Introduction

Commercial property depreciation is a tax benefit, not an accounting loss. The IRS allows building owners to deduct a portion of a property's value every year as a "phantom expense" that reduces taxable income without requiring an out-of-pocket payment. Unlike a repair bill or mortgage payment, depreciation is a non-cash deduction that increases your net cash flow while lowering your tax liability.

Many commercial property owners leave thousands in annual tax savings unclaimed because they misunderstand how depreciation works, which recovery periods apply, and what strategies can front-load deductions. Whether you own office buildings, retail centers, industrial facilities, or hotels, the rules around depreciation directly determine how much you keep after taxes.

This guide covers everything you need: the 39-year rule, depreciation calculations, MACRS vs. straight-line methods, cost segregation strategies, and depreciation recapture.

Key Takeaways:

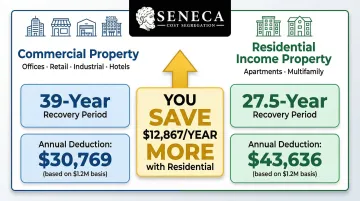

- Commercial properties depreciate over 39 years; residential income properties over 27.5 years

- Land never depreciates; only the building structure qualifies

- Cost segregation reclassifies building components into 5-, 7-, or 15-year asset classes to accelerate deductions

- Bonus depreciation is back to 100% for qualifying property placed in service after January 19, 2025, under current legislation

- Depreciation recapture is taxed at up to 25% on sale unless deferred through a 1031 exchange

What Is Commercial Property Depreciation?

Depreciation is the IRS-recognized process of spreading the cost of a building across its "useful life" for tax purposes. It allows owners to deduct a set amount each year as the structure ages and wears down. Critically, land never depreciates; only the structure itself qualifies for this deduction.

The "Phantom Expense" Advantage

Unlike a repair bill, depreciation does not require spending money. It is a non-cash deduction that reduces taxable income and improves real cash flow. For example, if your commercial property generates $100,000 in net rental income and you claim $30,000 in depreciation, your taxable income drops to $70,000, saving you thousands in federal taxes without affecting your actual cash position.

Core Recovery Periods Under IRS Tax Code

The IRS assigns different depreciation schedules based on property type:

| Property Type | Recovery Period | Annual Deduction ($1.2M Basis) |

|---|---|---|

| Commercial properties (offices, retail centers, industrial buildings, hotels) | 39 years | $30,769 |

| Residential income properties (apartments, multifamily) | 27.5 years | $43,636 |

A $1.2 million depreciable basis yields $30,769 annually over 39 years (commercial) versus $43,636 over 27.5 years (residential), a difference of nearly $13,000 per year in deductions.

The 80% Rule for Mixed-Use Buildings

If 80% or more of gross rental income comes from residential units, the entire mixed-use building may qualify for the shorter 27.5-year depreciation schedule. For a building with both commercial and residential tenants, that shift in schedule directly increases your annual deduction, but it requires consistent income tracking and documentation to defend the classification.

When Depreciation Begins

Depreciation starts when the property is "placed in service" (ready and available for rent), not the purchase date. The IRS applies the mid-month convention, meaning you claim only a half-month of depreciation in the month of acquisition and the month of sale. Knowing this upfront lets you set accurate expectations for your first-year deduction before you close.

How to Calculate Commercial Property Depreciation

Calculating depreciation requires two inputs: your depreciable basis and the IRS recovery period:

Step 1: Establish the Depreciable Basis

Subtract the land value from the total purchase price to get the depreciable basis. Since land does not wear out and cannot be depreciated, this allocation is critical:

Formula: Purchase Price − Land Value = Depreciable Basis

Example: You purchase a commercial property for $1.5 million. The county tax assessment allocates $300,000 to land. Your depreciable basis is $1,200,000.

Step 2: Apply the Straight-Line Formula

Divide the depreciable basis by the useful life (39 years for commercial, 27.5 years for residential):

Formula: Depreciable Basis ÷ 39 = Annual Depreciation Expense

Example: $1,200,000 ÷ 39 ≈ $30,769 per year

This $30,769 deduction offsets rental income each year for up to 39 years, reducing your taxable income and federal tax liability.

That clock, however, doesn't run indefinitely.

