Introduction

Many rental property owners spend years unknowingly forfeiting six figures in tax deductions by skipping depreciation claims. The mistake is common — and fully correctable.

Whether you missed depreciation for one year or ten, the IRS provides two primary correction paths: amended returns (Form 1040-X) for single-year omissions and Form 3115 for multiple years.

Here's what most investors don't realize: even if you never claimed a penny of depreciation, the IRS still treats it as if you did. This "allowed or allowable" rule affects your tax bill when you sell — potentially triggering recapture tax on deductions you never actually took.

This article shows you how to recover missed depreciation before it becomes a permanent loss.

TLDR

- Missing depreciation is correctable—file Form 1040-X for one year or Form 3115 for multiple years

- The IRS reduces your property's cost basis by depreciation you were entitled to claim, whether or not you claimed it

- A retroactive cost segregation study can compound your catch-up deduction through bonus depreciation on 5-, 7-, and 15-year assets

- Recovering depreciation before you sell converts a future recapture liability into a current-year deduction

- Every year you wait, you risk paying up to 25% recapture tax on deductions you never claimed

What Is Rental Property Depreciation (and Why So Many Investors Miss It)

The IRS allows rental property owners to deduct the cost of the building structure (not land) over 27.5 years for residential properties or 39 years for commercial properties using the Modified Accelerated Cost Recovery System (MACRS). This annual deduction reduces taxable rental income each year, which translates directly to lower tax bills.

Common reasons investors miss depreciation:

- Self-prepared returns without understanding the deduction rules

- Accountant set up depreciation incorrectly or skipped it entirely

- Inherited property where prior filings were never reviewed

- Converted a primary residence to rental without restarting the depreciation clock

- Assumed depreciation would be "automatic" or handled by tax software

The mistake often goes undetected for years until a new CPA reviews the return. The longer it goes uncorrected, the larger the potential recovery. It also compounds a hidden problem at sale: the IRS still treats unclaimed depreciation as if it was taken, triggering depreciation recapture tax on deductions you never actually used.

The "Allowed or Allowable" Rule: Why Missing Depreciation Still Costs You

Under IRC Section 1016(a)(2), your adjusted cost basis in a rental property must be reduced by depreciation that was "allowable"—meaning the depreciation you were entitled to claim—regardless of whether you actually claimed it. IRS Publication 946 confirms this principle explicitly.

The Practical Consequence

If you owned a property for 10 years and claimed zero depreciation, your basis is still reduced by 10 years' worth of allowable depreciation when you sell. This creates phantom income—a taxable gain with no corresponding cash in your pocket—and you'll owe recapture tax on deductions you never actually received.

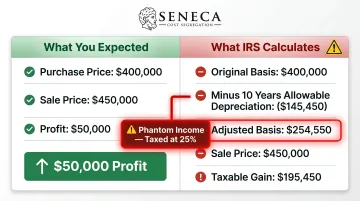

Example Scenario:

You purchased a residential rental property for $400,000 (excluding land value). Annual allowable depreciation is roughly $14,545 ($400,000 ÷ 27.5 years).

After 10 years without claiming depreciation:

- Total unclaimed depreciation: $145,450

- Original basis: $400,000

- Adjusted basis at sale (per IRS): $254,550

- Sale price: $450,000

- Taxable gain: $195,450 (not $50,000)

The difference between your actual profit ($50,000) and the IRS-calculated gain ($195,450) is $145,450—the exact amount of depreciation you never claimed but must now pay recapture tax on.

Depreciation Recapture Tax

That $145,450 in unclaimed depreciation doesn't disappear at sale—it gets recaptured. The IRS taxes previously allowed or allowable depreciation at a maximum rate of 25% under unrecaptured Section 1250 gain, whether or not you took the deductions.

In the example above, that means up to $36,363 in recapture tax on deductions you never received.

