Introduction

Real estate is one of the few investment classes the U.S. tax code actively rewards. The provisions aren't loopholes — they're intentional mechanisms built into the tax code to incentivize property investment, and most investors barely scratch the surface of what's available to them.

Many investors collect rental income, watch properties appreciate, and still leave tens of thousands in tax savings uncaptured each year. Tax strategy gets treated as an afterthought rather than a core part of the investment.

The difference between an investor who claims straight-line depreciation and one who layers cost segregation, 1031 exchanges, and strategic entity structuring can exceed $100,000 in deferred taxes on a single property: capital that could fund the next acquisition or eliminate debt.

TLDR

- Deduct operating expenses like mortgage interest, property taxes, insurance, and management fees directly against rental income each year

- Depreciation generates a non-cash deduction over 27.5 years (residential) or 39 years (commercial) — cost segregation can front-load much of that into year one

- Long-term capital gains rates (0%, 15%, or 20%) apply to properties held over one year, often saving 10%+ versus ordinary income rates

- 1031 exchanges allow indefinite tax deferral by reinvesting proceeds into like-kind properties within strict 45/180-day windows

- Stacking these strategies — depreciation, deductions, 1031s — can eliminate taxes on cash-flowing properties entirely, which is why tax structure often determines whether a deal pencils out

What Are the Tax Benefits of Real Estate Investing?

Real estate tax benefits are IRS-recognized deductions, deferrals, and exclusions that legally reduce the taxable income and capital gains generated by investment properties. They're not loopholes—they're intentional provisions codified in the Internal Revenue Code to encourage real estate investment and economic development.

These benefits apply primarily to investment and rental properties, not primary residences. Your level of active participation, total income, and entity structure all influence which benefits you can access. For example, an investor managing properties through an LLC may qualify for the Section 199A pass-through deduction, while a passive limited partner might face different limitations.

The sections below break down each major benefit — depreciation, deductions, capital gains treatment, and more — along with who qualifies and how to maximize what you keep.

Key Tax Benefits That Directly Reduce Your Annual Tax Bill

Operating Expense Deductions

Investors can deduct ordinary and necessary operating expenses against rental income each year, directly reducing taxable income. Qualifying expenses include:

- Mortgage interest

- Property taxes

- Insurance premiums

- Repairs and maintenance

- Property management fees

- Legal and accounting fees

- Advertising costs

- Travel related to property management

These aren't one-time write-offs. They recur annually, creating consistent tax savings throughout your holding period.

The Pass-Through Deduction (Section 199A)

Investors who own rental property through sole proprietorships, LLCs, partnerships, or S-Corps may deduct up to 20% of qualified business income on their personal returns. For 2026, this deduction begins to phase out at $201,750 for single filers and $403,500 for married couples filing jointly.

To qualify, rental activity must meet the IRS safe harbor under Revenue Procedure 2019-38: at least 250 hours of rental services performed annually, separate books maintained for each property, and contemporaneous time records. Triple-net leases and personal residences are explicitly excluded.

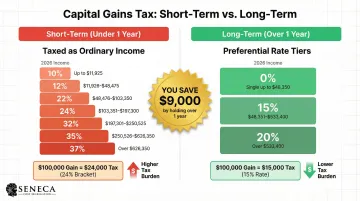

Capital Gains Tax Advantage

Properties held longer than one year qualify for long-term capital gains rates of 0%, 15%, or 20%, depending on income—far lower than ordinary income rates, which can reach 37%.

Example — $100,000 gain:

- Short-term (ordinary income at 24% bracket): $24,000 tax

- Long-term (15% LTCG rate): $15,000 tax

- Direct savings: $9,000

For 2026, the 15% LTCG rate applies to single filers with taxable income between $49,451 and $545,500, and married couples filing jointly between $98,901 and $613,700.

FICA Tax Exemption

Unlike self-employment income, net rental income reported on Schedule E is generally not subject to the 15.3% FICA payroll tax. This creates a meaningful advantage for investors who also earn W-2 income from other sources. However, if you provide substantial services—regular cleaning, concierge services, or daily management typical of hotels—the IRS may reclassify your activity as a trade or business subject to self-employment tax.

That said, the FICA exemption doesn't mean rental income escapes all payroll-adjacent taxes. Passive rental income may still be subject to the 3.8% Net Investment Income Tax (NIIT) if your Modified Adjusted Gross Income exceeds $200,000 (single) or $250,000 (married filing jointly).

