Introduction

The Opportunity Zone program offers a three-layer tax benefit—but most investors only recognize two. Everyone knows about the capital gains deferral and the 10-year appreciation exclusion. The third benefit, the one that quietly transforms cost segregation from a timing strategy into a permanent tax elimination tool, is depreciation recapture elimination.

This article is for real estate investors with capital gains to reinvest who are weighing a Qualified Opportunity Fund (QOF) and want to understand how depreciation and cost segregation interact with OZ rules to create compounding tax advantages.

According to Treasury Decision 9889 (2020), investors who hold QOF interests for 10 years can permanently eliminate all depreciation recapture—not just defer it. Layered with the One Big Beautiful Bill Act's restoration of 100% bonus depreciation, this stacks three permanent elimination layers that no other real estate tax structure currently matches.

TLDR

- Rolling capital gains into a Qualified Opportunity Fund (QOF) defers taxes, reduces the gain, and can eliminate them entirely after 10 years

- Cost segregation unlocks accelerated depreciation that reduces current-year taxable income

- After a 10-year hold, OZ rules permanently wipe out depreciation recapture — a major tax savings often overlooked

- The zero-basis problem is solved through qualified non-recourse debt in most OZ deals

- The One Big Beautiful Bill Act (2025) made OZ permanent and brought back 100% bonus depreciation

What Is the Opportunity Zone Depreciation Strategy?

The Opportunity Zone program, created by the 2017 Tax Cuts and Jobs Act under IRC Sections 1400Z-1 and 1400Z-2, directs capital gains into economically distressed census tracts via Qualified Opportunity Funds. For real estate investors, the program's real power lies in what happens to depreciation — not just the gains.

The Three Core OZ Tax Benefits

1. Capital Gains Deferral

The original capital gain from any source (stock sales, real estate, business interests) is deferred until the earlier of an inclusion event or the statutory deadline. Under the current framework, gains realized before December 31, 2026, must be recognized by that date. For investments made after January 1, 2027, a rolling 5-year deferral period applies.

2. Basis Step-Up

Investors who hold their QOF investment for at least 5 years receive a 10% basis step-up on the original deferred gain, effectively reducing the recognized gain by 10%. Under OZ 2.0, rural Qualified Opportunity Funds (QROFs) offer a 30% basis step-up instead—a meaningful upgrade for investors targeting qualifying rural markets.

3. Complete Appreciation Exclusion

After a 10-year hold period, investors can elect to step up their basis to fair market value on the date of sale, permanently eliminating all tax on appreciation.

The Fourth Benefit: Permanent Depreciation Recapture Elimination

Section 1400Z-2(c) allows QOF partnership and S corporation investors to exclude all gains and losses from asset sales after 10 years — including ordinary income depreciation recapture under Sections 1245 and 1250. This transforms cost segregation from a tax-deferral tool into a permanent tax elimination tool inside an OZ structure.

Qualifying Capital Gains and the 180-Day Window

Eligible gains include:

- Capital gains and qualified Section 1231 gains from asset sales, stock, real estate, and business interests

- Any portion of a qualifying gain — unlike a 1031 exchange, full reinvestment is not required

- Gains invested proportionally, with tax benefits applying only to the amount directed into the QOF

The IRS requires investment within a 180-day window beginning on the date the gain would be recognized for federal tax purposes. Per IRS FAQ #13, investors receive proportional benefits on whatever amount they invest.

The Two-Entity Structure

Understanding the structure matters for depreciation planning:

- Qualified Opportunity Fund (QOF): The investment vehicle (partnership or corporation) that investors contribute to, which must hold at least 90% of its assets in qualified OZ property

- Qualified Opportunity Zone Business (QOZB): The operating entity that holds the actual real estate and must satisfy a 70% tangible property standard

This two-tier structure allows the QOZB to hold and depreciate real estate while the QOF maintains compliance with the 90% investment standard.

How Cost Segregation Amplifies Opportunity Zone Returns

Cost segregation is an engineering-based analysis that reclassifies building components from 27.5-year (residential) or 39-year (commercial) straight-line depreciation into 5-, 7-, or 15-year MACRS categories. That reclassification unlocks front-loaded deductions — and inside an Opportunity Zone, those deductions carry far more power than they do on a standard investment.

The Power of 100% Bonus Depreciation

Under IRC Section 168(k), property with a MACRS recovery period of 20 years or less qualifies for bonus depreciation. The One Big Beautiful Bill Act (Public Law 119-21), enacted July 4, 2025, permanently restored 100% bonus depreciation for qualifying property acquired and placed in service after January 19, 2025.

That means components identified through a cost segregation study can be fully deducted in the year placed in service — not spread over decades.

