Introduction

Selling appreciated real estate can trigger significant capital gains taxes—often 20% at the federal level, plus an additional 3.8% Net Investment Income Tax for high earners, and up to 25% in depreciation recapture taxes on investment properties. For a property with $500,000 in gains, that's potentially $119,000 owed to the IRS.

Capital gains tax applies to the profit you make when selling property for more than you paid (adjusted for improvements and depreciation). Deferring these taxes is one of the most powerful wealth-building strategies available to real estate investors. It lets you reinvest the full proceeds rather than losing a substantial portion to taxes upfront.

This article covers the primary deferral strategies, what each one requires, and the most common mistakes that can wipe out the benefit entirely.

TL;DR

- Tax deferral delays capital gains taxes on real estate sales, letting you reinvest full proceeds instead of paying the IRS right away

- The 1031 exchange is the primary tool for investment properties, with strict 45-day and 180-day deadlines that allow no exceptions

- Installment sales, Charitable Remainder Trusts, primary residence exclusions, and step-up in basis are additional deferral options

- Eligibility and timing are critical—errors in either eliminate the benefit completely

- Pairing a 1031 exchange with cost segregation on the replacement property compounds your tax savings further

Tax Deferral Strategies for a Real Estate Sale: Know Your Options

Not all deferral strategies work for all property types. The right approach depends on whether you're selling a primary residence, investment property, or second home. This section maps out five core options before diving into execution details.

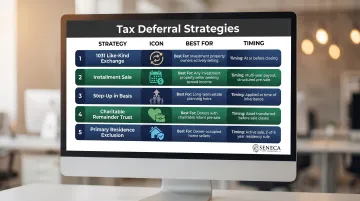

| Strategy | Best For | Timing |

|---|---|---|

| 1031 Like-Kind Exchange | Investment/business property | Active sale |

| Installment Sale | Any investment property | Multi-year income planning |

| Step-Up in Basis | Any property | Long-term estate planning |

| Charitable Remainder Trust | Appreciated property, charitable intent | Pre-sale planning |

| Primary Residence Exclusion | Owner-occupied home | Active sale |

1031 Like-Kind Exchange

A 1031 exchange (IRC Section 1031) allows investors to defer capital gains taxes by reinvesting sale proceeds from one investment property into a "like-kind" replacement property. According to the Tax Cuts and Jobs Act, Section 1031 now applies only to exchanges of real property, not personal or intangible property.

Critical limitation: This applies only to investment or business properties—not primary residences.

Installment Sale

An installment sale spreads payments—and the resulting capital gains—across multiple years, which can keep you in a lower tax bracket each year. You report a percentage of each payment as income, calculated by dividing gross profit by the contract price.

Warning: The IRS has placed "monetized installment sales" on its annual Dirty Dozen list of abusive tax schemes. Any structure offering upfront cash via non-recourse loans tied to installment notes faces aggressive IRS scrutiny.

Step-Up in Basis for Heirs

When a property owner passes away, heirs receive a stepped-up basis equal to fair market value at the time of death, wiping out accrued capital gains. The Joint Committee on Taxation estimates $379.3 billion in foregone revenue from this provision between 2025 and 2029.

Note: This works best as part of a longer-term estate plan—it doesn't help investors looking to sell in the near term.

Charitable Remainder Trust (CRT)

Donating appreciated property to a CRT allows the trust to sell the property without triggering immediate capital gains. You receive an income stream for a set period, a partial charitable deduction, and the remainder passes to charity. The remainder to charity must be at least 10% of the initial property value.

Primary Residence Exclusion (for Homeowners)

Homeowners who have lived in the property as their primary residence for at least 2 of the last 5 years can exclude up to $250,000 of gain ($500,000 for married couples) when filing jointly.

Worth noting: This is an exclusion, not a deferral—but it's the most accessible option for non-investor homeowners.

How to Execute a 1031 Exchange Step by Step

The 1031 exchange is the dominant deferral strategy for real estate investors, but even small procedural errors disqualify the entire exchange. According to economic impact analysis, 1031 exchanges supported $7.5 billion in business investment and employed nearly 976,000 workers in 2021 alone.

That scale reflects how many investors rely on this tool — and how costly a procedural misstep can be. Follow each step exactly.