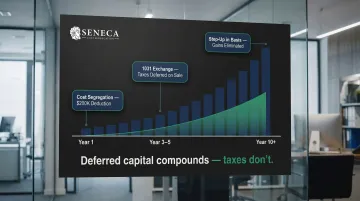

Step-Up in Basis Estate Planning Benefit

When investment property is inherited, heirs typically receive a stepped-up cost basis equal to fair market value at the time of inheritance. This can reduce or eliminate capital gains taxes on appreciated property entirely—making real estate one of the more tax-efficient ways to pass wealth between generations.

Example: You purchase a rental property for $300,000 that appreciates to $800,000 by the time of your death. Your heirs inherit the property with a $800,000 basis, erasing $500,000 in taxable gain that would otherwise trigger depreciation recapture and capital gains taxes.

Depreciation and Cost Segregation: The Non-Cash Deduction That Changes Everything

Depreciation and Cost Segregation: The Non-Cash Deduction That Shelters Rental Income

How Depreciation Works

The IRS allows investors to deduct the cost of an income-producing property (excluding land) over its "useful life"—27.5 years for residential rental properties and 39 years for commercial properties—even while the property may be increasing in market value. This is a non-cash deduction: no additional spending required, just a reduction in taxable income.

Straight-line depreciation example: For a residential rental property with a depreciable value of $350,000:

- Annual deduction: $350,000 ÷ 27.5 = $12,727

- At a 24% tax bracket: $3,055 annual tax savings

This deduction shields a substantial portion of annual rental income from taxation, turning what would be taxable cash flow into tax-free income.

Cost Segregation: Accelerating the Timeline

Cost segregation is an engineering-based strategy that reclassifies building components—flooring, fixtures, landscaping, specialty systems—from the 27.5 or 39-year schedule to 5, 7, or 15-year schedules. This allows investors to concentrate deductions in the first year rather than spreading them over decades.

Industry research shows that typically 20% to 40% of a building's cost can be reclassified to shorter-lived property. The net-present-value benefit: every $100,000 reclassified from 39-year to 5-year property yields approximately $16,000 in tax savings.

Bonus Depreciation Interaction

Components reclassified through cost segregation may qualify for bonus depreciation. The One, Big, Beautiful Bill Act (OBBBA) permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. This means investors can deduct a significant portion of reclassified asset values in year one.

Real-world impact: A $2 million commercial property might yield:

- Reclassified assets: $600,000 (30% of building basis)

- Bonus depreciation at 100%: $600,000 first-year deduction

- Tax savings at 35% rate: $210,000

That kind of result doesn't happen automatically — it requires a qualified cost segregation study executed before filing.

What to Look for in a Cost Segregation Provider

Not all cost segregation studies carry equal weight with the IRS. A qualified provider should follow the IRS Cost Segregation Audit Techniques Guide and use licensed engineers — not software-only tools — to classify each asset.

Seneca Cost Segregation uses an engineering-based methodology across all 50 states, with studies typically completed in 2–4 weeks. Their studies are designed to be audit-ready, and they back their work with an AuditDefense guarantee. Investors should coordinate with their CPA when applying these deductions, particularly to navigate passive activity loss limitations that can affect how much of the savings is usable in a given tax year.

Tax Deferral Strategies: Extending and Compounding Your Benefits

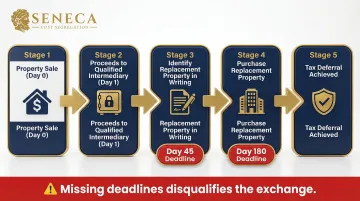

The 1031 Exchange (Like-Kind Exchange)

When you sell an investment property, IRC §1031 allows you to defer all capital gains taxes—and depreciation recapture—by reinvesting proceeds into a replacement property of equal or greater value.

Critical deadlines:

- 45 days: Identify replacement property in writing after closing on the sale

- 180 days: Complete the purchase of the replacement property

This can be repeated indefinitely, allowing investors to grow portfolios while deferring taxes and redeploying capital into larger assets. A qualified intermediary must hold proceeds during the exchange period; direct receipt of funds disqualifies the exchange.

Depreciation Recapture Planning

When a property is eventually sold without a 1031 exchange, the IRS taxes previously claimed depreciation as unrecaptured §1250 gain at a maximum rate of 25%. If cost segregation reclassified assets as personal property (§1245), that depreciation is recaptured at ordinary income rates up to 37%.

Savvy investors plan for this by:

- Executing a 1031 exchange to defer indefinitely

- Holding until death to trigger step-up in basis

- Strategically timing sales in lower-income years

- Working with tax advisors to model recapture scenarios

Opportunity Zone Investments

Investors who reinvest realized capital gains into a Qualified Opportunity Fund within 180 days may defer those gains until December 31, 2026, or upon an earlier inclusion event. Under certain holding conditions, they may eliminate capital gains on the new investment entirely after 10 years.

