Introduction

Every year, thousands of real estate investors take advantage of depreciation deductions to reduce their taxable rental income—often paying zero tax on properties generating solid cash flow. But when they finally sell, many face a jarring surprise: a five- or six-figure tax bill on income they never actually pocketed. One investor recently sold a rental property for a modest gain after paying down most of the mortgage, only to discover that $120,000 of the proceeds were immediately taxable due to depreciation recapture (income that appeared on paper, but never as cash in hand).

This is phantom income — one of the most misunderstood tax consequences in real estate. It's taxable, it's real, and most investors don't see it coming.

According to IRS Publication 544, depreciation recapture applies to all disposed depreciable property. Every investor who has claimed depreciation deductions is building deferred tax liability that will come due at sale — even if the property hasn't appreciated significantly.

That deferred liability is exactly what this article addresses. The focus here is the depreciation angle of phantom income — distinct from partnership allocations or cancellation-of-debt scenarios — because recapture is the form investors encounter most often and can actually plan around. You'll learn what phantom income from depreciation is, how it's triggered at sale, why cost segregation changes the math, and what strategies exist to manage or defer it.

TLDR

- Phantom income is taxable income the IRS recognizes that you never received as spendable cash—most commonly triggered by depreciation recapture at sale

- Depreciation reduces your property's cost basis each year; when you sell, the IRS recaptures those deductions as taxable income regardless of actual cash proceeds

- Section 1250 recapture (real property) is taxed at up to 25%; Section 1245 recapture (personal property) hits ordinary income rates up to 37%

- Cost segregation front-loads deductions but concentrates Section 1245 recapture exposure—knowing your exit strategy before you file matters

- 1031 exchanges, installment sales, and tax-loss harvesting can defer or reduce phantom income from recapture

What Is Phantom Income in Real Estate Depreciation?

Phantom income is taxable income that the IRS recognizes and requires you to pay taxes on, even though you never actually received that amount as spendable cash. The IRS taxes economic benefit, not just cash flow. If you benefited from a deduction, the reversal of that benefit becomes taxable income.

In real estate, the most common source of phantom income is depreciation recapture. When you take annual depreciation deductions to reduce taxable rental income over your holding period, those deductions artificially lower your property's cost basis. At sale, the IRS recaptures those prior deductions by treating a portion of your gain as taxable income.

How Recapture Is Classified

Depreciation recapture falls into two categories:

Section 1250 (Real Property):

- Applies to building structures (residential and commercial)

- Taxed at the unrecaptured Section 1250 rate of up to 25%

- Separate from long-term capital gains rates

- Example: A commercial building depreciated over 39 years

Section 1245 (Personal Property):

- Applies to furniture, equipment, land improvements, and reclassified building components from cost segregation

- Taxed as ordinary income (up to 37% in 2025)

- Example: Appliances, carpeting, sidewalks, electrical systems

A Simplified Example

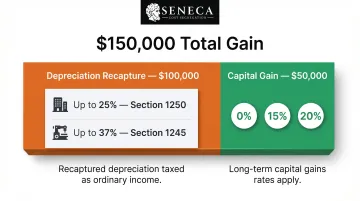

An investor buys a rental property for $400,000 and takes $100,000 in total depreciation deductions over 10 years, reducing the adjusted basis to $300,000. If they sell for $450,000:

- Sales price: $450,000

- Adjusted basis: $300,000 (original $400,000 minus $100,000 depreciation)

- Total gain: $150,000

Of that $150,000 gain:

- $100,000 is depreciation recapture (taxable at 25% or ordinary rates depending on asset type)

- $50,000 is capital gain (taxable at long-term capital gains rates)

Even if the investor's net proceeds after paying off a mortgage are minimal, the IRS still taxes the full $150,000 gain.

Why This Feels Unfair

That example shows the math — but the sting comes from timing and rates. Investors received real cash-flow benefit from the tax deductions each year, often sheltering income at an effective 0% rate. The recapture bill arrives all at once in the year of sale, which can create a liquidity crisis when proceeds are already committed to debt payoff or a new acquisition.

That mismatch is what creates the "phantom" sensation: income that was sheltered at 0% is now taxed at 25% or higher, in a single year.

How Depreciation Leads to a Phantom Tax Bill at Sale

The IRS calculates gain on sale using a simple formula:

Gain = Amount Realized – Adjusted Basis

Your adjusted basis is your original purchase price, plus capital improvements, minus accumulated depreciation. Because depreciation continuously reduces your adjusted basis, your taxable gain upon sale increases—even if the property hasn't appreciated significantly in market value.

