This guide shows you how to fix that. You'll learn how rental property depreciation works, the difference between standard and accelerated methods, how cost segregation can reclassify building components into shorter recovery periods, and how to manage depreciation recapture when you eventually sell. Whether you've owned your property for one year or ten, these strategies apply—and the cash flow impact can be immediate.

TLDR:

- Rental property depreciation allows owners to recover property costs over 27.5 or 39 years through annual tax deductions

- Cost segregation reclassifies building components into 5-, 7-, and 15-year schedules, dramatically front-loading deductions

- Bonus depreciation (60% in 2024, returning to 100% in 2025+) applies to accelerated assets with no annual cap

- Look-back studies via Form 3115 let long-time owners catch up on all missed depreciation in one year

- Real estate professional status unlocks the ability to offset W-2 income with rental depreciation losses

How Rental Property Depreciation Works

Depreciation is the IRS mechanism that allows rental property owners to recover the cost of a property over its "useful life" through annual tax deductions. Each year, you deduct a portion of the property's cost from your taxable rental income—reducing your tax bill without spending another dollar on the property.

Understanding the full mechanics—from qualification requirements to cost basis to recovery periods—determines how much you can deduct and when. Here's how each piece works.

Four IRS Requirements to Qualify

To depreciate rental property, you must meet four strict criteria:

- You own the property (including contract-for-deed or land contract arrangements)

- You use it for income-producing purposes (rented or available for rent, not personal use)

- The property has a determinable useful life (it wears out, decays, or becomes obsolete)

- It lasts more than one year (permanent improvements, not temporary installations)

Critical exception: Land cannot be depreciated because it doesn't wear out or become obsolete. You must separate land value from building value when calculating your depreciable basis.

Establishing Your Depreciable Cost Basis

Your depreciable basis is calculated as:

Purchase price + eligible closing costs − land value = depreciable basis

Example:

- Purchase price: $400,000

- Eligible closing costs (legal fees, title insurance, transfer taxes): $8,000

- Total cost basis: $408,000

- Assessed land value: $80,000

- Depreciable building basis: $328,000

If fair market value allocation is unclear, use the ratio from your property tax assessment to split purchase price between land and building.

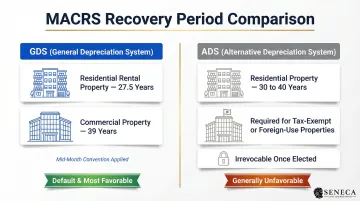

Standard Recovery Periods

The Modified Accelerated Cost Recovery System (MACRS) General Depreciation System (GDS) assigns specific recovery periods:

- 27.5 years for residential rental property (buildings where ≥80% of gross rental income comes from dwelling units)

- 39 years for commercial property (offices, retail, warehouses)

Both use the mid-month convention, meaning you claim half a month's depreciation in the month placed in service, regardless of the actual day.

When Depreciation Begins and Ends

Begins: The "placed in service" date—when the property is ready and available to generate income. Tenant occupancy isn't required. Buy a move-in-ready rental on July 15 and depreciation starts that month.

Ends: When you've fully recovered your cost basis, sell or dispose of the property, or convert it to personal use.

Standard vs. Accelerated Depreciation Methods

MACRS GDS vs. ADS

Two depreciation systems exist under MACRS:

General Depreciation System (GDS):

- Default method for rental property

- 27.5-year recovery for residential, 39-year for commercial

- Most favorable for maximizing near-term deductions

Alternative Depreciation System (ADS):

- 30 or 40-year recovery periods for residential property

- Required for certain properties (tax-exempt use, predominantly outside the U.S.)

- Electable but irrevocable once chosen

- Generally unfavorable unless legally mandated

Bonus Depreciation: The Primary Acceleration Tool

Bonus depreciation under IRC §168(k) allows owners to deduct a large percentage of qualifying property costs in the year placed in service. The Tax Cuts and Jobs Act (TCJA) phase-down schedule applies to property acquired before January 19, 2025:

- 2024: 60%

- 2025: 40%

- 2026: 20%

- 2027: 0%

Critical update: The One Big Beautiful Bill Act restored 100% bonus depreciation for qualified property acquired after January 19, 2025, making this an even more powerful tool moving forward.

Key advantages:

- Applies to both new and used property

- No annual dollar cap (unlike Section 179)

- Can create a net operating loss (NOL) to carry forward

Many investors also confuse bonus depreciation with Section 179 — but for rental property owners, they are not interchangeable.

