Introduction

According to the Government Accountability Office, at least 53% of individual taxpayers with rental real estate misreported their activities, contributing to a $12.4 billion net misreported income gap in a single tax year. More recently, the IRS projected a $28 billion underreporting tax gap specifically for rents and royalties in Tax Year 2022. This staggering figure reveals two critical truths: many landlords are overpaying in taxes by missing legitimate deductions, while others are underreporting income and risking penalties.

Rental property taxes are not a fixed cost. Your tax burden is determined by decisions made before, during, and after property ownership, and most landlords are leaving real money on the table. This guide covers the main tax cost drivers, how that burden builds over the ownership lifecycle, and three strategic angles for reducing what you owe: decisions at acquisition, ongoing management practices, and the broader context surrounding your property.

TL;DR

- Rental income is taxed as ordinary income, but landlords can access extensive deductions that sharply cut taxable income

- The biggest tax costs come from failing to maximize depreciation, misclassifying expenses, and structuring entities poorly

- Advanced strategies like cost segregation can front-load depreciation deductions and generate five- or six-figure savings in year one

- Reducing your tax burden takes action on three fronts: before purchase, during ownership, and at the entity level

- Real estate tax specialists regularly uncover deductions that add up to six figures: deductions most general CPAs never identify

How Rental Property Tax Burdens Accumulate Over Time

Rental tax liability doesn't appear as a single large bill. It builds gradually through a combination of:

- Ordinary income taxes on rent collected each year

- Annual property taxes assessed by local jurisdictions

- Depreciation recapture obligations deferred until sale

This incremental accumulation makes the cumulative burden easy to underestimate year over year.

Cost accumulation is often invisible because many landlords report gross rental income without fully claiming eligible deductions. Each filing season, taxable income runs higher than it should, widening the gap between what landlords owe and what they actually pay. Over a decade of ownership, these missed deductions can total tens or hundreds of thousands of dollars in unnecessary tax payments.

That ongoing drag reaches a peak at the point of sale. Depreciation recapture (taxed at up to 25%), capital gains taxes, and state-level taxes converge into a single large tax event. For a property held 15 years with substantial depreciation claimed, the recapture bill alone can reach six figures, a number that catches unprepared investors well short of their expected net proceeds.

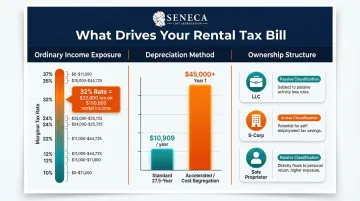

Key Drivers Behind Your Rental Property Tax Bill

Three factors drive the size of your rental tax bill, and each one is addressable with the right strategy:

- Ordinary income exposure: Rental income stacks directly on top of your taxable income and gets taxed at your marginal rate. For Tax Year 2025, federal marginal tax rates range from 10% to 37%. A landlord in the 32% bracket pays $32,000 in federal tax on $100,000 of net rental income, before state taxes.

- Depreciation method and timeline: Residential properties default to a 27.5-year straight-line schedule; commercial properties use 39 years. That limits annual deductions considerably. A $300,000 residential building depreciates at just $10,909 per year under the standard method, even though faster options like cost segregation or bonus depreciation exist.

- Ownership structure and activity classification: Whether you hold property as a sole proprietor, LLC, or S-Corp affects which deductions apply. Equally important, whether your rental activity is classified as passive or active determines whether losses can offset W-2 income. These setup decisions compound: get them wrong early, and you overpay for the full ownership period.

Strategies That Reduce Rental Property Taxes by Changing Decisions

Some of the highest-impact tax decisions are made before or at the point of acquisition. Entity type, purchase structure, and property classification all determine which tax rules apply for the entire investment lifecycle.

Choose the Right Ownership Entity

Entity choice affects liability, tax treatment, and which deductions are available. Two common structures for rental property investors:

| Entity Type | Key Features |

|---|---|

| LLC with pass-through taxation | Preserves access to deductions on the owner's personal return while providing liability protection |

| S-Corp election | May reduce self-employment tax exposure for active operators who draw a salary, though it adds administrative complexity |

A tax professional can evaluate entity structure options prior to acquisition based on the investor's specific circumstances.

Pursue Real Estate Professional Status

The IRS defines a real estate professional as someone who performs more than 750 hours per year materially participating in real estate and spends more than 50% of their personal services in real property trades or businesses. Qualifying allows investors to treat rental losses as active rather than passive, meaning they can offset ordinary W-2 income without restriction. For full-time investors, this is one of the most significant tax-saving opportunities available.

