Introduction

Real estate is one of the few asset classes where the U.S. tax code actively rewards investors. Through legal deductions, deferrals, and shelters, savvy owners can sharply reduce — or entirely eliminate — their federal tax liability. Yet thousands of investors leave substantial money on the table each year simply because they don't know which benefits they qualify for or how to claim them.

The gap is bigger than most people realize. Seneca Cost Segregation's clients average $171,243 in first-year deductions alone — money that stays in their pocket rather than going to the IRS. This guide breaks down the top tax benefits available to real estate investors and how to use them strategically.

TL;DR

- Deduct operating expenses like mortgage interest, property taxes, management fees, and repairs directly against rental income

- Depreciation creates paper losses that offset real taxable income — 27.5 years for residential, 39 for commercial properties

- 1031 exchanges allow indefinite deferral of capital gains taxes by reinvesting proceeds into replacement properties

- The pass-through (QBI) deduction lets eligible investors deduct up to 20% of qualified rental business income

- Cost segregation accelerates depreciation on specific components, front-loading six-figure deductions into year one instead of spreading them over decades

Why Real Estate Investing Comes With Exceptional Tax Advantages

Rental income receives preferential treatment under U.S. tax law. Unlike earned income, rental revenue is not subject to the 15.3% FICA (self-employment) tax. That alone saves investors up to 15.3% compared to self-employed individuals earning the same amount through active business income.

The concept of "paper losses" is equally powerful. Depreciation and other non-cash deductions can offset real cash income, legally reducing taxable income even during profitable years. You can collect positive cash flow while reporting a tax loss — a combination few other investment vehicles allow.

The core advantages that make real estate uniquely tax-efficient include:

- Rental income exempt from self-employment taxes

- Non-cash deductions (depreciation) that offset real profits

- Strategies that work in combination to amplify total savings

The sections below break down each of these benefits and how to apply them.

Top Tax Benefits for Real Estate Investors

Real estate investors have access to some of the most favorable tax treatment in the U.S. tax code. These benefits apply across property types—residential, commercial, short-term rentals, and multi-family—though eligibility and limits vary by situation. Work with a qualified CPA or tax advisor who specializes in real estate to confirm what applies to your portfolio.

Operating Expense Deductions

Investors can deduct virtually all ordinary and necessary costs of owning and managing a property:

- Mortgage interest

- Property taxes (fully deductible for investment properties, not subject to the $10,000 SALT cap)

- Landlord insurance

- Property management fees

- Maintenance and repair costs

- Advertising

- Legal and accounting fees

- Travel related to property management

Recordkeeping is critical. Retain receipts, invoices, and bank statements for at least 3–7 years in case of an IRS audit, especially for higher-value deductions. Property records used to calculate basis and depreciation must be kept until the period of limitations expires for the year you dispose of the property in a taxable transaction.

Depreciation (Straight-Line)

The IRS allows you to deduct the cost of a residential property (excluding land) over 27.5 years, or a commercial property over 39 years. This happens even while the property appreciates in market value — a rare case where the tax code works in an investor's favor regardless of performance.

Example: If you purchase a residential rental property with a building value of $275,000, you can deduct $10,000 annually ($275,000 ÷ 27.5 years) as depreciation.

Important: Depreciation recapture applies when you sell — the IRS taxes previously claimed depreciation at up to 25%. That's why deferral strategies like the 1031 exchange are commonly paired with depreciation planning.

Cost segregation takes this further by accelerating depreciation through an engineering analysis that reclassifies building components into shorter recovery periods (5, 7, or 15 years). Instead of spreading deductions over 27.5 years, investors can front-load significant deductions in years one through five.

The Pass-Through (QBI) Deduction

Investors who own rental properties through pass-through entities—sole proprietorships, LLCs, S-Corps, or partnerships—may deduct up to 20% of qualified business income (QBI) on their personal tax return under Section 199A.

