This guide unpacks seven core strategies that allow real estate investors to legally reduce, defer, or eliminate federal tax liability on rental income and property gains. From accelerated depreciation to capital gains deferral, each technique represents a deliberate policy choice designed to reward property ownership. Investors who understand and apply these provisions correctly can keep significantly more of what they earn, reinvesting capital into portfolio growth rather than handing it to the IRS.

TLDR: Key Takeaways

- The IRS tax code contains multiple legal provisions that defer or eliminate taxes on real estate income and gains

- Cost segregation turns 20–40% of property costs into front-loaded deductions, generating immediate tax savings in year one

- 1031 exchanges allow indefinite capital gains deferral by rolling proceeds into like-kind properties

- Real Estate Professional Status converts passive rental losses into active deductions that offset W-2 income

- Stacking strategies like cost segregation, 1031 exchanges, and the QBI deduction multiplies your total tax savings

What "Tax Loopholes" Actually Mean for Real Estate Investors

Real estate "tax loopholes" aren't illegal schemes. They're provisions explicitly written into the Internal Revenue Code by Congress to incentivize real estate investment, property improvement, and community development. Understanding the line between tax avoidance (legal) and tax evasion (illegal) matters. Tax evasion means underreporting income or providing false information to the IRS. Tax avoidance is the entirely legal practice of arranging your finances to maximize rightful deductions, credits, and adjustments.

The U.S. tax code treats real estate investors more favorably than most other income earners because property ownership drives housing supply and broader economic activity. Congress has backed this with real dollars: the Joint Committee on Taxation estimates the tax expenditure for like-kind exchanges at $52.0 billion for 2024-2028.

Depreciation advantages for rental housing add another $27.1 billion in tax expenditures for 2025-2029, a clear signal of how deeply embedded these incentives are in the tax code.

Investors who understand this framework can legally keep a far greater share of their income. The key is knowing which provisions apply to your situation, implementing them correctly, and keeping meticulous records to support your position if the IRS ever asks.

Depreciation and Cost Segregation: The Most Powerful Tax Reducer

The Modified Accelerated Cost Recovery System (MACRS) allows investors to deduct a property's cost (minus land value) over 27.5 years for residential rentals and 39 years for commercial property.

Here's what that looks like in practice: a residential rental purchased for $825,000 with a $125,000 land value yields a depreciable basis of $700,000. Standard depreciation produces an annual deduction of $25,455 ($700,000 ÷ 27.5 years), a predictable paper loss that offsets rental income year after year.

Accelerated Depreciation Through Cost Segregation

Cost segregation identifies property components such as fixtures, flooring, landscaping, and electrical systems that qualify for 5-, 7-, or 15-year depreciation schedules instead of 27.5 or 39 years. This allows investors to front-load the majority of deductions into the first few years rather than spreading them evenly.

The 2025 Bonus Depreciation Advantage:

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

| Period | Bonus Depreciation Rate |

|---|---|

| September 27, 2017 – December 31, 2022 | 100% |

| January 1, 2023 – December 31, 2023 | 80% |

| January 1, 2024 – December 31, 2024 | 60% |

| January 1, 2025 – January 18, 2025 | 40% |

| January 19, 2025 – December 31, 2030 (acquisition date January 19, 2025 or later) | 100% |

| 2025 (acquisition date before January 19, 2025) | 40% |

| 2026 (acquisition date before January 19, 2025) | 20% |

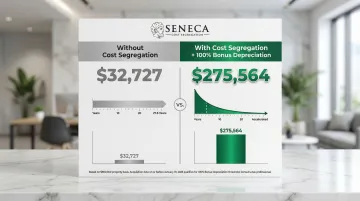

When combined with cost segregation, this creates significant first-year deductions. A property with a $900,000 cost basis could yield a first-year deduction of $275,564 with 100% bonus depreciation, compared to just $32,727 without cost segregation.

