Most real estate investors pay thousands in unnecessary taxes every year because they're using depreciation schedules designed for entire buildings, not for the dozens of components inside them that wear out much faster.

When you buy a $1 million commercial property, the IRS assumes every component, from the roof structure to the carpeting to the HVAC system, will last the same 39 years. Appliances, flooring, and specialized equipment don't last four decades. By treating them as if they do, you're deferring deductions you could claim today.

This guide is for residential rental owners, commercial property investors, multi-family operators, and short-term rental hosts who want to understand how cost segregation actually works, not just that it exists. Here's what you'll find inside:

- What cost segregation is and the tax mechanics behind it

- How the process works, from feasibility review through final report delivery

- Which properties and investor profiles benefit most

- When cost segregation may not be the right move

If you're leaving depreciation on the table, this guide shows you exactly what to do about it.

TL;DR

- Cost segregation reclassifies building components from 27.5–39 year timelines into 5-, 7-, or 15-year categories, generating immediate deductions

- IRS-sanctioned and engineering-backed: not a loophole, and fully defensible under audit

- The biggest benefit is accelerating deductions into early years when they offset active income or capital gains

- Works best for income-producing properties valued at $250,000+ held as investment assets

- An engineering-based study is what separates a compliant, audit-ready filing from an unsupported claim

What Is Cost Segregation and Why Does It Matter for Real Estate Investors?

Cost segregation is an IRS-approved tax strategy that involves hiring qualified professionals to break down a property's purchase price into individual components, each assigned a shorter depreciation life than the building as a whole.

The Depreciation Baseline Problem

By default, residential rental properties depreciate over 27.5 years and commercial properties over 39 years. A $1 million commercial property generates only about $25,640 in annual depreciation ($1M ÷ 39 years). Cost segregation challenges that default by identifying components, including flooring, cabinetry, landscaping, parking lots, specialty electrical systems, that legally qualify for 5-, 7-, or 15-year depreciation schedules.

According to IRS Publication 946, the Modified Accelerated Cost Recovery System (MACRS) establishes these standard lives, but most investors never look beyond the building-level classification.

The Tax Impact

Accelerating depreciation front-loads deductions into years 1–5 rather than spreading them over decades. This reduces taxable income in high-earning years when you need offsets most. Since depreciation offsets ordinary income first (taxed at rates up to 37%) before applying to capital gains, the savings can be significant: offsetting income taxed at 37% with depreciation deductions is far more valuable than letting that income hit your return untouched.

Example: A $500,000 property with 25% of its basis reclassified to 5-year property generates approximately $125,000 in accelerated deductions in year one (assuming 100% bonus depreciation). At a 37% tax rate, that's $46,250 in tax savings, money you can reinvest immediately.

How Cost Segregation Differs from Standard Depreciation

Cost segregation is not a replacement for straight-line depreciation but an engineering-led process that optimizes how the total cost basis is allocated across asset classes. It differs from bonus depreciation, which is a separate accelerator that often pairs with cost segregation to create even larger first-year deductions.

That distinction matters to the IRS as well. The IRS Cost Segregation Audit Techniques Guide endorses this strategy when conducted using proper engineering methodology, distinguishing it from aggressive tax shelters.

Who Qualifies

Any owner of income-producing real property can benefit:

- Commercial property owners (office, retail, industrial)

- Residential rental investors (single-family, multi-family)

- Mixed-use property operators

- Short-term rental hosts

- Hotel and hospitality investors

The key requirement: the property must be held for business or investment purposes, not purely as a personal residence.

How Cost Segregation Works: A Step-by-Step Breakdown

A cost segregation study begins at property acquisition (or can be completed retroactively) and produces a detailed engineering report that reclassifies building components into shorter depreciation lives. Understanding each step helps investors evaluate what to expect and how the resulting deductions flow into their tax filings.

Step 1: Property Assessment and Feasibility Review

The process begins with determining whether a study makes financial sense. The provider reviews:

- Property type and cost basis

- Year placed in service

- Investor's tax situation and ability to use deductions

- Documentation availability

Properties with a cost basis under $200,000–$300,000 may not generate enough deductions to justify study costs. Industry guidance suggests that properties below $500,000 in building basis should be carefully evaluated for ROI before proceeding.

