Introduction

Real estate investors face a sobering reality at the point of sale. A property purchased for $400,000 and sold for $700,000 might appear to generate a $300,000 profit, but after capital gains tax, depreciation recapture, and the Net Investment Income Tax, the IRS can claim $80,000 to $100,000 or more of that gain. Suddenly, years of property management produce a far smaller return than the numbers suggested.

The tax code provides legitimate, IRS-approved deductions and strategies that can substantially reduce taxable gain — but only for investors who know what to look for and have kept the right records. This guide covers every major deduction category, explains how depreciation recapture works, and outlines strategies to minimize your tax hit when selling investment property.

TLDR

- Selling costs (commissions, legal fees, closing costs) are deductible and directly reduce your taxable gain

- Capital improvements increase your adjusted basis, reducing the profit subject to tax

- Suspended passive activity losses from prior years can be released at sale to offset gain

- Depreciation recapture is taxed at up to 25%, separate from your capital gains rate

- A 1031 exchange lets you defer all capital gains tax by reinvesting proceeds into a like-kind property

How Capital Gains Tax Works When You Sell Investment Property

When you sell an investment property for more than your adjusted cost basis, the IRS classifies the profit as a capital gain and taxes it accordingly. Unlike primary residences (which qualify for the Section 121 exclusion of up to $250,000 for single filers or $500,000 for married couples), investment properties face full taxation on the gain.

Short-term vs. long-term capital gains:

- Short-term gains (property held one year or less): Taxed as ordinary income at rates up to 37%

- Long-term gains (held more than one year): Taxed at preferential rates of 0%, 15%, or 20% depending on your taxable income

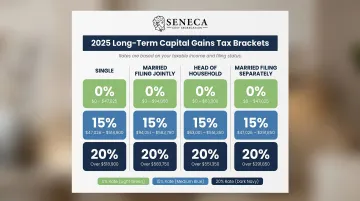

2025 Long-Term Capital Gains Tax Brackets

| Filing Status | 0% Rate | 15% Rate | 20% Rate |

|---|---|---|---|

| Single | Up to $48,350 | $48,351–$533,400 | Over $533,400 |

| Married Filing Jointly | Up to $96,700 | $96,701–$600,050 | Over $600,050 |

| Head of Household | Up to $64,750 | $64,751–$566,700 | Over $566,700 |

| Married Filing Separately | Up to $48,350 | $48,351–$300,000 | Over $300,000 |

Your taxable gain depends on your adjusted cost basis — the most critical number in your sale calculation. Adjusted basis starts with your original purchase price, increases with capital improvements made during ownership, and decreases by depreciation deductions taken each year. Getting this number wrong is one of the most common and costly errors investors make. Getting this number wrong is one of the most common and costly errors investors make. Capital gains rates, though, are only part of the tax picture — high-income investors also face a surtax on top of standard federal rates.

Net Investment Income Tax (NIIT)

High-income investors face an additional 3.8% surtax on net investment income — including real estate capital gains — when their modified adjusted gross income exceeds:

- $250,000 for married filing jointly

- $200,000 for single or head of household filers

- $125,000 for married filing separately

These thresholds are not indexed for inflation, meaning more investors cross into NIIT territory each year. State capital gains taxes may also apply on top of federal taxes, varying significantly by location. Before you list, calculate your combined federal, NIIT, and state exposure — the gap between your estimated gain and your actual after-tax proceeds can be substantial.

What You Can Deduct From the Sale of Investment Property

Investors can reduce their taxable gain by subtracting legitimate selling costs from sale proceeds before calculating profit. The IRS permits deductions for costs directly tied to completing the sale — meaning money spent to transfer the property to a buyer can come off your gain before taxes apply.

Selling Costs That Reduce Your Amount Realized

The IRS defines "amount realized" as total money received, plus the fair market value of any property or services received, plus liabilities assumed by the buyer (such as a mortgage), minus selling expenses.

IRS-recognized selling expenses that directly reduce your gain:

- Real estate agent commissions

- Attorney fees

- Title search and insurance fees

- Escrow fees

- Transfer taxes and recording fees

- Document preparation fees

- Advertising costs (photography, staging that doesn't physically alter the property)

- Notary fees

These expenses are subtracted from the sales price to arrive at your amount realized — they directly reduce your taxable gain, not as separate deductions.

Excluded expenses: Costs that physically affect the property — cleaning, cosmetic repainting, landscaping — cannot reduce your amount realized, even if they made the property easier to sell.

Capital Improvements That Increase Your Adjusted Basis

Any capital improvements made during ownership can be added to the property's cost basis, which reduces your taxable gain. A higher adjusted basis means a smaller profit for tax purposes.