Engineering-Based Studies vs. Software Approaches

The IRS Cost Segregation Audit Techniques Guide explicitly warns examiners to view "rule of thumb" approaches with caution due to insufficient documentation. That documentation standard matters when you're claiming large deductions. Engineering-based studies, conducted by construction professionals who visit properties, review construction documents, and classify components based on direct analysis, give you a far stronger audit position than software-generated estimates.

Seneca Cost Segregation conducts engineering-based studies that have generated an average first-year deduction of $171,243 across more than 10,200 properties nationwide. Studies are completed in 2-4 weeks with detailed documentation built to withstand IRS scrutiny.

The firm generally recommends cost segregation for properties meeting these thresholds:

- Residential properties with a depreciable basis of $300,000 or more

- Commercial properties with a depreciable basis of $750,000 or more

Depreciation Recapture: The Exit Consideration

When you sell a depreciated property, the IRS reclaims tax benefits through depreciation recapture. The unrecaptured Section 1250 gain, the portion of long-term capital gain attributable to previously allowed straight-line depreciation, is taxed at a maximum rate of 25%. However, strategies like 1031 exchanges can defer this liability indefinitely, allowing investors to keep reinvesting without triggering recapture.

Capital Gains Tax Loopholes: The 1031 Exchange and Beyond

When you sell an investment property for more than its purchase price, the IRS taxes that gain. Short-term gains (held under 1 year) hit your ordinary income rate. Long-term gains (held over 1 year) qualify for preferential rates based on your income bracket.

2025 Long-Term Capital Gains Tax Brackets:

| Tax Rate | Single Filers | Married Filing Jointly |

|---|---|---|

| 0% | Up to $48,350 | Up to $96,700 |

| 15% | $48,351 to $533,400 | $96,701 to $600,050 |

| 20% | Over $533,400 | Over $600,050 |

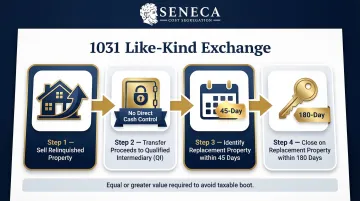

The 1031 Like-Kind Exchange

Section 1031 allows investors to defer 100% of capital gains taxes by reinvesting all net proceeds from a property sale into a qualifying replacement property. Done correctly, you can chain exchanges indefinitely, passing appreciated property to heirs at a stepped-up basis and never paying the deferred tax at all.

Critical 1031 Requirements:

- 45-day identification window: You must identify replacement properties in writing within 45 days of selling the relinquished property

- 180-day closing window: You must receive the replacement property within 180 days or by your tax return due date, whichever is earlier

- Qualified Intermediary: You must use a QI to hold proceeds, as taking control of cash triggers immediate taxable gain

- Equal or greater value: The replacement property must be of equal or greater value to avoid taxable "boot"

These deadlines are absolute and non-extendable. Missing either deadline disqualifies the exchange and triggers full capital gains taxation.

Strategic Gain Timing and Loss Harvesting

If you're sitting on capital losses from stocks, funds, or other investments, timing a property sale in the same tax year lets those losses offset your real estate gains dollar-for-dollar. A $50,000 stock loss in December can wipe out $50,000 of gain from a property sold that same year — reducing or eliminating what you owe. Capital gain and loss positions across the full investment portfolio are relevant to the timing of a property sale's closing date.

Primary Residence Conversion Strategy

Investors who convert a rental property into their primary residence for at least 2 of the 5 years before selling may qualify for the Section 121 exclusion of $250,000 for single filers, $500,000 for married filing jointly. However, any depreciation claimed during the rental period is subject to unrecaptured Section 1250 recapture and cannot be excluded.