Seneca Cost Segregation conducts a complimentary feasibility assessment before any commitment, helping investors understand potential savings without obligation.

Step 2: Engineering Analysis and Component Reclassification

A qualified engineer (ideally holding credentials like the Certified Cost Segregation Professional (CCSP) designation) conducts detailed property analysis using blueprints, site visits, or documented review to identify every component qualifying for accelerated depreciation.

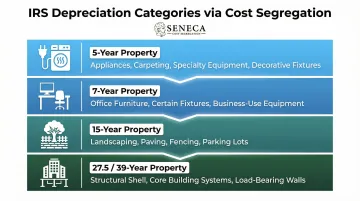

Typical asset categories:

- 5-year property: Appliances, carpeting, specialty equipment, decorative fixtures

- 7-year property: Office furniture, certain fixtures

- 15-year property: Land improvements (landscaping, paving, fencing, parking lots)

- 27.5/39-year property: Structural shell and core building systems

The IRS Cost Segregation ATG is direct on this point: "a study by a construction engineer is more reliable than one conducted by someone with no engineering or construction background." Engineering-based methodology produces more accurate, IRS-compliant results than rule-of-thumb estimates, and holds up far better under audit scrutiny.

Across 8,000+ studies analyzed, standard commercial and multifamily properties typically see 20%–30% of their depreciable basis reclassified to shorter lives, more for property types with higher personal property content, such as hotels or restaurants.

Step 3: Report Delivery and Tax Filing Integration

The completed study is a formal written report documenting each reclassified asset, its assigned depreciation life, and the resulting deduction schedule. Your CPA uses this report to amend or file tax returns accordingly.

A well-prepared study includes audit-ready documentation: detailed component schedules, cost allocations, and legal support for every reclassification. Seneca backs this with AuditDefense and a money-back guarantee, so investors have both the deductions and the protection to stand behind them.

Which Properties and Investors Benefit Most

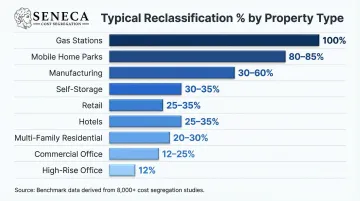

Property Types with Highest Reclassification Potential

According to comprehensive benchmark data from 8,000+ studies, reclassification percentages vary dramatically by property type:

| Property Type | Typical Reclassification % |

|---|---|

| Gas stations (fuel only) | 100% |

| Mobile home parks | 80-85% |

| Manufacturing facilities | 30-60% |

| Self-storage | 30-35% |

| Retail properties | 25-35% |

| Multi-family residential | 20-30% |

| Hotels | 25-35% |

| Commercial office | 12-25% |

| High-rise office buildings | 12% |

Commercial buildings and multi-family properties typically yield the highest dollar amounts of reclassifiable assets. Short-term rentals can also benefit given their personal property component density: furnishings, appliances, and guest amenities all qualify for 5-year treatment.

Investor Profiles Who Get the Most Value

Property type determines the size of the deduction. Whether you can use it is a separate question entirely, and the more important one.

Three investor profiles consistently capture the most value:

| Investor Profile | Details |

|---|---|

| Real Estate Professionals (REPS) | Investors who meet IRC §469(c)(7) requirements (750+ hours annually in real estate and more than 50% of total working time) can apply passive losses directly against W-2 or business income. |

| STR Operators | Short-term rental owners who satisfy the material participation test (average guest stay of 7 days or less) can offset non-passive income with rental losses under Temp. Treas. Reg. §1.469-1T(e)(3). |

| Passive Income Investors | Those with significant passive income from other properties can offset it with cost segregation losses with no REPS status required. |

Lookback Studies Expand Who Can Benefit

The profiles above focus on new acquisitions, but cost segregation isn't limited to recent purchases. Lookback studies allow investors who have owned a property for years to capture unclaimed accelerated depreciation in the current tax year without amending prior returns.

Using IRS Form 3115 and a Section 481(a) adjustment, you can claim the entire difference between what you've claimed and what you could have claimed, all in one year.

This expands the opportunity beyond new acquisitions to include properties placed in service as far back as January 1, 1987.

