Introduction

Having a completed cost segregation study in hand doesn't automatically translate into tax savings. Many property owners get stuck because they don't know how to convert that study into actual depreciation deductions on their return. The application process differs depending on whether your property was acquired in the current tax year or in a prior year, and errors can mean forfeited deductions, amended returns, or recapture risk.

This guide explains the exact steps to apply cost segregation results on your return, when Form 3115 is required, what documents you need, and the most costly mistakes to avoid. Whether you're filing for the first time or catching up on missed depreciation, this is the mechanical process that turns an engineering study into real dollars saved.

TL;DR

- Cost segregation reclassifies property components into shorter depreciation periods (5, 7, or 15 years), generating larger upfront deductions

- Newly acquired property: apply the study on your current-year return by updating Form 4562

- For properties already on your books, file Form 3115 to capture all missed depreciation at once, with no amended returns needed

- The Section 481(a) adjustment is your lump-sum "catch-up" deduction for all prior-year missed depreciation

- An engineering-based cost segregation study is required for IRS compliance and is your strongest defense if the deductions are ever audited

Step-by-Step: How to Apply Cost Segregation on Your Tax Return

Step 1: Commission a Quality, Engineering-Based Cost Segregation Study

Before anything can be applied to your return, you need a completed cost segregation study prepared by qualified professionals. The IRS expects studies to be methodologically defensible, which means working with licensed engineers or firms certified by the American Society of Cost Segregation Professionals (ASCSP).

To earn the Certified Cost Segregation Professional (CCSP) designation — the field's highest credential — practitioners must document at least 7,000 hours of direct experience, submit sample reports for review, and pass the comprehensive ASCSP exam.

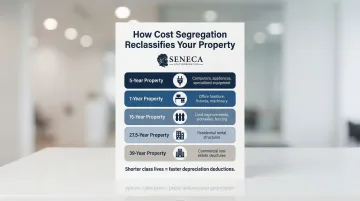

The study produces a detailed asset reclassification report breaking your property's total depreciable basis into specific MACRS property classes:

| Property Class | Examples |

|---|---|

| 5-year property | Carpeting, appliances, specialized electrical systems |

| 7-year property | Office furniture and fixtures |

| 15-year property | Parking lots, landscaping, fencing, sidewalks |

| 27.5-year property | Residential rental building structure |

| 39-year property | Commercial building structure |

This report becomes the direct input for your depreciation schedule. According to the IRS Cost Segregation Audit Techniques Guide, quality studies must include preparation by qualified individuals with construction expertise, detailed engineering take-offs, thorough legal analysis with citations, and reconciliation of allocated costs to total project costs.

Step 2: Review the Asset Reclassification Report with Your CPA

Once the study is complete, your CPA or tax advisor must review the report's asset schedules to understand which components were reclassified from 27.5-year or 39-year property into shorter-lived categories. This review determines whether bonus depreciation applies to any reclassified assets.

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively. For qualified property with an acquisition date of January 19, 2025 or later, the One, Big, Beautiful Bill Act (OBBBA) restored 100% bonus depreciation.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate |

|---|---|

| September 27, 2017 – December 31, 2022 | 100% |

| January 1, 2023 – December 31, 2023 | 80% |

| January 1, 2024 – December 31, 2024 | 60% |

| January 1, 2025 – January 18, 2025 | 40% |

| January 19, 2025 – December 31, 2030 | 100% (if acquisition date is January 19, 2025 or later); 40% in 2025 and 20% in 2026 (if acquisition date is before January 19, 2025) |

This means 5-year and 15-year reclassified assets could generate immediate deductions of 60–100% of their basis, multiplying your first-year deduction.

