Introduction

Real estate investors face a fundamental tension: rental income is fully taxable, yet the IRS provides powerful tools to legally offset that income through depreciation. Most investors aren't using these tools effectively. A Government Accountability Office study found that 53% of individual taxpayers with rental real estate misreport their activities, leaving billions in legitimate tax deductions unclaimed annually.

This guide covers three layers of depreciation strategy that work together to maximize cash flow:

- Standard MACRS depreciation, the baseline method most investors use

- Cost segregation, an engineering-based approach that accelerates deductions

- Bonus depreciation, which allows immediate expensing of qualifying assets

This guide is for residential rental owners, multi-family investors, commercial property owners, and short-term or long-term rental operators who want to move beyond basic depreciation and maximize the tax benefits available on their properties.

TLDR:

- Real estate depreciation allows investors to deduct building costs over time, reducing taxable income even as properties appreciate

- Cost segregation studies reclassify 20-40% of building components into 5-, 7-, or 15-year depreciation schedules instead of 27.5 or 39 years

- The One Big Beautiful Bill Act restored 100% bonus depreciation for properties acquired on or after January 19, 2025; the TCJA phase-down remains in effect for properties acquired before January 19, 2025

- Combining cost segregation with bonus depreciation can generate first-year deductions of $171,000+ on qualifying properties

- Depreciation recapture taxes apply when selling, but strategies like 1031 exchanges can defer this liability

What Is Real Estate Depreciation?

Real estate depreciation is an IRS mechanism that allows property owners to deduct the cost of an income-producing building over its useful life, accounting for wear and tear. This is strictly a tax strategy, not a reflection of market value—you can claim depreciation deductions even while your property appreciates in market value.

The IRS defines depreciation as "the recovery of the cost of income-producing property through yearly tax deductions." Land itself cannot be depreciated because the IRS considers land to have an indefinite useful life that doesn't wear out or become obsolete.

That land exclusion directly shapes how you calculate your depreciable basis. Your depreciable basis is the purchase price minus the land value; only this portion qualifies for annual deductions. For example, if you purchase a property for $500,000 and the land is valued at $100,000, your depreciable basis is $400,000.

Correctly separating land from building value is a step many investors get wrong. The IRS requires taxpayers to make this allocation using fair market value ratios from property tax assessments or professional appraisals.

Approximately 166,000 taxpayers illegally include land value in their depreciable basis, according to GAO data, a mistake that triggers audits and penalties.

What Can Real Estate Investors Depreciate?

The IRS establishes four eligibility criteria for depreciation:

- You must own the property (including properties with mortgages)

- It must be used for income production (primary residences don't qualify)

- It must have a determinable useful life greater than one year

- Land itself is explicitly excluded

Beyond the building structure, investors can depreciate multiple property components, each with different recovery periods:

| Asset Class | Recovery Period | Examples |

|---|---|---|

| Personal Property | 5–7 years | Appliances (refrigerators, dishwashers, washers, dryers), carpets and removable flooring, furniture and fixtures, decorative lighting, window treatments |

| Land Improvements | 15 years | Parking lots and driveways, landscaping and irrigation systems, fencing and gates, sidewalks and pathways, exterior lighting |

| Building Structure | 27.5 years (residential) / 39 years (commercial) | Structural framework, roof and foundation, walls and windows, HVAC systems (typically), plumbing and electrical systems |

A few rules trip up investors more than others:

- Primary residences never qualify for investment depreciation, regardless of any home office use

- Land never depreciates, even when improvements sit on top of it

- Depreciation stops once the property is fully depreciated or sold

How to Calculate Real Estate Depreciation: MACRS Explained

The Modified Accelerated Cost Recovery System (MACRS) is the IRS-mandated method for depreciating real estate. MACRS establishes two key recovery periods:

| Property Type | Recovery Period | Depreciation Method |

|---|---|---|

| Residential rental property | 27.5 years | Straight-line |

| Commercial property | 39 years | Straight-line |

The IRS also requires the "mid-month convention," meaning property placed in service during any month is treated as placed in service at the midpoint of that month.

The Depreciation Formula:

Depreciable Basis ÷ Recovery Period = Annual Deduction

Practical Example: Step-by-Step MACRS Calculation

Step 1 – Determine Depreciable Basis: You purchase a residential rental property for $500,000. The land is valued at $100,000, leaving a $400,000 depreciable basis.

Step 2 – Calculate Annual Depreciation: Annual depreciation: $400,000 ÷ 27.5 years = $14,545

Step 3 – Apply Mid-Month Convention (First Year): For the first year, you'll receive a prorated deduction based on the mid-month convention. If you place the property in service in July, you'll claim 5.5 months of depreciation (July–December): $14,545 × (5.5 ÷ 12) = $6,666.

The Limitation of Straight-Line MACRS:

This method spreads deductions evenly over decades, meaning investors who rely solely on this approach leave significant upfront tax savings on the table.