The Triple Tax Benefit Structure

When cost segregation and OZ investments are combined, three distinct tax advantages stack on top of each other:

- Deferred original gain — Your initial capital gain recognition is pushed to the statutory deadline or inclusion event via the QOF structure

- Immediate depreciation deductions — Cost segregation losses offset income from other sources in the current tax year

- Permanent tax elimination at exit — After 10 years, both appreciation and depreciation recapture are excluded from tax entirely

Conceptual Example:

A $5 million OZ property (excluding land) undergoes a cost segregation study. Based on analysis of over 8,000 engineering-based studies, the median total accelerated allocation is 24% of depreciable basis.

- Reclassified to shorter life: $1,200,000 (24% of $5M)

- First-year bonus depreciation: $1,200,000 (100% of eligible property)

- Tax savings at 37% marginal rate: $444,000 in Year 1

At normal depreciation recapture rates of 25%, the investor would owe $300,000 in recapture taxes upon sale. Under OZ rules, selling after 10 years wipes out that $300,000 recapture liability entirely. Not deferred. Gone.

When to Complete Your Study

Cost segregation benefits apply to both new construction and substantial improvement projects within OZ. Complete your study after improvements are substantially finished, but before filing that year's return. That's the window for maximum first-year deductions.

Missed the window? Investors who already own OZ property can use Form 3115 (Application for Change in Accounting Method) to claim catch-up depreciation via a Section 481(a) adjustment in a single tax year without amending prior returns. Seneca Cost Segregation assesses lookback eligibility and completes studies within 2–4 weeks.

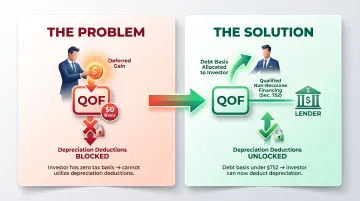

Navigating the Zero-Basis Problem

The Core Challenge

When an investor places deferred capital gains into a QOF, their initial tax basis is zero under Section 1400Z-2(b)(2)(B)(i). Without basis, the investor cannot deduct depreciation losses against other income—the losses simply sit unused.

The Solution: Qualified Non-Recourse Financing

Under Section 752, debt allocable to partners in a partnership increases their tax basis. Treasury Decision 9889 explicitly confirms that the initial zero basis in a QOF partnership is "adjusted to take into account the contributing partner's share of partnership debt under section 752."

If the QOF borrows $8 million against a project, investors receive allocable basis from that debt, which allows them to use the depreciation deductions generated by cost segregation.

The Reality: Most OZ Deals Already Solve This

Most OZ real estate development projects carry significant construction or permanent financing by nature, meaning the zero-basis problem is already solved in most real-world deals. Passive investors relying solely on deferred gains with no debt in the structure cannot use cost segregation deductions. This is a key qualifying factor to verify before planning.

State Tax Nuance

OZ rules are federal-only. If a property is purchased with no debt, there is no federal basis, but the full purchase price typically provides state tax basis. This means a cost segregation study may still deliver value for state tax purposes even when the federal benefit is constrained.

That state-level value depends on conformity, which varies widely. Two contrasting examples:

| State | OZ Conformity |

|---|---|

| California | Does not conform to federal OZ deferral or exclusion rules |

| New Jersey | Fully conforms to federal OZ rules |

What OZ 2.0 Changes for Depreciation Investors

Key OBBBA (July 2025) Changes

The One Big Beautiful Bill Act transformed the OZ landscape across three fronts:

| Change | What It Means |

|---|---|

| Program Permanency | OZ is now permanent, with 10-year review cycles for census tracts starting July 1, 2026. New designations take effect January 1, 2027, with tighter eligibility criteria (median family income below 70% of area median or poverty rate ≥ 20%). |

| Rolling 5-Year Deferral | The fixed December 31, 2026 deadline is replaced by a rolling 5-year deferral for QOF investments made after January 1, 2027 — eliminating the artificial urgency that defined OZ 1.0. |

| 100% Bonus Depreciation Restored | The Act permanently restored 100% bonus depreciation for qualifying property acquired and placed in service after January 19, 2025, making cost segregation inside OZ eligible for full first-year deductions on qualifying assets. |

The Rural Opportunity Zone Bonus

The OBBBA created Qualified Rural Opportunity Funds (QROFs) for tracts in communities under 50,000 population. QROFs offer:

- 30% basis step-up at 5 years (vs. 10% for standard QOFs)

- Reduced substantial improvement threshold of 50% instead of 100%

These enhancements make the cost segregation + OZ combination even more favorable in rural markets.

