This guide walks through a real cost segregation study example from start to finish — the engineering analysis, the component breakdown, and the actual dollar savings on a concrete property. By the end, you'll know exactly what to expect from a study and whether it makes sense for your portfolio.

TL;DR

- A cost segregation study reclassifies building components into 5-, 7-, or 15-year depreciation categories instead of the standard 27.5 or 39 years

- Engineering analysis identifies flooring, fixtures, land improvements, and specialty systems, all eligible for accelerated depreciation

- On a $1M property, studies typically reclassify 20–40% of the building's cost, generating substantial first-year deductions

- 100% bonus depreciation is restored for property acquired after January 19, 2025; reclassified assets can be fully deducted in year one

- Studies take 2–4 weeks and must meet IRS Cost Segregation Audit Technique Guide standards to withstand audit scrutiny

What Is a Cost Segregation Study?

A cost segregation study is a tax analysis — typically conducted by engineers — that breaks down a property's purchase price or construction cost into individual components. Each component is assigned to the IRS depreciation class it legitimately belongs to.

By default, the IRS requires residential rental properties to depreciate over 27.5 years and commercial properties over 39 years. This treats everything from the roof to the carpet as a single long-lived asset, understating legitimate annual deductions for owners who qualify for faster schedules.

Cost segregation addresses this by identifying components that deteriorate more quickly than the building structure itself. Worth clarifying:

- Not a loophole: It's an IRS-recognized method documented in the agency's own Cost Segregation Audit Techniques Guide

- Not an audit trigger: Properly executed studies claim depreciation at the correct rate, not an inflated one

How a Cost Segregation Study Actually Works: The Key Stages

A cost segregation study follows a defined engineering and tax analysis sequence. Each stage contributes to the defensibility and accuracy of the final report.

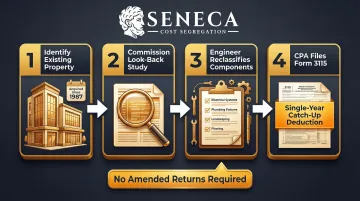

Property Review and Data Collection

The process begins with a property review, including purchase documents, blueprints, appraisals, and contractor invoices. Many firms conduct a physical site inspection to identify and photograph all building components.

The quality of this stage determines the depth of reclassification. A rigorous engineering inspection captures components that a surface-level review would miss entirely.

Asset Classification and Engineering Analysis

During the core analysis, a certified cost segregation specialist reviews each component and assigns it to the correct depreciation class:

| Depreciation Class | Examples |

|---|---|

| 5-year personal property | Appliances, Carpeting, Decorative lighting, Security systems |

| 15-year land improvements | Driveways, Fencing, Landscaping, Parking lots |

| 27.5/39-year structural real property | Roof, Walls, HVAC connected to the building, Plumbing |

Methodology quality directly affects both the size of deductions found and how well the study holds up under IRS scrutiny. Seneca Cost Segregation completes studies in 2–4 weeks (roughly half the industry standard of 4–8 weeks), using in-house engineering technology developed specifically for IRS compliance. Their team has assessed over 10,200 properties across all 50 states.

Report Preparation and IRS Compliance

Once the engineering analysis is complete, the findings are compiled into a formal report that must meet IRS standards. A compliant report includes:

- Asset classifications with documented justification for each

- Cost basis explanations for every reclassified component

- Full reconciliation of allocated costs against total actual costs

Anything missing from this structure creates audit exposure.

CPA Filing and Tax Return Integration

The report is delivered to the property owner and their CPA, who uses it to prepare the tax return. For properties already placed in service, the CPA files a Form 3115 (Change in Accounting Method) to claim retroactive deductions without amending prior returns, often recovering years of missed depreciation in a single filing.

A Real Cost Segregation Study Example: By the Numbers

Let's walk through a realistic property scenario to show exactly how value gets reclassified and what the tax impact looks like.

The Property Scenario

A real estate investor purchases a $1.2M multifamily rental property. The land is valued at $200,000 (non-depreciable), leaving a $1,000,000 depreciable basis.

Without a cost segregation study, this entire amount would be depreciated over 27.5 years at roughly $36,360 per year.

How the Study Reclassifies the Depreciable Basis

A cost segregation study breaks the $1,000,000 depreciable basis into categories:

- 15–20% identified as 5-year personal property ($150,000–$200,000)

- 8–10% as 15-year land improvements ($80,000–$100,000)

- Remaining 70–75% stays as 27.5-year structural real property

These ranges come from real-world studies; actual results vary by property type and condition.

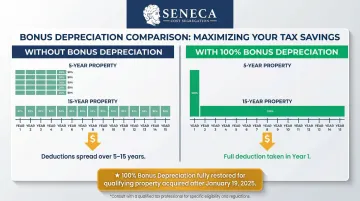

The Before vs. After Depreciation Comparison

| Method | Year-One Deduction | Tax Savings (32% Rate) |

|---|---|---|

| Standard (27.5-year) | $36,360 | ~$11,635 |

| With Cost Segregation | $250,000–$300,000 | $80,000–$96,000 |

With 100% bonus depreciation applied to qualifying reclassified assets, the year-one deduction could reach $250,000–$300,000.

The Tax Savings in Dollars

At a 32% federal tax rate, an additional $250,000 in year-one deductions reduces tax liability by approximately $80,000. That's capital available to reinvest in the next property, not locked up in a 27-year depreciation schedule.

That figure isn't hypothetical: Seneca's studies have delivered an average first-year deduction of $171,243 across more than 10,200 properties assessed nationwide.