When Depreciation Stops

Depreciation ends when:

- The entire depreciable basis has been claimed over the full recovery period

- The property is sold

- The property is permanently removed from income-generating use

Importance of Professional Land Value Assessment

A standard percentage assumption for land versus building value may result in an inaccurate annual deduction. The land allocation determines the annual deduction amount, and an incorrect allocation affects the actual deduction.

A defensible allocation is typically established through a licensed appraiser or by referencing the county property tax assessment. The IRS may challenge allocations that appear unreasonably low, and without supporting documentation (an appraisal report, tax records, or a cost segregation study), those deductions are at risk.

Depreciation Methods for Commercial Property

MACRS: The IRS-Standard System

The Modified Accelerated Cost Recovery System (MACRS) covers depreciation for most tangible property. It includes two sub-systems:

| Sub-System | Description |

|---|---|

| General Depreciation System (GDS) | Default for most commercial property, with shorter recovery periods that accelerate deductions |

| Alternative Depreciation System (ADS) | Uses longer periods; required for certain foreign-use properties or when electing out of business interest limitations |

Straight-Line Depreciation for Real Property

Unlike personal property (which can use accelerated methods), commercial buildings must use the straight-line method under GDS. This produces equal annual deductions spread across 39 years, the standard schedule for the building structure itself.

Section 1245 vs. Section 1250 Property

This distinction directly shapes your depreciation strategy:

| Characteristic | Section 1250 Property | Section 1245 Property |

|---|---|---|

| Property Type | Real property (the building structure itself) | Personal property and equipment (machinery, appliances, certain fixtures) |

| Depreciation Method | Straight-line over 39 years | Faster accelerated methods |

| Recapture on Sale | Capped at 25% rate | Recaptured as ordinary income |

The classification also determines your tax exposure when you sell. Section 1245 property is recaptured as ordinary income, while Section 1250 recapture is capped at a 25% rate, a meaningful difference when a property changes hands.

Depreciation Schedules for Non-Structural Components

Not everything in a commercial building follows the 39-year schedule:

| Asset Type | Recovery Period | Examples |

|---|---|---|

| Land improvements | 15 years | Parking lots, landscaping, sidewalks, fencing |

| Personal property | 5-7 years | Specialized equipment, certain flooring, cabinetry, appliances |

| Building structure | 39 years | Walls, roof, HVAC, plumbing, elevators |

Separating these components from the building structure, and capturing the shorter recovery periods, is precisely what a cost segregation study accomplishes.

How Accelerated Depreciation Works: Cost Segregation and Bonus Depreciation

Cost Segregation: Front-Loading Deductions

Cost segregation is the primary strategy to accelerate depreciation deductions. A cost segregation study, performed by licensed engineers and tax professionals, identifies building components that can be reclassified from 39-year real property into 5-, 7-, or 15-year personal property or land improvements.

This accelerates deductions into the early years of ownership where they have the most impact on cash flow. Seneca Cost Segregation's engineering-based studies have helped property owners across all 50 states identify significant first-year deductions, with an average first-year deduction of $171,243.

How It Works:

- Engineers identify components like carpeting (5 years), office furniture (7 years), and parking lots (15 years)

- These assets are reclassified from 39-year property into shorter recovery periods

- The result: substantially higher deductions in years 1-7 when cash flow matters most

Qualified Improvement Property (QIP)

Non-residential commercial buildings qualify for QIP on interior improvements made after the property is placed in service. These improvements carry a 15-year recovery period (not 39 years) and can be eligible for bonus depreciation.

Common QIP examples include:

- Tenant improvement allowances

- Interior build-outs and renovations

- Partition walls and suspended ceilings

- Upgraded flooring and finishes

QIP excludes building enlargements, elevators/escalators, and the internal structural framework.

When QIP qualifies, it can also be paired with bonus depreciation, making the combined tax impact even more immediate.

