This guide changes that. Whether you own single-family rentals, multi-family properties, or short-term rentals, this definitive checklist organizes every major deduction category in one place: operating costs, depreciation strategies, advanced tax planning techniques, and property-specific rules. Rental income is taxable, but deduction knowledge is one of the most valuable tools in a real estate investor's arsenal, often worth tens of thousands in tax savings annually.

TLDR: Your Rental Property Deductions Checklist at a Glance

- Rental deductions span 10+ categories: mortgage interest, property taxes, insurance, repairs, depreciation, management fees, and more

- Cost segregation combined with 100% bonus depreciation (restored in 2025) can accelerate substantial first-year deductions

- Short-term rentals face different rules than long-term rentals, particularly the 14-day personal use threshold

- Every deduction requires receipts and documentation; the IRS audits Schedule E frequently

- This checklist covers U.S. federal taxes (Schedule E) — confirm your state rules separately, as they vary

Everyday Operating Expense Deductions

The foundation of rental property tax strategy starts with Schedule E, where landlords deduct the ordinary and necessary costs of managing and maintaining rental property directly from rental income.

| Deduction Category | What Qualifies | Schedule |

|---|---|---|

| Mortgage Interest | Interest on loans used to acquire, build, or improve rental property | Schedule E |

| Property Taxes | State and local property taxes on rental property | Schedule E |

| Insurance Premiums | Landlord, liability, flood, and umbrella policies | Schedule E |

| Property Management & Professional Fees | Management companies, attorneys, accountants, advertising | Schedule E |

| Utilities & Services | Electricity, gas, water, landscaping, cleaning | Schedule E |

| Travel | Mileage at standard rate or actual vehicle expenses | Schedule E |

| Home Office | Dedicated exclusive-use space for rental management | Schedule E |

| Depreciation | Building cost over 27.5 years; components accelerated via cost segregation | Schedule E |

Mortgage Interest

Interest paid on loans used to acquire, build, or improve rental property is fully deductible on Schedule E. For leveraged investors, this typically represents one of the largest annual deductions: often $15,000 to $50,000+ depending on loan size. This deduction appears on Schedule E as a business expense, not Schedule A as a personal itemized deduction.

Two related costs require different treatment: points paid to obtain the mortgage must be amortized over the loan's life rather than deducted immediately, and loan origination fees are capitalized into the property's basis.

Property Taxes

State and local property taxes on rental properties are fully deductible as business expenses on Schedule E, completely bypassing the $10,000 SALT cap that restricts Schedule A personal deductions. A landlord with $15,000 in rental property taxes deducts the full amount. The same person's primary residence taxes would be capped at $10,000 under Schedule A.

Insurance Premiums

Landlord insurance, liability coverage, and specialty policies (flood, umbrella) tied specifically to the rental property are fully deductible. However, prepaid premiums require proration. If you pay a two-year policy upfront for $2,400, you can only deduct $1,200 in year one and $1,200 in year two. The IRS prohibits front-loading multi-year premiums into a single tax year.

Property Management and Professional Fees

Fees paid to property managers, real estate attorneys, accountants (for Schedule E preparation), and platform listing services are fully deductible on Lines 10 and 11 of Schedule E:

- Property management companies (typically 8–12% of monthly rent)

- Eviction attorney fees and lease drafting costs

- Tax preparation fees related to Schedule E filing

- Advertising costs on Zillow, Airbnb, VRBO, and other platforms

- Professional photography for listings

Utilities and Services

Utilities and services the landlord pays directly (not the tenant) are deductible. Common examples include:

- Electricity, gas, water, and sewage

- Trash collection and internet (for property management purposes)

- Landscaping, pest control, and snow removal

- Cleaning services between tenants

If tenants pay utilities directly, those costs are not deductible by the landlord.

Travel and Home Office Deductions

Travel to the rental property for management, maintenance, or inspection purposes is deductible under strict IRS rules. For 2026, the standard mileage rate is 72.5 cents per mile (up from 70 cents in 2025). Alternatively, landlords can deduct actual vehicle expenses (gas, maintenance, depreciation) using the percentage of business use.

One key restriction: Travel costs to improve the property (not maintain or manage it) must be capitalized and depreciated, not immediately deducted.

Home Office Deduction applies only if you use a dedicated space exclusively and regularly as your principal place of business for managing rentals. Two calculation methods exist:

- Simplified method: $5 per square foot up to 300 square feet (maximum $1,500 deduction)

- Actual expense method: Calculate the percentage of your home used for business and apply that ratio to mortgage interest, property taxes, utilities, and depreciation

| Method | Calculation | Maximum Deduction |

|---|---|---|

| Simplified method | $5 per square foot, up to 300 sq ft | $1,500 |

| Actual expense method | Business-use percentage × home expenses (mortgage interest, property taxes, utilities, depreciation) | No fixed cap |

This deduction faces heavy IRS scrutiny. The "exclusive use" test is strict — using your home office occasionally for personal tasks can disqualify the entire deduction.

