, they become repeatable tools for compounding equity without the tax drag that stops most investors from scaling.

The difficulty is execution. Tight timelines, complex financing, depreciation carryover, and legislative uncertainty make these strategies easy to misfire. A single misstep during the 45-day identification window — or a violation of Exchange Accommodation Titleholder (EAT) rules — can disqualify the entire exchange.

This guide covers the specific mechanics of each advanced structure, the compliance requirements that protect your deferral, and how to combine multiple techniques for compounding tax efficiency across successive transactions.

TLDR: Key Advanced 1031 Strategies at a Glance

- Reverse exchange: Buy the replacement property first using an EAT to park the asset, before selling the relinquished property

- Construction exchange: Use 1031 proceeds to fund improvements or new builds through an EAT within the 180-day window

- DSTs and 721 exchanges: Move from direct ownership into fractional institutional real estate, then into REIT operating partnership units, all tax-deferred

- Cost segregation on replacement property: Accelerate depreciation on the new property's excess basis to offset the low carried-over basis

- Primary conversion, refinancing, and related party tactics: Each carries specific IRS requirements that can make or break deferral

Reverse 1031 Exchange: How to Buy Before You Sell

The Problem a Reverse Exchange Solves

Investors in competitive markets often spot their ideal replacement property before their relinquished property has sold. IRC §1031(a)(3) does not permit a simple "buy first, sell second" structure without additional legal architecture. Without a reverse exchange, you face a forced choice: lose the replacement property or abandon the 1031 altogether.

The Exchange Accommodation Titleholder (EAT)

A Qualified Intermediary creates a separate LLC—the Exchange Accommodation Titleholder—that takes legal title to either the replacement or the relinquished property, "parking" it while the exchange is in progress. There are two parking strategies:

- "Exchange Later" (park replacement): The EAT holds the replacement property while you sell your relinquished property

- "Exchange First" (park relinquished): The EAT holds your relinquished property while you acquire the replacement

The QEAA Safe Harbor: Revenue Procedure 2000-37

A Qualified Exchange Accommodation Arrangement (QEAA) is what qualifies the structure for IRS safe harbor protection. Rev. Proc. 2000-37 allows the EAT to act as beneficial owner for federal tax purposes, while restricting the taxpayer's relationship with the parked property to prevent constructive ownership.

One hard limitation governs timing: Rev. Proc. 2004-51 bars safe harbor protection if you owned the replacement property within 180 days before transferring it to the EAT. Plan accordingly—any prior ownership of the target property within that window disqualifies the entire structure.

The Financing Challenge

The EAT has no funds of its own and must borrow 100% of the purchase price. Three financing options exist:

- Investor loans funds to EAT: You lend the purchase price directly to the EAT

- Third-party loan guaranteed by investor: A lender provides financing with your personal guarantee

- Combination: Mix of investor capital and third-party financing

Securing financing is where most reverse exchanges stall. Lenders unfamiliar with EAT structures often require full recourse terms, higher cash reserves, and shorter loan periods than a standard acquisition—plan for those conditions before you commit to the structure.

The 180-Day Maximum

The parked property cannot sit with the EAT beyond 180 calendar days. The relinquished property sale and exchange completion must both happen within that window. The standard 45-day identification rule still applies—if you're parking the replacement property, you must identify the relinquished property within 45 days of the EAT taking title.

Construction (Improvement) Exchange: Build or Improve with Deferred Proceeds

The Core Prohibition and Workaround

Investors cannot directly apply 1031 sale proceeds to labor or materials because the IRS classifies improvements as "not like-kind" to real property. A workaround using an EAT is required before the investor takes title.

The EAT Mechanism for Construction Exchanges

How it works:

- You sign a purchase contract with the seller

- You assign purchase rights to the EAT

- The EAT takes title and holds the property while improvements are made

- You direct all improvements under a Project Management Agreement with your Qualified Intermediary — this agreement is the legal bridge that keeps your control over the build-out compliant with exchange rules

The safe harbor allows you or a disqualified person to manage the property, supervise improvements, or act as a contractor for the EAT without violating exchange rules.

The 180-Day Constraint

The entire process—EAT purchase, all improvements, and your taking final title—must be completed within 180 calendar days of the relinquished property sale closing. Pre-planning with contractors and securing permits before the exchange begins is critical.

If planned improvements are not completed within 180 days, you'll recognize gain on any unimproved portion treated as boot.

Case Law Boundaries and IRS Non-Acquiescence

In Bartell v. Commissioner, the Tax Court allowed a 17-month parking period outside the safe harbor. However, the IRS issued Action on Decision 2017-06 stating non-acquiescence, warning that it will not follow the opinion for transactions outside Rev. Proc. 2000-37's scope. Transactions outside that safe harbor carry real audit exposure — adhere to the 180-day limit to protect your deferral.

