Introduction

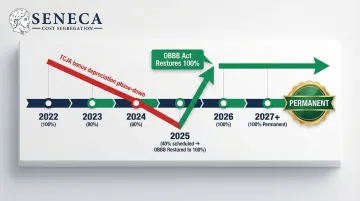

On July 4, 2025, the One Big Beautiful Bill Act (OBBB) permanently changed the tax planning landscape for real estate investors. The law restored 100% bonus depreciation for property placed in service on or after January 19, 2025. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

For real estate investors in 2026, that means the ability to deduct 100% of qualifying asset costs in year one instead of spreading them over 5 to 39 years. The catch: the building structure itself doesn't qualify.

The real savings come from identifying the components within your property that do qualify (appliances, fixtures, land improvements, and interior upgrades) and accelerating their depreciation to year one.

This article covers every key requirement for 100% bonus depreciation in 2026: which assets qualify, which don't, and how cost segregation maximizes the benefit.

TLDR: Key Rules for 100% Bonus Depreciation in 2026

- 100% bonus depreciation is permanent under the OBBB Act for property placed in service after January 19, 2025, where the acquisition date is also on or after January 19, 2025

- The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively

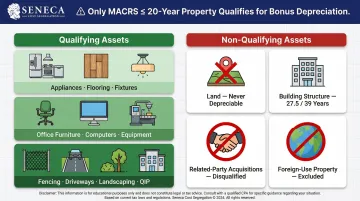

- Only property with a MACRS recovery period of 20 years or less qualifies

- Both new and used property qualify if new to the taxpayer

- Cost segregation unlocks bonus depreciation on 20-40% of a building's cost that would otherwise be missed

- State conformity varies. California and New York don't conform, so no state-level deduction applies there

What Is 100% Bonus Depreciation and What Changed in 2026?

Bonus depreciation is an accelerated tax deduction that lets property owners immediately write off 100% of a qualified asset's cost in the year it's placed in service. Instead of spreading deductions across 27.5 years (residential) or 39 years (commercial), you claim the full amount upfront for qualifying components.

The Legislative Timeline

The 2017 Tax Cuts and Jobs Act (TCJA) introduced 100% bonus depreciation, but included a scheduled phase-down:

| Date Range | Bonus Depreciation % | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | TCJA original rate |

| January 1, 2023 – December 31, 2023 | 80% | TCJA phase-down |

| January 1, 2024 – December 31, 2024 | 60% | TCJA phase-down |

| January 1, 2025 – January 18, 2025 | 40% | TCJA phase-down |

| January 19, 2025 – December 31, 2030 (acquisition on/after January 19, 2025) | 100% | OBBBA restored rate |

| 2025 (acquisition before January 19, 2025) | 40% | TCJA phase-down still applies |

| 2026 (acquisition before January 19, 2025) | 20% | TCJA phase-down still applies |

The OBBB Act, via Section 70301 of Public Law 119-21, permanently restored the 100% rate for property acquired and placed in service on or after January 19, 2025. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

What This Means for Investors

The permanent restoration removes the "will Congress extend it?" uncertainty that complicated tax planning under the TCJA. Investors now have a stable foundation to make long-range decisions with confidence:

- Acquisitions can be structured around immediate full deductions rather than a shrinking rate

- Cost segregation studies can be commissioned without timing pressure from phase-down deadlines

- Depreciation can be modeled into multi-year investment strategies with predictable tax outcomes

The Key Eligibility Rules for 100% Bonus Depreciation

Five rules determine whether a property or improvement qualifies. Each works as an independent checkpoint: miss one, and the deduction doesn't apply.

| Rule # | Requirement | Key Detail |

|---|---|---|

| 1 | MACRS recovery period of 20 years or less | Excludes 27.5-year residential and 39-year commercial structures |

| 2 | Placed in service after January 19, 2025 | Property must be ready and available for use |

| 3 | New to the taxpayer | Used property qualifies; related-party restrictions apply |

| 4 | Qualified Improvement Property (QIP) | Interior improvements to nonresidential commercial buildings (15-year property) |

| 5 | Business or income-producing use | Personal-use property does not qualify |

Rule 1: MACRS Recovery Period of 20 Years or Less

To qualify, property must be depreciated under the Modified Accelerated Cost Recovery System (MACRS) with a recovery period of 20 years or less, per IRC §168(k)(2)(A)(i)(I). The building structure itself never qualifies: 27.5 years for residential, 39 years for commercial. Only components with shorter recovery periods do.

Rule 2: Placed-in-Service Requirement

The asset must be acquired and placed into service after January 19, 2025 to qualify for 100% under the OBBB. The IRS defines "placed in service" as when property is "ready and available for a specific use whether in a trade or business, the production of income, a tax-exempt activity, or a personal activity."

For real estate, construction must be complete and the property usable. An asset purchased but not yet in use doesn't qualify for that tax year.

Rule 3: New to the Taxpayer (Used Property Eligibility)

Property doesn't have to be brand new—used property qualifies if it's new to the taxpayer (first time that specific taxpayer is using or depreciating the asset).