Example: If your original purchase price was $400,000 and you invested $60,000 in improvements, your basis before depreciation is $460,000. If you sell for $700,000, your gain before depreciation adjustments is $240,000 — not $300,000.

Capital improvements include:

- Additions and structural upgrades

- New systems (HVAC, plumbing, electrical)

- Major renovations and remodeling

- New roofing

- Paving, landscaping, or site improvements with a useful life exceeding one year

Improvements vs. repairs — a tax-critical difference: Capital improvements must be capitalized and increase your basis; repairs and maintenance are deductible as operating expenses but do not. According to IRS Publication 527, an expense must be capitalized if it results in a betterment, restores a substantial structural part, or adapts the property to a new use. Misclassifying one as the other creates costly miscalculations on your sale return.

Suspended Passive Activity Losses

If your property generated rental losses in prior years that were suspended due to passive activity loss rules, those "banked" losses can be fully released and deducted in the year you sell the property in a fully taxable transaction. This can reduce your taxable gain — or even offset other income.

IRC §469(g) and Publication 925 specify that suspended passive activity losses are allowed in full when you dispose of your entire interest in the passive activity in a fully taxable transaction to an unrelated party. Investors who held properties through loss years without claiming those losses should account for them before closing — the release is automatic once the disposition qualifies, but only if you've tracked the suspended amounts accurately over time.

Depreciation Recapture: The Tax Most Investors Underestimate

Depreciation recapture is the IRS "taking back" the benefit of depreciation deductions you claimed during ownership by taxing that portion of your gain at a higher rate. For residential rental property (Section 1250 property), this is called "unrecaptured Section 1250 gain" and is taxed at a maximum rate of 25% — higher than the standard long-term capital gains rate.

How Depreciation Recapture Works

Example: You bought a property for $500,000, depreciated it by $80,000 over the years, and sold it for $600,000. Your adjusted basis is now $420,000 ($500,000 - $80,000 depreciation), meaning your total gain is $180,000. But the IRS splits this gain into two buckets:

- $80,000 (depreciation recapture) taxed at up to 25%

- $100,000 (remaining capital gain) taxed at 0%, 15%, or 20% depending on your income bracket

Depreciation recapture applies regardless of whether you actually claimed depreciation on your tax returns. The IRS taxes depreciation "allowed or allowable," meaning investors who failed to claim depreciation are still subject to recapture on the depreciation they should have taken.

Cost Segregation and Depreciation Tracking

Investors who commissioned a cost segregation study during ownership took accelerated depreciation by reclassifying property components into shorter depreciable lives (5, 7, and 15 years). That front-loaded strategy improves cash flow during ownership, but at sale, those accelerated deductions reduce your adjusted basis and increase your taxable gain.

This is why a detailed depreciation schedule matters before you list. Seneca Cost Segregation's engineering-based studies have delivered an average first-year deduction of $171,243 across more than 10,200 properties assessed — and every dollar of that deduction factors directly into your recapture calculation at sale. Knowing your full depreciation history, including any accelerated amounts, lets you model your tax exposure before closing rather than discover it after.

Strategies to Reduce Your Tax Bill Before and During the Sale

1031 Like-Kind Exchange

A Section 1031 exchange allows investors to defer capital gains and depreciation recapture taxes entirely by reinvesting proceeds from the sale into a like-kind replacement property.

Key rules:

- Identify replacement properties within 45 days of selling your relinquished property

- Close on the replacement property within 180 days of the sale (or your tax return due date, whichever is earlier)

- Use a qualified intermediary — you cannot take direct control of the sale proceeds at any point

- Replace with a property of equal or greater value to fully defer the gain

A 1031 exchange defers — not eliminates — the tax. The deferred gain rolls into the new property's adjusted basis, which means you'll eventually face taxation when you sell the replacement property (unless you execute another 1031 exchange).

Tax-Loss Harvesting and Strategic Timing

If deferral isn't the right fit, two other levers can shrink your tax bill before you close.

If you have losses on other capital assets that year — stocks, another property, mutual funds — those losses offset gains from the sale dollar for dollar. Capital loss netting rules let you reduce your taxable gain by strategically timing when you realize those losses.

Timing the sale itself matters too. Selling in a year when your other taxable income is lower can push you into a lower capital gains bracket, reducing your overall rate on the gain.

Selling at a Loss (Section 1231 Losses)

If your adjusted basis exceeds the sale price, the result is a Section 1231 loss — a favorable type of loss that can offset ordinary income (salary, business income, other capital gains). Unlike personal residence losses, rental property losses from a sale are deductible.

When Section 1231 losses exceed Section 1231 gains for the year, the net result is an ordinary loss — fully deductible against wages, business income, or other earnings. A large Section 1231 loss can even create a net operating loss (NOL) that can be carried forward indefinitely (though limited to 80% of taxable income per year).