Bonus Depreciation: Current Status

The One, Big, Beautiful Bill Act (OBBBA) enacted July 4, 2025 permanently restored 100% bonus depreciation for qualifying assets acquired and placed in service after January 19, 2025. The TCJA phase-down had cut that rate to 60% in 2024 and 40% in early 2025. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate |

|---|---|

| September 27, 2017 – December 31, 2022 | 100% |

| January 1, 2023 – December 31, 2023 | 80% |

| January 1, 2024 – December 31, 2024 | 60% |

| January 1, 2025 – January 18, 2025 | 40% |

| January 19, 2025 – December 31, 2030 (acquisition date on or after January 19, 2025) | 100% |

If acquisition date is before January 19, 2025:

| Year of Placement in Service | Bonus Depreciation Rate |

|---|---|

| 2025 | 40% |

| 2026 | 20% |

Key rules under current law:

- Applies to property with a 20-year or shorter recovery period

- Covers short-lived assets identified through cost segregation or QIP

- Enables a 100% first-year deduction in the year the asset is placed in service

What Happens to Depreciation When You Sell

Depreciation Recapture Explained

When a commercial property is sold, the IRS "recaptures" the tax benefit of depreciation deductions claimed during ownership. The amount of depreciation taken is taxed at a maximum rate of 25% for Section 1250 property (the building structure), not the lower long-term capital gains rate.

How Recapture Is Calculated

The adjusted cost basis is calculated as:

Adjusted Basis = Original Depreciable Basis − Total Depreciation Claimed

Example:

- Original purchase price: $1,500,000

- Land value: $300,000

- Depreciable basis: $1,200,000

- Depreciation claimed over 10 years: $307,690

- Adjusted basis: $1,200,000 − $307,690 = $892,310

If you sell the property for $1,800,000:

- Unrecaptured Section 1250 gain: $307,690 (taxed at 25%)

- Remaining capital gain: $1,800,000 − $1,500,000 = $300,000 (taxed at long-term capital gains rates)

The 1031 Exchange: Deferring Recapture

That recapture tax can be significant, but investors have a legal path to avoid triggering it at sale. By reinvesting sale proceeds into a "like-kind" income-producing property within IRS timelines, investors can defer both capital gains taxes and depreciation recapture indefinitely.

1031 Exchange Requirements:

| Requirement | Details |

|---|---|

| 45-day identification period | Must identify replacement property in writing within 45 days of transferring the relinquished property |

| 180-day exchange period | Must receive replacement property within 180 days (or tax return due date, whichever is earlier) |

| Qualified intermediary required | Must use a QI to hold funds; disqualified persons (agents, related parties, your attorney/broker) cannot serve as QI |

Investors can chain these exchanges indefinitely, a strategy known as "swap till you drop." When a property owner dies, heirs receive a stepped-up cost basis, effectively wiping out the deferred tax liability entirely. That makes the timing of a 1031 exchange, and how depreciation has been accelerated beforehand, a key part of long-term estate planning.

Frequently Asked Questions

Can you depreciate commercial property?

Yes, commercial property is fully depreciable for tax purposes under the IRS MACRS system, as long as it is used in a trade or business or held for the production of income. Land cannot be depreciated, only the building structure.

How many years can you depreciate commercial property?

Commercial property is depreciated over 39 years under the IRS straight-line method, while residential income properties (such as apartment buildings) use a shorter 27.5-year schedule. Specific components of a commercial building can be depreciated over shorter periods (5, 7, or 15 years) through cost segregation.

How do you calculate depreciation for commercial property?

Subtract land value from the purchase price to find the depreciable basis, then divide the depreciable basis by 39 to get the annual depreciation deduction. A cost segregation study or tax advisor can verify the accurate land value split.

What components of commercial property can be depreciated over 5, 7, or 15 years?

Personal property such as specialized equipment, certain flooring, cabinetry, and appliances can be depreciated over 5-7 years, while land improvements like parking lots, fencing, and landscaping depreciate over 15 years. These are identified through a cost segregation study and are not automatically separated from the 39-year building basis.

What is the difference between 1245 and 1250 property?

Section 1250 property refers to real property (the building structure), which is subject to straight-line depreciation and a 25% recapture rate on sale. Section 1245 property covers personal property and equipment that uses accelerated depreciation.

What happens when a building is fully depreciated?

Once a commercial building is fully depreciated (after 39 years), the owner can no longer claim annual depreciation deductions. The property can still be owned and rented, but those deductions are gone. If sold, the adjusted cost basis for the depreciated portion is zero, which maximizes recapture and capital gains tax exposure.