Introduction

Many rental property owners are caught off guard at closing when they face a larger-than-expected tax bill — sometimes tens of thousands of dollars more than anticipated. The culprit is depreciation recapture: the IRS's method of reclaiming the tax benefit you received from depreciation by taxing that portion of your gain at a higher rate than standard capital gains when you sell.

This applies to any landlord or real estate investor who claimed — or was eligible to claim — depreciation on rental property. Even if you never took the deduction, the IRS still reduces your cost basis by the allowable amount, triggering recapture tax liability upon sale.

This article breaks down what depreciation recapture is, how it's calculated, which tax rates apply, and the strategies investors use to minimize or defer it.

TL;DR

- Depreciation recapture is triggered when you sell rental property for more than its adjusted cost basis

- For residential rentals, recaptured amounts are taxed at a maximum 25% rate, not standard capital gains rates

- The IRS assumes you claimed depreciation whether you did or not — skipping deductions doesn't avoid recapture

- A 1031 exchange, holding until death, or donating to charity are the most common deferral strategies

- Higher-income investors may owe an additional 3.8% Net Investment Income Tax (NIIT) on top of recapture tax

What Is Depreciation Recapture on Rental Property?

Every year you own a rental property, the IRS lets you deduct a portion of the building's value as depreciation — spreading the structure's cost over 27.5 years under MACRS. That deduction reduces your taxable income while you hold the property, but it also lowers your adjusted cost basis.

When you sell, the IRS wants some of that benefit back. Depreciation recapture isn't a new tax on your profit — it's a reclassification of how part of your gain is taxed, at a higher rate than standard long-term capital gains.

Two Types of Gain at Sale

When you sell rental property, the IRS splits your gain into two components:

- Unrecaptured Section 1250 gain — The portion up to total accumulated depreciation, taxed at a maximum of 25%

- Capital gain above that — Taxed at long-term capital gains rates (0%, 15%, or 20% depending on income)

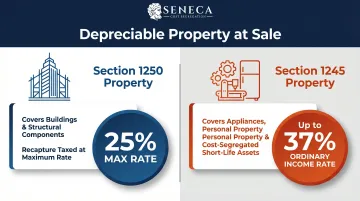

Section 1245 vs. Section 1250 Property

Not all depreciable property is taxed the same way at sale:

| Property Type | What It Covers | Recapture Tax Rate |

|---|---|---|

| Section 1250 | Buildings and structural components | Maximum 25% |

| Section 1245 | Appliances, personal property, short-life cost-segregated assets (5-, 7-, 15-year) | Ordinary income rates, up to 37% |

Investors who complete a cost segregation study and claim bonus depreciation on short-life components should be aware that those assets carry Section 1245 recapture rules, making pre-sale planning essential to avoid surprise tax bills at closing. Seneca Cost Segregation works with investors to map out exactly how accelerated depreciation affects recapture exposure before a sale — so there are no surprises when the deal closes.

Land Is Never Recaptured

Land is never depreciated and therefore never subject to recapture. Only the depreciable building and improvements contribute to recapture calculations.

How Depreciation Recapture Is Calculated Step by Step

The recapture amount equals total accumulated depreciation claimed — or allowable — during ownership. For rental real property, this becomes unrecaptured Section 1250 gain taxed at up to 25%, capped at your total gain on the sale.

One critical rule shapes every calculation: the IRS reduces your adjusted basis by the full amount of depreciation you were entitled to claim, not just what you actually claimed. Skipping deductions doesn't reduce your recapture liability — it only lowers your cost basis and increases your taxable gain.

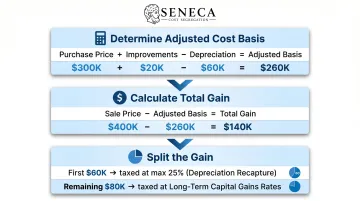

Step 1: Determine Your Adjusted Cost Basis

Adjusted cost basis is calculated as:

Original purchase price (including closing costs attributable to the building) + capital improvements − accumulated depreciation

Example: You purchased a rental property for $300,000, invested $20,000 in capital improvements, and claimed (or were eligible to claim) $60,000 in depreciation over 10 years.