Bonus Depreciation's Role in Maximizing Year-One Impact

Bonus depreciation is what makes reclassified short-life assets fully deductible in year one rather than over 5 or 15 years. The "One Big Beautiful Bill" (P.L. 119-21) restored 100% bonus depreciation for qualified property acquired after January 19, 2025. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline

| Acquisition / In-Service Period | Bonus Depreciation Rate |

|---|---|

| September 27, 2017 – December 31, 2022 | 100% |

| January 1, 2023 – December 31, 2023 | 80% |

| January 1, 2024 – December 31, 2024 | 60% |

| January 1, 2025 – January 18, 2025 | 40% |

| January 19, 2025 – December 31, 2030 (acquisition date January 19, 2025 or later) | 100% |

| Acquired before January 19, 2025, placed in service in 2025 | 40% |

| Acquired before January 19, 2025, placed in service in 2026 | 20% |

The difference in practice:

- Without bonus depreciation: Reclassified assets depreciate over 5 or 15 years (real savings, but spread out)

- With bonus depreciation: The entire reclassified amount hits your current year's return in full

What the Results Mean: Tax Savings in Practice

Cash Flow, Not Just Paper Savings

The tax savings from a cost segregation study are real cash flow. Reduced tax liability means more money available to reinvest in the next property, fund improvements, or pay down debt faster.

Most investors conflate this with simple deferral — but deferral misses the point. The time value of money means accessing $80,000 now versus over 27 years is a materially different financial outcome.

Depreciation Recapture: The Trade-Off to Understand

When the property is eventually sold, the IRS recaptures accelerated depreciation:

- Section 1245 assets (5/7-year): Taxed at ordinary income rates up to the amount of depreciation taken

- Section 1250 assets (15-year and structural): Capped at 25%

This is not a reason to avoid cost segregation, but depreciation recapture is a factor to account for in long-term planning. 1031 exchanges defer recapture indefinitely.

Look-Back Studies: Retroactive Savings for Existing Properties

Cost segregation is not only for new acquisitions. Property owners can conduct a "look-back" study on properties acquired, constructed, or renovated since 1987. By filing a Form 3115, they can claim all missed depreciation in the current tax year without amending returns.

For long-term holders who have been under-depreciating for years, this single filing can generate a large, immediate deduction, often matching or exceeding what a new acquisition would produce.

IRS Compliance and Audit Protection

A properly prepared, engineering-based cost segregation study is fully IRS-compliant. The IRS Audit Technique Guide directly addresses engineering-based methodology as the accepted standard. The risk isn't in doing a study; it's in using a low-quality one that can't withstand scrutiny.

Seneca's studies come with AuditDefense and a money-back guarantee. Every report is engineered to hold up under IRS examination, not just satisfy a checkbox.

Who Should Get a Cost Segregation Study — and When

Ideal candidates:

| Criterion | Detail |

|---|---|

| Depreciable basis | Property owners with a depreciable basis of $300,000 or more typically see the strongest ROI on study costs |

| Tax bracket | Investors in higher tax brackets (28%+) with income they need to offset |

| Property types | Covers residential rentals, multifamily, commercial, short-term rentals, and owner-occupied business properties |

Optimal timing:

| Priority | Scenario |

|---|---|

| Best | The same year a property is placed in service (purchased or construction completed), so the full year-one bonus depreciation benefit is captured |

| Second best | A look-back study on existing properties during a high-income year when larger deductions are most valuable |

Studies for properties already owned can be done retroactively without amending prior returns.

Provider matters: Working with a specialized, certified provider affects both the size of the benefit and audit risk. Firms with CCSP-certified specialists and an engineering-based methodology identify more reclassifiable assets and produce reports that hold up under IRS scrutiny. Seneca Cost Segregation, for example, has completed studies on over 10,200 properties nationwide using this approach — something a CPA without engineering training typically cannot replicate.

Frequently Asked Questions

What is an example of a cost segregation study?

A property's depreciable basis is broken into components (5-year, 15-year, structural). The reclassified short-life assets generate significantly larger first-year deductions than standard straight-line depreciation. On a $1M property, 20–40% typically gets reclassified. Seneca Cost Segregation clients average $171,243 in first-year deductions.

How is cost segregation calculated?

A certified engineer reviews blueprints, invoices, and the physical property to identify each component. They assign it an IRS-defined depreciation class and allocate a portion of the total cost basis to each class. The total must reconcile with the actual purchase price, which is what makes the study defensible in an IRS audit.

What property types qualify for cost segregation?

Most income-producing real estate qualifies — residential rentals, multifamily, commercial buildings, hotels, retail, warehouses, and short-term rentals. Owner-occupied business properties also qualify. The strategy applies to both new construction and existing properties.

What is the typical cost of a cost segregation study?

Fees typically range from $2,000–$5,000 for residential properties and $5,000–$15,000+ for larger commercial assets, depending on size and complexity. Most investors recover the study fee many times over. Seneca clients average $171,243 in first-year tax deductions.

How do I report cost segregation on my tax return?

The cost segregation report is used by a CPA to populate depreciation schedules on the tax return. For properties already owned, a Form 3115 (change in accounting method) is filed with the return to claim all prior-year catch-up depreciation in a single year without amending past returns.

Can I write off the cost of a cost segregation study?

Yes, the fee paid for a cost segregation study is generally deductible as a business expense. A CPA can confirm the applicability based on specific tax circumstances.