Section 1250 is the IRS mechanism for "recapturing" depreciation deductions you've claimed over the years. While these deductions reduced your tax bill during ownership, the IRS wants a portion back when you sell at a gain. Understanding Section 1250 is critical for any property owner, because the tax treatment of your sale depends on how your property was depreciated, which components were reclassified through strategies like cost segregation, and whether you've structured your exit to defer or minimize recapture.

This guide breaks down what qualifies as Section 1250 property, how depreciation and recapture work, the key differences between Section 1250 and Section 1245 property, and how proactive tax strategies can affect your bottom line at sale.

TLDR: Key Takeaways

- Section 1250 covers depreciable real property, including commercial buildings, rental homes, and structural components like roofs and HVAC systems

- Depreciation recapture on 1250 property is taxed as "unrecaptured Section 1250 gain" at a maximum 25% federal rate, not the standard 0–20% long-term capital gains rates

- Section 1245 property (equipment, personal property) triggers harsher recapture: 100% of depreciation taxed as ordinary income at rates up to 37%

- Cost segregation reclassifies components from 1250 to 1245, accelerating deductions upfront but shifting your recapture profile at sale

- 1031 exchanges defer Section 1250 recapture but don't erase it: the tax liability carries over to your replacement property

What Is Section 1250 Property?

Section 1250 property is defined by IRC §1250(c) as any real property (other than Section 1245 property) that is or has been subject to the depreciation allowance under Section 167. In plain language, this covers buildings and their structural components, the physical structures you depreciate over time.

What qualifies as Section 1250 property:

- Commercial buildings (office buildings, retail centers, warehouses)

- Residential rental properties (apartment complexes, single-family rentals)

- Hotels and hospitality properties

- Industrial facilities

- Structural components: roofs, load-bearing walls, plumbing systems, central HVAC when treated as part of the building structure

These properties are depreciated using the Modified Accelerated Cost Recovery System (MACRS) with straight-line depreciation: 27.5 years for residential rental property and 39 years for nonresidential real property.

What Section 1250 does NOT include:

- Land – Land is not depreciable because it doesn't have a finite useful life

- Section 1245 personal property – Equipment, machinery, carpeting, and removable fixtures

- Inventory property – Real estate held primarily for sale to customers

The Section 1231 Framework

Understanding what Section 1250 excludes clarifies where it fits within the broader tax code. Section 1250 property sits inside the Section 1231 framework, which covers all depreciable business property held more than one year.

Section 1250 provides the specific recapture rules for the real property subset of Section 1231 assets. When you sell Section 1250 property at a gain, the portion attributable to depreciation is subject to special recapture rules. Any remaining gain above your original cost basis receives favorable long-term capital gains treatment.

Historical Context: Why Section 1250 Exists

Section 1250 originally targeted accelerated depreciation methods that were common before the Tax Reform Act of 1986. Prior to 1986, property owners could use accelerated methods that front-loaded deductions far beyond what straight-line depreciation would produce. After 1986, the IRS mandated straight-line depreciation for real property, making traditional full-recapture scenarios rare.

However, the "unrecaptured Section 1250 gain" rule didn't disappear with the 1986 reform. All accumulated straight-line depreciation is still taxed at up to 25% upon sale, a meaningful tax hit that investors need to plan around before listing a property.

Common Examples of Section 1250 Property

Real estate investors encounter Section 1250 property daily. Here are the most common examples:

Commercial and Investment Properties:

- Office buildings and professional centers

- Retail strip malls and shopping centers

- Apartment complexes and multi-family buildings

- Single-family rental homes

- Self-storage facilities

- Warehouses and distribution centers

- Hotels and resorts

- Industrial manufacturing facilities

Structural Components:

- Roofs and exterior walls

- Load-bearing walls and structural framing

- Foundation and structural concrete

- Central plumbing systems

- Flooring permanently affixed to the structure

- Central HVAC systems serving general building functions

Borderline Examples: Classification Matters

Some building components create classification confusion, and the distinction has significant tax consequences:

HVAC systems can fall under either Section 1250 (structural component) or Section 1245 (equipment), depending on installation and function. A central air conditioning system serving the entire building's general climate control remains Section 1250 property.