Depreciation, Repairs, and Capital Improvements

Depreciation is the most powerful non-cash deduction available to real estate investors, but it requires strict adherence to IRS classification rules.

Depreciation Basics

The IRS allows landlords to deduct the cost of the building (not land) over 27.5 years for residential rental property using straight-line depreciation. This non-cash deduction reduces taxable income annually without requiring you to spend money.

Simple calculation example: Purchase price of $550,000, with land valued at $100,000 (often determined by property tax assessor ratios). Depreciable basis = $450,000. Annual depreciation = $450,000 ÷ 27.5 years = $16,364 per year.

Critical rule: Land is never depreciable because it doesn't wear out or become obsolete. Deducting the full purchase price without separating land value is a guaranteed audit adjustment.

Repairs vs. Capital Improvements

This is one of the most misunderstood areas in rental property taxation. The IRS applies the "BAR test" (Betterment, Adaptation, Restoration) to distinguish between immediately deductible repairs and improvements that must be depreciated.

Repairs (fully deductible in the year incurred):

- Fixing a broken window or door

- Patching a roof leak (not replacing the entire roof)

- Repainting walls in existing colors

- Repairing plumbing leaks or replacing a section of pipe

Capital Improvements (must be depreciated over time):

- Installing a new roof system

- Adding a new HVAC system or replacing the entire unit

- Finishing a basement or adding square footage

- Installing new flooring throughout the property

| Type | IRS Treatment | Examples |

|---|---|---|

| Repairs | Fully deductible in year incurred | Fixing broken windows/doors; patching roof leaks; repainting walls; repairing plumbing |

| Capital Improvements | Must be depreciated over time | New roof system; new HVAC; basement finishing; new flooring throughout |

Misclassifying a capital improvement as a repair is one of the most common audit triggers. The IRS Tangible Property Regulations (T.D. 9636) provide additional guidance for uncertain cases.

One way to sidestep this issue for smaller purchases: De Minimis Safe Harbor. Taxpayers without an Applicable Financial Statement can immediately deduct tangible property purchases up to $2,500 per invoice or item. This election is made annually by attaching a statement to your tax return.

Section 179 Expensing

Section 179 allows immediate expensing of certain personal property placed in service in a rental — including appliances, furniture for short-term rentals, and qualified real property improvements such as roofs, HVAC, and fire/security systems. For 2025 and 2026, the maximum deduction is $2,500,000, with phase-out beginning at $4,000,000.

Critical limitation: Section 179 cannot create or increase a net rental loss. If your rental activity is already showing a loss, Section 179 won't help. Bonus depreciation does not have this business income limitation.

| Feature | Section 179 | Bonus Depreciation |

|---|---|---|

| 2025–2026 Maximum Deduction | $2,500,000 | No dollar limit |

| Phase-Out Threshold | $4,000,000 | N/A |

| Can Create Net Rental Loss? | No | Yes |

| Applicable Property | Personal property + qualified real property improvements (roofs, HVAC, fire/security) | Property with recovery period of 20 years or less |

Bonus Depreciation

The One Big Beautiful Bill Act (enacted July 2025) permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. Landlords can now immediately deduct the full cost of qualifying personal property — those with recovery periods of 20 years or less — in the year placed in service.

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | |

| January 1, 2023 – December 31, 2023 | 80% | |

| January 1, 2024 – December 31, 2024 | 60% | |

| January 1, 2025 – January 18, 2025 | 40% | |

| January 19, 2025 – December 31, 2030 | 100% | Acquisition date must be January 19, 2025 or later |

| 2025 (acquisition date before January 19, 2025) | 40% | TCJA phase-down applies |

| 2026 (acquisition date before January 19, 2025) | 20% | TCJA phase-down applies |

Qualifying property includes:

- Appliances and carpets

- Furniture (especially relevant for short-term rentals)

- Certain building components identified through cost segregation studies

When combined with a cost segregation study, this strategy can generate first-year deductions of $100,000 to $500,000+ depending on property value.

Depreciation Recapture Warning

When you sell a rental property, the IRS "recaptures" depreciation deductions taken over the years. The portion attributable to depreciation on real property is taxed at a maximum rate of 25% (unrecaptured Section 1250 gain). A 1031 exchange defers this recapture tax by rolling sale proceeds into a replacement property, but timing matters. Waiting until after a sale closes to plan an exit eliminates that option entirely.