Step 3: Determine Your Filing Path: New Property vs. Existing Property

The application process splits into two distinct scenarios:

| Scenario | Description | Required Form |

|---|---|---|

| New or recently acquired property (placed in service this year) | Apply cost segregation results directly on this year's return by listing all reclassified assets with their correct MACRS classes and placed-in-service dates on Form 4562. No Form 3115 is required because you're establishing the correct depreciation method from day one. | Form 4562 |

| Property already placed in service in a prior year | You've been depreciating the full building at 27.5 or 39 years, which means a change in accounting method is required. You must file Form 3115. Under Treasury Regulation §1.446-1(e), changing depreciation recovery periods constitutes a change in method of accounting requiring IRS consent. You cannot simply amend prior returns to claim missed depreciation from a cost segregation study on previously placed-in-service property. The IRS requires the formal method change process instead, which prevents taxpayers from duplicating or omitting deductions. | Form 3115 |

Step 4: File IRS Form 3115 If Applying to an Existing Property

Form 3115 is the IRS form used to change your depreciation method from impermissible (straight-line over 27.5 or 39 years for the entire building) to permissible component depreciation using MACRS class lives from the cost segregation study.

Filing mechanics:

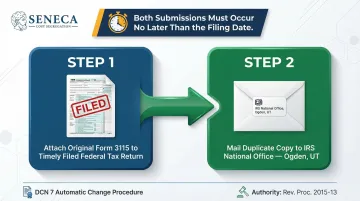

- Attach the original Form 3115 to your timely filed federal income tax return for the year of change

- Submit a duplicate copy to the IRS National Office (Internal Revenue Service, 1973 N. Rulon White Blvd., Ogden, UT 84201, Attn: M/S 6111) no later than the date you file the original

This follows the automatic change procedures under Rev. Proc. 2015-13 and the current List of Automatic Changes (Rev. Proc. 2025-23). Most cost segregation reclassifications use Designated Change Number (DCN) 7, which covers changes from impermissible to permissible depreciation methods.

This form triggers the Section 481(a) adjustment, the cumulative catch-up deduction for all prior-year missed depreciation, which you claim as a single negative income adjustment in the year of change.

Step 5: Update Your Depreciation Schedule and Report the Deductions

Your CPA will update your depreciation schedule to reflect all newly reclassified assets, removing them from the building account and placing them on shorter-lived asset lines with the appropriate placed-in-service dates, MACRS class, and depreciation method.

The Section 481(a) catch-up amount is reported as an "other deduction" on your return, on Schedule E for rental property investors or the appropriate business return form. This gives you all previously missed depreciation in one year, which is the primary driver of the large first-year tax benefit cost segregation is known for.

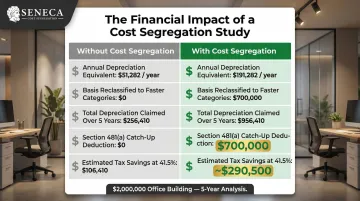

Example: $2M office building, cost segregation applied in year 5:

| Without Cost Segregation | With Cost Segregation | |

|---|---|---|

| Annual depreciation (years 1–5) | $50,000/yr ($250,000 total) | $190,000/yr equivalent |

| Basis reclassified to faster categories | $0 | $900,000 |

| Total depreciation claimed over 5 years | $250,000 | $950,000 |

| Section 481(a) catch-up deduction | N/A | $700,000 (claimed in year 5) |

| Estimated tax savings at 41.5% rate | N/A | ~$290,500 |

The $700,000 catch-up deduction ($950,000 – $250,000) is claimed entirely in the current tax year, generating approximately $290,500 in tax savings at a 41.5% combined rate.

When Should You Apply Cost Segregation on Your Return?

Cost segregation isn't always the right move in every tax year. Timing directly affects how much benefit you capture.

Ideal scenarios for applying cost segregation:

- You have significant taxable income this year and need deductions to offset it

- You acquired or placed property in service this year: apply correct MACRS classes from day one

- You've held a property for multiple years, and accumulated "missed" depreciation can be captured via a Section 481(a) catch-up adjustment

The Journal of Accountancy recommends cost segregation studies whenever expenditures for a structure equal or exceed $750,000. Other established benchmarks cite a minimum threshold of $500,000 to justify the typical $5,000–$15,000 study cost.

