Introduction

"I've been using cost segregation for years — now I'm selling. How much of those tax savings do I actually have to give back?" This question trips up real estate investors as they approach the sale of a property, and it's one of the most misunderstood moments in their journey.

Selling a property triggers depreciation recapture — the IRS reclaims a portion of those front-loaded deductions you claimed in earlier years. What most investors don't realize is that recapture is not a loss. After recapture taxes are paid, the strategy still delivers a net positive return, thanks to the time value of money and smart exit planning.

This article breaks down exactly how recapture works, the critical difference between Section 1245 and Section 1250 assets, whether cost segregation was still worth it, and specific strategies to minimize or defer what you owe when you sell.

TLDR

- Selling triggers depreciation recapture — the IRS taxes prior depreciation deductions you claimed

- Personal property (Section 1245) is recaptured at ordinary income rates up to 37%

- Real property (Section 1250) is taxed at a maximum 25% "unrecaptured gain" rate

- Cost segregation stays net-positive: deductions come at ordinary rates, recapture is capped at lower rates

- Strategies like 1031 exchanges, Opportunity Zones, and partial dispositions can reduce or defer recapture taxes

What Is Depreciation Recapture and Why It Matters When You Sell

Depreciation recapture is the IRS mechanism that "claws back" a portion of the depreciation deductions you previously claimed when you sell a property at a gain. Because those deductions reduced your taxable income at ordinary income rates (up to 37%), the IRS requires you to pay tax on the portion of your gain attributable to depreciation — at rates higher than standard long-term capital gains.

Depreciation reduces your taxable income each year, which simultaneously lowers your tax basis in the property. When you sell, the IRS compares the sale price to that reduced basis and taxes the difference attributable to depreciation at recapture rates.

When Recapture Is Triggered

Recapture primarily occurs when you sell at a gain. However, selling at an overall loss can still trigger partial recapture on specific asset classes — a nuance most investors don't anticipate. For example, if your building loses value but certain personal property components (like appliances or specialty lighting) are sold at a gain, recapture applies to those specific assets.

The "Allowed or Allowable" Rule

Under IRC §1016(a)(2), the IRS calculates recapture based on depreciation that was "allowed or allowable" — even if you never claimed it. This means:

- If you skipped a cost segregation study and took straight-line depreciation only, the IRS still reduces your basis by the accelerated depreciation you could have claimed

- You'll face recapture on deductions you never received the benefit of using

- This is a key reason why doing a cost segregation study upfront is almost always the right move — you're taxed on the deductions either way

Front-Loading and Timing

Cost segregation accelerates deductions into earlier years (often Year 1 with bonus depreciation). This means recapture on accelerated assets comes due at sale rather than gradually over 27.5 or 39 years. That tradeoff works in your favor: you capture maximum tax savings when your capital is most constrained and repay them later, after your portfolio has had years to grow.

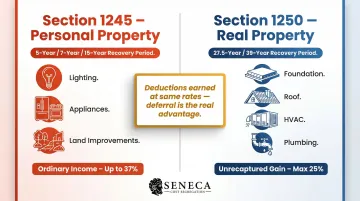

Section 1245 vs. Section 1250 Recapture: What Gets Taxed and at What Rate

The tax rate applied to recaptured depreciation depends entirely on how assets were classified during your cost segregation study.

Section 1245 Assets (Personal Property)

Section 1245 assets are personal property components identified through cost segregation:

- Specialty lighting systems

- Cabinetry and decorative millwork

- Dedicated electrical outlets serving specific equipment

- Appliances (refrigerators, ranges, dishwashers)

- Land improvements (parking lots, fencing, landscaping — 15-year property)

Recapture treatment: All prior depreciation on Section 1245 assets is recaptured and taxed at ordinary income rates — up to 37% federally for high-income taxpayers.

Section 1250 Assets (Real Property)

Section 1250 assets are structural components — the "building shell":

- Foundation and framing

- Roof structure

- HVAC systems (general comfort heating/cooling)

- General building electrical and plumbing

- Exterior walls and windows

Recapture treatment: Section 1250 recapture rules are more favorable. Only excess depreciation above straight-line is recaptured at ordinary rates; the remaining "unrecaptured Section 1250 gain" is taxed at a maximum federal rate of 25%.

Why This Distinction Matters for Cost Segregation

A cost segregation study identifies and correctly classifies assets that were already personal property — components that default depreciation schedules lump into the 39-year structural category. Moving them into 5-, 7-, or 15-year buckets has a direct consequence at sale.

When you sell, more depreciation is recaptured at ordinary income rates. That sounds like a drawback. It isn't. Those same assets generated the largest deductions in earlier years — at the same ordinary rate — while you still owned and operated the property. The real benefit is deferral: dollars saved in Year 1 are worth more than dollars paid in Year 7 or Year 10, and that gap compounds over time.