Advanced Tax Strategies: Cost Segregation, Passive Losses, and Real Estate Professional Status

Rental real estate is generally classified as "passive" by the IRS, meaning rental losses can typically only offset passive income, not W-2 wages or active business income. However, specific exceptions can unlock far greater tax benefits.

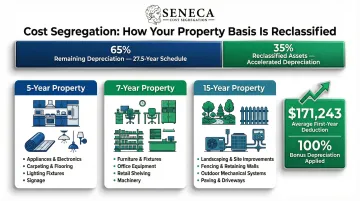

Cost Segregation Studies: The Multiplier Deduction

A cost segregation study is an engineering-based analysis that reclassifies building components from 27.5-year depreciation schedules into 5-, 7-, or 15-year schedules. Components commonly reclassified include:

- 5-year property: Carpeting, appliances, decorative lighting, ceiling fans, furniture

- 15-year property: Landscaping, irrigation systems, outdoor lighting, fencing, sidewalks, pools

| Property Category | Recovery Period | Examples |

|---|---|---|

| Personal property | 5 years | Carpeting, appliances, decorative lighting, ceiling fans, furniture |

| Land improvements | 15 years | Landscaping, irrigation systems, outdoor lighting, fencing, sidewalks, pools |

According to the American Society of Cost Segregation Professionals, these studies typically reclassify approximately 30% of a property's basis into shorter-lived categories. When combined with 100% bonus depreciation, this strategy turns 20-40% of property cost into immediate tax savings.

Real-world example: Seneca Cost Segregation, which has completed over 10,200 IRS-compliant studies nationwide, reports an average first-year deduction of $171,243. For a single-family rental purchased at $420,000, one study identified $72,505 in assets qualifying for accelerated depreciation — generating $41,832 in first-year tax savings.

Cost segregation delivers the highest ROI when:

- Properties were recently acquired or renovated

- The property includes significant personal property (furnishings, appliances, specialty systems)

- The owner can apply accelerated deductions against active income

Passive Activity Loss Rules

The IRS provides a $25,000 passive loss allowance for landlords who actively participate (approve tenants, set rental terms, arrange repairs).

Phase-out: This allowance reduces by 50 cents for every dollar your Modified Adjusted Gross Income (MAGI) exceeds $100,000 and is completely eliminated at $150,000 MAGI. For high earners, this makes rental losses difficult to utilize without additional strategies.

| MAGI Level | Allowable $25,000 Passive Loss Deduction |

|---|---|

| $100,000 or below | Full $25,000 |

| $100,001 – $149,999 | Reduced by $0.50 per $1 over $100,000 |

| $150,000 and above | $0 (fully eliminated) |

Real Estate Professional Status

Landlords who qualify as Real Estate Professionals under IRC §469(c)(7) can deduct rental losses against ordinary income without restriction. Two requirements must be met:

- More than 750 hours per year in real property trades or businesses

- More than 50% of personal services performed during the year must be in real property activities

| Requirement | Threshold |

|---|---|

| Hours in real property trades or businesses | More than 750 hours per year |

| Percentage of personal services in real property activities | More than 50% |

This designation carries real power, but the IRS scrutinizes it closely. Spouses can qualify on joint returns, which makes the threshold achievable for households where one partner focuses full-time on real estate.

Proper hour documentation is non-negotiable. Detailed records covering the following are required:

- Property management activities and decisions

- Tenant communications and lease negotiations

- Maintenance coordination and vendor oversight

- In-person property visits

The Short-Term Rental Loophole

Short-term rental properties with an average guest stay of 7 days or fewer may be treated as non-passive activities under specific IRS material participation tests. This allows STR investors to use losses to offset W-2 or business income even without real estate professional status.

Material participation tests (must meet one):

- You participated for more than 500 hours during the year

- Your participation constituted substantially all participation (including non-owners)

- You participated for more than 100 hours, and no one else participated more

| Test | Requirement |

|---|---|

| Hours test | More than 500 hours of participation during the year |

| Substantially all test | Participation constituted substantially all participation (including non-owners) |

| Comparative hours test | More than 100 hours, and no one else participated more |

This strategy requires strict documentation of hours worked in the STR business, including property management, guest communication, cleaning coordination, and maintenance oversight.

Short-Term Rental (STR) Specific Deductions

Short-term rentals face unique IRS rules regarding personal use and expense allocation that can significantly restrict deduction eligibility.

The 14-Day / 10% Rule

If you use your rental property personally for more than 14 days or 10% of the days it's rented at fair market rate (whichever is greater), the IRS classifies it as a personal residence and restricts deductions. Expenses cannot exceed rental income, and losses cannot offset other income—they must be carried forward.