Situations requiring timing adjustment:

- You're already in a net operating loss (NOL) position, so additional deductions won't generate immediate cash benefit

- You expect to sell the property soon, as depreciation recapture under Section 1250 could erode the tax savings

- The depreciable basis is under $500,000 (at that level, study costs often outweigh the benefit)

- You're in a low marginal tax bracket this year, since the deductions will be worth more in a higher-income year

One timing question worth addressing upfront: how far back can you go? There's no statutory limit on Section 481(a) lookback adjustments, but industry practice typically focuses on properties placed in service within the past 10–15 years. Beyond that, the remaining adjusted basis rarely justifies the study cost.

What You Need Before Applying Cost Segregation to Your Return

Three things must be in place before your cost segregation study can translate into a defensible tax return: complete property documentation, a compliant study prepared with engineering methodology, and a CPA experienced with depreciation mechanics.

Documents and Property Information Required

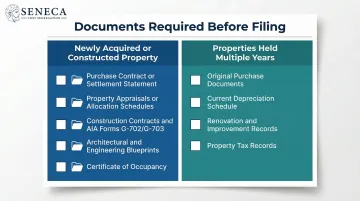

For newly acquired or constructed property:

- Purchase contract or settlement statement: confirms total acquisition cost and closing date

- Property appraisals or allocation schedules: separates land value from building value

- Construction contracts and AIA Forms G-702/G-703: contractor payment applications that break down costs by building component

- Original architectural and engineering blueprints: identifies specialty components and building systems

- Certificate of occupancy: establishes the placed-in-service date

For properties held multiple years:

- Original purchase documents: establishes acquisition basis

- Current depreciation schedule: shows how the property has been depreciated to date

- Renovation and improvement records: documents capital improvements made during ownership

- Property tax records: helps verify values and ownership history

The IRS ATG explicitly recommends reviewing AIA Forms G-702 and G-703 to verify actual construction costs. Form G-702 summarizes overall payment requests. Form G-703 breaks down the contract sum into detailed portions of work, providing objective, third-party documentation that substantiates asset pricing.

A Qualified, IRS-Compliant Cost Segregation Study

With your documents in hand, the next requirement is a study that meets the quality standards outlined in the IRS Cost Segregation Audit Techniques Guide:

- Prepared by personnel with construction, engineering, and tax expertise

- Uses detailed engineering methodology, not "rule of thumb" approaches based on fixed percentages

- Includes a full asset schedule reconciled to total project cost

- Supported by legal analysis with proper citations for each asset classification

The IRS explicitly warns examiners to view rule-of-thumb approaches with caution, noting they lack sufficient documentation and rely on industry averages rather than actual project data. Seneca Cost Segregation's engineering-based methodology addresses this directly, with each study built from actual project data and backed by an AuditDefense guarantee.

A Qualified CPA or Tax Advisor

A quality study only produces results when applied correctly. Your CPA or tax professional needs hands-on experience with:

- Form 3115 mechanics and filing procedures

- MACRS depreciation rules and conventions

- Bonus depreciation elections and phase-down schedules

- Section 481(a) adjustment calculations

Cost segregation providers typically coordinate directly with your CPA to deliver reports in formats that make return filing straightforward.

Understanding Form 3115 and the Section 481(a) Catch-Up Deduction

Form 3115 is widely misunderstood, yet it's one of the most valuable tools in real estate taxation. It allows property owners who have been depreciating a building as a single 27.5- or 39-year asset to switch to the correct MACRS component method retroactively, without amending a single prior-year return.

The Legal Basis

The IRS treats cost segregation reclassification as a "change in accounting method" under Treasury Regulation §1.446-1, which is why Form 3115 is required rather than an amended return. This is an automatic change (DCN 7), meaning the IRS does not need to pre-approve it. You file the form with your current-year return and the change takes effect.

The Section 481(a) Adjustment

The adjustment represents the cumulative difference between depreciation you actually claimed in prior years and what you could have claimed with proper cost segregation from day one. That entire difference becomes a single lump-sum deduction in the year of change.