Adjusted basis = $300,000 + $20,000 − $60,000 = $260,000

Step 2: Calculate Your Total Gain

Total gain = Sale price − adjusted cost basis

If the sale price is below adjusted cost basis, there is no gain and therefore no recapture.

Selling that same property for $400,000 produces:

Total gain = $400,000 − $260,000 = $140,000

Step 3: Identify and Tax the Recapture Amount

The $140,000 gain is split:

- First $60,000 (equal to total accumulated depreciation) = unrecaptured Section 1250 gain taxed at a maximum 25% rate

- Remaining $80,000 above accumulated depreciation = taxed at long-term capital gains rates

If the entire gain is less than total accumulated depreciation (e.g., gain of $40,000 when depreciation was $60,000), the entire gain is taxed as unrecaptured Section 1250 gain.

Net Investment Income Tax (NIIT)

Recapture tax isn't the only liability to factor in. Higher-income investors may also owe the 3.8% Net Investment Income Tax (NIIT) on the full gain amount, depending on Modified Adjusted Gross Income (MAGI).

| Filing Status | MAGI Threshold |

|---|---|

| Single or head of household | $200,000 |

| Married filing jointly | $250,000 |

| Married filing separately | $125,000 |

These thresholds aren't adjusted for inflation, so more investors cross the NIIT threshold each year.

Strategies to Minimize or Defer Depreciation Recapture

1031 Like-Kind Exchange

The 1031 like-kind exchange is the most widely used deferral tool. When you sell a rental property and reinvest proceeds into another qualifying like-kind property, both capital gains and recapture taxes are deferred.

Strict timelines apply:

- Identify replacement property within 45 days of sale

- Close on replacement property within 180 days of sale

Important: This strategy only defers taxes, it doesn't eliminate them — unless the investor continues exchanging or passes the property to heirs.

Step-Up in Basis at Death

Holding the property until death triggers a basis step-up to fair market value at the date of death under IRC §1014. This eliminates accumulated depreciation and wipes out both recapture and capital gains for heirs.

For investors who've used cost segregation aggressively or held property for decades, the accumulated depreciation erased can run into six or seven figures — making this one of the most valuable estate planning tools available.

Charitable Giving

Donating the property to a qualified charity or donor-advised fund allows the owner to avoid depreciation recapture entirely, while potentially claiming a charitable deduction equal to the property's fair market value (subject to AGI limits of typically 30%).

Note: Under IRC §170(e)(1)(A), the deduction must be reduced by any amount that would have been ordinary income had the property been sold — meaning Section 1245 recapture reduces your deduction dollar-for-dollar. Straight-line depreciation and a holding period exceeding one year are also required.

Tax-Loss Harvesting

Selling a losing investment in the same tax year can reduce overall capital gains, but it does not directly offset the ordinary income portion of Section 1245 recapture — so coordinate this with a tax advisor before assuming it solves the recapture problem.

Qualified Opportunity Fund (QOF)

Investing capital gains proceeds in a Qualified Opportunity Fund within 180 days can defer capital gains. Before pursuing this route, understand the key limitations:

- QOFs do not defer the recapture portion of the gain — only capital gains above accumulated depreciation qualify

- Minimum investment thresholds are typically high

- Maximum tax benefit requires a holding period of 10+ years

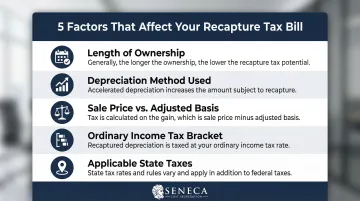

Key Factors That Affect the Size of Your Recapture Tax Bill

Your recapture tax bill isn't fixed — it can vary widely depending on how you've held, depreciated, and sold the property. These five factors drive the difference:

- Length of ownership — Longer hold periods mean more accumulated depreciation and a larger recapture amount

- Depreciation method used — Accelerated methods like bonus depreciation or cost segregation front-load deductions, which increases the amount subject to ordinary income rates under Section 1245 at sale

- Sale price relative to adjusted basis — A higher sale price increases total gain, meaning more of the gain falls above the recapture portion and may qualify for lower capital gains rates

- Taxpayer's ordinary income tax bracket — The 25% cap on unrecaptured Section 1250 gain only applies if your marginal rate is at or above 25% — investors in lower brackets may pay less

- Applicable state taxes — Many states (including California, New York, and New Jersey) do not conform to federal recapture rules and may tax gains differently, which can push your combined effective rate meaningfully higher

Common Misconceptions About Depreciation Recapture

Myth: "I Didn't Claim It So I Won't Owe It"

Many landlords believe that skipping depreciation on their returns protects them from recapture. This is incorrect. The IRS calculates recapture based on depreciation "allowed or allowable," meaning if you were eligible to claim it, your basis is reduced regardless of whether you did. If you skipped depreciation claims, a CPA can file amended returns to correct your basis before you sell.

Myth: Holding Longer Avoids Recapture

No minimum holding period eliminates depreciation recapture. Unlike short-term vs. long-term capital gains (which are determined by a 1-year threshold), recapture applies regardless of how long the property was held. The only exception is when property is transferred at death via step-up in basis.

Myth: "Depreciation Recapture and Capital Gains Are the Same Thing"

Many investors use these terms interchangeably, but they are separate components of total gain. Recapture is taxed at ordinary income rates (Section 1245) or capped at 25% (Section 1250), while true capital gain above the recapture amount is taxed at the lower long-term capital gains rate. Treating them as identical is one of the most common reasons investors are caught off guard at closing — the actual tax bill is higher than they planned for.

Frequently Asked Questions

Do I have to recapture depreciation when I sell a rental property?

Yes, depreciation recapture is mandatory if the property sold for more than its adjusted cost basis. It applies regardless of whether you actually claimed depreciation, because the IRS reduces basis by "allowed or allowable" depreciation.

What is the depreciation recapture tax rate for rental property?

Residential rental property (Section 1250) recapture is taxed as "unrecaptured Section 1250 gain" at a maximum rate of 25%. Personal property components (Section 1245 — such as appliances or cost-segregated short-life assets) are taxed at your ordinary income rate, up to 37%.

How do I calculate depreciation recapture on a rental property?

Start with your original purchase price plus improvements, subtract accumulated depreciation to get adjusted cost basis, then subtract that from your sale price for total gain. The portion of gain equal to accumulated depreciation is recaptured at up to 25%; anything above that is taxed at long-term capital gains rates.

How do you avoid or defer depreciation recapture on a rental property?

Three strategies apply: a 1031 like-kind exchange defers both recapture and capital gains; holding until death passes the property to heirs with a stepped-up basis that erases recapture; and donating to a qualified charity avoids recapture entirely while potentially yielding a fair market value deduction.

How long do you have to hold a rental property to avoid depreciation recapture?

There is no holding period that avoids depreciation recapture. Unlike capital gains (which require a 1-year hold for long-term treatment), recapture applies regardless of how long the property is held. The only scenario where recapture disappears is when property is transferred via inheritance and the heir receives a stepped-up basis.

Is there depreciation recapture if I sell a rental property at a loss, and can losses offset it?

If the sale price is below adjusted cost basis, there is no gain and no recapture. If there is any gain — even a small one — recapture applies up to that amount, and capital losses from other investments generally cannot offset the ordinary income portion of Section 1245 recapture.

Need help understanding how your cost segregation study affects future recapture exposure? Contact Seneca Cost Segregation for a complimentary analysis of your property's depreciation strategy and long-term tax planning options.