Simplified Recapture Example

Section 1245 scenario:

- You claim $100,000 in accelerated depreciation on personal property in Year 1

- You sell the property in Year 4 at a gain

- The full $100,000 is recaptured at your ordinary income rate (37% = $37,000 recapture tax)

Section 1250 scenario:

- You claim $100,000 in depreciation on structural property over 10 years using straight-line

- You sell in Year 10 at a gain

- The depreciation was taken at straight-line, so the unrecaptured amount is taxed at a maximum 25% rate ($25,000 recapture tax)

Recapture Rate Comparison Table

| Asset Type | Depreciation Recovery Period | Recapture Rate at Sale | Maximum Federal Tax Rate |

|---|---|---|---|

| Section 1245 (Personal Property) | 5, 7, or 15 years | Ordinary income | 37% |

| Section 1250 (Real Property) - Straight-Line | 27.5 or 39 years | Unrecaptured §1250 gain | 25% |

| Section 1250 (Real Property) - Excess Depreciation | 27.5 or 39 years | Ordinary income | 37% |

Was Cost Segregation Still Worth It? Running the Real Numbers

The real question isn't whether recapture taxes apply — it's whether cost segregation still comes out ahead after you pay them. The numbers make a clear case.

Time Value of Money: The Core Advantage

Receiving $100,000 in tax savings in Year 1 is worth far more than paying $25,000–$37,000 in recapture taxes five or more years later. This is the time value of money principle.

According to foundational research published in the Journal of Accountancy, "Each $100,000 in assets reclassified from a 39-year recovery period to a five-year recovery period results in approximately $16,000 in net-present-value savings, assuming a 5% discount rate and a 35% marginal tax rate."

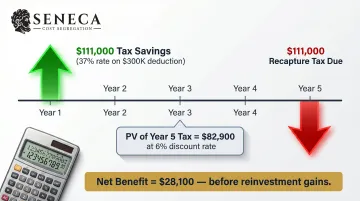

Realistic Example: $300,000 Accelerated Depreciation

Let's model a realistic scenario:

Assumptions:

- Property purchased for $1,500,000

- Cost segregation identifies $300,000 in personal property eligible for 100% bonus depreciation

- Investor is in 37% federal tax bracket

- Property held for 5 years, then sold at a gain

- 6% discount rate for present value calculations

Year 1 Tax Savings:

- $300,000 × 37% = $111,000 in federal tax savings

Year 5 Recapture Tax:

- $300,000 recaptured at 37% ordinary rate = $111,000 recapture tax

Present Value of Year 5 Recapture Tax (6% discount rate):

- $111,000 ÷ (1.06)^5 = $82,900

Net Present Value Advantage:

- $111,000 (Year 1 savings) - $82,900 (PV of Year 5 recapture) = $28,100 net benefit

Even in this scenario where the recapture rate equals the original deduction rate, the investor gains a $28,100 advantage purely from deferral. Reinvesting that $111,000 into another property, paying down high-interest debt, or deploying it elsewhere compounds that advantage further — the $28,100 figure is a floor, not a ceiling.

When Cost Segregation Is Least Favorable

Cost segregation delivers the smallest benefit for short-term holds under 3 years where recapture occurs before deferred tax savings compound. In these cases:

- The present value of recapture is much closer to the original savings

- There's less time to reinvest and earn returns on the tax savings

- Transaction costs and study fees consume a larger percentage of the benefit

However, even in 3-year scenarios, the strategy still produces a net positive — the advantage is smaller, not absent.

Seneca's Complimentary Tax Assessment

Seneca Cost Segregation offers complimentary tax assessments to help investors model the net benefit of cost segregation relative to their anticipated hold period and tax situation before committing to a study. With an average first-year deduction of $171,243 across more than 10,200 completed studies, the assessment gives you a concrete projection — not a guess — before you spend a dollar on a study.

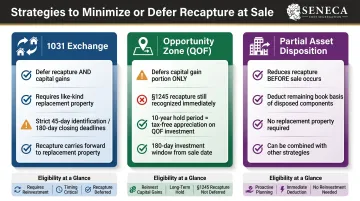

Strategies to Reduce or Defer Depreciation Recapture

1031 Exchange

A 1031 like-kind exchange allows investors to defer both capital gains taxes and depreciation recapture by rolling proceeds into a new qualifying property.

Key requirements:

- Identify replacement property within 45 days of the transfer

- Complete the exchange within 180 days (or tax return due date, whichever is earlier)

- Use a qualified intermediary to hold proceeds

Under IRC §1245(b)(4) and §1250(d)(4), recapture recognition works as follows:

- Ordinary income recapture is limited to the gain you actually recognize — typically only on "boot" (cash or non-like-kind property received)

- Receive no boot and acquire sufficient replacement property, and recapture is fully deferred

- Deferred recapture carries forward into the replacement property — it's not forgiven until that property is eventually sold (or exchanged again)

Opportunity Zone Investments

Rolling gains into a Qualified Opportunity Zone (QOF) fund can defer recapture taxes and, if held for 10 years, allow appreciation in the OZ investment to be entirely tax-free.