Two Exit Options for Unwinding the Exchange

- Direct deed closing: The EAT conveys the improved property to you through a standard closing — straightforward, but requires a full title transfer process

- Membership interest assignment: You acquire ownership of the EAT entity itself, skipping the deed transfer — often faster and preserves any existing financing already in place

Delaware Statutory Trusts and 721 Exchanges: The Institutional Evolution of 1031 Strategy

DSTs as an Advanced Replacement Property Vehicle

Delaware Statutory Trusts offer fractional beneficial interests in large, institutional-quality real estate assets—multifamily, industrial, net-leased, medical office. Revenue Ruling 2004-86 established that DSTs qualify as like-kind replacement property, provided the trustee's powers are strictly limited (no power to dispose of property and acquire new property, or renegotiate leases).

For 1031 investors working against tight deadlines, DSTs solve three structural problems:

- Precision equity matching: Allocate exchange proceeds across multiple DSTs to hit your required reinvestment target within the 45-day window

- Access to institutional assets: Fractional ownership gives individual investors entry into assets typically reserved for institutional buyers

- No landlord responsibilities: Property management, leasing, and operations are handled by the DST sponsor

In 2025, DST fundraising totaled $8.2 billion, a 45.4% increase from the prior year—a signal that more investors are prioritizing passive income over active management.

The 721 Exchange: Transitioning to REIT Operating Partnership Units

An investor contributes DST interests (or direct real estate) into the operating partnership of a REIT in exchange for OP units, typically on a tax-deferred basis under IRC §721. This enables a transition from illiquid, directly-owned real estate into diversified, potentially liquid REIT exposure without triggering a taxable event.

Used alone, the 721 exchange is a powerful tool. Combined with a 1031 and DST, it becomes part of a longer-term wealth-building sequence.

The Sequential "Staircase" Strategy

More investors are stringing these tools together in a deliberate sequence:

- Sell appreciated property

- 1031 into a DST

- Later execute a 721 exchange into a REIT operating partnership

This progression moves an investor from active landlord to passive real estate exposure — without a taxable event at any step — and can span multiple market cycles.

Estate Planning Dimension

Because the deferred gain is never recognized during the investor's lifetime under this structure, heirs receive a stepped-up basis at death under IRC §1014. In practice, this can eliminate the accumulated capital gains liability entirely — the deferred taxes simply disappear at death.

That outcome aligns directly with the "buy, borrow, die" strategy: accumulate appreciating assets, access liquidity through borrowing, and transfer wealth to heirs at a stepped-up basis.

Stacking Cost Segregation with Your 1031 Replacement Property

The Depreciation Carryover Problem

In a 1031 exchange, your tax basis in the relinquished property transfers to the replacement property under IRC §1031(d). This often means a very low adjusted basis and correspondingly small future depreciation deductions—especially problematic for investors who have held a property for many years or completed multiple prior exchanges.

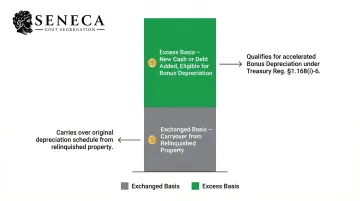

Treasury Regulation §1.168(i)-6: Exchanged Basis vs. Excess Basis

Treasury Regulation §1.168(i)-6 divides the basis of replacement MACRS property into two parts:

- Exchanged basis: The carryover basis from the relinquished property

- Excess basis: Any new cash or debt added during the acquisition

The excess basis is treated as newly placed in service and is eligible for bonus depreciation if the property qualifies.

100% Bonus Depreciation Restoration (2025)

The "One Big Beautiful Bill Act" (Public Law 119-21), enacted July 4, 2025, permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. This applies to the excess basis of 1031 replacement properties.

How Cost Segregation Maximizes First-Year Deductions

A cost segregation study on the newly acquired replacement property can generate substantial new accelerated depreciation by reclassifying eligible components:

- Personal property (5-year assets)

- Land improvements (15-year assets)

- Building components with shorter useful lives (7-year assets)

This front-loads depreciation deductions, offsetting income in the early years of ownership — and bonus depreciation applies to every qualifying component identified in the study.

Capturing these deductions requires an engineering-based study that correctly maps components to their appropriate asset classes. Seneca Cost Segregation has completed over 10,200 studies nationwide, with an average first-year deduction of $171,243 and CCSP-certified engineers producing audit-ready deliverables — identifying 20–40% of building basis for reclassification. A complimentary tax assessment can help determine whether a study fits your specific replacement property type and holding plan.

Other Advanced Tactics: Primary Conversion, Pre-Exchange Refinancing, and Related Party Rules

Primary Residence Conversion and the Section 121 Combination

Execute a 1031 exchange into a property you plan to eventually use as a primary residence. Rent it for at least two years ("seasoning" under Rev. Proc. 2008-16), then convert it. Once you meet the use requirements, it can qualify for the Section 121 exclusion — $250,000 for single filers, $500,000 for joint filers.