Key Factors That Affect Your Cost Segregation Outcomes

Property Characteristics

Three property-level variables drive most of the variation in study outcomes:

- Cost basis: A $2 million property generates more absolute deductions than a $500,000 property at the same reclassification rate. Higher basis means more dollars eligible for accelerated depreciation.

- Property type and age: Newer construction typically contains a higher share of personal property components. Older properties require more complex analysis but still yield strong results. Benchmark data across 8,000+ studies shows condominiums average 29.3% in 5-year personal property allocations, offsetting their 0% land improvement category.

- Study methodology: Engineering-based studies that itemize individual components capture more deductions than percentage-estimate approaches. The IRS explicitly warns against rule-of-thumb methods lacking proper component-level documentation.

Ability to Utilize Deductions

Passive activity rules under IRC §469 determine whether your accelerated losses offset non-passive income immediately or carry forward as suspended losses. A real estate investor without Real Estate Professional Status (REPS) or STR material participation may generate large paper deductions that can't be used until the property is sold or sufficient passive income exists. Qualifying for REPS or meeting the STR material participation threshold unlocks those losses in the current tax year.

How Bonus Depreciation Amplifies First-Year Deductions

When paired with cost segregation, bonus depreciation allows investors to deduct a large percentage of 5-, 7-, and 15-year property in the year placed in service. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | — |

| January 1, 2023 – December 31, 2023 | 80% | — |

| January 1, 2024 – December 31, 2024 | 60% | — |

| January 1, 2025 – January 18, 2025 | 40% | — |

| January 19, 2025 – December 31, 2030 | 100% | Applies only if acquisition date is January 19, 2025 or later |

| 2025 (if acquisition date is before January 19, 2025) | 40% | TCJA phase-down still applies |

| 2026 (if acquisition date is before January 19, 2025) | 20% | TCJA phase-down still applies |

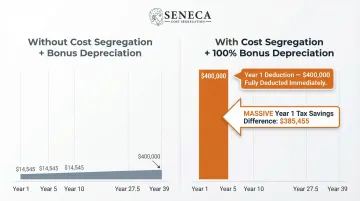

For a property where a cost segregation study identifies $400,000 in 5- and 15-year assets, 100% bonus depreciation converts that entire amount into a year-one deduction, compared to spreading it across 5 to 15 tax years without the study.

Note: The Tax Cuts and Jobs Act (TCJA) phased down bonus depreciation to 40% in early 2025 before OBBBA's restoration. Properties placed in service between January 1, 2025, and January 19, 2025, received only 40% bonus depreciation.

Depreciation Recapture Risk

Accelerated depreciation creates depreciation recapture liability under IRC §1250 and §1245 when you eventually sell. Personal property (Section 1245) is recaptured as ordinary income at your marginal rate (up to 37%), while real property recapture (unrecaptured Section 1250 gain) is capped at 25%.

| Asset Type | Tax Treatment |

|---|---|

| Personal property (Section 1245) | Recaptured as ordinary income at your marginal rate (up to 37%) |

| Real property recapture (unrecaptured Section 1250 gain) | Capped at 25% |

Investors holding long-term can defer recapture through 1031 exchanges and potentially eliminate it entirely if the property transfers at death with a stepped-up basis. According to Form 8824 instructions, a properly structured like-kind exchange defers all depreciation recapture until you sell without exchanging.

Common Misconceptions About Cost Segregation

"It's an Aggressive Tax Shelter"

Cost segregation is explicitly authorized under IRS Revenue Procedure 87-56 and supported by case law including Hospital Corp. of America v. Commissioner, 109 T.C. 21 (1997). The real risk comes from poorly documented or inaccurate studies, not the strategy itself.

The IRS Cost Segregation ATG explicitly sanctions cost segregation when conducted using proper engineering methodology. A study holds up under IRS scrutiny when it follows established protocols — which is why credentialed engineering firms and CCSP-certified professionals matter.

A compliant study typically includes:

- A site visit or detailed property review by a licensed engineer

- Component-level analysis tied to cost allocation

- Documentation that maps directly to IRS asset class guidelines

- A written report defensible under audit

"It Only Benefits Large Commercial Investors"

Residential rental properties, single-family rentals, and STRs above a $250,000 cost threshold can all generate meaningful deductions. Seneca Cost Segregation's clients average $171,243 in first-year deductions across diverse property types and sizes — not just large commercial portfolios.