Step 1: Confirm Eligibility of the Relinquished Property

The property must be held for investment or business purposes, not personal use. Real property (land and buildings) qualifies; stocks, inventory, and partnership interests do not.

Before closing, also calculate your adjusted cost basis: original purchase price + improvements − depreciation claimed. This figure tells you your full taxable gain at stake — and what you stand to defer.

Step 2: Engage a Qualified Intermediary (QI) Before Closing

A QI must be in place before the sale closes — you cannot touch the proceeds at any point. The QI holds funds in escrow and facilitates the entire exchange on your behalf.

The QI must also be genuinely independent: no financial relationship with you within the past two years. That disqualifies your attorney, accountant, broker, or any family member.

Step 3: Identify the Replacement Property Within 45 Days

The clock starts the day your relinquished property closes. Within 45 days, you must formally identify potential replacement properties in writing to the QI.

Most U.S. real estate qualifies as like-kind to other U.S. real estate — type doesn't matter. You can exchange an apartment building for commercial property, raw land for a warehouse, or a strip mall for a mixed-use building. U.S. property is not like-kind to foreign property.

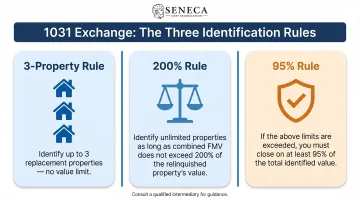

Identification rules:

- 3-Property Rule: Identify up to 3 properties without value limits

- 200% Rule: Identify any number of properties if their total value doesn't exceed 200% of the relinquished property value

- 95% Rule: If you exceed the above, you must close on properties representing at least 95% of total identified value

Step 4: Close on the Replacement Property Within 180 Days

The replacement property purchase must close within 180 days of the original sale—not 180 days from identification. Both deadlines are absolute with no extensions except federally declared disasters.

To defer 100% of your gain, the replacement property must be of equal or greater value. If you receive any cash or take on less debt — known as "boot" — that difference becomes immediately taxable.

Pairing a 1031 exchange with a cost segregation study on the replacement property compounds the advantage further. A Seneca Cost Segregation study averages $171,243 in first-year deductions on the new asset, turning a deferral strategy into an immediate offset.

What You Need Before Deferring Taxes on a Real Estate Sale

Preparation before the sale closes is non-negotiable. Most disqualifying errors happen before the exchange formally begins.

Property and Ownership Requirements

Before moving forward, confirm two things:

- Holding period: The property must have been held for investment or business use—not recently converted from personal use. Pull rental income history to document business purpose.

- Adjusted cost basis: Include all improvement costs and prior depreciation deductions. This number drives both your taxable gain calculation and your replacement property value requirements.

Professional Team Requirements

Assemble these key professionals:

- Qualified Intermediary (mandatory for 1031): Must be an independent third party with no prior service relationship to you

- CPA or tax advisor: Must have real estate capital gains expertise

- Real estate attorney: Optional, but worth it for complex or high-value transactions

Critical warning: Using an unqualified intermediary or attempting to hold proceeds personally invalidates the exchange entirely.

Financial Threshold Awareness

Not every transaction justifies the professional fees involved. Use these thresholds as a starting point:

- Cost segregation studies: Generally worthwhile when the building basis (excluding land) is $300,000 or more

- 1031 exchanges: Professional costs are typically justified when deferred gains exceed $100,000

- Smaller transactions: May still qualify if depreciation recapture exposure is significant

Before committing, add up QI fees, legal review costs, and any cost segregation study expenses—then weigh that total against your projected tax deferral to confirm the math works in your favor.

Key Variables That Affect Your Tax Deferral Outcome

Even investors who follow the 1031 rules correctly can lose a significant portion of their deferral benefit to variables they didn't plan for. Four factors in particular determine how much tax you actually defer — and how long that deferral holds.

Depreciation Recapture

Any depreciation deductions taken during your holding period are "recaptured" by the IRS upon sale and taxed at up to 25%—separate from capital gains tax. This applies even in a 1031 exchange if the replacement property is of lesser value.

Running a cost segregation study on your replacement property can offset this exposure by front-loading new depreciation deductions — creating paper losses that counterbalance the recaptured income. Seneca Cost Segregation's average client achieves first-year deductions of $171,243, which can substantially reduce net recapture liability.