A dedicated unit serving specific equipment — such as server room cooling or manufacturing process temperature control — may qualify as Section 1245 property, because it serves equipment rather than the building itself.

This is exactly the type of classification that engineering-based cost segregation studies are designed to analyze. Licensed engineers apply the Whiteco permanency test to determine whether components can be moved, are designed to remain permanently, would cause damage if removed, and how they're affixed to the building.

What Is Always Excluded:

- Land – Cannot be Section 1250 property because land is not depreciable

- Personal property items – Machinery, office equipment, carpeting, removable fixtures fall under Section 1245

- Intangible assets – Fall outside both Section 1250 and Section 1245

How Section 1250 Depreciation Works

Section 1250 property is depreciated using the straight-line method under MACRS. IRS Publication 946 establishes the recovery periods:

| Property Type | Recovery Period |

|---|---|

| Residential rental property | 27.5 years |

| Nonresidential real property | 39 years |

Straight-line depreciation means equal deductions each year across the property's recovery period. If you purchase a $1,000,000 commercial building (excluding land), you deduct approximately $25,641 per year ($1,000,000 ÷ 39 years) over the building's recovery period.

"Additional Depreciation" vs. Straight-Line

"Additional depreciation" under Section 1250 technically refers to the amount by which accelerated depreciation exceeds what straight-line depreciation would have produced. Because straight-line is now mandated for post-1986 real property, additional depreciation in the traditional sense is rare. That said, this concept matters when reviewing historical property records and pre-1986 assets.

Unrecaptured Section 1250 Gain: The Modern Reality

For properties depreciated using straight-line methods (the vast majority of real estate today), the more relevant concept is unrecaptured Section 1250 gain. Even when only straight-line depreciation has been used, the portion of gain attributable to accumulated depreciation deductions is subject to a maximum federal capital gains rate of 25%, rather than the standard long-term capital gains rates of 0%, 15%, or 20%.

Simplified Example: How It Works

Say you buy a rental property for $500,000 ($400,000 building, $100,000 land). Over 10 years, you claim $145,455 in straight-line depreciation ($400,000 ÷ 27.5 years × 10 years), dropping your adjusted basis to $354,545. You then sell the property for $600,000.

The gain breaks into three layers:

| Gain Component | Amount | Tax Treatment |

|---|---|---|

| Total gain | $245,455 ($600,000 sale price − $354,545 adjusted basis) | — |

| Unrecaptured Section 1250 gain | $145,455 (the depreciation claimed) | Taxed at 25% |

| Remaining gain | $100,000 ($600,000 − $500,000 original price) | Taxed at standard long-term capital gains rates |

The unrecaptured Section 1250 gain worksheet is available in the IRS Schedule D instructions.

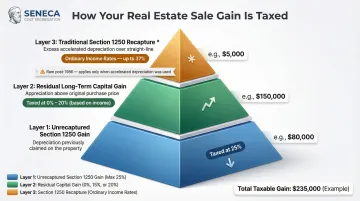

Section 1250 Depreciation Recapture: Tax Treatment When You Sell

When you sell Section 1250 property at a gain, the IRS applies a three-layer tax treatment structure:

| Layer | Description | Tax Rate |

|---|---|---|

| Layer 1: Traditional Section 1250 Recapture | Applies when accelerated depreciation exceeds straight-line amounts (rare post-1986) | Ordinary income rates up to 37% |

| Layer 2: Unrecaptured Section 1250 Gain | All depreciation claimed under straight-line methods | Maximum 25% federal rate |

| Layer 3: Residual Long-Term Capital Gain | Remaining gain above original purchase price (pure appreciation) | 0%, 15%, or 20% |

Layer 1: Traditional Section 1250 Recapture (Rare Post-1986)

This layer only triggers when accelerated depreciation exceeds straight-line amounts — taxed at ordinary income rates up to 37%. Because straight-line depreciation is mandated for post-1986 real property, it rarely applies to modern transactions. If your property was acquired after 1986, you can likely skip this layer.