The Critical 2026–2027 Transition Point

Those QROF advantages also sharpen the timing question for anyone with gains in late 2026. Investors should carefully weigh whether to commit under OZ 1.0 rules — with a deferral window closing December 31, 2026 — or wait until January 2027 to access the superior OZ 2.0 framework. The 180-day reinvestment window usually provides enough flexibility to make that call deliberately. Work with a qualified tax advisor to model both scenarios before deciding.

Step-by-Step: Implementing the OZ + Cost Seg Strategy

The Implementation Sequence

1. Trigger a qualifying capital gain event

Sell an asset (stock, real estate, business interest) and recognize a capital gain or qualified Section 1231 gain for federal tax purposes.

2. Invest within 180 days into a QOF

Direct all or a portion of your capital gain into a properly structured Qualified Opportunity Fund within the 180-day window. Remember: you only need to invest the gain amount, not the entire proceeds.

3. QOF acquires or develops OZ property

The QOF acquires or develops OZ property through a QOZB, securing adequate debt to establish investor basis. Most real estate projects naturally carry construction or permanent financing.

4. Commission a cost segregation study

Once improvements are substantially complete, engage an engineering-based cost segregation provider like Seneca Cost Segregation to complete the study. Seneca typically delivers studies within 2–4 weeks.

5. Claim bonus depreciation deductions in Year 1

Use the cost segregation results to claim 100% bonus depreciation on all property with MACRS recovery periods of 20 years or less.

6. Hold for the full 10-year period

Maintain your QOF investment for at least 10 years to qualify for the full benefit package: appreciation exclusion and recapture elimination.

7. Exit tax-free

After 10 years, elect the basis step-up to fair market value under Section 1400Z-2(c), eliminating both appreciation taxes and depreciation recapture.

Key Compliance Requirements

Investors and their advisors must track:

- Form 8996 - Annual QOF self-certification and 90% investment standard compliance

- Form 8997 - Individual investor reporting of OZ investment status

- Substantial improvement documentation - Purchase agreements, improvement contracts, architectural specs, construction invoices

- Depreciation allocation provisions - Operating agreement language allocating depreciation among partners

The OBBBA added enhanced reporting obligations with significant daily penalties for non-compliance under new IRC Sections 6039K, 6039L, and 6726. The penalty for failure to comply is $500 per day.

The 10-Year Commitment

Meeting those compliance requirements is only part of the commitment — the strategy also demands a long investment horizon. Investors who exit early forfeit the appreciation exclusion and recapture elimination — retaining only the accelerated depreciation already claimed (subject to normal recapture rules).

The bottom line: tax benefits amplify a good investment; they don't rescue a bad one. Before committing capital, verify the underlying project on its fundamentals — cash flow projections, local market demand, and sponsor track record — independent of any OZ designation.

Frequently Asked Questions

Can I do cost segregation on an Opportunity Zone property?

Yes, cost segregation is available for OZ properties, but investors must have sufficient tax basis (typically from debt in the project structure) to use the resulting depreciation deductions. Without basis, the losses cannot be claimed currently.

What happens to depreciation recapture in an Opportunity Zone after 10 years?

Under Section 1400Z-2(c), investors who hold their QOF interest for at least 10 years can elect a stepped-up basis to fair market value at sale. This permanently eliminates both appreciation taxes and depreciation recapture, making cost segregation a permanent tax benefit rather than a timing strategy.

Do I need debt in my QOF investment to benefit from cost segregation?

Yes, most investors need allocated debt under Section 752 to establish tax basis in the QOF and use depreciation losses. Most real estate OZ projects carry construction or permanent financing, which typically solves this automatically.

When is the best time to order a cost segregation study for an OZ property?

Studies should be completed after improvements are substantially finished but before filing that year's tax return. Investors who missed the window can use Form 3115 to claim catch-up depreciation in a single year without amending prior returns.

Can I invest only part of my capital gain in a Qualified Opportunity Fund?

Yes, unlike a 1031 exchange, OZ investments do not require reinvesting the entire gain. Investors can direct any portion of a qualifying gain into a QOF and receive proportional tax benefits on the invested amount.

What changed for OZ investors under the One Big Beautiful Bill Act?

The OBBBA (July 2025) made the OZ program permanent, replaced the fixed 2026 deferral deadline with a rolling 5-year deferral for post-2026 investments, and restored 100% bonus depreciation permanently. It also created enhanced benefits for rural Opportunity Funds, including a 30% basis step-up.

Ready to explore how cost segregation can amplify your Opportunity Zone returns? Seneca Cost Segregation has completed over 10,200 property assessments with an average first-year deduction of $171,243. Our engineering-based studies follow IRS guidelines and come with full audit defense. Contact us at info@senecacostseg.com or call +1 530-797-6539 for a complimentary preliminary analysis of your OZ property.