Boot Received

"Boot" is any cash received or debt reduction resulting from an unequal exchange. The IRS taxes boot immediately, even in an otherwise valid 1031 exchange.

Example: If you sell a property with a $400,000 mortgage and buy a replacement property with a $350,000 mortgage, the $50,000 debt reduction is taxable boot—unless you contribute $50,000 cash to make up the difference.

Holding Period of the Replacement Property

The replacement property must generally be held as an investment. Selling it quickly after acquisition or converting it to personal use raises IRS scrutiny and can retroactively invalidate your deferral.

No statutory minimum holding period exists, but tax professionals recommend holding replacement property for at least two years to demonstrate investment intent. Two practical rules of thumb:

- File at least two tax returns showing the property as an investment asset

- Avoid converting it to personal use (such as a primary residence) during that window

State and Local Tax Exposure

Capital gains tax deferral under a 1031 exchange applies at the federal level, but some states do not conform to federal 1031 rules:

| State | Conformity Status |

|---|---|

| California | Conforms but requires annual reporting (Form FTB 3840) until deferred gain is recognized |

| Oregon | Enforces clawback tax when out-of-state replacement property is sold (Form OR-24) |

| Montana | Enforces clawback on Montana-source gains when recognized |

| Massachusetts | Enforces clawback unless transferor consents to MA jurisdiction |

Action required: Confirm your state's treatment before proceeding to avoid unexpected tax bills years later.

Common Mistakes When Deferring Taxes on a Real Estate Sale

1031 exchanges fail more often than most investors expect. The rules are strict, the deadlines are absolute, and the IRS offers almost no room for procedural errors.

Missing the 45-Day or 180-Day Deadlines

These deadlines are absolute. No extensions are granted except in federally declared disaster areas. A single day's delay nullifies the exchange and triggers full capital gains tax liability.

Best practice: Work backward from the closing date to ensure timelines are feasible before listing the property. Consider market conditions that could delay replacement property closings.

Taking Constructive Receipt of Sale Proceeds

"Constructive receipt" means any scenario where you have control over, access to, or benefit from sale proceeds before the QI transfers them to the replacement property purchase. This immediately disqualifies the deferral.

Common violations:

- Depositing proceeds in your personal or business account, even temporarily

- Having signatory authority over the QI escrow account

- Receiving proceeds to pay off personal debts

Choosing a Disqualified Intermediary or Skipping One Entirely

Using a "related party" as a QI violates IRS rules—this includes family members, personal attorneys, or regular accountants who have provided services within the past two years.

Some investors attempt the exchange without a QI entirely, believing it's optional. It is not. The QI is a mandatory requirement under Treasury Regulations — skipping one disqualifies the exchange outright.

Frequently Asked Questions

How to defer taxes when selling a home?

Homeowners who have lived in the property as their primary residence for 2 of the last 5 years may qualify for the $250,000/$500,000 capital gains exclusion. Investment property owners should look at a 1031 exchange or installment sale; these strategies work best for investors reinvesting into similar properties.

Is property tax deferral a good idea?

Deferral is generally beneficial when you plan to keep reinvesting in real estate, letting you build wealth with untaxed dollars. Investors who need liquidity or are exiting real estate entirely may be better served by other strategies or simply paying the tax upfront.

What is the 45-day rule in a 1031 exchange?

You have exactly 45 days from the closing date of the relinquished property to formally identify up to three potential replacement properties in writing to your Qualified Intermediary. Missing this deadline by even one day cancels the entire exchange and triggers full tax liability.

What is "boot" in a 1031 exchange and how does it affect my taxes?

Boot is any cash received or net debt reduction in an exchange, and it is taxable in the year of the exchange even if the rest of the transaction qualifies for deferral. To avoid boot, ensure your replacement property's value and debt level match or exceed the relinquished property.

Can I do a 1031 exchange on my primary residence?

No. Primary residences do not qualify for a 1031 exchange since the property must be held for investment or business purposes. However, homeowners may qualify for the $250,000/$500,000 capital gains exclusion instead if they meet the 2-of-5-year use requirement.

What happens to deferred taxes if I never sell the replacement property?

Deferred gains follow the property indefinitely through successive 1031 exchanges. When heirs inherit the property at your death, the stepped-up basis may eliminate the deferred tax liability entirely, as they inherit at current market value with no tax on the accumulated appreciation.