One critical limitation: IRC §121(b)(5) requires that gain be allocated to periods of "nonqualified use," which reduces the exclusion. Don't expect a completely tax-free exit. Calculate the nonqualified use ratio to project actual taxable gain before you sell.

Pre-Exchange Refinancing

Refinancing the relinquished property before a 1031 exchange is permissible only if you have an independent economic reason (cash flow issues, a separate investment opportunity). Refinancing purely to extract equity just before a sale is treated by the IRS as taxable boot under the step-transaction doctrine.

In Fredericks v. Commissioner, the Tax Court upheld cash-out refinancing because it was independent of the exchange, not conditioned on closing, and completed sufficiently in advance. If pre-exchange refinancing is unavoidable, document a clear, non-tax business purpose well before the sale closes — or better yet, refinance the replacement property post-exchange instead.

Related Party Exchanges

Related-party transactions carry their own landmines under IRC §1031(f). When buying replacement property from a family member or controlled entity, both parties must hold their respective properties for at least two years — otherwise the IRS disallows the exchange.

Key rules to know:

- Two-year hold requirement: Applies to both sides of the exchange when a related party is involved as the replacement property seller

- QI workaround doesn't hold up: Revenue Ruling 2002-83 makes clear that routing the deal through a Qualified Intermediary won't save you. If the related party cashes out after the exchange, the IRS treats the structure as tax avoidance — and the transaction becomes fully taxable

- Direction matters: Selling your relinquished property to a related party is generally permitted; buying replacement property from a related party is where the restrictions hit hardest

The 2026 Legislative Landscape: What Investors Need to Know Now

Ongoing Legislative Uncertainty

The Biden Administration's FY2025 budget proposed limiting 1031 deferral to $500,000 per taxpayer ($1 million for married filing jointly) per year — a change the Tax Foundation estimated would raise $17.9 billion over 10 years.

That proposal didn't survive. The "One Big Beautiful Bill Act" (PL 119-21), enacted July 4, 2025, left Section 1031 fully intact for real property exchanges. Even so, investors building long-term exchange chains should keep legislative risk on their radar — prior proposals show Congress views high-dollar deferrals as a revenue target.

Key facts to track:

- Section 1031 remains unchanged under current law as of July 2025

- The $500,000 cap proposal has been introduced in multiple prior budget cycles

- Real estate accounts for over 90% of gains deferred by individuals annually

- Future proposals could resurface with different thresholds or phase-in structures

Step-Up in Basis at Death: The Ultimate Backstop Strategy

That legislative uncertainty makes the death step-up worth understanding as a built-in hedge. Under IRC §1014, heirs inherit property at its fair market value on the date of death — not the original cost basis. For investors who have chained multiple 1031 exchanges, this can wipe out decades of deferred capital gains entirely.

In other words: even if Congress eventually caps 1031 deferrals, investors who hold exchanged property until death may face zero tax on those gains. That outcome makes long-term exchange planning an estate strategy as much as a tax strategy.

The Joint Committee on Taxation estimated the tax expenditure for like-kind exchanges at $9.9 billion in 2019, with real estate transactions accounting for over 90% of gains deferred by individuals. That scale explains why 1031 reform keeps appearing in federal budget proposals — and why investors should treat the current legislative window as an opportunity to structure exchanges with long-term flexibility built in.

Frequently Asked Questions

What is a 1031 exchange and how does it work as a tax strategy?

A 1031 exchange allows investors to sell investment property and defer capital gains and depreciation recapture taxes by reinvesting proceeds into like-kind replacement property through a Qualified Intermediary. The deferred gain carries forward in the replacement property's basis, allowing indefinite tax deferral through sequential exchanges.

How can I defer capital gains taxes using a 1031 exchange?

Full deferral requires meeting four conditions:

- Purchase replacement property of equal or greater value

- Replace all debt or equity from the relinquished property

- Use a Qualified Intermediary to hold proceeds

- Meet the 45-day identification and 180-day closing deadlines

Any cash received or debt not replaced triggers taxable boot.

How many replacement properties can I identify in a 1031 exchange?

The three-property rule lets you identify up to three replacement properties of any value within the 45-day window. Identifying more triggers the 200% rule — total identified value cannot exceed 200% of the sale price — unless you close on at least 95% of all identified property value.

What is the 2-year holding rule for 1031 exchanges?

Under IRC §1031(f), related-party exchanges require both parties to hold their respective properties for at least 24 months post-exchange. The same 24-month threshold applies to primary residence conversions under Rev. Proc. 2008-16, where rental use must precede any conversion to personal use.

Will the 1031 exchange tax deferral be eliminated or changed in 2026?

1031 exchanges remain intact following passage of the "One Big Beautiful Bill Act" (PL 119-21) in July 2025. That said, investors with large appreciated portfolios should monitor proposals that would cap deferral above certain dollar thresholds — completing exchanges sooner reduces exposure if limits are introduced.