The Two Gain Buckets

Investors often confuse the total gain on sale with the depreciation recapture component:

Depreciation recapture: The portion of gain up to the amount of depreciation previously taken. This is taxed at Section 1250 rates (up to 25%) for real property or ordinary income rates (up to 37%) for Section 1245 property.

Capital gain: Gain above the original purchase price. This is taxed at long-term capital gains rates (0%, 15%, or 20% depending on income).

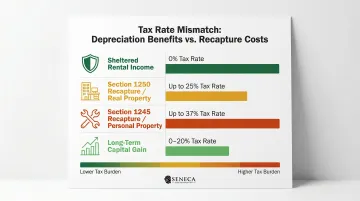

The Tax Rate Mismatch

Depreciation shelters rental income during ownership — sometimes bringing your effective rate to 0% through paper losses. At sale, that math reverses sharply:

| Income Type | Tax Rate |

|---|---|

| Sheltered rental income (during hold) | 0% (offset by depreciation) |

| Section 1250 recapture (real property) | Up to 25% |

| Section 1245 recapture (personal property) | Up to 37% (ordinary income) |

| Long-term capital gain (above original basis) | 0%, 15%, or 20% |

The result is a disproportionate tax bill in the sale year relative to the cash actually received.

Foreclosure and Debt Forgiveness Scenarios

The rate mismatch is especially painful in distressed situations. If a property is surrendered to a lender, the IRS still treats the forgiven loan amount as a deemed sale price. According to a Tax Adviser analysis of foreclosure tax consequences, investors can face large recapture income even when they received little or no cash. This scenario has become more common in distressed commercial real estate markets.

Bracket Stacking Risk

Depreciation recapture is recognized in the year of sale and stacks on top of your other income. A significant recapture event can push you into a higher tax bracket, making the effective tax rate on recapture higher than the stated 25% ceiling suggests. A $400,000 recapture event added to $150,000 of ordinary income, for instance, can trigger the 3.8% Net Investment Income Tax on top of standard recapture rates. Running multi-year projections before listing — not after — is what separates investors who plan for this from those who get caught short at closing.

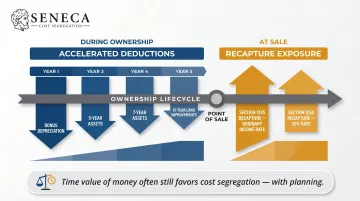

How Cost Segregation Affects Phantom Income Risk

Cost segregation is an IRS-approved engineering methodology that accelerates depreciation deductions by reclassifying building components from long-lived real property (27.5 or 39 years) into shorter-lived asset classes (5, 7, and 15 years).

What Gets Reclassified

A cost segregation study, governed by IRC §168 and detailed in the IRS Cost Segregation Audit Techniques Guide, typically identifies:

5-year and 7-year property (Section 1245):

- Carpeting

- Cabinetry

- Specialized electrical systems

- Decorative fixtures

15-year property (Section 1245):

- Land improvements: paving, fencing, landscaping, sidewalks

According to industry benchmarks from ASCSP, 15% to 40% of a building's depreciable basis can typically be reclassified into shorter-lived categories.

The Amplified Upfront Benefit

Cost segregation delivers large first-year deductions, especially when combined with bonus depreciation. For 2025, the One, Big, Beautiful Bill Act (OBBBA) permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025. Assets reclassified to 20-year or shorter recovery periods qualify for this immediate expensing.

That upfront tax savings is real — but it comes with a tradeoff. Accelerating deductions reduces your adjusted basis faster, which means a larger portion of your sale-year gain becomes subject to recapture. Section 1245 assets face recapture at ordinary income rates, not just the 25% cap that applies to Section 1250 property.

Cost Segregation Doesn't "Cost You at Sale"

A common misconception is that cost segregation creates a net tax disadvantage. In reality, the deductions were real savings taken in prior years at potentially high marginal rates, while recapture happens at capped rates (25% for Section 1250, ordinary income for Section 1245). The time value of money and rate differential often still favor cost segregation—but you must plan for the sale-year cash demand.

Forward-Looking Analysis

The best cost segregation studies don't stop at year-one deductions. They model future recapture exposure — showing you the projected tax liability at sale so you can build reserves or time your exit around favorable rate conditions. Seneca Cost Segregation's engineering-based studies include this analysis as a standard deliverable, helping investors plan around recapture rather than getting blindsided by it at closing.

What Income Can Be Offset by Real Estate Depreciation?

Depreciation — including accelerated depreciation from cost segregation — can offset rental income and, for qualifying real estate professionals or active participants, other forms of passive income. These deductions reduce net taxable income reported on Schedule E, sheltering cash flow from tax.