The sub-15-day exception: If the property is rented for fewer than 15 days annually, rental income is completely tax-free, but no rental expenses can be deducted.

STR-Specific Deductible Expenses

Short-term rental operators can deduct expenses directly related to the rental activity:

- Platform host fees (Airbnb service fees, VRBO commissions)

- Guest supplies (toiletries, coffee, welcome baskets, linens)

- Furnishings and decor (fully deductible if property qualifies as non-personal residence)

- Professional photography and staging

- STR management software and booking tools

- Enhanced cleaning between guests

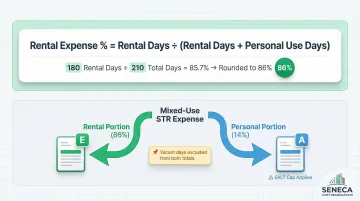

Mixed-Use Property Allocation

When a property serves both rental and personal purposes, expenses must be allocated proportionally using this IRS formula:

Rental expense percentage = Total days of rental use ÷ Total days of rental and personal use

Two rules govern how the split applies once you have your percentage:

- Vacant days don't count: days the property sits unused are excluded from both rental and personal day totals

- Schedule routing matters: the rental portion of mortgage interest and property taxes goes on Schedule E; the personal portion moves to Schedule A (subject to SALT caps and itemization requirements)

What You Cannot Deduct on a Rental Property

Attempting to deduct non-qualifying expenses is a fast route to an IRS audit and potential penalties.

Land and Personal Expenses

Land cannot be depreciated; only buildings and improvements can be. Personal expenses mixed into rental activities are strictly non-deductible:

- Groceries or meals during property visits (unless traveling away from home overnight)

- Personal vehicle use unrelated to the rental

- Home expenses not tied to an exclusive-use home office

- Personal property improvements unrelated to the rental

The IRS Audit Techniques Guide directs examiners to heavily scrutinize Schedule E for commingled personal and business expenses.

Capital Improvements Misclassified as Repairs

Improperly expensing a capital improvement as a repair is a frequent audit trigger. The IRS may reclassify it, resulting in penalties and interest.

When in doubt, apply the BAR test: an expense is likely a capital improvement (requiring depreciation) if it meets any of these criteria:

- Betterment: Adds value or fixes a pre-existing defect

- Adaptation: Converts the property to a new or different use

- Restoration: Returns the property to like-new condition

| BAR Criterion | Description |

|---|---|

| Betterment | Adds value or fixes a pre-existing defect |

| Adaptation | Converts the property to a new or different use |

| Restoration | Returns the property to like-new condition |

Pre-Rental and Post-Sale Expenses

Expenses incurred before a property is "ready and available for rent" cannot be deducted as operating expenses. They must be capitalized into the property's basis. This includes initial renovation costs, carrying costs before the first tenant, and marketing expenses before the property is listed.

The same boundary applies at the other end of the timeline. Costs incurred after a property leaves the rental market, such as post-sale repairs and closing costs, are not deductible as rental operating expenses, though they may affect capital gains calculations.

Frequently Asked Questions

What expenses are deductible on a rental property?

Landlords can deduct ordinary and necessary rental expenses including mortgage interest, property taxes, insurance, repairs, depreciation, property management fees, utilities, advertising, and professional services, all reported on Schedule E as long as they're directly related to producing rental income.

What is the most overlooked tax deduction for rental property?

Depreciation, especially accelerated depreciation through cost segregation, is among the most underutilized deductions. Most landlords default to 27.5-year straight-line depreciation, missing the chance to front-load deductions by reclassifying 20–40% of property costs into 5, 7, and 15-year categories through an engineering-based cost segregation study.

What is the rental property tax loophole?

The term typically refers to two strategies. Real Estate Professional Status lets investors meeting the 750-hour and 50% time tests offset ordinary income with passive losses. The short-term rental exception applies when average stays are 7 days or fewer, potentially bypassing passive loss limitations under material participation rules.

What is the 50% rule in rental property?

The 50% rule is a real estate investing rule of thumb (not an IRS tax rule) suggesting that roughly 50% of gross rental income goes toward operating expenses excluding mortgage principal and interest. It's used to estimate cash flow and profitability before purchase, not to determine tax deductions.

Can I deduct repairs and improvements on my rental property?

Repairs that maintain current condition (fixing broken windows, patching leaks, repainting) are fully deductible in the year incurred. Improvements that add value or extend useful life (new roof, HVAC system, additions) must be depreciated over time. Misclassifying improvements as repairs is one of the most common audit triggers for landlords.