Layer 2: Unrecaptured Section 1250 Gain

This is the layer that catches most investors off guard, and the one that actually matters for post-1986 real estate.

All depreciation claimed under straight-line methods gets recaptured here at a maximum 25% federal rate. That's higher than the 0%, 15%, or 20% rates that apply to long-term capital gains, even though straight-line is the slowest depreciation method available. Every Section 1250 property sale where depreciation was claimed is subject to this layer.

Layer 3: Residual Long-Term Capital Gain

Any remaining gain above your original purchase price — pure appreciation — is taxed at long-term capital gains rates:

| Rate | Threshold |

|---|---|

| 0% | For income below the threshold |

| 15% | For taxable income over $47,025 (Single) or $94,050 (Married Filing Jointly) |

| 20% | For income over $518,900 (Single) or $583,750 (Married Filing Jointly) |

2024 thresholds per IRS Topic 409. This layer only applies when your sale price exceeds your original purchase price.

Important Limitation: Gain Recognized Caps Recapture

The recapture amount can never exceed your actual gain. If you sell below your original purchase price but above your depreciated adjusted basis, only the real gain is subject to recapture — not the full depreciation claimed. This cap provides meaningful protection in partial-loss sale scenarios.

Exceptions: When Section 1250 Recapture Does NOT Apply

Several important exceptions eliminate or defer Section 1250 recapture:

| Exception | Effect on Recapture | Key Details |

|---|---|---|

| Gifts | No recapture triggered | Recipient receives a carryover basis, inheriting the depreciation history and potential recapture liability |

| Transfers at Death | Recapture eliminated | Stepped-up basis to fair market value at the date of death eliminates accumulated depreciation and recapture exposure entirely |

| Like-Kind Exchanges (Section 1031) | Recapture deferred, not eliminated | Accumulated depreciation and recapture potential carry over to the replacement property |

| Tax-Free Corporate and Partnership Reorganizations | Recapture limited | Under IRC §§ 332, 351, 361, 721, and 731 where basis carries over to the transferee entity |

Gifts

Property transferred as a gift triggers no recapture. The recipient receives a carryover basis, meaning they inherit the depreciation history and potential recapture liability.

Transfers at Death

Property transferred at death receives a stepped-up basis to fair market value at the date of death. This step-up eliminates accumulated depreciation and the associated recapture exposure entirely, making it a significant advantage for estate planning.

Like-Kind Exchanges Under Section 1031

A properly structured 1031 exchange defers Section 1250 recapture, but it does not eliminate it. The accumulated depreciation and recapture potential carry over to the replacement property. When you eventually sell in a taxable transaction, all deferred recapture becomes due.

Investors frequently use these rules in combination:

- Sequential 1031 exchanges defer recapture across multiple property cycles

- Holding until death results in a stepped-up basis that eliminates recapture permanently

- Receiving boot (cash or non-like-kind property) triggers recapture to the extent of the boot received

Tax-Free Corporate and Partnership Reorganizations

Certain tax-free transfers under IRC §§ 332, 351, 361, 721, and 731 limit recapture where basis carries over to the transferee entity. Each of these exceptions requires careful structuring, as missteps can inadvertently trigger the recapture they were meant to avoid.

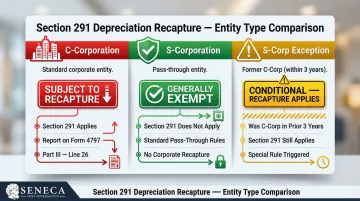

Corporate Investor Nuance: Section 291 Adds Extra Recapture

C-corporations face an additional recapture rule under Section 291. Under this provision, 20% of the gain that would have been ordinary income under Section 1245 rules is treated as ordinary income. This applies on top of any Section 1250 recapture already owed.

