While the concept sounds simple, the results vary dramatically depending on which method you use, how you calculate cost basis, what recovery period applies, and whether you're leaving deductions on the table. A 2025 IRS Cost Segregation Audit Techniques Guide analysis shows that investors who properly reclassify building components can more than double their cumulative deductions over the first five years compared to standard straight-line depreciation.

This guide covers IRS eligibility rules, a step-by-step depreciation process, the key variables that affect your deduction, common mistakes, and how savvy investors accelerate their depreciation to maximize first-year savings.

TL;DR

- Property depreciation lets you deduct an income-producing property's cost over its IRS-defined useful life: 27.5 years (residential) or 39 years (commercial)

- Eligible properties must be owned by you, used for business or income-producing purposes, have a determinable useful life greater than one year, and not be land

- Straight-line depreciation under MACRS is standard, but bonus depreciation and cost segregation can front-load deductions significantly

- Annual deduction size depends on cost basis, recovery period, depreciation method, and the mid-month convention

- Common mistakes include depreciating land value, using wrong recovery periods, and missing components that qualify for 5-, 7-, or 15-year schedules

How to Depreciate Property: Step-by-Step

Step 1: Determine If Your Property Qualifies

The property must meet all four IRS criteria from Publication 946:

- You own it (or made capital improvements to it)

- Business or income-producing use (not personal use)

- Determinable useful life (greater than one year)

- Not land or personal-use property (land has infinite useful life and is explicitly excluded)

Both residential rentals and commercial properties qualify, as do certain improvements and personal property components within the building. The IRS defines "placed in service" as when the property is ready and available for rent, not necessarily when it's first occupied or when you purchased it.

Once you've confirmed eligibility, the next step is establishing what you can actually depreciate: your cost basis.

Step 2: Calculate Your Cost Basis

Cost basis is not simply the purchase price. It includes:

- Purchase price minus the value of the land

- Plus allowable closing costs (title fees, recording fees, legal fees)

- Plus any capital improvements made before placing the property in service

Land value must be subtracted because land is never depreciable. According to IRS Publication 551, you can separate land from building value using either fair market value allocations or assessed values from your property tax statement.

Example: You purchase a rental property for $800,000. The tax assessment shows land represents 25% of the total value ($200,000). You paid $15,000 in capitalizable closing costs (title insurance, recording fees, legal fees). Your depreciable basis is $800,000 - $200,000 + $15,000 = $615,000.

Capitalizable vs. Non-Capitalizable Closing Costs:

| Add to Basis | Expense or Amortize |

|---|---|

| Abstract/title fees | Casualty insurance premiums |

| Recording fees | Pre-closing rent/utilities |

| Legal fees (title search, deed) | Loan origination fees |

| Surveys | Mortgage insurance premiums |

| Transfer taxes | Credit report costs |

| Owner's title insurance | Lender-required appraisal fees |

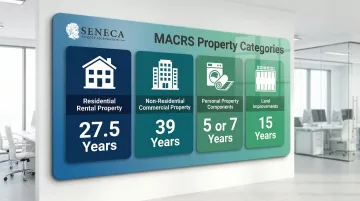

Step 3: Identify the Correct Recovery Period and Depreciation System

The IRS requires the Modified Accelerated Cost Recovery System (MACRS) for most U.S. real estate:

| Property Type | Details |

|---|---|

| Residential rental property: | 27.5-year recovery period |

| Non-residential commercial property: | 39-year recovery period |

| Personal property components: | 5 or 7 years (appliances, carpeting, furniture) |

| Land improvements: | 15 years (parking lots, fencing, sidewalks, landscaping) |

Personal property components within a building may qualify for shorter recovery periods, which is the basis of cost segregation studies that can accelerate deductions by years. With your recovery period confirmed, you then need to apply the correct convention for calculating your first-year deduction.

Step 4: Apply the Correct Depreciation Convention

The IRS requires real estate to use the mid-month convention, which assumes the property was placed in service at the midpoint of the month. This affects the deduction in both the first and last year of ownership.

As noted in Step 1, the placed-in-service date is when the property is ready and available for rent. If you buy a rental property on March 15th and it's ready to rent on April 1st, your placed-in-service date is April 1st, giving you 8.5 months of depreciation in year one.

Step 5: Calculate the Annual Deduction and Report on Form 4562

Straight-line calculation:

The annual deduction is calculated by dividing the depreciable cost basis by the recovery period, then adjusting for the mid-month convention in year one.

Example: $300,000 depreciable basis ÷ 27.5 years = $10,909/year

If placed in service in January, you'll claim 11.5 months in year one: $10,909 × (11.5/12) = $10,454

Depreciation is reported on IRS Form 4562 (Depreciation and Amortization) and flows to Schedule E for rental properties. This form is required every year a deduction is claimed, in the first year and each subsequent year.

