Introduction

Most real estate investors know they can depreciate property, but far fewer realize they're leaving a 20% income deduction on the table every single year through the Section 199A qualified business income (QBI) deduction. For an investor netting $100,000 from rental properties, that's a potential $20,000 annual deduction—yet many miss it entirely because rental income doesn't automatically qualify.

The IRS has specific requirements that catch many property owners off guard. Getting them right can mean thousands of dollars saved annually; overlooking them means losing that deduction year after year.

This guide covers how the Section 199A deduction works, whether your rental qualifies, the safe harbor rule, income limits, and practical strategies to maximize the benefit, including how a cost segregation study can amplify your deduction if you're a high-income investor.

TLDR: Key Takeaways

- Section 199A allows eligible real estate investors to deduct up to 20% of qualified business income (QBI) from rental activities on their individual tax return

- Rental properties must qualify as a "trade or business" under IRC Section 162—passive investments don't count

- The IRS safe harbor (Rev. Proc. 2019-38) requires 250+ annual rental service hours, separate books, and contemporaneous time records

- High-income investors face W-2 wage and UBIA limitations that can reduce or eliminate the deduction

- Strategic planning through aggregation elections and cost segregation studies can maximize your eligible deduction

What Is the Section 199A Deduction and How Does It Work?

Section 199A was created by the Tax Cuts and Jobs Act (TCJA) of 2017 and allows owners of pass-through entities—sole proprietorships, partnerships, S corporations, LLCs, trusts, and estates—to deduct up to 20% of their qualified business income. The deduction appears on Line 13 of Form 1040 and applies at the individual level, not the business entity level.

Basic Calculation

The deduction equals 20% of net QBI from qualified rental activity, capped at the lesser of that amount or 20% of total taxable income (minus net capital gains).

Example:

- Net rental income: $100,000

- Potential Section 199A deduction: $20,000 (20% × $100,000)

- If taxable income is $90,000, the deduction is capped at $18,000 (20% × $90,000)

For most investors in the 22%–24% federal bracket, that $18,000–$20,000 deduction puts $4,000–$5,000+ back in their pocket — capital that can go directly toward the next acquisition.

Current Legislative Status

The deduction was originally set to expire after December 31, 2025. The One Big Beautiful Bill Act (Pub. L. 119-21), enacted July 4, 2025, changed that. Key updates include:

- Permanent status: Section 199A no longer sunsets — investors can plan around it long-term

- $400 minimum deduction: Applies to taxpayers with at least $1,000 of active QBI, effective for tax years beginning after December 31, 2025

Does Your Rental Property Qualify for Section 199A?

Rental income is presumed to be passive investment income by default, not trade or business income under IRC Section 162—and only trade or business income qualifies for the Section 199A deduction. Meeting this standard requires demonstrating both a profit motive and regular, continuous participation in the activity.

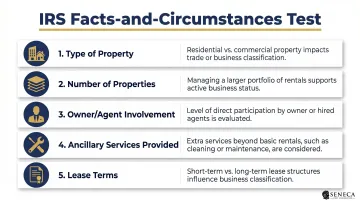

The IRS Facts-and-Circumstances Test

The IRS evaluates whether a rental rises to the level of a trade or business using several factors:

- Type of property — Residential vs. commercial rental characteristics

- Number of properties owned — Multiple properties strengthen the case

- Owner/agent day-to-day involvement — Active management vs. passive oversight

- Ancillary services provided — Maintenance, utilities, cleaning, concierge services

- Lease terms — Short-term vs. long-term, triple-net vs. traditional leases

The more factors you can document, the stronger your trade or business argument. Historical cases like Hazard v. Commissioner (7 T.C. 372) and Fackler v. Commissioner (133 F.2d 509) illustrate how courts have weighed regular involvement when evaluating this standard.

The NNN Lease Exception

Properties with triple-net leases face an uphill battle. Since the tenant handles taxes, insurance, and maintenance, the IRS argues the owner's activity lacks the hallmarks of an active business. Two key points for NNN landlords:

- NNN leases are explicitly excluded from the 199A safe harbor (discussed below)

- Qualification is still possible through a direct facts-based argument, but requires strong documentation

Investors holding NNN leases should work with a tax advisor to build that case proactively.

Self-Rental and SSTB Taint Rule

If a property owner rents to their own commonly controlled Specified Service Trade or Business (SSTB)—such as a law firm or medical practice—the rental income can become "tainted" and lose eligibility for the 199A deduction. The threshold is 50% or more common ownership between the rental entity and the SSTB. At that level, Treasury Regulation § 1.199A-5(c)(2) treats the rental activity as part of the SSTB for Section 199A purposes — eliminating the deduction.

For investors who don't fall into the SSTB trap, the IRS safe harbor offers a more predictable route to qualification — covered in the next section.

The Section 199A Safe Harbor: Requirements and Compliance

IRS Revenue Procedure 2019-38 established the formal safe harbor rule for rental real estate enterprises. Investors who meet all four requirements get IRS confirmation that their rental activity qualifies as a trade or business for 199A purposes — no subjective facts-and-circumstances argument required.