The tradeoff involves concentration risk in designated census tracts and illiquidity over a longer hold period — a qualified advisor can help you weigh deferred gain timing against those constraints before committing capital.

How Deferral Strategies Compound

An investor who uses cost segregation to generate $200,000 in first-year depreciation deductions, then executes a 1031 exchange on sale, can compound tax savings across multiple properties — deferring that same $200,000 liability for decades while reinvesting freed-up capital into progressively larger assets.

What Happens When Investors Leave These Benefits on the Table

The Real Cost of Under-Using Tax Benefits

An investor relying only on straight-line depreciation rather than cost segregation may be leaving $50,000 to $150,000 in deferred taxes on the table in the first year alone. Those are dollars that could otherwise be:

- Reinvested into the next property

- Used to pay down high-interest debt

- Deployed to increase cash reserves and financial flexibility

The opportunity cost compounds annually. Over a 10-year holding period, the difference between strategic tax planning and passive depreciation can exceed $500,000 in cumulative lost deferral value on a multi-million-dollar property portfolio.

The Compounding Opportunity Cost

Real estate tax benefits don't compound automatically: they require active claiming and strategic layering. Investors who stay passive about tax planning effectively pay a premium on every year of ownership.

Common mistakes that accelerate this cost include:

- Inconsistent recordkeeping across tax years

- Failure to identify and track depreciable assets

- Not engaging a cost segregation professional early in ownership

The IRS does allow "look-back" studies via Form 3115 to capture missed depreciation in the current year. Even so, that's no substitute for years of foregone tax deferral and lost reinvestment opportunity.

How to Get the Most from Real Estate Tax Benefits

These benefits work best when applied consistently and in combination. The foundational practices that separate investors who use these benefits fully from those who only scratch the surface include:

Maintain detailed records:

- Track every property expense with receipts and documentation

- Log time spent on rental activities to meet 199A safe harbor

- Separate books for each rental enterprise

- Contemporaneous records, not reconstructed later

Structure ownership strategically:

- Use pass-through entities (LLCs, partnerships) to access 199A deductions

- Coordinate with estate planning to maximize step-up in basis

- Consider entity structure before acquisition, not after

Time property sales strategically:

- Identify 1031 exchange opportunities before listing properties

- Model depreciation recapture scenarios for each exit strategy

- Coordinate with tax advisors to time sales in lower-income years

Engage specialized professionals:

- Work with a real estate-experienced CPA who understands passive activity rules

- Get a cost segregation study from an engineering-based firm like Seneca Cost Segregation

- Connect with qualified intermediaries before initiating 1031 exchanges

Of all these steps, one delivers the most immediate impact on your tax position.

A cost segregation study is one of the highest-ROI steps an investor can take, especially in the first year of ownership or shortly after acquisition, because accelerated deductions hit hardest when front-loaded. Investors with properties above $300,000 to $500,000 in depreciable basis are strong candidates — and those who act early capture the largest deductions while cash flow from the property is still building.

Frequently Asked Questions

What are the tax benefits of real estate investing?

The major categories include annual operating expense deductions, depreciation (accelerated via cost segregation), preferential capital gains treatment for properties held over one year, 1031 exchanges for indefinite tax deferral, and FICA exemption on passive rental income. When used together, these tools can reduce an investor's effective tax rate by 15-25% or more.

What is tax deductible for investment property?

Common deductible expenses include mortgage interest, property taxes, insurance, repairs and maintenance, property management fees, legal and accounting fees, advertising, and travel related to property management. Depreciation is also deductible despite requiring no cash outlay, which makes it one of the most powerful tools in a real estate investor's tax strategy.

What is the $250,000 / $500,000 home sale exclusion?

This exclusion applies to primary residences, not investment properties. Single filers can exclude up to $250,000 and married filers up to $500,000 in capital gains from the sale of a home they've lived in for at least 2 of the past 5 years. Rental properties do not qualify unless converted back to a primary residence and the occupancy test is met.

What is the most tax-efficient way to own real estate?

Structure ownership through a pass-through entity (LLC or partnership) to access the 199A deduction, front-load deductions with cost segregation, and use 1031 exchanges to defer capital gains on sale. The right combination depends on your income level, portfolio size, and estate planning objectives — a tax advisor can help you prioritize.

What is the downside of a 1031 exchange?

Key limitations to know:

- Tight deadlines: 45 days to identify a replacement property, 180 days to close

- No access to proceeds: funds must be held by a qualified intermediary

- Full reinvestment required: proceeds must go into equal or greater value property to defer all taxes

- Deferral, not elimination: taxes still apply on eventual sale unless the property is held until death and receives a step-up in basis