What Qualifies as Depreciable Property (and What Doesn't)

The IRS draws clear lines between what can and cannot be depreciated. Getting this wrong is one of the most common errors real estate investors make.

What Can Be Depreciated

Main categories of depreciable real property:

| Can Be Depreciated | Cannot Be Depreciated |

|---|---|

| Residential rental buildings (where 80%+ of gross rental income comes from dwelling units) | Land (infinite useful life; the IRS does not allow depreciation) |

| Commercial buildings (offices, stores, warehouses) | Your primary residence or personal vehicle (personal-use property) |

| Structural improvements and renovations | Fix-and-flip properties (inventory held primarily for sale) |

| Personal property components within buildings (appliances, flooring, fixtures) | Assets with no business use component |

| Land improvements (parking lots, fencing, sidewalks, landscaping) | Artwork or antiques held purely for appreciation |

| — | Property placed in service and disposed of in the same tax year |

Capital improvements to property you don't own, such as leasehold improvements, can also be depreciated if they have a useful life greater than one year.

What Cannot Be Depreciated

Not every asset tied to real estate qualifies. The following are explicitly excluded:

The personal use rule: When a property has mixed personal and business use, such as a vacation rental the owner also occupies, only the business-use percentage is depreciable. According to IRS Topic 415, a dwelling unit qualifies as a residence if personal use exceeds the greater of 14 days or 10% of the total days rented at fair rental price.

If your property is classified as a residence and rented fewer than 15 days per year, you cannot report rental income or deduct any rental expenses, including depreciation.

Key Variables That Determine Your Depreciation Deduction

The size and timing of your depreciation deduction isn't fixed. Four variables control how much you can deduct and when.

Cost Basis

A higher depreciable cost basis (building value minus land) directly increases the annual deduction. Errors in calculating cost basis, such as not including eligible closing costs or incorrectly valuing the land, can understate or overstate deductions.

According to IRS Publication 551, these settlement costs must be added to your basis:

- Title insurance premiums and recording fees

- Legal fees for title search and deed preparation

- Transfer taxes and survey costs

Loan-related costs, including origination fees and mortgage insurance, must be amortized separately. Properly capitalizing eligible costs can add thousands to your depreciable basis.

Recovery Period

The IRS recovery period determines how many years deductions are spread across. Shorter recovery periods (5, 7, or 15 years for certain components) generate larger annual deductions than the standard 27.5- or 39-year schedules.

An engineering-based cost segregation study identifies components that qualify for shorter recovery periods, converting a portion of the building's cost into accelerated early-year deductions. For example, carpeting and appliances qualify for 5-year depreciation, while parking lots and landscaping fall under 15-year schedules.

Depreciation Method

Straight-line depreciation spreads equal deductions each year over the recovery period. Accelerated depreciation methods front-load deductions in earlier years. Under MACRS, real property (buildings) must use straight-line, while personal property can use accelerated methods.

Impact comparison over first 5 years:

| Scenario | Year 1 | Year 2-5 | 5-Year Total |

|---|---|---|---|

| Standard 27.5-year straight-line ($300,000 basis) | $10,455 | $10,909 each | $54,091 |

| With 30% reclassified to 5-year + 40% bonus | $54,118 | Varies | $124,753 |

That difference in early-year cash flow is what makes the depreciation method, and the classification of property components, worth examining carefully.

Bonus Depreciation and Section 179

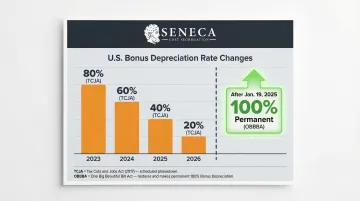

Bonus depreciation allows qualifying property to be fully or partially expensed in the year it's placed in service, rather than over the recovery period. Under the Tax Cuts and Jobs Act (TCJA), bonus depreciation was phasing down: 40% in 2025, 20% in 2026. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Section 179 allows similar immediate expensing up to an annual dollar cap: $2.56 million for 2026 according to Revenue Procedure 2025-32.

One important boundary applies to both: neither bonus depreciation nor Section 179 applies to the building structure itself. Building structures (27.5-year and 39-year property) are explicitly excluded. These benefits only reach real estate through a cost segregation study, which reclassifies eligible components into shorter-lived property classes that do qualify.

Common Mistakes When Depreciating Property

These four errors show up repeatedly, and each one either reduces your deductions or creates IRS exposure.