Why Section 179 Doesn't Help Most Rental Owners

Section 179 allows immediate expensing up to $2,500,000 (for 2025), but its eligibility rules effectively exclude most rental property owners:

- Active business required: Section 179 only applies to an active trade or business — not passive investments

- Income limitation: The deduction cannot exceed taxable business income for the year

- Passive treatment: Standard residential rental property is classified as a passive investment, disqualifying it outright

For rental property owners, bonus depreciation is the right tool — and when combined with a cost segregation study to reclassify assets into shorter recovery periods, it can accelerate a significant portion of your property's total cost into year-one deductions.

Cost Segregation: The Most Powerful Tool for Maximizing Depreciation

Cost segregation is an IRS-approved engineering-based tax strategy that reclassifies property components from 27.5- or 39-year recovery periods into shorter 5-, 7-, or 15-year depreciation schedules. This dramatically front-loads deductions into the early years of ownership.

What Gets Reclassified

The IRS Cost Segregation Audit Techniques Guide recognizes three accelerated asset categories:

5-Year Personal Property:

- Carpeting and vinyl flooring

- Appliances (refrigerators, ranges, dishwashers)

- Decorative lighting fixtures

- Window treatments and blinds

- Specialty electrical and plumbing serving specific equipment

7-Year Personal Property:

- Office furniture and cabinetry

- Removable partitions

- Certain flooring and finishes

15-Year Land Improvements:

- Parking lots and driveways

- Landscaping and irrigation systems

- Fencing and retaining walls

- Outdoor lighting and signage

- Swimming pools and recreational amenities

Structural components (walls, roof, HVAC, plumbing mains, foundation) remain on the standard 27.5- or 39-year schedule.

A well-executed study typically reclassifies 20%–40% of a property's total cost into accelerated categories, with specialty properties (restaurants, medical facilities) reaching even higher percentages.

Cash Flow Impact: A Real-World Scenario

Consider a $1,000,000 rental property with an $800,000 depreciable basis (after excluding land). Without cost segregation, standard straight-line depreciation generates $29,091 annually ($800,000 ÷ 27.5 years).

With cost segregation reclassifying 30% ($240,000) into 5-, 7-, and 15-year categories and 60% bonus depreciation applied:

- Bonus depreciation on accelerated assets: $240,000 × 60% = $144,000

- Remaining accelerated depreciation: $240,000 × 40% ÷ weighted average life ≈ $19,200

- Structural component depreciation: $560,000 ÷ 27.5 = $20,364

- Total first-year deduction: $183,564

That's a $154,473 increase in first-year depreciation compared to straight-line alone.

For perspective, Seneca Cost Segregation reports an average first-year deduction of $171,243 across 10,200+ completed studies—a credible benchmark that demonstrates the tangible value of engineering-based cost segregation.

Look-Back Studies: Catching Up on Missed Depreciation

That scenario assumes cost segregation is ordered at acquisition — but investors who've owned a property for years without a study can still capture those missed deductions. The IRS allows a "catch-up" of all missed accelerated depreciation in the current tax year via a **§481(a) adjustment on Form 3115** (Application for Change in Accounting Method).

The process is straightforward:

- Calculate what depreciation you should have claimed with cost segregation

- Compare it to what you actually claimed using straight-line

- Capture the difference as a single adjustment in the current year

- No need to amend prior-year returns

This is an automatic change under Designated Change Number (DCN) 7 and does not require IRS pre-approval.

Choosing the Right Cost Segregation Provider

Engineering-based studies following the IRS Cost Segregation Audit Techniques Guide withstand scrutiny far better than software-only or "rule of thumb" approaches.

Seneca Cost Segregation uses an engineering-based methodology with ASCSP-credentialed professionals, offering:

- AuditDefense with a money-back guarantee (100% fee refund if an audit reveals >5% depreciation adjustment caused by Seneca)

- 2–4 week turnaround

- Service across all 50 states

- Direct coordination with your CPA

- Complimentary tax assessments beyond the study itself

That engineering rigor is what makes the difference between a study that holds up under IRS scrutiny and one that doesn't.

Additional Strategies to Maximize Rental Property Tax Benefits

Real Estate Professional Tax Status

Under IRC §469, rental losses are generally passive and can only offset passive income. But qualifying as a Real Estate Professional (REP) converts rental losses into nonpassive losses that can offset W-2 and other ordinary income.

Two-part test:

- 750+ hours per year in real property trades or businesses (property management, leasing, development, brokerage, construction)

- More than 50% of your total personal services in all businesses performed in real property activities

Plus material participation: You must also materially participate in each rental activity (or elect to group all rentals as a single activity).

Impact: When combined with accelerated depreciation, REP status allows six-figure depreciation losses to offset a high-earning spouse's W-2 income. For high-income households, the combined tax reduction can be substantial.