Opportunity Zone Investments

Beyond deferral strategies, Opportunity Zones offer a path to outright tax elimination on future gains. The OBBBA legislation overhauled the program's timeline. Here's what applies to new investments made after December 31, 2026:

| Feature | New Investments (After Dec 31, 2026) | Legacy Investments (Before Jan 1, 2027) |

|---|---|---|

| Deferral Window | Rolling 5-year deferral window from the date of investment (replacing the hard December 31, 2026 deadline) | Original gain deferral deadlines |

| Basis Step-Up | Single 10% basis step-up after 5 years | Old basis step-up schedule |

| Long-Term Growth | Tax-free growth on post-investment gains if held 10+ years | — |

| Rural Opportunity Zones | Enhanced 30% basis step-up after 5 years for Qualified Rural Opportunity Zones | — |

Investments made before January 1, 2027 remain under the original Opportunity Zone rules, including the old basis step-up schedule and gain deferral deadlines. If you hold both legacy and new QOZ positions, your tax treatment differs between them, and the applicable rules determine the projected exit tax treatment.

Income Reduction Strategies: REPS, QBI Deduction, and Deductible Expenses

Real Estate Professional Status (REPS)

The IRS normally classifies rental income and losses as "passive," meaning rental losses can only offset other passive income (excluding W-2 and business income). Investors who qualify as Real Estate Professionals can reclassify their real estate activity as "active," unlocking the ability to deduct rental losses, including depreciation, against any income source.

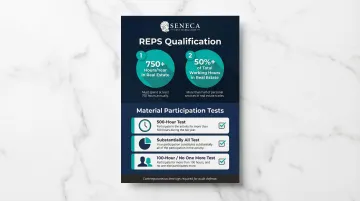

REPS Qualification Requirements:

- More than 750 hours per year spent in real estate activities

- More than 50% of total working hours spent in real estate

High-earning spouses frequently use this strategy to offset household W-2 income. Qualifying taxpayers can also make an irrevocable election under Treasury Regulation 1.469-9(g)(3) to group all rental real estate interests as a single activity, making it easier to meet material participation thresholds across a portfolio. Either way, contemporaneous time logs are essential for audit defense.

Material Participation Tests:

After qualifying for REPS, you must also materially participate in the rental activity. The most common tests include:

| Test | Requirement |

|---|---|

| 500-Hour Test | Participate for more than 500 hours during the year |

| Substantially All Test | Your participation constitutes substantially all participation by all individuals |

| 100-Hour/No One More Test | Participate more than 100 hours, and no one else participates more than you |

Contemporaneous time logs detailing hours, dates, and descriptions of services performed are required for IRS audit defense.

The Qualified Business Income (QBI) Deduction

Section 199A allows eligible real estate investors to deduct up to 20% of qualified rental income from their taxable income. Revenue Procedure 2019-38 provides a safe harbor treating rental real estate as a trade or business for QBI purposes if the enterprise:

- Maintains separate books and records

- Performs 250 or more hours of rental services annually

- Maintains contemporaneous time logs

Triple-net leases and personal residences are excluded from this safe harbor.

2025 QBI Phase-Out Thresholds:

| Filing Status | Phase-Out Begins | Fully Phases Out |

|---|---|---|

| Married Filing Jointly | $394,600 | $494,600 |

| Single Filers | $197,300 | $247,300 |

Beyond the QBI deduction, reducing taxable income also means capturing every legitimate operating expense. Together, these strategies compound your total tax reduction.

Deductible Operating Expenses

Real estate investors can deduct the following operating expenses:

- Property management fees

- Mortgage interest

- Property taxes

- Insurance premiums

- Repairs and maintenance

- Professional services (legal, accounting)

- Travel to and from properties

Repairs vs. Capital Improvements:

| Category | Tax Treatment |

|---|---|

| Repairs | Deductible in full in the year incurred |

| Capital Improvements | Must be depreciated over time |

The 2014 Tangible Property Regulations (TD 9636) require analyzing the "unit of property" and applying the RABI test (Betterment, Restoration, or Adaptation) to determine proper treatment.

