Introduction

When real estate investors sell a property, many are blindsided by a hefty tax bill on previously claimed depreciation deductions. This surprise is called depreciation recapture, and Section 1245 is one of the primary IRS rules that triggers it.

The issue is particularly acute for investors who accelerated depreciation through cost segregation or bonus depreciation strategies. Assets reclassified to 5- or 7-year property lives generate significant upfront tax savings. Those savings reverse at sale, however, with recaptured gains taxed as ordinary income at rates up to 37%.

This article explains exactly what Section 1245 property is, how recapture is calculated, how it differs from Section 1250, and what investors can do to plan around it.

TLDR

- Section 1245 property includes equipment, furniture, and tangible personal property—not buildings or structural components

- All depreciation claimed on Section 1245 property is recaptured as ordinary income when sold at a gain

- The IRS taxes depreciation you could have taken, even if you never claimed it ("allowed or allowable" rule)

- Cost segregation increases Section 1245 exposure while delivering significant near-term tax savings

- 1031 exchanges defer recapture, but the exposure carries forward into the replacement property's basis until that property is eventually sold

What Is Section 1245 Property?

Section 1245 property includes any tangible or intangible personal property subject to depreciation or amortization and used in a trade or business, excluding buildings and their structural components. For real estate investors, understanding this distinction directly affects how depreciation recapture is calculated when a property is sold.

Primary Categories of Section 1245 Property

Section 1245 property typically includes:

- Equipment and machinery used in business operations

- Furniture and fixtures (desks, chairs, cabinets, shelving)

- Carpeting installed in commercial or rental properties

- Appliances such as refrigerators, stoves, washers, and dryers

- Certain electrical and plumbing systems serving business operations rather than general building comfort

- Section 197 intangibles such as goodwill, trademarks, and licenses

What Does NOT Qualify as Section 1245 Property

The following are classified as Section 1250 property, not Section 1245:

- Buildings and structural frameworks

- Walls, floors, windows, doors, and roofs

- Central HVAC systems serving occupant comfort

- Plumbing and electrical systems integral to the building's general function

- Elevators, escalators, and fire suppression systems

The boundary between these two categories isn't always obvious—some assets look structural but function differently.

Grey-Area Assets: When Structure Becomes Personal Property

The key test is whether an asset serves the taxpayer's specific business operations or the building's general function. Assets tied to a particular trade or process often qualify as Section 1245 property even when they're physically attached to the structure.

Examples include:

- HVAC systems installed primarily for manufacturing or production operations

- Special-purpose storage tanks for oil, gas, or agricultural products

- Grain bins and agricultural processing equipment

- Refrigeration units in restaurants or food service facilities

The IRS Cost Segregation Audit Techniques Guide uses the Whiteco factors to determine whether an asset is "inherently permanent" or qualifies as personal property.

Relationship to Section 1231

Section 1245 property is a subset of Section 1231 property. When you sell Section 1245 property:

- Section 1245 applies depreciation recapture first as ordinary income

- Only the gain in excess of total depreciation is treated as Section 1231 gain

- Section 1231 gain may qualify for favorable long-term capital gains treatment

How Depreciation Recapture Works Under Section 1245

When Section 1245 property is sold at a gain, the IRS recaptures the lesser of:

- (a) Total depreciation allowed or allowable, or

- (b) The recognized gain on the sale

This recaptured amount is taxed as ordinary income, not at favorable capital gains rates.

Step-by-Step Example

Suppose an investor purchases $50,000 in equipment for a commercial property:

- Purchase price: $50,000

- Depreciation claimed over 5 years: $30,000

- Adjusted basis at sale: $50,000 - $30,000 = $20,000

- Sale price: $40,000

- Total gain: $40,000 - $20,000 = $20,000

Recapture calculation:

- Lesser of depreciation allowed ($30,000) or gain realized ($20,000) = $20,000

- Ordinary income recapture: $20,000 (taxed at rates up to 37%)

- Section 1231 capital gain: $0 (no gain in excess of depreciation)

If the sale price were $60,000 instead:

- Total gain: $60,000 - $20,000 = $40,000

- Ordinary income recapture: $30,000 (all depreciation taken)

- Section 1231 capital gain: $10,000 (taxed at preferential capital gains rates)

These examples assume the investor claimed every depreciation deduction available — but what if they didn't? That's where the "allowed or allowable" rule comes in.