Key details:

- Invest capital gains into a QOF within 180 days of the sale

- Only capital gains and qualified §1231 gains are eligible for QOF deferral

- Important limitation: Ordinary income from Section 1245 depreciation recapture is NOT eligible for QOF deferral

- Unrecaptured Section 1250 gain (taxed at 25%) is treated as capital gain and is eligible

If the QOF investment is held for at least 10 years, you can elect to step up the basis to fair market value upon sale — permanently excluding any gains earned inside the fund.

This makes QOF particularly useful when you have a mix of gain types: the §1245 recapture must be recognized regardless, but sheltering the capital gain portion inside a QOF still produces meaningful tax savings — without the like-kind property matching required by a 1031.

Partial Asset Disposition (PAD) Election

Unlike a 1031 or QOF, which defer recapture into future investments, a PAD election proactively reduces the recapture amount before the sale closes. If you renovate or dispose of specific components, a PAD election under Treasury Regulation §1.168(i)-8 lets you write off the remaining depreciable basis of removed assets in the year of disposal.

How it works:

- You recognize a loss equal to the adjusted depreciable basis of the disposed component

- The IRS allows "any reasonable method" to determine the unadjusted basis if original records don't break out component costs

- A cost segregation study is an explicitly approved method for valuation

Example: You replace a roof that originally cost $80,000 and has $50,000 remaining basis. With a PAD election, you deduct the $50,000 loss immediately rather than continuing to depreciate it.

When Cost Segregation Still Makes Sense Even If You Plan to Sell

A common misconception circulates among investors: cost segregation is never worth it for short-term holds. The math tells a different story.

The outcome depends on four key variables:

- Your current tax rate

- The size of the deductions

- Your expected sale timeline

- Available deferral strategies

Even 2-3 Year Holds Can Benefit

If you have high ordinary income in the current year, large passive income to offset, or plan to execute a 1031 exchange, front-loaded deductions can still outperform straight-line depreciation overall — even on a two-year hold.

Scenarios where short-term cost segregation makes sense:

- High-income year: You're selling a business or have unusually high W-2 income and need immediate offsets

- Passive income offset: You have substantial passive income from other properties that can absorb accelerated losses

- 1031 exchange planned: Recapture is deferred entirely to the replacement property

- Partial renovation planned: You'll claim PAD losses on removed components, reducing recapture exposure

Beyond Generic Rules of Thumb

Every investor's tax situation is different, and the right answer depends on your income profile, exit strategy, and available deferral tools. Seneca Cost Segregation's engineering-based studies pair with no-cost tax strategy consultations to map out exactly where accelerated depreciation fits — or doesn't — for your specific timeline.

Across 10,200+ properties assessed, the average first-year deduction has reached $171,243. At that scale, a personalized analysis almost always reveals more opportunity than a blanket rule of thumb would suggest.

Frequently Asked Questions

What happens to cost segregation when you sell?

Selling triggers depreciation recapture — previously claimed accelerated deductions become taxable at ordinary income rates (for Section 1245 assets) or at a maximum 25% rate (for unrecaptured Section 1250 gains). Despite recapture, the strategy typically results in a net tax advantage due to the time value of upfront savings.

What is the payback period for cost segregation?

The ROI on a cost segregation study is typically well over 10-to-1, with study fees ranging from $5,000 to $15,000 for standard properties. Most investors recoup study costs within the first tax year; the hold period affects net benefit when accounting for recapture, but the vast majority of investors recoup fees many times over.

Do I have to pay back depreciation when I sell a rental property?

You don't "pay back" depreciation directly — the IRS taxes gains attributable to prior depreciation at recapture rates. This applies whether or not you actually took the deductions due to the "allowed or allowable" rule under IRC §1016(a)(2), meaning you're taxed on depreciation you could have claimed even if you didn't.

Can a 1031 exchange help me avoid depreciation recapture?

A 1031 exchange defers both capital gains and depreciation recapture by rolling proceeds into a like-kind replacement property. The recapture isn't eliminated — it carries forward to the replacement property and triggers upon a future taxable sale, unless the property passes through an estate or other qualifying transfer.

Is cost segregation still worth it if I plan to sell in a few years?

It depends on your tax situation, hold period, and exit strategy. In many cases — especially when a 1031 exchange or Opportunity Zone investment is planned — cost segregation remains net-positive even for shorter holds. A break-even analysis comparing upfront deductions against projected recapture will give you a clear answer for your specific situation.

Ready to see how cost segregation fits your exit strategy? Seneca Cost Segregation offers complimentary tax assessments that model net benefit against your hold period and tax position. Backed by 12+ years of engineering-based studies, AuditDefense with a money-back guarantee, and a 95% client referral rate, Seneca gives real estate investors a clear, defensible path to better after-tax returns. Contact Seneca Cost Segregation at 503-383-1158 or info@senecacostseg.com to request your free analysis.