Use a 1031 Exchange to Defer Capital Gains

Under IRC Section 1031, selling a rental property and reinvesting proceeds into a "like-kind" property defers both capital gains tax and depreciation recapture indefinitely. Strict timelines apply:

- Replacement property must be identified within 45 days of sale

- The exchange must be completed within 180 days

Used repeatedly across an investment career, 1031 exchanges let investors defer the tax bill at each sale, keeping more capital working in the next property instead of going to the IRS.

Classify Short-Term Rentals Correctly

Properties rented for an average of 7 days or fewer may not be treated as passive rental activity under IRS temporary regulations. If the owner materially participates in the short-term rental business (meeting the 100-hour or 500-hour tests), losses can offset other active income without the passive activity limitations that apply to long-term rentals. This classification can generate significant tax savings for STR operators.

Time Property Improvements Strategically

The decision to classify work as repairs versus capital improvements has direct tax consequences. Repairs are fully deductible in the current year, while improvements must be depreciated over 27.5 or 39 years. The tax outcome depends on the timing and categorization of work: replacing a broken HVAC unit is a repair, but upgrading to a more efficient system is an improvement.

Strategies That Reduce Rental Property Taxes Through Better Management

Ongoing management decisions determine how much of your rental income is actually taxable. Landlords who track expenses diligently and understand what qualifies as a deduction consistently report lower taxable income than those who do not.

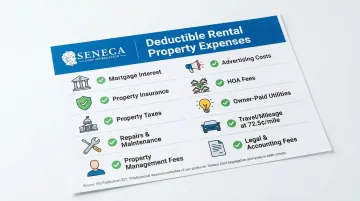

Claim Every Eligible Operating Deduction

IRS Publication 527 explicitly lists deductible rental expenses. Many landlords fail to claim all of these consistently:

- Mortgage interest

- Property insurance premiums

- Property taxes

- Repairs and maintenance

- Property management fees

- Advertising costs

- HOA fees

- Utilities paid by the owner

- Travel to properties (IRS standard mileage rate: 72.5 cents per mile for 2026)

- Legal and accounting fees

Accounting software with rental property categories can simplify the process of tracking and categorizing expenses at tax time.

Distinguish Repairs from Capital Improvements Rigorously

Under Treasury Regulation §1.263(a)-3, expenses must be capitalized if they result in a betterment, restoration, or adaptation to a new use. Repairs that restore a property to its original working condition are immediately deductible. Misclassifying improvements as repairs is a common IRS audit trigger, so documentation matters.

Safe harbors can help:

| Safe Harbor | Description |

|---|---|

| De Minimis Safe Harbor | Deduct amounts up to $2,500 per invoice/item (without an Applicable Financial Statement) or $5,000 (with AFS) |

| Small Taxpayer Safe Harbor | Deduct repairs and improvements up to the lesser of 2% of building basis or $10,000 annually if average annual gross receipts are $10M or less |

Leverage the QBI Deduction Where Eligible

Under Section 199A, qualifying rental income through a pass-through entity may allow a deduction of up to 20% of qualified business income. Rev. Proc. 2019-38 provides a safe harbor that treats rental real estate as a trade or business. To qualify, the enterprise must:

- Maintain separate books and records for each rental property

- Perform 250+ hours of rental services annually

- Keep contemporaneous time records documenting those services

For Tax Year 2025, the deduction begins phasing out when taxable income exceeds $197,300 (single) or $394,600 (married filing jointly).

Implement a Systematic Record-Keeping Process

The IRS requires documentation to substantiate any deduction claimed. Publication 583 mandates keeping records for at least 3 years from the filing date, or up to 6 years if income is underreported by more than 25%.

Property-level documentation includes:

- Receipts and contractor invoices

- Bank and credit card statements

- Mileage logs for property visits

- Copies of lease agreements and management contracts

Landlords with organized, property-level documentation are better positioned to claim every eligible deduction and hold up under an audit.

Strategies That Reduce Rental Property Taxes by Changing the Context Around Your Property

In many cases, the surrounding strategy (how depreciation is structured, who advises on taxes, and when key financial events occur) is the real lever for large-scale tax reduction, not just the deductions claimed year to year.

