Introduction

In 2021, real estate investors collectively reported $2.1 trillion in capital gains—yet another $0.3 trillion legally escaped taxation through exclusions and deferral strategies. That gap isn't luck. Capital gains tax on real estate is not a fixed, unavoidable cost — the amount you owe is shaped by decisions made before you purchase, during ownership, and at the point of sale. Most investors overpay simply because they don't know where the liability originates.

Knowing where tax liability builds — and where it can be reduced — often means the difference between paying full freight and saving six figures. This guide covers how liability accumulates, what factors amplify it, and three strategy categories that legally reduce what you owe: planning decisions, ownership tactics, and transaction structuring.

TL;DR

- Capital gains tax is triggered by the gap between your sale price and adjusted cost basis—lower basis or shorter holding periods mean higher bills

- Long-term rates (0%, 15%, or 20%) apply only after one year of ownership; earlier sales face ordinary income rates up to 37%

- IRS-sanctioned strategies like the primary residence exclusion, 1031 exchanges, and accelerated depreciation can reduce or defer your tax bill substantially

- Front-loading depreciation through cost segregation improves cash flow and cuts your effective tax burden during ownership

- Stacking strategies early—not just at closing—delivers the biggest cumulative tax savings

How Capital Gains Tax Liability Typically Builds Up on Real Estate

Capital gains tax liability hits as a single taxable event at sale, but its size is shaped by decisions made across the entire ownership period: purchase price, improvements made, depreciation claimed, and holding duration.

Adjusted Cost Basis: The Foundation of Your Tax Bill

Your adjusted cost basis determines how much gain is taxable. The IRS defines basis as your original purchase price plus acquisition costs. Every capital improvement — roof replacements, HVAC upgrades, kitchen remodels — increases your basis and reduces your eventual gain.

Conversely, every depreciation deduction you claim lowers your basis and increases your exposure to depreciation recapture tax at sale. Tracking both carefully throughout ownership is essential.

Short-Term vs. Long-Term: A Tens-of-Thousands-Dollar Difference

The most consequential classification is whether your gain is short-term or long-term. The IRS draws a hard line at one year of ownership:

Short-term capital gains (≤1 year): Taxed as ordinary income at rates up to 37%

Long-term capital gains (>1 year): Taxed at preferential rates of 0%, 15%, or 20%

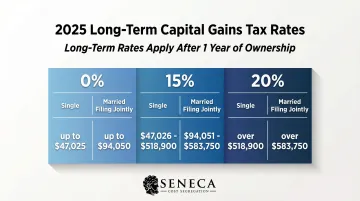

Selling a property after 11 months versus 13 months can mean tens of thousands of dollars in extra taxes on the same sale. Each bracket threshold represents the upper limit of taxable income at that rate — once your income exceeds the 15% ceiling, the excess is taxed at 20%. The 2025 long-term capital gains brackets are:

| Filing Status | 0% Rate Up To | 15% Rate Up To | 20% Rate Applies Above |

|---|---|---|---|

| Single | $48,350 | $533,400 | $533,400 |

| Married Filing Jointly | $96,700 | $600,050 | $600,050 |

Knowing which bracket you fall into before you sell gives you time to plan — and potentially restructure the transaction to reduce what you owe.

Key Factors That Drive Your Capital Gains Tax Bill

Four primary cost drivers determine your final tax burden:

1. Sale Price Appreciation Above Adjusted Basis

The larger the gap between your sale price and adjusted basis, the higher your taxable gain. This is the single largest variable.

2. Depreciation Recapture

Unrecaptured Section 1250 depreciation is taxed at up to 25%—separately from the capital gain. The IRS reclaims the tax benefit of prior depreciation deductions, meaning investors who never claimed depreciation still owe the recapture tax—without ever getting the deduction.

3. Income Bracket and Filing Status

Your taxable income determines which long-term rate tier (0%, 15%, or 20%) applies. High earners may also face the 3.8% Net Investment Income Tax (NIIT), which triggers at $200,000 MAGI for single filers and $250,000 for married filing jointly.

4. Exemption Eligibility

Properties qualifying for the primary residence exclusion or structured through 1031 exchanges face dramatically different tax consequences than standard sales.