The "Allowed or Allowable" Rule

According to Treasury Regulation §1.1016-3, the IRS uses whichever is greater:

- Depreciation actually claimed ("allowed"), or

- Depreciation that could have been claimed ("allowable")

This means investors who deliberately skip depreciation deductions will still face recapture based on what they should have claimed—calculated using the straight-line method.

Reporting and Installment Sale Rules

Investors report Section 1245 recapture on Form 4797, Part III (lines 19–25); that amount then flows to Part II as ordinary income. Any remaining Section 1231 gain goes on Schedule D.

One timing rule catches many investors off guard: under IRC §453(i), Section 1245 recapture must be recognized in full in the year of sale—even when proceeds arrive over multiple years. Recapture income cannot be spread across installment payments the way other gains can.

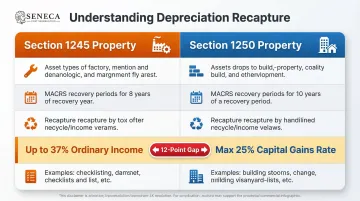

Section 1245 vs. Section 1250: Key Differences

Section 1250 property includes all depreciable real property that is not Section 1245 property—primarily buildings and their structural components.

Section 1250 Recapture Rule

For residential and commercial real property placed in service after 1986 and depreciated using straight-line MACRS, there is no "additional depreciation" to recapture as ordinary income under Section 1250.

However, the unrecaptured Section 1250 gain (the portion attributable to total depreciation taken) is taxed at a maximum 25% federal capital gains rate — higher than the standard long-term capital gains rate of 15% or 20%.

Critical Tax Rate Difference

| Feature | Section 1245 Property | Section 1250 Property |

|---|---|---|

| Asset Type | Personal property (equipment, furniture, fixtures) | Real property (buildings, structural components) |

| MACRS Recovery Period | 5-, 7-, or 15-year | 27.5-year (residential) or 39-year (commercial) |

| Recapture Type | Lesser of depreciation allowed or gain realized | Unrecaptured Section 1250 gain (MACRS straight-line) |

| Tax Rate | Ordinary income (up to 37%) | Maximum 25% federal rate |

| Examples | Appliances, carpeting, machinery, reclassified assets | Buildings, roofs, walls, central HVAC, plumbing |

This distinction matters significantly at sale. An investor in the 37% tax bracket pays 12 percentage points more on Section 1245 recapture than on Section 1250 unrecaptured gain. That gap makes asset classification a direct tax planning lever — understanding which assets fall under each category is essential before selling a property.

The "Allowed or Allowable" Rule: A Common Investor Trap

Many investors incorrectly assume they can avoid recapture by simply not claiming depreciation. This is false.

How the Trap Works

The IRS requires basis to be reduced by the greater of depreciation allowed or allowable. This means:

- You lose the deduction benefit if you don't claim it

- You still owe recapture tax as if you had claimed it

Practical Scenario

An investor inherits a rental property and deliberately avoids taking depreciation for five years, believing this will reduce their tax bill at sale.

Reality:

- The IRS calculates allowable depreciation using the straight-line method

- Basis is reduced by this amount, whether claimed or not

- The IRS calculates recapture on the allowable depreciation

- The investor pays recapture tax without having received the deduction benefit

Planning Implication

That outcome — paying recapture tax on deductions never taken — is the trap in practice. Because recapture applies regardless of what you claimed, investors are always better off taking every eligible depreciation deduction annually. The tax-deferred cash from those deductions can be reinvested years before the recapture bill comes due.

How Cost Segregation Affects Section 1245 Recapture

Cost segregation studies reclassify building components from 39-year Section 1250 property to 5-, 7-, or 15-year Section 1245 property, enabling accelerated depreciation deductions.

According to the IRS Cost Segregation Audit Techniques Guide, engineering-based studies typically reclassify 20% to 45% of a property's depreciable basis into shorter-lived asset classes, depending on property type.