Three restrictions apply:

- Cannot be acquired from a related party

- Cannot have been previously used by the taxpayer or a predecessor

- Taxpayer's basis cannot be determined by the transferor's adjusted basis

Investors buying existing rental properties can still claim bonus depreciation on qualifying components, even if the building has changed hands before.

Rule 4: Qualified Improvement Property (QIP)

QIP is any improvement to the interior of a nonresidential commercial building made after the building was first placed in service. The CARES Act retroactively classified QIP as 15-year property, making it bonus-depreciation eligible.

| Qualifies as QIP | Does Not Qualify as QIP |

|---|---|

| Interior flooring upgrades | Building enlargements |

| HVAC systems | Elevators or escalators |

| Lighting | Internal structural framework |

| Plumbing modifications inside the building | Improvements to residential rental buildings |

Rule 5: Business or Income-Producing Use Requirement

To claim bonus depreciation, property must be used in a trade or business or held for the production of income. Personal-use property doesn't qualify.

For rental property investors, the asset must be part of an income-generating rental activity. Passive activity rules apply unless you qualify as a Real Estate Professional (REP) or meet the short-term rental exception, covered in the next section.

Which Real Estate Assets Qualify (and Which Don't) for 100% Bonus Depreciation

Qualifying Asset Categories

| Asset Class | MACRS Life | Examples |

|---|---|---|

| Personal property | 5 years | Appliances (refrigerators, stoves, dishwashers), carpeting and flooring, cabinets and countertops, fixtures and hardware, smart home technology, security systems, interior furnishings |

| Personal property | 7 years | Office furniture used in managing rental business, computers and technology (used in property management, distinct from smart home tech), desks and filing systems, maintenance and operational equipment |

| Land improvements | 15 years | Fences and gates, driveways and parking lots, sidewalks and walkways, landscaping and irrigation systems, outdoor lighting, site improvements |

| QIP | 15 years | Interior non-structural improvements to commercial buildings, new flooring in commercial spaces, updated HVAC systems, lighting upgrades, plumbing modifications |

These are the most common assets identified in cost segregation studies for residential rental properties.

Assets That Do Not Qualify

The building structure itself is the most common misconception. Residential buildings depreciate over 27.5 years and commercial buildings over 39 years, so both exceed the 20-year threshold required for bonus depreciation eligibility.

Other non-qualifying property:

| Non-Qualifying Asset |

|---|

| Land (never depreciable under any method) |

| Assets used in furnishing or selling utilities |

| Property acquired from related parties in non-arm's-length transactions |

| Property used predominantly outside the U.S. |

Without a cost segregation study, the vast majority of a property's value sits in non-qualifying categories by default. A proper engineering-based study typically reclassifies 20-40% or more of total property cost into 5-, 7-, or 15-year assets, making the study itself the mechanism that unlocks bonus depreciation at scale.

How Cost Segregation Unlocks the Full Power of 100% Bonus Depreciation

The Problem Cost Segregation Solves

When you purchase a property, the IRS default treats nearly the entire building value as a single asset depreciated over 27.5 or 39 years. Without a cost segregation study, you miss the opportunity to identify components with shorter MACRS lives that qualify for immediate 100% bonus depreciation.

What a Cost Segregation Study Does

An engineering-based analysis breaks a building's cost into individual components:

- Structural elements (stays at 27.5 or 39 years)

- Land improvements (15 years)

- Personal property components (5 or 7 years)

This reclassification creates the shorter-lived asset categories that become eligible for 100% bonus depreciation.

The Financial Impact

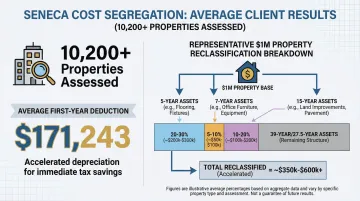

Consider a $1 million rental property. Through cost segregation, 25-40% of its value might be reclassified into 5, 7, and 15-year property. That reclassification can look like this for a $1M acquisition:

| Asset Class | Typical % of Property Value | Treatment |

|---|---|---|

| 5-year personal property (fixtures, equipment) | ~10-15% | Immediate deduction |

| 7-year personal property (specialized systems) | ~5-10% | Immediate deduction |

| 15-year land improvements (paving, landscaping) | ~10-15% | Immediate deduction |

| Structural elements | ~60-75% | 27.5-year or 39-year depreciation |

Across more than 10,200 properties assessed, Seneca Cost Segregation clients average a $171,243 first-year deduction, a figure that reflects what systematic reclassification actually produces in practice.

Look-Back Studies: Catching Up on Missed Depreciation

The financial impact above applies to new acquisitions, but owners of existing properties aren't locked out. A look-back cost segregation study lets you catch up on missed depreciation through a Form 3115 (Change in Accounting Method) filing, with no need to amend prior-year returns.

For property owners who have never run a study, this is a direct path to recovering deductions that have been sitting on the table for years.