Capital Improvements vs. Repairs

Classification determines immediate vs. deferred deductions:

Capital Improvements (must be depreciated):

- New roof replacement

- HVAC system installation

- Room additions or structural changes

- Major renovations that extend property life

Repairs and Maintenance (deducted immediately):

- Patching a roof leak

- Replacing a broken faucet

- Repainting existing walls

- Routine servicing of HVAC

Pro tip: Capital improvements may qualify for bonus depreciation if they constitute separate assets (e.g., a new HVAC system) or are personal property (appliances, flooring). Getting this classification right impacts cash flow significantly.

LLC Structuring and Entity Considerations

While primarily an asset protection tool, entity structure directly affects how depreciation flows to your tax return. Each structure carries different rules:

- Single-member LLCs (disregarded entities): Depreciation passes through directly to your individual return

- Partnerships/multi-member LLCs: Pass-through treatment applies, with depreciation allocated per the operating agreement

- S-corps: Require careful planning around reasonable compensation and distribution timing before depreciation benefits can flow cleanly

Work with a qualified CPA to align your entity structure with your overall depreciation strategy — particularly if you're pursuing REP status, using cost segregation, or scaling across multiple properties.

Managing Depreciation Recapture When You Sell

How Depreciation Recapture Works

When you sell a rental property at a gain, the IRS "recaptures" the depreciation deductions you previously took. The portion of gain attributable to depreciation is taxed at up to 25% (unrecaptured Section 1250 gain), separate from the long-term capital gains rate applied to the remaining profit.

High-income taxpayers (MAGI above $200,000 single / $250,000 married filing jointly) may also owe the 3.8% Net Investment Income Tax (NIIT) on the entire gain.

Here's how that plays out in practice:

Simplified Example

- Original purchase price: $300,000

- Accumulated depreciation over 10 years: $54,000

- Adjusted cost basis: $300,000 − $54,000 = $246,000

- Sale price: $400,000

- Total gain: $400,000 − $246,000 = $154,000

Tax breakdown:

- Depreciation recapture (first $54,000 of gain): taxed at 25% = $13,500

- Remaining capital gain ($100,000): taxed at 15% or 20% long-term capital gains rate

- Potential NIIT: 3.8% on entire $154,000 gain if applicable

That $13,500 recapture bill—before capital gains taxes—is why many investors look for ways to defer rather than absorb the hit.

Deferring Recapture with a 1031 Exchange

A Section 1031 like-kind exchange allows you to defer depreciation recapture, capital gains, and NIIT indefinitely by reinvesting sale proceeds into a qualifying replacement property of equal or greater value.

Timeline requirements:

- 45 days to identify replacement property after closing

- 180 days to complete the exchange

Benefits:

- Defers all taxes (recapture + capital gains + NIIT)

- Resets the depreciation clock on the new property

- Opens the door to a fresh cost segregation study on the replacement property

Important: The depreciable basis carries over to the replacement property, meaning you're deferring recapture, not eliminating it. Any additional capital invested ("excess basis") is treated as newly placed in service property and qualifies for full depreciation treatment.

Frequently Asked Questions

What is the best depreciation method for rental property?

For most rental property owners, MACRS GDS is the standard method. However, combining it with a cost segregation study to reclassify components into 5-, 7-, and 15-year schedules delivers the highest first-year and near-term deductions. Accelerated depreciation via cost segregation is the most effective overall approach for maximizing cash flow.

How do you accelerate depreciation on a rental property?

The primary way to accelerate depreciation is through a cost segregation study, which reclassifies building components into shorter recovery periods and allows bonus depreciation to be applied to those assets. The result: substantially front-loaded deductions in the first few years of ownership, when the tax savings have the most reinvestment value.

Is claiming depreciation on rental property mandatory?

While not technically required each year, the IRS assumes you've taken allowable depreciation when calculating recapture at sale. You may owe tax on depreciation you never claimed, so taking the deduction annually is essential.

What is depreciation recapture and how is it taxed?

Depreciation recapture is the IRS's mechanism for taxing the portion of a property sale gain that corresponds to depreciation previously deducted. It's taxed at a rate up to 25% (plus potentially 3.8% NIIT for high earners), separate from the long-term capital gains rate applied to the remaining gain.

Can you do a cost segregation study on a property you've already owned for several years?

Yes. A "look-back" cost segregation study lets owners catch up on all missed accelerated depreciation in the current tax year through a Form 3115 accounting method change — no amended prior-year returns required.

What types of rental properties qualify for cost segregation?

Cost segregation applies to residential rentals (single-family, multifamily, short-term rentals), commercial properties, and mixed-use buildings. Properties with a depreciable cost basis above $150,000–$200,000 benefit most, and those at $300,000+ typically produce the clearest ROI relative to study costs.