Income thresholds for 2024:

- Married Filing Jointly: Phase-out range of $383,900 to $483,900

- Single/Other filers: Phase-out range of $191,950 to $241,950

To qualify under the safe harbor established by the IRS, you must maintain separate books and records for each rental enterprise and perform at least 250 hours of rental services annually with contemporaneous documentation.

Long-Term Capital Gains Treatment

The holding period of your property directly impacts tax liability at sale:

- Short-term: Properties held one year or less generate short-term capital gains, taxed as ordinary income

- Long-term: Properties held more than one year qualify for preferential rates of 0%, 15%, or 20% based on your taxable income

At lower income levels, some investors owe $0 in capital gains tax on a profitable sale. For investors in the 0% bracket, a buy-and-hold strategy can mean walking away from a gain entirely tax-free.

The 1031 Exchange

A 1031 (like-kind) exchange allows you to sell an investment property and defer paying capital gains taxes entirely, as long as sale proceeds are reinvested into a new property of equal or greater value within IRS-defined timeframes:

- 45-day identification window: You must identify replacement property in writing within 45 days of transferring the relinquished property

- 180-day closing window: You must receive the replacement property within 180 days or by your tax return due date, whichever comes first

Key limitations:

- Must use a qualified intermediary to facilitate the exchange

- Applies only to investment or business property (not primary residences)

- Cannot access proceeds during the exchange without triggering taxable recognition

- Deferred gains eventually become due upon a taxable sale

However, successive 1031 exchanges can defer taxes indefinitely. When property passes to heirs at death, they receive a stepped-up basis under IRC §1014, potentially eliminating the deferred gain entirely.

Opportunity Zone Investments

The IRS designates certain economically distressed areas as Opportunity Zones. Investors who place unrealized capital gains into a Qualified Opportunity Fund (QOF) can:

- Defer capital gains until the earlier of the QOF investment sale or December 31, 2026

- Exclude post-acquisition appreciation permanently if the QOF investment is held for at least 10 years

Most advisors consider this strategy meaningful for investors with at least $500,000 in unrealized gains. Vetting the QOF sponsor's track record is essential — the tax benefits are only as strong as the underlying investment performing over a 10-year hold.

Cost Segregation: The Most Powerful (and Most Overlooked) Tax Tool for Investors

Cost segregation is an IRS-compliant engineering study that reclassifies building components—flooring, lighting, landscaping, electrical systems, cabinetry—from 27.5- or 39-year depreciation schedules to accelerated 5-, 7-, or 15-year schedules. This allows you to front-load years of depreciation into the first year of ownership.

Instead of claiming 1/27.5th of a building's value each year, you can reclassify 20–40% or more of a property's cost into shorter-lived assets and claim those deductions immediately.

The Bonus Depreciation Connection

Under current tax law following the One Big Beautiful Bill Act signed in 2025, assets with a useful life under 20 years qualify for **100% bonus depreciation** for property placed in service after January 19, 2025. When combined with cost segregation, this combination can produce six-figure first-year deductions.

To put that in concrete terms: a multi-family property purchased for $1.5 million might generate a first-year deduction well into six figures. Across more than 10,200 properties studied nationwide, Seneca Cost Segregation reports an average first-year deduction of $171,243.

Who Benefits Most

Cost segregation delivers the highest ROI for:

- Investors who purchased or renovated a property worth $500,000+ in the last several years

- Those in higher income tax brackets

- Investors with passive income they want to offset

- Property owners who need immediate cash flow improvements

Already own properties you purchased in prior years? You may still qualify. You can apply cost segregation retroactively through a look-back study via IRS Form 3115 (change in accounting method), claiming missed depreciation in the current year without amending prior returns.

Seneca Cost Segregation conducts engineering-based studies—backed by AuditDefense and a money-back guarantee—typically completed within 2–4 weeks for investors across all 50 states.

