Introduction

A 1031 exchange is a tax-deferral strategy under IRC Section 1031 that lets real estate investors reinvest sale proceeds into like-kind property without immediately paying capital gains tax. For active investors, the cost of skipping it is steep. Capital gains tax combined with depreciation recapture can consume 30%–40% of your profit on a sale. In high-tax states like California, effective rates can reach 42%.

What follows covers how the 1031 exchange works, the rules that govern it, the types available, and the mistakes that cause exchanges to fail — so you keep more capital working across every transaction.

TL;DR

- A 1031 exchange defers capital gains and depreciation recapture taxes by reinvesting sale proceeds into a qualifying replacement property

- You have 45 days to identify a replacement property and 180 days to close; missing either deadline by even one day voids the exchange

- All proceeds must be held by a Qualified Intermediary (QI) — touching the money at any point invalidates the exchange

- To defer all taxes, the replacement property must match or exceed both the value and debt of the relinquished property — any shortfall becomes taxable "boot"

- Investors who exchange throughout their lifetime can eliminate deferred tax liability through stepped-up basis at death

What Is a 1031 Exchange?

Section 1031 of the Internal Revenue Code allows investors who sell investment or business property to defer all capital gains and depreciation recapture taxes by rolling proceeds into a "like-kind" replacement property. The mechanism defers taxes rather than eliminating them, letting you reinvest 100% of your pre-tax proceeds and grow equity without cutting a check to the IRS first.

Following the Tax Cuts and Jobs Act (TCJA) of 2017, Section 1031 is strictly limited to real property. Personal property, equipment, and partnership interests no longer qualify.

Understanding "Like-Kind"

"Like-kind" is broader than most investors assume. Under Treasury Regulation §1.1031(a)-1, it refers to the nature and character of the property—investment or business use—not type, quality, or geography.

Qualifying like-kind exchanges:

- Single-family rental → Commercial warehouse

- Vacant land → Multi-family apartment building

- Office building → Retail shopping center

What does NOT qualify:

- Primary residences (personal use)

- Dealer/flip inventory (held for sale, not investment)

- Foreign property exchanged for U.S. property

- Partnership interests

How It Differs From a Standard Sale

| Standard Sale | 1031 Exchange | |

|---|---|---|

| Tax timing | Due in year of sale | Deferred until future sale |

| Basis in new property | Full fair market value | Carries over (lower adjusted basis) |

| Death of owner | Gain may be recognized | Gain eliminated via stepped-up basis |

The deferred gain carries forward into the replacement property's adjusted basis. If the property passes to heirs, stepped-up basis at death can eliminate the accumulated gain entirely.

Why Real Estate Investors Use 1031 Exchanges

Capital Preservation Through Deferral

The core benefit is simple: by reinvesting the full sale proceeds rather than after-tax proceeds, you deploy significantly more capital into your next acquisition. Without a 1031 exchange, selling highly appreciated, depreciated property triggers:

- Federal long-term capital gains tax: 0%, 15%, or 20%

- Net Investment Income Tax (NIIT): 3.8% for high earners

- Depreciation recapture under Section 1250: up to 25%

- State taxes: up to 13.3% in California

Tax Scenario (High-Income Investor):

| Tax Type | Federal Rate | State Tax (CA) | Total |

|---|---|---|---|

| Pure Capital Gain | 23.8% | 13.3% | 37.1% |

| Depreciation Recapture | 28.8% | 13.3% | 42.1% |

A 1031 exchange prevents this 37–42% capital erosion.

Portfolio Scaling: Trading Up Without Tax Drag

Investors use 1031 exchanges to "trade up" from smaller properties into higher-value, higher-income assets without liquidating equity to pay taxes. The Joint Committee on Taxation estimated that $9.9 billion in tax revenue was deferred in 2019 due to like-kind exchanges. The Federation of Exchange Accommodators estimates roughly $100 billion worth of real estate assets were exchanged that same year.