The Tax Foundation notes that delayed deductions discourage investment because inflation and the time value of money erode its value. A dollar in tax savings today is worth far more than the same dollar deferred 27 years into the future.

Accelerated Depreciation Through Cost Segregation

Cost segregation is an engineering-based analysis that reclassifies property components from 27.5- or 39-year life into 5-, 7-, or 15-year asset classes. This dramatically front-loads deductions into the first years of ownership rather than spreading them over decades.

How Cost Segregation Works

A professional study identifies components that qualify as personal property or land improvements rather than building structure:

| Asset Class | Recovery Period | Examples |

|---|---|---|

| Personal property | 5 years | Specialty flooring (decorative tile, hardwood), carpeting and padding, appliances and equipment, decorative fixtures, fire protection systems |

| Office/specialized property | 7 years | Office furniture and fixtures, specialized equipment |

| Land improvements | 15 years | Parking lots and paving, landscaping and irrigation, fencing and gates, sidewalks and outdoor lighting |

Once reclassified, these components may also qualify for bonus depreciation, compounding the tax impact well beyond what straight-line depreciation delivers.

Cost Segregation Combined With Bonus Depreciation

When assets are reclassified to shorter lives, they may qualify for immediate expensing under bonus depreciation rules. The result is a dramatically larger deduction in year one. Seneca's studies across 10,200+ properties show that 20–30% of a building's depreciable basis typically shifts into accelerated categories.

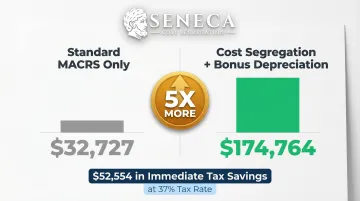

Example Impact

For a $900,000 cost basis property placed in service in 2025 (with 100% bonus depreciation):

- Without cost segregation: $32,727 annual deduction

- With cost segregation and bonus depreciation: $174,764 first-year deduction

- Additional first-year benefit: $142,037 (more than 5 times the standard deduction)

At a 37% federal tax rate, this translates to approximately $52,554 in immediate tax savings in year one alone.

Who Benefits Most

Investors with properties valued at $300,000+ in depreciable basis (residential) or $750,000+ (commercial) typically see the greatest ROI from a cost segregation study.

| Property Type | Minimum Depreciable Basis |

|---|---|

| Residential | $300,000+ |

| Commercial | $750,000+ |

The strategy also applies to properties you already own, not just new acquisitions:

- New property purchases

- Existing properties via "look-back" studies (no amendment required)

- Renovated buildings

- Properties placed in service as far back as January 1, 1987

Seneca Cost Segregation has completed over 10,200 cost segregation studies nationwide, with an average first-year deduction of $171,243. Every study includes AuditDefense with a money-back guarantee, and all work is performed by licensed professional engineers, the methodology the IRS explicitly prefers over software-only approaches.

Bonus Depreciation: Rules, Phase-Out, and Current Status

Bonus depreciation allows investors to immediately deduct a large percentage of qualifying assets (those with a useful life of 20 years or less) in the year they are placed in service, rather than over their standard recovery period.

Legislative History and Current Status:

The Tax Cuts and Jobs Act of 2017 established 100% bonus depreciation for qualified property acquired after September 27, 2017, with a scheduled phase-down beginning in 2023. However, the One Big Beautiful Bill Act (Public Law 119-21), enacted July 4, 2025, restored 100% bonus depreciation for property acquired and placed in service on or after January 19, 2025. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Current Bonus Depreciation Schedule:

| Period (Placed in Service) | Acquisition Date | Bonus Depreciation % |

|---|---|---|

| Sep 27, 2017 – Dec 31, 2022 | Any | 100% |

| Jan 1, 2023 – Dec 31, 2023 | Any | 80% |

| Jan 1, 2024 – Dec 31, 2024 | Any | 60% |

| Jan 1, 2025 – Jan 18, 2025 | Any | 40% |

| Jan 19, 2025 – Dec 31, 2030 | On or after Jan 19, 2025 | 100% |

| 2025 (placed in service) | Before Jan 19, 2025 | 40% |

| 2026 (placed in service) | Before Jan 19, 2025 | 20% |

How Bonus Depreciation Works with Cost Segregation:

A cost segregation study identifies which assets qualify for bonus depreciation. Together, these strategies can allow investors to deduct 20-40%+ of a property's total cost in year one.

Practical Example:

You purchase a $2 million commercial property in 2025. A cost segregation study identifies $600,000 in 5-, 7-, and 15-year property. With 100% bonus depreciation:

- Immediate deduction: $600,000

- Tax savings at 37% rate: $222,000

- Standard depreciation alternative: $15,385 annually over 39 years

The accelerated approach delivers 14 years' worth of deductions immediately: $222,000 in year one versus waiting decades for the same result.