When Your Decisions Matter Most

Understanding these four drivers matters, but timing matters just as much. The tax burden is shaped more by decisions made early—purchase structure, property classification, depreciation tracking—than by anything done at closing. Which variable dominates depends on your property type:

- Primary homeowners: Exclusion eligibility is typically the key variable

- Rental investors: Depreciation recapture and accumulated gains dominate

- Commercial property owners: Holding period and transaction structure carry the most weight

Strategies to Reduce Capital Gains Tax on Real Estate

The right strategy depends on when you act. Some options only exist before you purchase or during ownership; others must be executed at or after the point of sale. Combining strategies from each stage produces the greatest reduction.

Strategies That Reduce Tax by Changing Planning Decisions

These approaches are taken before or shortly after acquiring a property and establish lower tax liability from the outset.

Optimize Your Adjusted Cost Basis from Day One

Keep meticulous records of all capital improvements, purchase closing costs, and legal fees. These additions raise your basis and directly reduce the taxable gain when you sell. Many investors lose thousands in potential deductions simply by failing to document improvement costs.

Use the Primary Residence Exclusion Strategically

Under IRS Section 121, single filers can exclude up to $250,000 of gain and married filers up to $500,000, provided they:

- Owned and lived in the home for at least two of the five years preceding the sale

- Haven't used the exclusion within the past two years

This requires intentional planning around occupancy timing. If you fail the two-year test but sell due to employment change (new job at least 50 miles farther away), health reasons, or unforeseen circumstances (death, divorce, disaster), you may qualify for a prorated partial exclusion.

Extend Your Holding Period Deliberately

Confirm whether a property is on track to cross the 12-month threshold before listing. Any gain recognized before that point is taxed as ordinary income (potentially 10%–37%) rather than at the preferential long-term rate (0%–20%). A few extra weeks of ownership can save thousands.

Classify Property Use Carefully at Acquisition

Decisions about whether a property is a primary residence, rental, or mixed-use asset determine which tax rules apply throughout the ownership period and at sale. Reclassifying later creates complications and missed planning windows.

Strategies That Reduce Tax Through Active Ownership Choices

These ongoing actions during ownership reduce taxable income, lower the adjusted basis trajectory in a planned way, and front-load deductions.

Claim Depreciation Consistently Every Year

Residential rental properties depreciate over 27.5 years and commercial over 39 years. Failing to claim this deduction doesn't eliminate the recapture obligation at sale—investors who skip it lose the benefit but still pay the tax.

Accelerate Depreciation Through Cost Segregation

An engineering-based cost segregation study identifies building components—flooring, fixtures, landscaping, electrical systems—that qualify for 5-, 7-, or 15-year depreciation schedules rather than the standard 27.5 or 39 years. This front-loads substantial deductions in the early years of ownership.

A review of over 8,000 cost segregation studies found that 20% to 30% of a building's depreciable basis can be reclassified to accelerated schedules. With 100% bonus depreciation restored for property acquired after January 19, 2025, these front-loaded deductions can eliminate federal tax liability in year one for qualifying properties.

Seneca Cost Segregation's engineering-based studies have delivered an average first-year deduction of over $171,000 across more than 10,200 properties assessed.

Deduct All Eligible Operating Expenses

Deductible operating expenses reduce net taxable rental income every year the property is held. Common eligible expenses include:

- Property management fees and landlord insurance

- HOA dues and advertising costs

- Repairs (not capital improvements)

- Legal and accounting fees

- Travel directly related to managing the property

Use Tax-Loss Harvesting Across Your Portfolio

If you hold other assets (stocks, funds) with unrealized losses, selling them in the same tax year as a real estate gain can offset the capital gain dollar-for-dollar. Unlike equities, real estate is exempt from the IRS wash-sale rule, allowing immediate reinvestment after harvesting losses. You can offset up to $3,000 of ordinary income annually ($1,500 if married filing separately), with unused losses carrying forward indefinitely.

Strategies That Reduce Tax by Changing the Transaction Context

These approaches alter the structure, timing, or destination of sale proceeds to defer or reduce the tax event itself.