Why Acting Before You Sell Matters

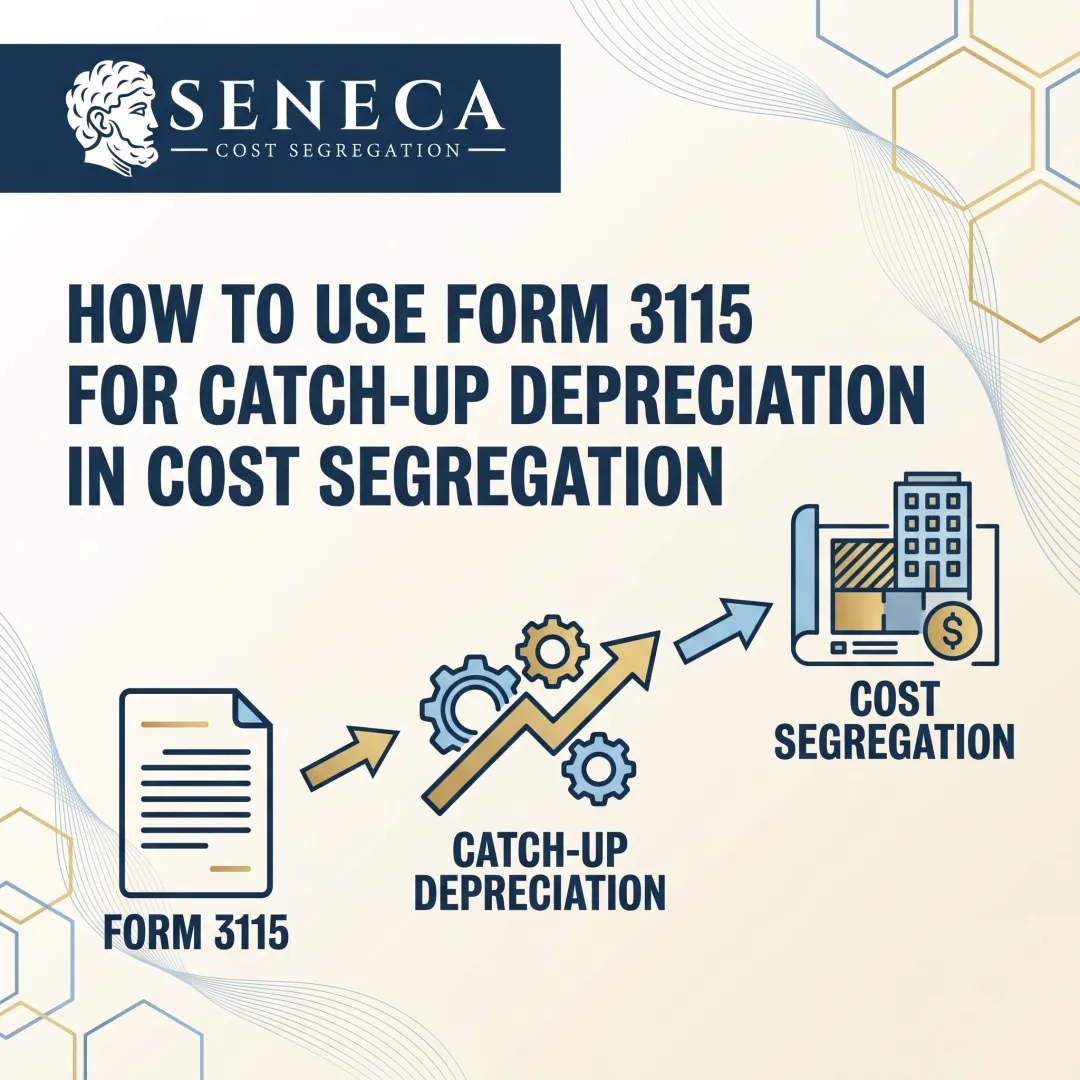

Recovering missed depreciation before a sale converts a future tax liability into a current-year deduction. The correction is typically filed via Form 3115 (Change in Accounting Method) and can be completed within a single tax year—turning years of forfeited deductions into immediate tax savings before you close.

How to Recover Missed Depreciation on Rental Property

There are two IRS-approved paths to recover missed depreciation, and which one applies depends on how many years were skipped.

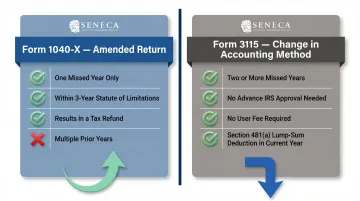

Option 1: File an Amended Return (Only for One Missed Year)

If depreciation was only missed in a single tax year and that year is still within the IRS statute of limitations—generally 3 years from the filing date—you can file an amended return (Form 1040-X) to correct the error and claim a refund for the missed deduction.

Key limitation: If depreciation was missed for two or more years, this option is no longer available for the earlier years. The IRS treats repeated failure to claim depreciation as adopting an impermissible accounting method — and that triggers a different corrective process entirely.

Option 2: File Form 3115—Change in Accounting Method (The Standard Fix)

Form 3115, Application for Change in Accounting Method, is the primary IRS-approved tool for correcting missed depreciation spanning two or more years. Under Revenue Procedure 2015-13, this is an automatic change—no advance IRS approval is needed and there is no user fee.

The Section 481(a) Adjustment

The total amount of missed depreciation across all prior years is calculated and claimed as a single lump-sum deduction in the current tax year. If the adjustment is negative (favorable to the taxpayer), it can be deducted in full in the year of the change.

For example: If you missed $145,450 in depreciation over 10 years, you claim the entire $145,450 deduction in the current year via the Section 481(a) adjustment.

Correct DCN Codes

- Code 7: Applies to assets still in use — covers the switch from not taking depreciation to taking it correctly going forward

- Code 107: Applies when the asset has already been sold or disposed of

What Form 3115 Cannot Do

Form 3115 cannot be used to make a late Section 179 election, change the date an asset was placed in service, or change the asset's use.