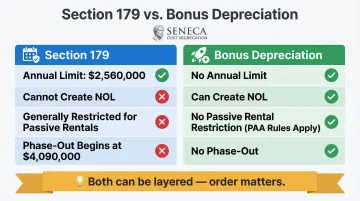

Bonus Depreciation vs. Section 179: What Real Estate Investors Need to Know

Both provisions allow accelerated deductions, but they differ in important ways:

| Feature | Section 179 | Bonus Depreciation |

|---|---|---|

| Annual Limit | $2,560,000 in 2026 | No limit |

| Can Create NOL? | No (limited to taxable income) | Yes |

| Rental Property | Generally cannot use for passive rentals | No restriction (though PAA rules apply) |

| Phase-Out | Begins at $4,090,000 in 2026 | None |

Strategic Interplay

Many real estate investors use Section 179 first for certain qualifying improvements, then layer bonus depreciation on top for remaining eligible costs, particularly when combined with cost segregation results. The two can be used together, but order matters.

That sequencing decision also depends on the type of property involved. Section 179 generally cannot be used for rental property that qualifies as a passive activity under IRS rules. Bonus depreciation doesn't carry that restriction. Even so, passive activity loss rules still limit when the deduction can offset income, so the two provisions aren't fully interchangeable for rental investors.

Important Considerations Before You Claim 100% Bonus Depreciation

Before claiming 100% bonus depreciation, there are three planning layers that can catch investors off guard: recapture liability, state tax divergence, and passive activity rules. Understanding each one upfront saves costly surprises later.

Depreciation Recapture Risk

When you sell property after claiming bonus depreciation, the IRS requires depreciation recapture. Accelerated deductions on personal property are recaptured as ordinary income under IRC §1245, potentially at rates higher than long-term capital gains rates.

The recapture impact warrants consideration before claiming large upfront deductions, especially when a sale is anticipated within a few years.

State Tax Conformity: Know Your State's Rules

While 100% bonus depreciation is permanent at the federal level, states aren't required to conform.

| State | Conformity Status | Treatment |

|---|---|---|

| California | Does not conform | Does not conform to federal bonus depreciation; add-back required |

| New York | Does not conform | Does not allow the federal special depreciation deduction; adjustments via Form IT-398 |

| Florida (Corporate) | Does not conform | Addition required for bonus depreciation; subtracted back over 7 years |

| Colorado | Conforms | Rolling conformity to IRC; follows federal treatment |

Real estate investors operating in non-conforming states face state tax treatment that differs from federal treatment.

The STR Loophole for Bonus Depreciation

Short-term rental (STR) owners with an average guest stay of 7 days or less are NOT subject to passive activity rules that typically limit rental loss deductions.

That means they can use bonus depreciation losses from a cost segregation study to directly offset active W-2 income, without needing Real Estate Professional (REP) status.

Requirements:

- Average guest stay of 7 days or less

- Material participation (typically 500+ hours or meeting another IRS test)

Under Temporary Treasury Regulation §1.469-1T(e)(3)(ii)(A), this activity isn't considered a "rental activity" at all, so it escapes automatic passive classification. For a high-earning STR owner in the 37% bracket, that distinction can translate to tens of thousands in tax savings in year one alone.

Frequently Asked Questions

Will there be 100% bonus depreciation in 2026?

Yes, 100% bonus depreciation is available in 2026. The One Big Beautiful Bill Act, signed July 4, 2025, permanently restored the 100% rate for qualifying property placed in service on or after January 19, 2025, where the acquisition date is also on or after January 19, 2025. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

What assets are eligible for 100% bonus depreciation?

Eligible assets must have a MACRS recovery period of 20 years or less, including appliances, office equipment, land improvements, and Qualified Improvement Property (QIP). The building structure itself doesn't qualify.

Can you take bonus depreciation on a rental home?

You cannot take bonus depreciation on the rental home structure itself (27.5-year life), but you can claim it on qualifying components identified within the property—such as appliances, carpeting, and land improvements. A cost segregation study is the best way to identify these eligible components.

Is a 39-year property eligible for bonus depreciation?

No. Commercial buildings (39-year property) exceed the 20-year MACRS threshold and don't qualify. That said, components within the building, such as QIP, equipment, and land improvements, can qualify when properly reclassified through a cost segregation study.

Is bonus depreciation always 60%?

No. Bonus depreciation was 60% in 2024 under the TCJA phase-out schedule. It had been scheduled to drop to 40% in 2025, but the OBBB Act restored it to 100% effective January 19, 2025 for property acquired on or after that date. The TCJA phase-down is still in effect for property acquired before January 19, 2025. In 2026, bonus depreciation remains 100% for qualifying property with an acquisition date of January 19, 2025 or later.

What is the STR loophole for bonus depreciation?

The STR loophole applies to short-term rental owners (average guest stay of 7 days or less) who materially participate in their rental activity. It allows them to deduct bonus depreciation losses against ordinary or W-2 income, bypassing the passive activity rules that normally block rental losses from offsetting non-passive income.