Including land in your depreciable basis. Land has no useful life and is explicitly excluded by the IRS. If you depreciate it anyway, the IRS can disallow those deductions and assess the 20% accuracy-related penalty under IRC 6662, plus interest.

Using the wrong recovery period or start date. Commercial property depreciates over 39 years, not 27.5; misclassifying it costs you deductions. Miscalculating the "placed in service" date is equally common; the ready-for-rent date, not the purchase date, is the correct reference.

Treating the entire property as a single long-lived asset. Appliances, flooring, and land improvements qualify for 5-, 7-, or 15-year recovery. Skipping a cost segregation analysis means you're likely depreciating those components over 27.5 or 39 years, a significant missed opportunity.

Not filing Form 4562 every year. Depreciation must be claimed annually on Form 4562. Skipping a year forfeits that deduction unless corrected. Under the "allowed or allowable" rule, the IRS calculates recapture tax as if you had taken the depreciation regardless. Form 3115 can be used to recover missed deductions in a single year without amending prior returns.

How to Accelerate Depreciation on Real Estate

Standard straight-line depreciation on a 27.5- or 39-year schedule is the baseline, but investors who want to maximize first-year cash flow have IRS-compliant strategies to front-load deductions significantly.

Cost Segregation Studies

A cost segregation study is an engineering-based analysis that reclassifies components of a building from the standard 27.5/39-year schedule into shorter 5-, 7-, or 15-year property classes, unlocking bonus depreciation on those components and substantially increasing first-year deductions.

The IRS Cost Segregation Audit Techniques Guide defines this as an analysis used to allocate building costs to tangible personal property (Section 1245 property). The IRS does not prescribe a specific methodology, but states that a "quality" study is accurate, well-documented, and prepared by an individual with expertise in both construction and tax law.

This strategy is most effective for recently purchased or newly constructed properties. Seneca Cost Segregation has helped investors achieve an average first-year deduction of $171,243 by conducting IRS-compliant, engineering-based cost segregation studies across all property types. Their engineering team has completed over 10,200 studies nationwide, analyzing over $5 billion in property costs.

Cost segregation unlocks a second lever: bonus depreciation. The reclassified short-life components qualify for bonus depreciation immediately, while the building shell does not.

Bonus Depreciation (Phasedown Schedule)

Current bonus depreciation rates depend on when property was acquired and placed in service:

| Acquisition / Placed-in-Service Period | Governing Law | Bonus Depreciation Rate |

|---|---|---|

| September 27, 2017 – December 31, 2022 | TCJA | 100% |

| January 1, 2023 – December 31, 2023 | TCJA | 80% |

| January 1, 2024 – December 31, 2024 | TCJA | 60% |

| January 1, 2025 – January 18, 2025 | TCJA | 40% |

| January 19, 2025 – December 31, 2030 (acquisition date on or after January 19, 2025) | OBBBA | 100% |

| 2025 (acquisition date before January 19, 2025) | TCJA (still in effect) | 40% |

| 2026 (acquisition date before January 19, 2025) | TCJA (still in effect) | 20% |

Note: The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

With the TCJA schedule declining each year, every year of delay reduces the bonus percentage available on reclassified components. A cost segregation study completed now on a recently acquired property captures a meaningfully higher deduction than the same study completed in 2026.

Frequently Asked Questions

What is depreciable property?

Depreciable property is any asset you own and use for business or income-producing purposes that loses value over time. To qualify, it must meet all four IRS criteria from Publication 946: ownership, business use, determinable useful life, and a useful life exceeding one year.

What are examples of depreciable property?

Examples include residential rental buildings, commercial properties, machinery, vehicles, computers, appliances within a rental unit, and land improvements like parking lots and fencing. Land itself is excluded, as are personal-use assets like your primary residence.

What is 5-year depreciable property?

5-year property under MACRS includes assets like computers, appliances, and certain vehicles. In real estate, components such as carpeting and appliances in a rental property can qualify. A cost segregation study identifies and reclassifies these components to unlock faster deductions.

What is the depreciation recovery period for rental property?

Residential rental properties use a 27.5-year recovery period under MACRS; commercial properties use 39 years. Both default to the straight-line method unless components are reclassified through cost segregation into shorter 5-, 7-, or 15-year schedules.

Can you depreciate a property you're still paying a mortgage on?

Yes, you can depreciate a mortgaged property. The IRS only requires that you own the property and use it for income-producing purposes. Your loan balance does not affect your eligibility to claim depreciation deductions.

What happens to depreciation when you sell a rental property?

When you sell a depreciated property, the IRS requires depreciation recapture. The accumulated deductions are taxed as "unrecaptured Section 1250 gain" at a maximum rate of 25%. Any remaining profit above that amount is subject to standard capital gains tax separately.