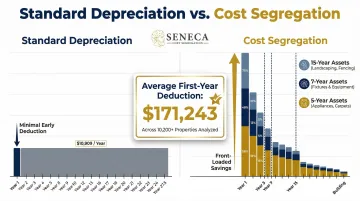

Use Cost Segregation to Front-Load Depreciation Deductions

Standard depreciation spreads the cost of a property over 27.5 or 39 years. A cost segregation study reclassifies components of the building into shorter depreciation categories:

| Property Class | Examples |

|---|---|

| 5-year property | Appliances, carpets, furniture |

| 7-year property | Office furniture, fixtures |

| 15-year property | Landscaping, fencing, sidewalks |

This sharply accelerates deductions into the early years of ownership when they have the highest value. Seneca Cost Segregation's engineering-based studies have generated an average first-year deduction of $171,243 across more than 10,200 properties, with studies typically completed within 2–4 weeks.

Combine Cost Segregation with Bonus Depreciation

Under Section 168(k), assets identified through cost segregation that fall into 5-, 7-, or 15-year property classes may qualify for bonus depreciation. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively. This allows a large portion of reclassified costs to be deducted in year one rather than spread over several years, generating immediate cash flow for reinvestment.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | |

| January 1, 2023 – December 31, 2023 | 80% | |

| January 1, 2024 – December 31, 2024 | 60% | |

| January 1, 2025 – January 18, 2025 | 40% | |

| January 19, 2025 – December 31, 2030 | 100% | Acquisition date must be January 19, 2025 or later |

| 2025 | 40% | Acquisition date before January 19, 2025 |

| 2026 | 20% | Acquisition date before January 19, 2025 |

Engage a Tax Professional Who Specializes in Real Estate

A general CPA may handle your returns competently but still miss real estate-specific strategies like cost segregation, passive activity loss rules, and the QBI deduction. A specialist working exclusively with rental investors knows where to look. Common areas general tax professionals overlook include:

- Passive activity grouping elections that unlock loss deductions

- Short-term rental exceptions that bypass passive activity limits

- QBI deduction eligibility for rental portfolios structured as a business

- Catch-up depreciation on prior-year studies through a 481(a) adjustment

The right advisor can recover more in year one than their entire fee.

Time Major Income and Expense Events Deliberately

Two straightforward moves (deferring income and accelerating deductions) can lower the effective tax rate on rental profits without changing the underlying investment. Completing repairs before December 31 shifts deductions into the current year. Timing a property sale to coincide with a lower-income year reduces the capital gains rate that applies. Neither requires structural changes to your portfolio, just deliberate planning ahead of year-end.

Conclusion

The landlords who pay the least in taxes aren't the ones who work harder at filing time. They're the ones who understand where tax liability originates. Income treatment, depreciation timing, ownership structure, and sale events each present decision points. Getting those decisions right is what separates a tax-efficient portfolio from one that consistently overpays.

The most tax-efficient landlords approach this as an ongoing strategy across the full ownership lifecycle, not a once-a-year filing activity. The right professional partnerships (a specialized CPA and an engineering-based cost segregation firm like Seneca Cost Segregation, which has delivered an average first-year deduction of $171,243 across more than 10,200 properties) turn tax savings into reinvestment capital that funds the next acquisition.

Frequently Asked Questions

How are property taxes on rental property calculated?

Local governments assess property taxes based on the property's assessed value multiplied by the local millage rate. Assessments vary by jurisdiction and are often lower than market value due to assessment caps. Property taxes paid are fully deductible as a rental expense on federal returns.

How do taxes work for landlords?

Landlords report rental income on Schedule E and pay ordinary income tax at their marginal rate. They can offset that income with a wide range of eligible deductions, and depreciation is typically the single largest one available.

How can I minimize taxes on rental property income?

Applicable strategies include maximizing all eligible operating deductions, using accelerated depreciation including cost segregation, selecting the right entity structure, and engaging a tax professional who specializes in real estate. Investors who apply all four strategies together routinely cut their taxable rental income by 40% or more in the first year.

What is the 50% rule in rental property?

The 50% rule is an investing heuristic (not a tax rule) used to estimate that roughly 50% of gross rental income will be consumed by operating expenses. This helps investors quickly gauge whether a property will generate positive cash flow without running a full financial model.

Does the IRS know if you rent out your property?

Yes. The IRS receives information from multiple sources including 1099 filings, tenant-reported payments, and property records. Unreported rental income is a common audit trigger, and all rental income must be reported on a federal return regardless of whether a 1099 is issued.

What is depreciation recapture and how does it affect rental property taxes?

Depreciation recapture requires investors to pay tax (at a rate of up to 25%) on all depreciation deductions claimed when a rental property is sold. This is why many investors use 1031 exchanges to defer the tax hit and roll proceeds into a new property instead.