Filing Requirements

A copy of Form 3115 must be attached to the tax return for the year of change, and a signed copy must also be mailed to the IRS. Given the filing requirements and the size of the deductions involved, working with a qualified tax professional — or a cost segregation firm that handles depreciation corrections — significantly reduces the risk of errors that could delay or reduce your recovery.

How a Cost Segregation Study Maximizes Your Catch-Up Deductions

A standard catch-up via Form 3115 recovers only straight-line 27.5-year (or 39-year) depreciation. A cost segregation study goes much further.

What Cost Segregation Adds

An engineering-based cost segregation study reclassifies components of the building—flooring, cabinetry, specialty electrical, parking lots, landscaping—into 5-, 7-, or 15-year property classes. These shorter-lived assets qualify for accelerated depreciation and potentially bonus depreciation.

According to American Society of Cost Segregation Professionals (ASCSP) case studies, engineering-based studies typically reclassify 20% to 25% of a building's total purchase price into accelerated categories.

The Compounded Recovery

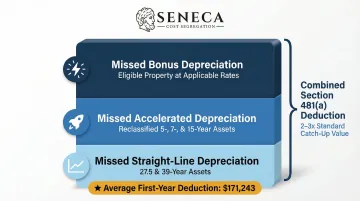

When a cost segregation study is performed retroactively, the Section 481(a) adjustment on Form 3115 captures:

- Missed straight-line depreciation (27.5 or 39 years)

- Missed accelerated depreciation on reclassified 5-, 7-, and 15-year assets

- Missed bonus depreciation on eligible property

For a property purchased several years ago, this can mean a deduction two to three times larger than a standard straight-line catch-up.

Bonus depreciation eligibility depends on when the property was acquired — rates differ sharply:

Bonus depreciation rates for 2026:

- 100% bonus depreciation for property acquired after January 19, 2025

- 20% bonus depreciation for property acquired before January 19, 2025

Income Offset Potential

This larger deduction can offset:

- Rental income from the subject property

- Passive gains from other rental properties

- Active income for investors qualifying under Real Estate Professional Status (REPS) or the Short-Term Rental (STR) loophole (average use ≤ 7 days)

For investors who have held property for several years without a study, a retroactive cost segregation analysis can recover all three categories at once. Seneca Cost Segregation has completed over 10,200 engineering-based studies nationwide, with an average first-year deduction of $171,243, a 2–4 week turnaround, and AuditDefense backed by a money-back guarantee.

What Happens If You Never Claimed Depreciation and Then Sell?

The Worst-Case Scenario

If you sell a rental property without ever having corrected missed depreciation, you still face depreciation recapture on the full "allowed or allowable" amount—paying up to 25% on deductions you never actually received. This is effectively a double penalty.

Post-Sale Correction

Code 107 on Form 3115 allows you to catch up omitted depreciation on a disposed asset. Acting before the sale delivers the greatest benefit — once the property closes, your recovery options narrow significantly and the recapture liability stays on the books.

Basis Impact on Capital Gains

The "allowed or allowable" rule reduces your adjusted basis whether or not you claimed the deduction. That lower basis means:

- Higher recognized gain on sale

- Potentially higher total tax liability (capital gains + recapture)

Correcting missed depreciation before selling puts the deduction in your pocket first — so when recapture hits, you've already used those dollars to offset taxable income.

Frequently Asked Questions

Can I claim missed depreciation on rental property for previous years?

Yes. Missed depreciation can be recovered through an amended return (Form 1040-X) for one missed year within the statute of limitations, or through Form 3115 for multiple missed years, with all unclaimed amounts deducted as a Section 481(a) adjustment in the current year.

How far back can I claim depreciation on rental property?

Form 3115 has no hard lookback limit for the catch-up calculation. The Section 481(a) adjustment can include all missed depreciation back to when the property was placed in service. Amended returns are limited to the 3-year statute of limitations window.

What happens if you never took depreciation on a property and then sold it?

The IRS still reduces your adjusted basis by the "allowed or allowable" depreciation, meaning you pay recapture tax (up to 25%) on deductions you never took—resulting in a higher taxable gain with no offsetting benefit.

What happens if you forget to take depreciation on rental property?

Forgetting depreciation for one year can be corrected with an amended return. Two or more years of omission is treated as an impermissible accounting method requiring Form 3115 to correct. Either way, the IRS still reduces your basis for the missed years.

Is it worth doing a cost segregation study to recover missed depreciation?

For properties with a cost basis above $500,000, a cost segregation study can multiply the catch-up deduction well beyond straight-line recovery, often producing immediate tax savings that far exceed the study's cost. Properties below this threshold may still qualify. Contact Seneca Cost Segregation for a complimentary preliminary analysis to find out.

Missed depreciation has a real cost. Every year you go without correcting it, your tax basis erodes further—and any future sale triggers recapture on deductions you never received. Contact Seneca Cost Segregation for a free preliminary analysis and find out what a combined Form 3115 filing and retroactive cost segregation study could recover for your property.