"All Tax Savings Are Permanent"

Cost segregation creates accelerated deductions, not permanent ones. The total depreciation taken over the asset's life remains the same; it's just redistributed forward. The benefit is the time value of money: front-loaded deductions offset income during your highest-earning years.

Example: Whether you depreciate $100,000 over 5 years or 39 years, you eventually claim $100,000 in deductions. But claiming $100,000 in years 1–5 at a 37% tax rate is worth far more than claiming it in years 20–39. By then, your rate may be lower, and inflation will have eroded the dollar's purchasing power.

When Cost Segregation May Not Make Sense

Unfavorable ROI Scenarios

Three scenarios where the numbers typically don't work in your favor:

| Scenario | Details |

|---|---|

| Low cost basis | Properties with a depreciable basis below $200,000–$300,000 rarely generate enough tax savings to justify study costs ($5,000–$15,000 depending on complexity). |

| Near-term sale plans | Selling within 2–3 years means depreciation recapture will claw back those accelerated deductions as ordinary income, often wiping out the short-term benefit. |

| Low tax brackets | Investors in the 12% or 22% federal brackets receive far less absolute benefit than those in the 32%–37% range. The math rarely works in your favor at lower income levels. |

Inability to Use Passive Losses

Investors who pursue cost segregation without first understanding whether they qualify to use accelerated losses (REPS, STR rules, or passive income offset) may generate suspended losses that sit unused for years.

According to IRS Publication 925, passive activity losses from rental real estate can only offset passive income unless you qualify for specific exceptions. A cost segregation study generating $200,000 in depreciation deductions is worthless on paper if those deductions can't touch your W-2 income and must carry forward indefinitely.

A CPA review of whether the deductions can actually be deployed is an important step prior to commissioning a study. A cost segregation strategy without a broader tax plan behind it delivers far less than it promises.

Frequently Asked Questions

What type of property is best for cost segregation?

Commercial properties and multi-family buildings typically yield the highest reclassification percentages (20–40% of building basis), but residential rentals, STRs, and mixed-use properties above $250,000 cost basis can also generate substantial deductions. The key variable is how much of the property consists of personal property and land improvement components versus structural shell.

Is it worth it to do a cost segregation study?

For investors with income-producing properties valued at $250,000 or more who can actively use the deductions — via REPS, STR material participation, or passive income offset — a cost segregation study typically delivers strong ROI. Seneca Cost Segregation clients average over $171,000 in first-year deductions, with returns of 10:1 to 25:1 on study costs.

How much should I pay for a cost segregation study?

Study costs vary by property type, size, and provider methodology, typically ranging from $5,000–$15,000. Engineering-based studies from CCSP-certified professionals provide greater accuracy and IRS defensibility than lower-cost alternatives. A low-cost, non-engineering study can miss qualifying assets or fail audit scrutiny, negating the savings.

Can I do a cost segregation study on a property I've already owned for several years?

Yes, lookback studies are available for properties already placed in service. Investors can capture all previously unclaimed accelerated depreciation in the current tax year via a Section 481(a) adjustment filed with that year's tax return, without needing to amend prior-year returns. Properties placed in service as far back as January 1, 1987, may qualify.

What happens to my taxes when I sell a property where I used cost segregation?

Depreciation recapture applies upon sale. Accelerated deductions taken under cost segregation are subject to recapture as ordinary income (personal property at your marginal rate up to 37%, real property at 25% for unrecaptured Section 1250 gain). This can be deferred using a 1031 exchange or mitigated by long-term hold strategies.

How does cost segregation interact with bonus depreciation?

Bonus depreciation allows investors to immediately deduct 100% (or the applicable percentage for the tax year) of qualifying 5-, 7-, and 15-year assets identified through cost segregation, rather than depreciating them over their class life. Together, the two strategies can compress years of deductions into a single tax year, significantly reducing or eliminating federal tax liability upfront.

Ready to explore cost segregation for your property? Seneca Cost Segregation offers complimentary feasibility assessments to help you understand your potential tax savings before any commitment. With over 12 years of experience, 10,200+ completed studies, and an AuditDefense guarantee backing every report, Seneca's engineering-based approach ensures IRS compliance and maximum deductions. Contact Seneca at 503-383-1158 or visit senecacostseg.com to schedule your free consultation.