Introduction

Selling a rental property can trigger a tax bill that catches even experienced investors off guard. According to the Tax Foundation, the average effective tax rate on realized capital gains was 15.1% in 2024 and is estimated at 18.0% for 2025 — but that figure alone understates what rental property sellers actually owe.

Taxes on a rental property sale aren't just capital gains. They layer in depreciation recapture (taxed at up to 25%), state taxes, and potentially the 3.8% Net Investment Income Tax (NIIT). What looks like a clean profit on paper becomes a complex, multi-line tax event when you file.

The good news: there are legal strategies to reduce each of these tax layers. This article covers the most effective ones — from 1031 exchanges and installment sales that defer what you owe, to cost segregation and opportunity zone investing that can reduce or eliminate it outright. Whether you're planning ahead or already under contract, you'll find actionable options here.

TLDR

- Rental property sales trigger multiple tax events: long-term capital gains (0–20%), depreciation recapture (up to 25%), and potentially the 3.8% NIIT

- Your holding period, adjusted cost basis, and total depreciation claimed determine your final tax bill

- Pre-sale strategies like 1031 exchanges or primary residence conversion offer the highest leverage for tax reduction

- Property management decisions—tracking capital improvements and accelerating depreciation through cost segregation—directly reduce your taxable gain

- Transaction structures like installment sales or Qualified Opportunity Zone reinvestment can defer or eliminate taxes entirely

How Your Tax Liability Builds Up When You Sell a Rental Property

The taxable gain at sale is not simply "sale price minus purchase price." The IRS uses a more complex formula that accounts for every dollar of depreciation you've claimed over the years.

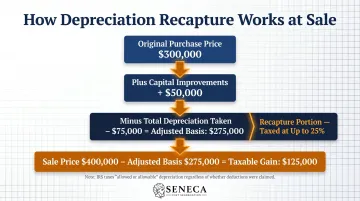

Your adjusted cost basis equals: Original purchase price + capital improvements − total depreciation taken = adjusted basis. The IRS defines this as "your original cost or other basis increased by certain additions and decreased by certain deductions."

Consider a property purchased for $300,000 with $50,000 in improvements and $75,000 in depreciation. The adjusted basis drops to $275,000. Sell for $400,000, and your taxable gain is $125,000—nearly triple the $50,000 in price appreciation you actually realized.

This process, called depreciation recapture, catches many investors off guard. The IRS taxes "unrecaptured Section 1250 gain at a maximum 25% rate"—meaning every depreciation deduction you took during ownership comes back as taxable income at sale.

The tax burden compounds further when:

- The gain is short-term (held one year or less), taxed as ordinary income up to 37% federally

- The seller has high taxable income, triggering the 20% long-term rate plus 3.8% NIIT

- State-level capital gains taxes apply, which vary widely by jurisdiction

Understanding exactly where your liability comes from is the first step—the strategies that follow address each of these pressure points directly.

Key Factors That Determine Your Tax Bill at Sale

Holding Period

The primary driver is your holding period. Assets held over one year qualify for long-term capital gains rates (0%, 15%, or 20%), while those held one year or less are taxed as ordinary income—reaching 37% federally in 2025.

2025 Long-Term Capital Gains Thresholds:

- 0% rate: Single filers up to $48,350 taxable income; married filing jointly up to $96,700

- 15% rate: Single filers $48,351 to $533,400; married filing jointly $96,701 to $600,050

- 20% rate: Above these thresholds

Source: IRS Rev. Proc. 2024-40

Total Depreciation Claimed

The second major driver is total depreciation claimed over ownership. All prior depreciation is subject to recapture at up to 25% regardless of the long-term capital gains rate.

Here's the critical point: the IRS taxes "allowed or allowable" depreciation. Failing to claim depreciation during ownership does not avoid this—you're taxed on the depreciation you should have taken.

Income Level and Filing Status

Your adjusted gross income and filing status determine whether the 0%, 15%, or 20% capital gains rate applies. They also determine whether the 3.8% NIIT is triggered, which applies when your modified adjusted gross income exceeds $200,000 (single) or $250,000 (married filing jointly).

Timing matters here. Strategies like deferring other income, bunching deductions, or spreading a sale across tax years via installment reporting can shift you into a lower bracket — cutting your effective rate before the sale closes.

Strategies That Reduce Taxes by Changing Pre-Sale Decisions

The most powerful tax-reduction moves happen before the sale closes. How you time the sale, where proceeds go, and how you use the property beforehand can each cut your tax bill significantly — or eliminate it entirely.

Defer Taxes by Reinvesting Into Like-Kind Property (1031 Exchange)

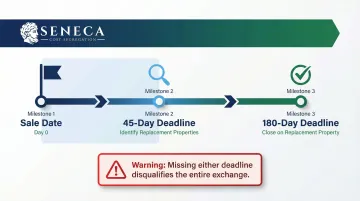

A 1031 exchange allows sellers to defer all capital gains and depreciation recapture taxes by reinvesting proceeds into a "like-kind" replacement property. The deferred tax carries forward into the new property's basis rather than being eliminated.