Passive Activity Rules

For most investors, IRC §469 passive activity rules limit how depreciation losses can be used:

- Passive investors: Real estate losses (including paper losses from depreciation) can only offset other passive income, not W-2 wages or active business income

- Real estate professionals: Those who log more than 750 hours in real property trades or businesses — where that work exceeds half their total personal services for the year — can treat rental losses as non-passive, offsetting W-2 or active business income

- Active participation exception: Active participants may deduct up to $25,000 of passive losses against non-passive income; this allowance phases out between $100,000–$150,000 MAGI and disappears entirely above $150,000

Basis and At-Risk Limitations

Even when passive activity rules allow deductions, IRC §465 at-risk rules limit deductible losses to the amount you have "at risk" in the activity. Additionally, partners and S-corporation shareholders face basis limitations under IRC §704(d), which restrict loss deductions to the taxpayer's adjusted basis in the entity.

How to Deal with Phantom Income from Real Estate Depreciation

Managing depreciation recapture starts before you list the property. These four strategies give you the most control over the outcome:

1031 Exchange: The Primary Deferral Tool

A like-kind exchange under IRC §1031 allows investors to defer depreciation recapture (and capital gains) by rolling proceeds into a replacement property. The accumulated depreciation carries over to the new property's basis, deferring the eventual recapture — not eliminating it.

Key requirements:

- Replacement property must be identified within 45 days of closing

- Exchange must be completed within 180 days

- Properties must be held for investment or business use, not personal use

- Any cash received or debt relief ("boot") triggers taxable gain and potential recapture

Installment Sale Strategy

If a 1031 exchange isn't feasible, spreading sale proceeds over multiple years via an installment sale can distribute capital gain recognition across tax years, potentially keeping you in lower brackets.

One significant constraint: IRC §453(i) forces immediate recognition of all Section 1245 and Section 1250 recapture in the year of sale, even if no cash is received. Only gain above the recapture amount can be spread across years. That makes installment sales far less effective for heavily depreciated properties — particularly those that went through cost segregation.

Opportunity Zone Investment

Investing realized gains in a Qualified Opportunity Zone fund can defer recognition until 2026 and potentially reduce the total owed. Not all gain qualifies, though:

- Eligible for deferral: capital gains and qualified §1231 gains

- Not eligible: ordinary income from Section 1245 recapture-1) does not qualify for deferral

Reserve Planning and Estimated Taxes

The most practical near-term step is modeling your recapture exposure before you list. Three actions make a real difference:

- Calculate estimated recapture liability using your full depreciation schedule

- Set aside adequate cash reserves to cover the tax bill in the sale year

- Adjust quarterly estimated payments to avoid underpayment penalties

Working with a cost segregation specialist at acquisition — not just at sale — gives you the complete depreciation schedule needed to run these numbers accurately.

Frequently Asked Questions

What is phantom income from real estate depreciation?

Phantom income is the taxable gain the IRS recognizes from depreciation recapture at sale—income that appears on your tax return even when you did not receive an equivalent cash payout, because prior depreciation deductions reduced the property's cost basis.

How do you deal with phantom income from real estate depreciation?

The main mitigation strategies are:

- 1031 exchange — defers recapture by rolling proceeds into a replacement property

- Installment sale — spreads capital gain across years (recapture is still due in year one)

- Tax reserves — set aside funds before closing to cover the recapture liability

- Early advisor modeling — work with a tax advisor before listing to quantify exposure

What income can be offset by real estate depreciation?

Depreciation offsets passive rental income for most investors. It can offset broader passive income streams or even active income for qualifying real estate professionals, but passive activity rules limit its use for W-2 earners without real estate professional status.

Is depreciation recapture taxed as ordinary income or capital gains?

Section 1250 unrecaptured depreciation on real property structures is taxed at a maximum 25% rate (not the standard long-term capital gains rate). Section 1245 recapture on personal property—accelerated by cost segregation—is taxed at ordinary income rates (up to 37%).

Can a 1031 exchange help avoid phantom income from depreciation?

A 1031 exchange defers but does not eliminate depreciation recapture. The accumulated depreciation carries forward into the replacement property's basis, meaning recapture is postponed until you eventually sell outside of a 1031 exchange or pass the property to heirs (who receive a stepped-up basis).

Does cost segregation increase phantom income risk at sale?

Cost segregation accelerates deductions and concentrates more Section 1245 recapture exposure at sale. However, the net benefit over time often still favors cost segregation due to the time value of money and tax rate differentials—as long as you plan ahead for the sale-year tax liability.

Final Takeaway: Phantom income from depreciation recapture is manageable—but only if you model your exposure before you sell. Seneca Cost Segregation provides the engineering analysis and recapture projections you need to plan a tax-efficient exit.