The Estate Planning Advantage: "Defer, Defer, Die"

When an investor holds 1031 exchange property until death, IRC Section 1014 provides a stepped-up basis. Heirs receive the property with a tax basis equal to its fair market value at the date of death, effectively eliminating the accumulated deferred gain entirely.

Example:

- Original property purchased: $300,000

- Exchanged into Property B: $600,000

- Exchanged into Property C: $1,200,000

- Fair market value at death: $1,500,000

- Heirs' basis: $1,500,000 (all deferred gains eliminated)

Tax-Stacking Strategy: Pairing 1031 With Cost Segregation

Pairing a 1031 exchange with a cost segregation study on the replacement property compounds the tax benefit: defer capital gains from the sale while simultaneously generating accelerated depreciation deductions on the new property.

Only the "new" cash invested above the exchanged equity is eligible for a fresh cost segregation study on the replacement property. For investors completing a 1031 exchange, this makes the timing and scope of the cost segregation study a key planning decision — one where an engineering-based study, like those Seneca Cost Segregation performs on replacement properties, has averaged a first-year deduction of $171,243 across more than 10,200 properties assessed nationwide.

Risks and Trade-Offs

- Timeline pressure: 45 and 180-day deadlines can force suboptimal replacement property selection

- Reduced basis: Deferred gain carries forward as a lower adjusted basis, reducing future depreciation deductions

- Illiquidity: Proceeds cannot be accessed mid-process without disqualifying the exchange

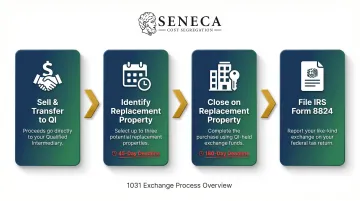

How a 1031 Exchange Works

Here's the high-level flow before we break down each step:

- Sell the relinquished property and transfer proceeds directly to a Qualified Intermediary (QI)

- Identify replacement property in writing within 45 days of closing

- Close on the replacement property within 180 days

- File IRS Form 8824 with your tax return for the exchange year

The QI holds and disburses funds throughout—the investor never touches the proceeds.

Step 1: Engage a Qualified Intermediary Before Closing

The QI must be engaged before the relinquished property closes—not after—because funds must flow directly from closing to the QI without touching your account. Any actual or constructive receipt of exchange funds disqualifies the entire exchange.

QI disqualification rules: Your QI cannot be your attorney, accountant, real estate agent, or anyone who acted as your agent in the two-year period ending on the transfer date.

Selecting a QI:

- Segregated client accounts

- Fidelity bonds and errors & omissions insurance

- Demonstrated real estate transaction experience

- References from other investors

Step 2: Close the Sale and Start the Clock

The 180-day exchange period and 45-day identification window both start on the closing date of the relinquished property. The 180 days is not in addition to the 45 days—they run concurrently.

Critical: If day 45 or day 180 falls on a weekend or federal holiday, the deadline does not shift. These are absolute calendar days.

Step 3: Identify Replacement Property Within 45 Days

Identification must be in writing, signed, and delivered to the QI or another party involved in the exchange—not to your own attorney or agent. Investors who wait until day 40+ leave themselves very little time to negotiate and close.

You must comply with one of three identification rules:

- Three-Property Rule: Cap at 3 properties regardless of value — the simplest approach for most single-asset exchanges

- 200% Rule: No limit on property count, but combined FMV cannot exceed 200% of the relinquished property's value — useful for portfolio-style exchanges

- 95% Exception: Identify unlimited properties at any value, but you must close on at least 95% of the aggregate identified value — rarely used due to its strict closing requirement

Step 4: Close on the Replacement Property Within 180 Days

The QI disburses held funds directly to purchase the replacement property at closing—the investor never takes direct receipt of proceeds. The exchange isn't fully complete until the tax reporting is filed.

IRS Form 8824 must be filed with your tax return for the year the exchange occurred, reporting the deferred gain, adjusted basis, and exchange details.