The safe harbor is optional. Missing it doesn't automatically disqualify your deduction, but you'll need to make the more subjective facts-and-circumstances case instead — a harder standard to meet and defend under audit.

Requirement 1: Separate Books and Records

Each rental real estate enterprise must maintain separate books reflecting income and expenses. Investors can group residential properties into one enterprise and commercial properties into another (but cannot mix the two). Within each enterprise, property-level income and expense statements must be maintained and can then be consolidated.

Requirement 2: The 250-Hour Rule

The taxpayer (or their employees, agents, or contractors) must perform at least 250 hours of rental services per year for the enterprise. This applies to the enterprise as a whole, not each individual property.

What counts toward 250 hours:

- Repairs and maintenance

- Tenant communications and rent collection

- Property management activities

- Advertising for tenants and leasing activities

- Purchasing materials and supplies

- Supervising employees and contractors

What does NOT count:

- Financial or investment analysis

- Arranging financing or procuring property

- Studying financial statements or appreciation monitoring

- Property improvements under IRC § 1.263(a)-3(d)

- Travel time to and from the property

Requirement 3: Contemporaneous Records

For tax years beginning after 2019, investors must maintain contemporaneous time logs documenting:

- Hours of all services performed

- Description of services

- Dates performed

- Who performed the services

This is the requirement investors most often neglect, and it creates the most audit exposure. Track time in real-time — not reconstructed at year-end. Property management software with activity logging is the most reliable way to satisfy this requirement.

Requirement 4: Written Statement

A statement confirming the enterprise meets safe harbor requirements must be attached to the timely filed tax return for each year the deduction is claimed. For investors with multiple rental enterprises, a single statement can be submitted but must list each enterprise separately.

Once you understand the four requirements, staying compliant comes down to consistent habits throughout the year — not a scramble at tax time.

Compliance Best Practices

- Track time in real-time using property management software or dedicated time logs

- Perform an annual review before filing season to verify the 250-hour threshold has been met

- Maintain documentation for at least three years (standard IRS audit window)

- Work with your CPA to ensure the written statement is properly attached to your return

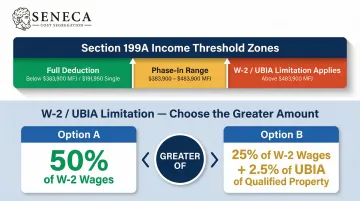

Income Thresholds and the W-2 Wage/UBIA Limitation

Section 199A uses a two-tier system based on taxable income.

2024 Income Thresholds

For the 2024 tax year, Rev. Proc. 2023-34 established the following thresholds:

| Filing Status | No Limitation (Below) | Full Limitation (Above) | Phase-In Range |

|---|---|---|---|

| Married Filing Jointly | $383,900 | $483,900 | $100,000 |

| Single / Other Returns | $191,950 | $241,950 | $50,000 |

Below the threshold: You receive the full 20% QBI deduction with no additional limitations.

Above the threshold: The deduction becomes limited to the greater of:

- (a) 50% of W-2 wages paid by the qualified trade or business, or

- (b) 25% of W-2 wages plus 2.5% of the unadjusted basis immediately after acquisition (UBIA) of all qualified depreciable property

What Is UBIA for Real Estate?

UBIA is the original cost basis of all depreciable tangible property (buildings, improvements, equipment) used in the rental business(the unadjusted figure before any depreciation is taken). Even investors with zero W-2 payroll can claim a significant deduction based on property basis alone.

Example: High-Income Investor Calculation

An investor with:

- Net rental income (QBI): $150,000

- W-2 wages paid: $0 (no employees)

- UBIA of rental properties: $2,000,000

Deduction calculation:

- Option (a): 50% of W-2 wages = $0

- Option (b): (25% × $0) + (2.5% × $2,000,000) = $50,000

- Allowable deduction: $50,000 (greater of the two)

This is why UBIA matters: even with zero payroll, this investor claims a $50,000 deduction (33% of their $150,000 QBI), thanks to their property basis.

The Phase-In Range

Taxpayers in the phase-in range receive a partial deduction. The limitation phases in proportionally based on how far your taxable income falls into the range.

Example:

- Married filing jointly with taxable income of $433,900 (halfway through the $383,900–$483,900 range)

- The W-2/UBIA limitation is applied at 50% strength

- If the full limitation would reduce your deduction from $30,000 to $20,000, the phase-in reduces it only to $25,000

Income planning near these thresholds — through retirement contributions, tax-loss harvesting, or strategic income timing — can preserve thousands in deductions. Dropping taxable income even $20,000–$30,000 can shift you from a partially limited to a fully unlimited deduction.

Strategies to Maximize Your Section 199A Deduction

Leverage the Aggregation Election

Investors who own multiple rental properties may elect to aggregate them into a single enterprise for purposes of the 250-hour requirement and the W-2/UBIA limitation test. This can significantly help investors who couldn't individually meet the hour threshold or wage test on each property alone.