Here's how the rule applies by entity type:

| Entity Type | Section 291 Applies? | Notes |

|---|---|---|

| C-corporations | Yes | Subject to Section 291 recapture; report additional ordinary income on Form 4797, Part III, Line 26 |

| S-corporations | Generally No | Generally exempt from Section 291 recapture |

| S-corp exception | Yes (if applicable) | If the S-corporation (or a predecessor) was a C-corporation in any of the three immediately preceding tax years, Section 291 still applies |

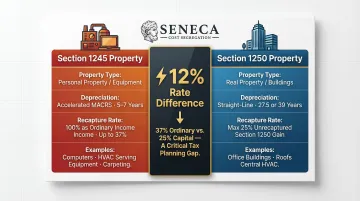

Section 1250 vs. Section 1245: Key Differences

The distinction between Section 1250 and Section 1245 property directly affects your tax bill at sale — and it shapes every classification decision in a cost segregation study.

| Attribute | Section 1250 Property | Section 1245 Property |

|---|---|---|

| Property Type | Real property: buildings and structural components | Tangible personal property: equipment, machinery, removable fixtures |

| Depreciation Method | Straight-line over 27.5 or 39 years | Accelerated MACRS over 5 or 7 years |

| Recapture on Sale | Straight-line depreciation taxed at max 25%; only excess accelerated depreciation (rare) taxed as ordinary income | 100% of all depreciation recaptured as ordinary income at rates up to 37% |

| Examples | Office buildings, apartment complexes, warehouses, structural HVAC, roofs, plumbing | Computers, office furniture, specialized equipment, carpeting, removable fixtures, dedicated machinery |

Concrete Comparison: Why Classification Matters

Scenario: Equipment Classified as Section 1245: Full Recapture at Ordinary Rates

You purchase a $50,000 HVAC unit classified as Section 1245 property serving dedicated equipment. Fully depreciated over 7 years, then sold. 100% of the gain up to depreciation taken is taxed as ordinary income at rates up to 37%.

Scenario: Building Classified as Section 1250: Capped at 25%

You own a commercial building with $500,000 in accumulated straight-line depreciation. Upon sale, that $500,000 is taxed at the 25% unrecaptured Section 1250 gain rate, not ordinary income rates.

That's a 12-percentage-point difference in recapture tax (37% vs. 25%), which is why how each component gets classified in a cost segregation study has real dollar consequences at disposition.

Section 1245 recapture is more aggressive: every dollar of depreciation comes back as ordinary income. Yet for most investors, the upfront cash flow from accelerated depreciation still wins — provided the holding period is long enough to benefit from the time value of those earlier deductions.

How Cost Segregation Interacts with Section 1250 Property

Cost segregation is an engineering-based tax strategy that identifies and reclassifies building components typically lumped into Section 1250 property (39-year or 27.5-year depreciation) and moves qualifying components into Section 1245 categories (5-year or 7-year property) or 15-year land improvements.

What Gets Reclassified

| Asset | Classification | Recovery Period |

|---|---|---|

| Carpet and vinyl flooring (when not cemented) | Section 1245 | 5-year or 7-year |

| Decorative lighting and specialty fixtures | Section 1245 | 5-year or 7-year |

| Window treatments and blinds | Section 1245 | 5-year or 7-year |

| Removable cabinetry and appliances | Section 1245 | 5-year or 7-year |

| Equipment-serving electrical outlets and dedicated wiring | Section 1245 | 5-year or 7-year |