Critical IRS deadlines:

- 45 days to identify potential replacement properties

- 180 days to close on the replacement property

Both deadlines run from the sale date of your relinquished property. Missing either deadline disqualifies the entire exchange.

Delaware Statutory Trusts (DSTs) qualify as 1031 replacement properties under IRS Rev. Rul. 2004-86. This makes them practical for investors who want to exit active property management while still deferring taxes through passive, institutional-grade real estate investments.

According to the Real Estate Roundtable, 15-20% of commercial transactions involve a like-kind exchange.

Convert the Rental to a Primary Residence Before Selling

Moving into a rental and living there as your primary residence for at least two of the five years before the sale may qualify you for the IRS Section 121 exclusion — up to $250,000 for single filers or $500,000 for married filing jointly. This exclusion directly reduces your taxable gain.

One significant caveat: depreciation recapture still applies and cannot be excluded. Any depreciation taken after May 6, 1997 is recaptured at up to 25%, regardless of how long you lived in the property.

Time the Sale Around Income Levels

Sellers who expect significantly lower taxable income in a future tax year can reduce or eliminate capital gains tax by timing the sale to fall when their income places them in the 0% bracket.

For 2025, the 0% long-term capital gains rate applies to:

- Single filers with taxable income up to $48,350

- Married filing jointly with taxable income up to $96,700

Source: IRS Rev. Proc. 2024-40

Timing the sale to coincide with retirement, a business loss year, or a year with significant deductions can eliminate federal capital gains tax entirely.

Strategies That Reduce Taxes by Changing How the Property Was Managed

Tax liability at sale is heavily shaped by decisions made during ownership—particularly how depreciation was handled, what improvements were tracked, and whether the property's depreciation potential was fully maximized.

Accelerate Depreciation with a Cost Segregation Study

A cost segregation study identifies property components—flooring, fixtures, landscaping, HVAC, appliances—that can be depreciated over 5, 7, or 15 years instead of the standard 27.5 years for residential rental property.

This generates significantly larger deductions in early ownership years. According to an ASCSP case study on a luxury apartment complex, approximately 20% of a property's total purchase price was reclassified into 5-year and 15-year property categories, substantially accelerating first-year depreciation.

That front-loaded depreciation can produce passive losses that offset other income. When the property is sold, any suspended passive losses are released and can offset the gain at sale under IRC §469, reducing your overall tax liability.

Seneca Cost Segregation conducts engineering-based cost segregation studies with licensed professional engineers, supporting IRS-compliant reclassification and providing audit defense if deductions are ever challenged.

Track Capital Improvements to Maximize Your Adjusted Cost Basis

Every qualifying capital improvement—roof replacements, HVAC systems, additions, major renovations—increases your adjusted cost basis, which directly reduces the taxable gain at sale.

Many investors fail to maintain records of improvements and end up overpaying taxes on gains that were partially funded by capital they already spent. Keep detailed receipts, invoices, and project documentation for:

- Structural additions or renovations

- New roofs, HVAC systems, or major appliances

- Paving, landscaping, or site improvements

- Electrical or plumbing upgrades

These aren't deductible as current expenses—they must be capitalized and depreciated over time. At sale, they increase your basis and reduce your taxable gain dollar-for-dollar.

Use Tax-Loss Harvesting to Offset Sale Gains

If you have capital losses in the same tax year from other investments—stocks, REITs, other properties—those losses can offset gains from the rental property sale dollar-for-dollar.

The IRS allows you to:

- Offset capital gains with capital losses

- Deduct up to $3,000 of excess losses against ordinary income ($1,500 if married filing separately)

- Carry forward unused losses to future tax years

Use IRS Form 8949 and Schedule D to calculate and report this netting. Any carryforward losses from prior years apply against current-year gains as well.

Deduct Allowable Sale-Related Expenses

Direct costs of selling the property reduce the amount realized from the sale and therefore reduce the taxable gain. According to IRS Publication 544, selling expenses include:

- Real estate agent commissions

- Legal fees

- Title insurance and escrow fees

- Transfer taxes

- Recording fees

- Advertising costs

These expenses are not separately deductible—they reduce your sales proceeds for purposes of calculating gain. Keep documentation of all selling costs to maximize this benefit.

Strategies That Reduce Taxes by Changing the Context Around the Sale

Some tax-reduction strategies work not by changing the property or its management, but by changing the structure of the transaction, the reinvestment destination, or the ownership and estate context.

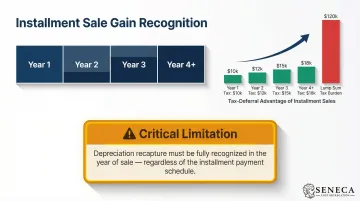

Use an Installment Sale to Spread the Tax Burden

Structuring the sale as an installment sale (seller financing) spreads the recognized taxable gain across multiple years as payments are received, rather than creating a single large tax event.