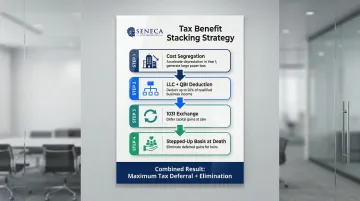

How to Stack These Tax Benefits for Maximum Tax Savings

These tax benefits compound when used in combination. Here's what a well-structured strategy can look like:

Example stack:

- Use cost segregation to accelerate depreciation in year one (generating a large paper loss)

- Structure ownership through an LLC to access the QBI deduction (up to 20% additional deduction)

- Use a 1031 exchange when selling to defer capital gains

- Hold until death for stepped-up basis, eliminating deferred gains for heirs

Real Estate Professional Status

Achieving "real estate professional" tax status requires spending more than 750 hours per year materially participating in real estate activities. That status lets you use passive real estate losses to offset active W-2 or business income, which can dramatically increase the value of accelerated depreciation deductions.

Not pursuing professional status? Short-term rental properties with average stays of 7 days or fewer can offer similar loss-offsetting benefits, provided you meet material participation tests — no professional status required.

Key qualifications to keep in mind:

- 750-hour threshold: Must be documented with time logs for IRS scrutiny

- Material participation: Applies separately to each rental activity unless you group them

- STR exception: Average stay of 7 days or fewer triggers non-passive treatment

Before filing: Work with a CPA who specializes in real estate investing, not a generalist. And commission a cost segregation study in the same tax year you purchase a property — retroactive studies are possible but add cost and complexity.

Conclusion

Real estate is one of the most tax-advantaged investment vehicles in the U.S. tax code. The investors who capture those advantages, though, are the ones who actively use them — not just those who happen to own property.

Cost segregation, in particular, is the strategy most investors overlook — despite it routinely delivering the largest single-year tax savings of any approach available. Commissioning an engineering-based study is one of the highest-ROI decisions a property owner can make.

Ready to maximize your tax benefits? Reach out to Seneca Cost Segregation for a complimentary tax assessment to find out how much you could save. With over 10,200 properties assessed, a 95% client referral rate, and an average first-year deduction of $171,243, Seneca's team of Certified Cost Segregation Professionals serves investors in all 50 states.

Frequently Asked Questions

What are the tax advantages of investing in real estate?

Real estate offers operating expense deductions, depreciation over 27.5–39 years, preferential long-term capital gains rates (0%–20%), 1031 exchange deferral, and exemption from the 15.3% self-employment tax on rental income—creating multiple layers of tax savings.

What is the most overlooked tax deduction for real estate investors?

Cost segregation is the most underutilized benefit. It accelerates depreciation by reclassifying 20–40% of building costs into shorter depreciation schedules, often generating six-figure first-year deductions that most investors never claim because they don't know the strategy exists.

What is the maximum tax deduction for real estate taxes?

For investment properties, property taxes paid are fully deductible as a business expense on Schedule E. Unlike personal residences, they are not subject to the $10,000 SALT cap that applies to Schedule A itemized deductions.

Can you avoid capital gains tax by using a 1031 exchange when reinvesting in real estate?

A 1031 exchange defers (but does not permanently eliminate) capital gains tax. If you hold the replacement property until death, your heirs receive a stepped-up cost basis under IRC §1014 — which can effectively eliminate the deferred gain entirely.

What are the downsides of using a 1031 exchange?

Strict IRS timelines require identifying replacement property within 45 days and closing within 180 days. You must use a qualified intermediary and cannot access proceeds during the exchange. Depreciation recapture is also deferred, not eliminated — it becomes due at the time of a future taxable sale.

What is the 2-Year Rule for a 1031 Exchange?

Under IRC §1031(f), related-party exchanges require both parties to hold their properties for at least 2 years post-exchange, or the tax deferral is disallowed. Confirm current rules with a qualified intermediary or tax advisor before proceeding.