Net Operating Losses (NOLs):

Bonus depreciation can create a net operating loss when deductions exceed taxable income. Under current IRC §172 rules:

- NOLs arising after 2017 cannot be carried back

- NOLs can be carried forward indefinitely

- The NOL deduction in future years is limited to 80% of taxable income

- Any excess carries into subsequent years until fully utilized

Section 179 vs. Bonus Depreciation:

Section 179 is a related but distinct tool. For 2026, the maximum deduction is $2.56 million with a phase-out threshold beginning at $4.09 million. For most rental property investors, bonus depreciation is the stronger choice. Here's why:

| Feature | Section 179 | Bonus Depreciation |

|---|---|---|

| Property scope | Applies primarily to equipment and tangible personal property, not the building structure | Applies to assets with a useful life of 20 years or less |

| Can create NOL | No (unlike bonus depreciation) | Yes |

| Annual dollar cap | Yes ($2.56 million for 2026, phase-out begins at $4.09 million) | No dollar cap |

| Limited to current-year income | Yes | No |

| Best suited for | Owner-occupied businesses | Rental portfolios |

Bonus depreciation has no dollar cap, can generate NOLs, and scales with the size of your portfolio.

Depreciation Recapture and Passive Activity Loss Rules

Depreciation Recapture

When you sell a property, the IRS "recaptures" depreciation deductions taken as taxable income. Section 1250 recapture taxes this at up to 25% for real property. Depreciation is a deferral strategy, not permanent tax elimination. You're postponing liability until sale or exchange.

Assets reclassified via cost segregation (moved from Section 1250 real property to Section 1245 personal property) face ordinary income tax rates up to 37% upon sale, not the capped 25% rate. That 12-point rate gap is exactly why exit strategy planning matters before you accelerate depreciation.

| Section | Property Type | Recapture Tax Rate |

|---|---|---|

| Section 1250 | Real property | Up to 25% |

| Section 1245 | Personal property (cost segregation reclassified) | Up to 37% (ordinary income rate) |

Deferring Recapture with 1031 Exchanges

Section 1031 like-kind exchanges let investors defer both capital gains and depreciation recapture by rolling proceeds into replacement properties. When executing a 1031 after using cost segregation, the replacement property requires sufficient Section 1245 property. Otherwise, any "boot" received (cash or non-like-kind property) can trigger ordinary income recapture immediately.

Exit planning under 1031 directly affects how useful your passive loss deductions are, which brings PAL rules into the picture.

Passive Activity Loss (PAL) Rules

Under IRC §469, rental activities are generally considered passive. Passive losses can only offset passive income (not W-2 wages or business income) unless you qualify for Real Estate Professional Status (REPS).

REPS Requirements

To deduct rental losses against active income:

- More than 50% of personal services performed in all trades/businesses during the year must be in real property trades or businesses

- More than 750 hours of service must be performed in those real property trades or businesses

Meeting REPS requirements transforms passive losses into active losses that can offset ordinary income, making cost segregation deductions immediately usable against high W-2 income.

Required Documentation

The following records support deductions and IRS inquiries:

- Depreciation schedules for each property and asset class

- IRS Form 4562, filed annually to claim depreciation

- Purchase documents showing the land/building cost allocation

- Cost segregation report from a qualified engineering study

Cost segregation studies carry audit risk if not properly documented. Seneca Cost Segregation handles IRS inquiries at no additional cost and backs every study with a money-back guarantee if adjustments exceed 5% due to study errors.

Frequently Asked Questions

Is depreciation on investment property tax deductible?

Yes, depreciation on investment property is fully tax deductible under IRS rules. It reduces taxable rental income each year, letting you deduct the cost of the building over its useful life.

What can be depreciated by an investor in real estate?

Real estate investors can depreciate most property components, but not the land itself:

- Building structure: 27.5 years (residential) or 39 years (commercial)

- Land improvements like parking lots and landscaping: 15 years

- Interior components such as flooring and cabinets: 5–15 years

- Personal property including appliances and equipment: 5–7 years

What is depreciation recapture and how is it taxed?

When you sell a property, the IRS recaptures depreciation previously claimed and taxes it as ordinary income, capped at 25% under Section 1250 for real property. Strategies like 1031 exchanges can defer this liability by reinvesting proceeds into replacement properties.

How does cost segregation accelerate depreciation?

A cost segregation study reclassifies building components into shorter-life asset classes (5, 7, or 15 years instead of 27.5 or 39). This front-loads deductions into early ownership years, often generating $100,000+ in first-year savings when combined with bonus depreciation.

Can I take depreciation on a property I still have a mortgage on?

Yes, the IRS allows depreciation as long as you legally own the property and use it for income production. Having a mortgage does not affect eligibility—depreciation is based on the property's cost basis, regardless of how it's financed.

What happens to bonus depreciation after 2026?

The One Big Beautiful Bill Act (Public Law 119-21) enacted in July 2025 restored 100% bonus depreciation for qualified property acquired on or after January 19, 2025. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.