The Timing Benefit

Shorter-lived Section 1245 assets are often fully depreciated before a property is sold. If sufficient time has passed, recapture may be minimal or zero.

Example:

- 5-year property is fully depreciated after 6 years (using half-year convention)

- 7-year property is fully depreciated after 8 years

- Holding a property for 5+ years after a cost segregation study can significantly reduce Section 1245 recapture exposure

That timing advantage only works when asset classifications are documented correctly from the start — which is where study quality matters.

Documentation and Defensibility

A professional cost segregation study identifies and documents correct asset classifications upfront — maximizing depreciation benefits and ensuring recapture calculations that hold up under IRS scrutiny. Seneca Cost Segregation uses an engineering-based methodology that satisfies the IRS's detailed analysis standard, steering clear of the "rule of thumb" shortcuts the IRS Cost Segregation Audit Techniques Guide flags as audit risks.

Strategies to Minimize or Defer Section 1245 Recapture

Three strategies can reduce or defer Section 1245 recapture liability: structuring exchanges carefully, timing asset disposals, and using estate planning to reset basis entirely.

1031 Like-Kind Exchange Strategy

Under IRC §1245(b)(4) and IRS Publication 544, Section 1245 recapture is deferred only if the replacement property is also Section 1245 property.

- If you exchange Section 1245 property for Section 1250 real property, recapture is triggered in the year of the exchange—even if no cash is received

- Recapture potential carries over to the new property only when the replacement qualifies as Section 1245 property

Holding Period and Depreciation Exhaustion Strategy

Assets held until their depreciation life is fully exhausted and then sold near their depreciated value minimize recapture.

Under MACRS half-year convention, the recovery period extends one year beyond the asset's class life — so 5-year property depreciates over 6 years, and 7-year property over 8 years. Once fully depreciated, selling at or below adjusted basis produces no recapture income.

- Hold assets through full depreciation before selling

- Target sale prices at or below adjusted basis to eliminate recapture exposure

- Works best for equipment or personal property with predictable resale values

Gift and Estate Planning Angle

Under IRC §1014, property acquired from a decedent receives a stepped-up basis (reset to fair market value at the date of death). This wipes out any accumulated Section 1245 recapture exposure for heirs.

For long-term holders approaching retirement, this makes a compelling case for holding depreciated assets rather than selling:

- Heirs inherit a fresh basis with zero recapture liability

- Holding through death is most advantageous when accumulated depreciation is substantial

- Coordinate with an estate attorney and tax advisor — the interaction between estate taxes and stepped-up basis requires careful planning

Frequently Asked Questions

What is the difference between Section 1245 and Section 1250 property?

Section 1245 covers depreciable personal property—equipment, machinery, and furniture—while Section 1250 covers real property such as buildings and structural components. The critical difference is tax rate: Section 1245 recapture is taxed as ordinary income (up to 37%), while Section 1250 unrecaptured gain is capped at 25%.

Is a rental property classified as Section 1245 or Section 1250 property?

The building structure itself is Section 1250 property. However, certain components within a rental property—such as appliances, carpeting, equipment, and assets reclassified through cost segregation—qualify as Section 1245 property. Classification depends on the specific asset, not the property type.

What is included in Section 1245 property?

Section 1245 property includes machinery, equipment, furniture and fixtures, carpeting, Section 197 intangibles, and assets reclassified through cost segregation. Qualifying electrical systems that serve specific business operations—rather than the building generally—also fall into this category.

What is included in Section 1250 property?

Section 1250 property is all depreciable real property that is not Section 1245 property. This covers buildings and structural components: walls, roofs, floors, windows, doors, central HVAC, plumbing, and electrical systems that serve the building's general function.

How is Section 1245 depreciation recapture calculated?

Recapture equals the lesser of (a) total depreciation allowed or allowable on the property or (b) the gain realized on the sale. This recaptured amount is taxed as ordinary income, with any remaining gain treated as Section 1231 gain eligible for capital gains rates.

Can a 1031 exchange help avoid Section 1245 recapture?

A 1031 exchange defers Section 1245 recapture only if the replacement property received is also Section 1245 property. If the replacement property is Section 1250 real property, the Section 1245 recapture is triggered in the year of the exchange, even if no cash is received.