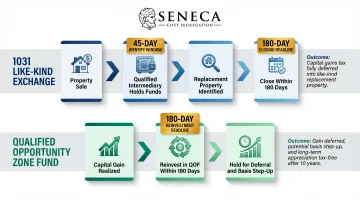

Execute a 1031 Like-Kind Exchange

Reinvesting proceeds from a rental or investment property sale into similar property within IRS-mandated timelines—45 days to identify, 180 days to close—defers the entire capital gains and depreciation recapture tax liability to the replacement property. A Qualified Intermediary must hold the funds; receiving cash directly triggers immediate constructive receipt and voids the exchange.

Investors can roll exchanges forward indefinitely, and heirs receive a stepped-up basis under IRC Section 1014 that can eliminate the accumulated deferred gain entirely.

Invest Eligible Gains Into a Qualified Opportunity Zone Fund

Capital gains reinvested into a Qualified Opportunity Fund (QOF) within 180 days of a property sale can qualify for deferral. The 2025 One Big Beautiful Bill Act made the OZ program permanent, replacing the fixed 2026 sunset with a rolling 5-year deferral period. Investments held for 30 years can qualify for a stepped-up basis, potentially excluding post-acquisition appreciation entirely.

For investors in designated rural zones, Qualified Rural Opportunity Funds (QROFs) offer an additional incentive: a 30% basis step-up after a 5-year hold.

Donate Appreciated Property to Charity

Transferring property to a qualified 501(c)(3) organization eliminates capital gains tax on appreciation entirely. The donor receives a charitable deduction for the fair market value at time of donation, limited to 30% of AGI for public charities or 20% for private foundations.

A Charitable Remainder Trust (CRT) allows you to transfer appreciated property into an irrevocable trust that sells the property tax-free, reinvests the proceeds, and pays you an income stream for life or up to 20 years. The remaining assets pass to charity at the end of the term.

Plan for the Step-Up in Basis Through Estate Transfer

If a property is passed to heirs rather than sold, the adjusted basis resets to the fair market value at the time of death—effectively erasing decades of accumulated capital gain. This makes inheritance planning a meaningful capital gains elimination strategy for long-term holders.

Conclusion

Reducing capital gains tax on real estate comes down to understanding exactly where your liability originates — basis, holding period, depreciation recapture, transaction structure — and applying the right strategy at each stage of ownership.

The investors who pay the least in capital gains taxes are those who plan continuously across the ownership lifecycle—not those who scramble at listing. A cost segregation study, a well-timed 1031 exchange, and a documented improvement record can collectively shift what looks like a large tax event into a fraction of its original size. The earlier you put these tools in place, the more of that gain stays in your pocket.

Frequently Asked Questions

How can I avoid paying taxes on my investment property?

Complete avoidance is rare, but significant reduction or indefinite deferral is achievable. Common approaches include 1031 exchanges to defer gains, cost segregation to reduce taxable income during ownership, and stepped-up basis at inheritance to permanently eliminate accumulated gains.

What reduces capital gains tax on real estate?

The most impactful levers are increasing your adjusted cost basis through documented improvements, holding the property over one year to qualify for long-term rates, claiming depreciation deductions (including via cost segregation), and using the primary residence exclusion if eligible.

What is depreciation recapture and how does it affect capital gains tax?

Depreciation recapture requires investors to pay tax (up to 25%) on the depreciation they claimed when they sell, calculated separately from the capital gain. Plan around recapture exposure rather than forgoing depreciation deductions entirely.

Can I use a 1031 exchange to avoid capital gains tax forever?

A 1031 exchange defers—not eliminates—capital gains tax, allowing investors to roll proceeds into new properties indefinitely. If the property is eventually passed to heirs, the stepped-up basis can permanently eliminate the deferred liability.

Does cost segregation help reduce capital gains tax on real estate?

Cost segregation reduces taxable income during ownership by accelerating depreciation deductions, improving cash flow and lowering your tax burden. It does increase depreciation recapture exposure at sale, so it works best alongside a deferral strategy.

What is the primary residence exclusion for capital gains tax?

The IRS allows single filers to exclude up to $250,000 in gains—and married couples filing jointly up to $500,000—from the sale of a primary residence. You must have owned and lived in the home for at least two of the five years before the sale and not used the exclusion in the prior two years.