Per IRS guidance on accounting method changes, negative Section 481(a) adjustments are taken entirely in the year of change with no statutory look-back cap. The adjustment reaches back to the original placed-in-service date to prevent any omission or duplication of deductions.

What Happens Without Form 3115

Skipping Form 3115 isn't a workaround. It's a compliance failure. Reclassifying assets on an amended return alone is not permitted. Filing without it exposes you to:

- IRS adjustments reversing the claimed deductions

- Accuracy-related penalties on the underpayment

- Complete disallowance of the catch-up depreciation

Common Mistakes When Applying Cost Segregation on Your Tax Return

Using an Unqualified or "Rule of Thumb" Study

The IRS Cost Segregation Audit Techniques Guide specifically flags studies prepared without engineering expertise or without reconciliation to actual costs as high-risk. A study lacking proper documentation can fail audit scrutiny and trigger penalties under IRC §6662 for substantial understatement, specifically a 20% penalty on the underpayment amount. Working with a CCSP-certified firm that carries engineering credentials and audit defense protection reduces this exposure considerably.

Forgetting to File Form 3115 or Filing It Incorrectly

A costly error is simply updating depreciation schedules on an existing property without filing Form 3115, which constitutes an impermissible method change. Form 3115 has specific timing requirements:

- Must be attached to the timely filed original return for the year of change

- Duplicate must be sent to Ogden, UT

- Failure on either point can invalidate the method change

Failing to Coordinate Cost Segregation with Bonus Depreciation Elections

Many taxpayers and CPAs overlook the interaction between cost segregation and bonus depreciation. Reclassified 5-year and 15-year property may qualify for current-year bonus depreciation. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively. For qualified property with an acquisition date of January 19, 2025 or later, 100% bonus depreciation allows the entire basis of those assets to be deducted immediately, multiplying the immediate tax benefit.

Common coordination failures that forfeit these deductions include:

- Missing the bonus depreciation claim entirely on reclassified assets

- Making an inadvertent "election out" of bonus depreciation for an asset class

- CPAs and cost segregation providers working in silos rather than aligning on asset classifications

Reviewing the completed cost segregation study before filing is necessary to confirm proper bonus depreciation treatment is applied across every reclassified asset class.

Frequently Asked Questions

How do I apply cost segregation on my tax return?

For new properties, apply the study's reclassified asset schedule directly on Form 4562 in the year of acquisition. For existing properties, file Form 3115 with your current-year return to change your accounting method and claim all prior missed depreciation as a Section 481(a) catch-up deduction in a single year.

What is Form 3115 and is it required for cost segregation on my tax return?

Form 3115 is the IRS Application for Change in Accounting Method. It's required when applying cost segregation to a property already placed in service in a prior year, as it allows you to retroactively claim missed depreciation without amending prior returns.

What happens if I skip Form 3115 when doing a cost segregation study?

Form 3115 is required whenever assets on a property previously reported on prior tax returns are reclassified. Without it, the IRS considers any reclassification an impermissible method change, potentially disallowing all reclassified deductions and exposing you to accuracy-related penalties.

How far back can I do a cost segregation study?

There is no statutory limit—the Section 481(a) catch-up adjustment can go all the way back to the original placed-in-service date. In practice, most studies focus on the past 10-15 years, as assets held longer may have already been fully depreciated under the standard schedule.

Can I deduct the cost of a cost segregation study on my tax return?

Yes. The fee is generally deductible as an ordinary and necessary business expense under IRC §162 in the year it is paid. Treatment may vary depending on your entity structure.

What is the IRS stance on cost segregation studies?

The IRS recognizes cost segregation as a legitimate tax strategy, publishing a detailed Cost Segregation Audit Techniques Guide used by examiners. Studies must be prepared by qualified professionals using engineering-based methodology—the IRS scrutinizes quality closely and requires proper documentation to withstand audit review.