The Rules That Determine Whether Your Exchange Succeeds

The Three Identification Rules

Treasury Regulation §1.1031(k)-1(c) establishes three identification methods:

| Rule | How It Works | Best For |

|---|---|---|

| Three-Property Rule | Identify up to 3 properties of any value | Standard exchanges with a few targets |

| 200% Rule | Identify unlimited properties with combined FMV ≤ 200% of relinquished property value | Diversifying into multiple lower-cost properties |

| 95% Exception | Identify unlimited properties at any value, but must close on ≥ 95% of aggregate identified value | High-risk fallback if first two rules breached |

Equal-or-Greater-Value and Debt Replacement Requirements

To achieve full deferral, replacement property must equal or exceed both the sale price and the outstanding debt of the relinquished property. Debt can be offset with additional cash, but cash cannot substitute for debt in the other direction.

Understanding "Boot" and Why It's Taxable

Boot is any non-like-kind value received in the exchange, taxable to the extent of your realized gain:

Types of boot:

- Cash boot: Proceeds not reinvested into the replacement property

- Mortgage boot: Taking on less debt than you carried on the relinquished property

- Personal property boot: Furniture or appliances bundled into the sale

Mortgage boot example:

- Relinquished property debt: $500,000

- Replacement property debt: $400,000

- Mortgage boot: $100,000 (taxable unless you add $100,000 cash)

Hidden boot traps:

- Prorated property taxes paid from QI funds

- HOA adjustments

- Repair credits

- Loan payoff fees paid from exchange funds

Boot is only one way exchanges fail. Ownership structure is another — and it's easier to overlook than you might expect.

Taxpayer Identity Rule

The entity that sells the relinquished property must be identical to the entity that purchases the replacement property. Selling as an LLC and buying as an individual — or the reverse — disqualifies the exchange entirely.

Holding Intent Requirement

Both properties must be held for investment or productive business use — not personal use or immediate resale. The IRS scrutinizes any property converted to personal use after closing.

Key holding intent guidelines:

- No formal minimum holding period exists under Section 1031

- Two years is the IRS's practical benchmark — conversions before that trigger close scrutiny

- Flip strategies (buying to resell quickly) do not qualify; intent matters as much as actual hold time

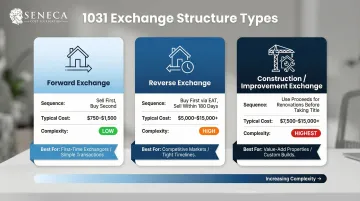

Types of 1031 Exchanges

Each 1031 exchange follows one of three structural paths. Which one fits your situation depends on timing, market conditions, and how much renovation you plan to complete on the replacement property.

Forward (Standard) Exchange

The most common structure: sell the relinquished property first, then identify and acquire the replacement property within the 45/180-day windows. Most investors start here because the transaction sequence matches how deals naturally flow.

Typical cost: $750–$1,500

Reverse Exchange

Used when you find a specific replacement property before selling the relinquished property. An Exchange Accommodation Titleholder (EAT) takes temporary title to the new property while you sell the old one, still within 180 days.

When to use: Competitive markets where you can't risk losing the replacement property Typical cost: $5,000–$15,000+

Construction/Improvement Exchange

Allows you to use exchange proceeds to complete renovations or ground-up builds on the replacement property before taking title, with the EAT holding title during construction.

Any improvements not finished within the 180-day window lose their tax-deferred treatment — so construction timelines need to be locked in before the exchange begins.

When to use: Value-add investors seeking to improve replacement property Typical cost: $7,500–$15,000+

Common Mistakes and When a 1031 Exchange May Not Be the Right Move

Exchange-Killing Mistakes

Most common failures:

- Touching the money: Any direct receipt of funds by the investor disqualifies the entire exchange

- Missing the 45-day deadline by even one day

- Taxpayer name mismatch between selling and buying entity

- Failing the 95% rule when exceeding the 200% threshold

While some marketing materials claim a 30% failure rate, the National Association of Realtors estimates 8–10% of exchanges fail to complete— most often due to missing the 45-day identification window or failing to secure financing.