Aggregation eligibility requirements (under Treas. Reg. § 1.199A-4):

- The same person or group must own 50% or more of each trade or business for a majority of the tax year

- All must use the same tax year

- None can be a Specified Service Trade or Business (SSTB)

- Satisfy at least two of three factors: (1) provide products/services customarily offered together, (2) share facilities or centralized business elements, or (3) operate in coordination or reliance upon one another

Important: Once elected, aggregation must be disclosed annually and cannot easily be reversed. Disaggregation is only permitted if a significant change in facts and circumstances causes the prior aggregation to no longer qualify.

Increase Qualified Property Documentation with a Cost Segregation Study

For investors above the income threshold who are relying on the UBIA-based limitation, properly documenting your qualified property basis is just as important as meeting the hour requirements. A professional cost segregation study identifies and classifies all depreciable components of a property—ensuring the full qualified property basis is accurately captured for the 2.5% UBIA calculation.

Cost segregation reclassifies components of your building from 27.5- or 39-year real property into shorter depreciation categories (5-year, 7-year, and 15-year property). UBIA is calculated before depreciation, so accelerated reclassification doesn't reduce your qualified property basis. It does, however:

- Confirms and documents your total qualified property basis for the 2.5% UBIA calculation

- Generates immediate depreciation deductions through bonus depreciation and accelerated schedules

- Strengthens audit defense by providing IRS-compliant engineering documentation

Seneca Cost Segregation uses an engineering-based methodology to identify every depreciable component across a property. With over 12 years of experience and more than 10,200 properties assessed nationwide, their studies document your UBIA for the Section 199A deduction while simultaneously generating accelerated depreciation deductions—two meaningful tax outcomes from a single study.

Example:

- Property purchase price: $2,000,000

- Land value: $400,000

- Depreciable basis: $1,600,000

- Cost segregation reclassifies 30% into shorter-life property

Result:

- UBIA for Section 199A: $1,600,000 (unchanged by accelerated depreciation)

- Section 199A UBIA component: 2.5% × $1,600,000 = $40,000

- Plus $200,000–$300,000+ in first-year accelerated depreciation from the study

Seneca's studies are completed within 2–4 weeks and come with AuditDefense and a money-back guarantee, ensuring IRS compliance and audit protection.

Consult a Tax Advisor to Model Your Specific Situation

The 199A deduction interacts with passive activity rules, real estate professional status (REPS), the short-term rental loophole, and bonus depreciation in ways that shift significantly based on individual income, property mix, and activity levels. Investors should run projections before year-end to determine whether they're on track to meet the safe harbor hours, whether aggregation is advantageous, and whether income shifting strategies could help them stay below the phase-out threshold.

Year-end planning checklist:

- Are you on track to meet 250 hours? If not, can you accelerate maintenance or leasing activities?

- Should you aggregate properties to pool hours and wages?

- If you're near the income threshold, can retirement contributions or charitable giving bring you below it?

- Would a cost segregation study strengthen your UBIA documentation and provide additional depreciation benefits?

Frequently Asked Questions

How does Section 199A deduction work?

Section 199A allows pass-through business owners and rental property investors to deduct up to 20% of their qualified business income on their individual tax return. The deduction is subject to income thresholds and the requirement that the activity qualifies as a trade or business under Section 162.

Who qualifies for Section 199A deduction QBI?

Individual taxpayers who receive income from sole proprietorships, partnerships, S corporations, LLCs, trusts, or rental real estate enterprises that qualify as a trade or business under Section 162 are eligible. C corporation income and employee wages do not qualify.

What property qualifies for Section 199A?

Qualifying property for the UBIA component includes depreciable tangible property used in the qualified trade or business during the year—for rental investors this primarily means buildings and improvements. The property must still be within its depreciable life under IRS guidelines.

What is one of the requirements for rental real estate to qualify for the Section 199A safe harbor?

The most notable requirement is performing 250 or more hours of rental services per year for the enterprise. These hours must be documented through contemporaneous records including time logs, descriptions of services, dates, and the names of who performed the work.

Can I aggregate rental properties for QBI?

Yes. Investors may elect to aggregate multiple rental properties into a single enterprise, which allows them to pool hours and W-2 wages across properties. This election must be made on a timely filed return and disclosed in every year it applies.

Where to report Section 199A deduction?

The deduction is reported on Form 8995 (simpler returns) or Form 8995-A (returns subject to the W-2/UBIA limitation or with multiple businesses). It flows to Line 13 of Form 1040 as a deduction from gross income.

Ready to maximize your Section 199A deduction and uncover hidden tax savings? Seneca Cost Segregation offers complimentary tax assessments to help you determine whether a cost segregation study can strengthen your UBIA documentation and accelerate your depreciation deductions. With over 10,200 properties assessed and an average first-year deduction of $171,243, Seneca's engineering-based studies are IRS-compliant and backed by audit defense.

Contact Seneca today at 503-383-1158 or visit senecacostseg.com to schedule your free consultation.