Under IRC §453, an installment sale is "a sale of property where you receive at least one payment after the tax year of sale." Gain is recognized proportionally as payments are received.

This can:

- Keep the seller in a lower tax bracket each year

- Potentially reduce the applicable capital gains rate

- Avoid NIIT thresholds

Critical limitation: Under IRC §453(i), all depreciation recapture must be recognized in the year of sale, even if no payments are received. Only the capital appreciation portion of the gain can be spread. Report installment sale income on IRS Form 6252. For investors whose gains span multiple tax brackets, this structuring choice alone can shift the effective rate on a portion of the gain.

Invest Capital Gains Into a Qualified Opportunity Zone (QOZ) Fund

By reinvesting the capital gain (not total proceeds) into a Qualified Opportunity Fund within 180 days of sale, investors can defer recognition of that gain.

Current QOZ rules provide:

- Deferral of capital gains until December 31, 2026 (or earlier sale of QOF interest)

- If held 10+ years, complete exclusion of appreciation on the QOF investment itself

2025 OBBBA Changes: The One Big Beautiful Bill Act made the QOZ program permanent but altered mechanics for investments after December 31, 2026. It introduced a rolling 5-year deferral and maintained the 10% basis step-up at year five, but eliminated the additional 5% step-up at year seven.

Plan for a Step-Up in Basis Through Estate and Gifting Strategies

Property passed to heirs at death receives a step-up in basis to fair market value at the time of death under IRC §1014, potentially eliminating all accumulated capital gains and depreciation recapture for the heirs. For older investors with heavily appreciated property and no pressing liquidity need, this can effectively zero out decades of embedded tax liability.

Estate planning strategies:

- Charitable Remainder Trusts (CRTs): Transfer appreciated property to an irrevocable CRT under IRC §664. The trust sells the asset tax-free and distributes income to beneficiaries over time.

- Family Limited Partnerships: Transfer property interests to family members at discounted valuations while retaining control

- Gifting strategies: Transfer property to lower-bracket family members before sale

Federal estate tax basic exclusion amounts are $13.99 million for 2025 and $15.0 million for 2026 — high enough that the majority of real estate investors can plan around these strategies without triggering estate tax exposure.

Conclusion

Reducing taxes on a rental property sale comes down to identifying where the taxable gain originates—capital appreciation, depreciation recapture, or both—and selecting strategies that address that specific source.

Pre-sale timing decisions, management choices during ownership, and transaction structuring all play distinct roles. A 1031 exchange defers everything. A primary residence conversion excludes capital gains but not recapture. Cost segregation accelerates deductions during ownership and releases passive losses at sale. No single approach fits every situation—the right combination depends on your property type, hold period, and income profile.

The most effective tax planning starts well before the sale closes. Investors who wait until a sale is under contract have already closed off most of their options. Structuring cost segregation, identifying passive losses, and evaluating exchange eligibility all require lead time—often months, not days. Working with a qualified tax advisor well before listing is where the real savings happen.

Frequently Asked Questions

How to avoid paying capital gains tax on sale of rental property?

Complete avoidance is rare, but deferral is achievable through several IRS-sanctioned strategies. A 1031 exchange defers all capital gains by reinvesting in like-kind property, a Section 121 conversion excludes up to $500,000 after two years as a primary residence, and Qualified Opportunity Zone Funds offer partial deferral and potential exclusion.

What expenses can be deducted from the sale of rental property?

Selling costs — commissions, legal fees, title insurance, transfer taxes, and escrow fees — reduce your amount realized and lower your taxable gain. Capital improvements made during ownership increase your adjusted cost basis, shrinking the gain further.

What are the tax implications if I sell my rental property?

You'll face three main tax events: long-term or short-term capital gains tax on appreciation (0%, 15%, or 20% for long-term; up to 37% for short-term), depreciation recapture taxed at up to 25%, and potentially the 3.8% Net Investment Income Tax if your income exceeds $200,000 (single) or $250,000 (married filing jointly).

What is the tax loophole for rental property?

The most used strategies — all IRS-sanctioned provisions, not loopholes — are the 1031 exchange (indefinite deferral of gains), the Section 121 exclusion (up to $500,000 for a converted primary residence), and the step-up in basis at death, which eliminates accumulated gains for heirs entirely.

What is depreciation recapture and how does it affect my rental property sale taxes?

Depreciation recapture is the IRS requirement to "repay" prior depreciation deductions at sale, taxed at a maximum rate of 25% on the recaptured amount. This applies whether or not you actually claimed depreciation during ownership—the IRS taxes "allowed or allowable" depreciation, meaning you're taxed on depreciation you should have taken.

Should I do a cost segregation study before selling my rental property?

A cost segregation study is most valuable when completed early in ownership, not right before selling. Done during ownership, it generates accelerated depreciation deductions and builds suspended passive losses that are fully released at sale to offset your taxable gain.