When a 1031 Exchange May Not Be the Right Tool

Consider alternatives when:

- You're exiting real estate entirely and prefer an installment sale to spread tax recognition

- You cannot realistically find qualifying replacement property within 45 days in a tight market

- Your deferred gain is small relative to the cost and complexity of coordinating an exchange

- You want passive income without active management — a Delaware Statutory Trust (DST) may be the better fit

Depreciation Recapture in 1031 Exchanges

A failed or mishandled exchange doesn't just cost you the tax deferral — it can trigger depreciation recapture you were counting on avoiding.

In a properly structured exchange, depreciation recapture (taxed at 25% under Section 1250) is deferred and carries into the replacement property's lower basis. Recapture becomes due if:

- The exchange fails

- You receive boot

- You enter a DST (which creates a recapture event)

If you completed a cost segregation study on the relinquished property, flag this with your CPA and qualified intermediary before closing. Reclassified components under Section 1245 carry their own recapture rate and must be accounted for separately in the exchange structure.

Conclusion

A 1031 exchange is a legal, IRS-sanctioned mechanism to defer capital gains and depreciation recapture taxes, compound wealth across transactions, and—with careful long-term planning—eliminate deferred taxes entirely for heirs. The strategy allows you to trade from one investment property into another without immediately paying federal or state taxes on the gain.

The rules, however, are unforgiving. To recap the non-negotiables:

- Start planning before you list the relinquished property—not after going under contract

- Identify replacement properties within 45 days of closing the sale

- Close on the replacement within 180 days total

- Work with a qualified intermediary from the start; you cannot touch the proceeds

Miss any of these deadlines, and the full tax bill comes due immediately.

Once you close on the replacement property, one additional move can amplify your tax position: a cost segregation study. Investors who acquire replacement properties through a 1031 exchange can accelerate depreciation on the "new" cash invested above the exchanged equity—generating substantial first-year deductions on top of the deferral already achieved.

Seneca Cost Segregation has completed over 10,200 engineering-based studies nationwide, with an average first-year deduction of $171,243. If you want to see what that looks like for your replacement property, request a free assessment from Seneca.

Frequently Asked Questions

What are the 1031 exchange identification rules (three-property, 200% and 95% rules)?

Investors must choose one of three identification methods: the Three-Property Rule (up to 3 properties of any value), the 200% Rule (unlimited properties with combined FMV not exceeding 200% of relinquished property value), or the 95% Exception (unlimited properties at any value, but must close on at least 95% of total identified value). Most investors use the Three-Property Rule for simplicity.

What is "boot" in a 1031 exchange and how do I avoid it?

Boot is any non-like-kind value received during the exchange—cash proceeds, debt reduction, or personal property. To avoid it, the replacement property must equal or exceed the sale price and carry equal or greater debt; cover any equity shortfall with additional cash.

Can I do a 1031 exchange on a short-term rental property?

Yes, provided the property is held for investment or business use rather than personal use. Revenue Procedure 2008-16's safe harbor requires fair-market-rate rental for at least 14 days per year, with personal use capped at the greater of 14 days or 10% of rental days. Document rental activity carefully—the IRS scrutinizes vacation properties.

How does a 1031 exchange affect depreciation recapture?

Depreciation recapture (taxed at 25% for Section 1250 property) is deferred along with capital gains in a valid 1031 exchange and carries forward into the replacement property's adjusted basis. If the exchange fails or boot is received, recapture becomes taxable in the year of the exchange.

What happens if I miss the 45-day or 180-day deadline?

The exchange fails entirely, the QI returns the funds to the investor, and capital gains and depreciation recapture taxes become due for that tax year. No extensions are granted except in presidentially declared disasters—start identifying replacement properties well before day 45 to protect your exchange.

Can I combine a cost segregation study with a replacement property acquired in a 1031 exchange?

Yes—a cost segregation study on a 1031 replacement property lets you stack accelerated depreciation on top of your deferred capital gain. Note that only the incremental "new" cash invested above the exchanged equity qualifies for first-year bonus depreciation.