| Specialized security systems | Section 1245 | 5-year or 7-year |

| False balconies and ornamental features | Section 1245 | 5-year or 7-year |

| Asphalt parking lots | 15-Year land improvements | 15-year |

| Concrete sidewalks and walkways | 15-Year land improvements | 15-year |

| Landscaping and irrigation systems | 15-Year land improvements | 15-year |

| Site lighting and exterior signage | 15-Year land improvements | 15-year |

| Fencing and gates | 15-Year land improvements | 15-year |

| Retention ponds and drainage systems | 15-Year land improvements | 15-year |

The Trade-Off: Faster Deductions vs. Higher Recapture

Assets reclassified to Section 1245 via cost segregation receive faster depreciation, meaning larger deductions in the early years of ownership. However, these assets are subject to 100% recapture as ordinary income upon sale (at rates up to 37%) rather than the 25% unrecaptured Section 1250 gain rate.

Why the trade-off typically favors cost segregation:

Front-loading deductions and reinvesting those tax savings produces a time-value advantage that outweighs the higher recapture rate at exit. According to the Journal of Accountancy, the immediate cash flow from accelerated deductions (especially with bonus depreciation) yields a net present value that typically exceeds the future ordinary income tax cost.

Many investors push the math even further by pairing cost segregation with 1031 exchanges, deferring recapture indefinitely, or holding until death to receive a stepped-up basis that eliminates recapture entirely.

Engineering-Based Studies Are Required

A professional, engineering-based cost segregation study is required to properly substantiate property reclassification under IRS standards. The IRS Cost Segregation Audit Techniques Guide outlines 13 elements of quality studies, including detailed engineering analysis, proper documentation, and legal citations supporting the Section 1245 classifications.

Studies conducted by licensed engineers provide the detailed analysis and audit defense necessary to withstand IRS scrutiny. Seneca Cost Segregation's engineering team has completed over 10,200 studies nationwide, applying the Whiteco permanency test and functional allocation analysis to determine which building components qualify for accelerated treatment.

Frequently Asked Questions

What is Section 1250 real estate?

Section 1250 real estate covers any depreciable real property, including commercial buildings, residential rentals, and their structural components. The classification determines how sale gains are taxed: accumulated depreciation is treated as either ordinary income or the special 25% unrecaptured gain rate.

What are examples of 1250 property?

Common examples include apartment buildings, commercial office buildings, retail spaces, warehouses, self-storage facilities, single-family rental homes, and structural components such as roofs, load-bearing walls, and central plumbing systems. Land itself is excluded because it is not depreciable.

What is the difference between 1245 and 1250 property?

Section 1245 covers personal property (equipment, machinery) and recaptures 100% of depreciation as ordinary income at rates up to 37%. Section 1250 covers real property (buildings and structural components), taxing straight-line depreciation at a maximum 25% capital gains rate. Only excess accelerated depreciation (rare post-1986) is taxed as ordinary income.

Is equipment like HVAC 1245 or 1250 property?

It depends on classification. HVAC serving the building generally qualifies as Section 1250; removable units serving a specialized function typically fall under Section 1245. A cost segregation study by licensed engineers is the most reliable way to make this determination.

Can land be 1250 property?

No, land cannot be Section 1250 property because land is not depreciable. The depreciation allowance under Section 167 applies only to assets with a finite useful life. The cost of land must be separated from the cost of the building and improvements when calculating depreciation.

Can you have 1250 gain without 1231 gain?

Yes. If a property sells below its original purchase price but above its depreciated basis, ordinary income recapture can still apply, even while the overall Section 1231 position shows a loss. A tax professional can provide property-specific analysis.

Want to put Section 1250 rules to work for your portfolio? Seneca Cost Segregation delivers engineering-based studies backed by a 100% money-back AuditDefense guarantee. With over 10,200 completed studies and an average first-year deduction of $171,243, our licensed engineers help real estate investors capture every available depreciation benefit in full IRS compliance. Seneca Cost Segregation can be reached at 503-383-1158 or info@senecacostseg.com for a complimentary tax assessment.