Lesser-Known Tax Advantages Real Estate Investors Overlook

The Short-Term Rental Loophole

When a property is rented for an average of 7 days or fewer per guest, the rental activity may be classified as non-passive if the owner materially participates. This means losses can offset active income without requiring full REPS qualification.

Material Participation for STRs:

You need to meet just one of the material participation tests—such as the 100-hour/no-one-more test—rather than the stricter REPS requirements. This makes STRs particularly valuable for high-earning W-2 employees who want to use rental losses to offset ordinary income.

Short-term rentals naturally contain a higher percentage of components qualifying for accelerated depreciation, such as furniture, appliances, electronics, and specialized lighting, making them ideal candidates for cost segregation studies.

Self-Directed Retirement Accounts

Self-directed IRAs and Solo 401(k)s can hold real estate investments, allowing gains to grow tax-deferred (traditional) or tax-free (Roth). However, the IRS strictly enforces prohibited transaction rules under Section 4975.

Critical Restrictions:

- No self-dealing: Disqualified persons (including the account owner, spouse, and lineal descendants) cannot borrow from the account, sell property to it, or use the property for personal benefit

- Custodian requirement: A qualified custodian must hold and administer the account

- UDFI tax: If a self-directed IRA uses a non-recourse loan to buy property, it triggers Unrelated Debt-Financed Income tax

Solo 401(k) plans enjoy a specific statutory exemption from UDFI on leveraged real estate, making them superior vehicles for debt-financed acquisitions.

Combining These Strategies for Compounding Savings

Each of the strategies above works independently, but the real tax advantage comes from stacking them. Sophisticated investors combine multiple provisions to amplify outcomes. An investor who:

- Uses cost segregation to generate large depreciation losses

- Claims REPS status to apply those losses against ordinary income

- Executes a 1031 exchange when selling to defer capital gains

...can potentially pay near-zero taxes on both ownership and sale, reinvesting 100% of proceeds into the next deal. Identifying which combination applies to your portfolio is where the real work begins.

Seneca Cost Segregation's complimentary tax assessment goes beyond cost segregation to map these opportunities across your full portfolio. Notably, 70% of investors who complete the free assessment engage Seneca for additional strategy work, because the assessment consistently surfaces savings they hadn't accounted for.

Frequently Asked Questions

How do real estate investors avoid taxes?

Real estate investors use legal IRS provisions, including depreciation, 1031 exchanges, REPS, and QBI deductions, to reduce or eliminate taxes on rental income and property gains. These are lawful strategies written into the tax code, not evasion.

How to avoid paying taxes when selling real estate?

The 1031 exchange is the primary strategy for deferring capital gains taxes on investment property sales. By reinvesting all proceeds into like-kind replacement property within strict timelines, investors defer 100% of capital gains indefinitely. The primary residence exclusion and tax-loss harvesting also apply in specific scenarios.

What is the most overlooked tax break in real estate?

Cost segregation and accelerated depreciation remain severely underused. An engineering-based study can reclassify 20–40% of a building's basis into shorter depreciation schedules, front-loading deductions into year one rather than spreading them over 27.5 or 39 years.

What is the short-term rental tax loophole?

STR properties rented for an average of 7 days or fewer per stay may qualify for non-passive loss treatment if the owner materially participates. This allows depreciation losses to offset W-2 or other active income without needing full REPS qualification.

Do I need a professional cost segregation study to accelerate depreciation?

While investors can theoretically attempt component allocation themselves, a professionally conducted engineering-based study is required to withstand IRS scrutiny. The IRS Cost Segregation Audit Techniques Guide explicitly warns against rule-of-thumb approaches.

What is the 3-3-3 rule in real estate?

The 3-3-3 rule is a community guideline advising buyers to have 3 months of emergency savings, 3 months of mortgage reserves, and to evaluate 3 comparable properties before purchasing. This is a budgeting heuristic, not an IRS regulation or legal safe harbor.