Introduction

Many condo investors assume cost segregation is reserved for sprawling commercial buildings or large apartment complexes — a misconception that costs them thousands in unnecessary tax payments every year. The reality is simpler: condo units contain numerous interior components (flooring, appliances, cabinetry, HVAC systems, specialty lighting) that qualify for reclassification into 5-year and 15-year depreciation schedules, well ahead of the IRS standard 27.5-year straight-line schedule.

The financial stakes are real. A cost segregation study can reclassify 20% to 40% of a condo's depreciable basis into accelerated categories, producing an average first-year deduction of $171,243 — directly improving cash flow. Research from the IRS Cost Segregation Audit Techniques Guide confirms this approach is both legal and defensible when executed with proper engineering documentation.

This article explains the practical, measurable benefits of a cost segregation study for condo owners — covering the real financial outcomes it produces, including how the 2025 restoration of 100% bonus depreciation amplifies these savings even further.

TL;DR

- Cost segregation reclassifies condo components from 27.5-year depreciation into 5- or 15-year categories, front-loading deductions

- Condo owners—especially short-term rental operators—gain significant first-year tax savings and improved cash flow

- Paired with 100% bonus depreciation restored under the 2025 One Big Beautiful Bill Act, studies yield immediate, large deductions

- Retroactive savings are available through look-back studies filed via IRS Form 3115—no amended returns required

- Tax savings routinely exceed study costs by 10:1—Seneca clients average $171,243 in first-year deductions

What Is a Cost Segregation Study for Condo Owners?

A cost segregation study is an engineering-based analysis that breaks down a property into individual components and assigns each one its correct IRS depreciation life—rather than lumping everything into the building's default 27.5-year schedule.

Condo owners legally own their interior unit—walls, floors, fixtures, appliances, and systems within the unit—but standard practice depreciates everything at the same slow rate.

The IRS Modified Accelerated Cost Recovery System (MACRS) mandates a 27.5-year recovery period for residential rental property by default. It doesn't require that timeline for components that qualify for shorter lives.

A cost segregation study corrects this through a systematic process:

- Identifying which components qualify for accelerated 5- or 15-year recovery periods

- Reallocating costs from the building structure to personal property categories

- Creating detailed engineering documentation that supports the reclassification

- Establishing component-level records for future partial disposition elections

This is a tax timing strategy, not a new deduction. It doesn't create tax benefits that didn't exist—it accelerates existing depreciation into earlier ownership years, taking advantage of the time-value of money and improving near-term cash flow.

Key Benefits of Cost Segregation Studies for Condo Owners

The three benefits below focus on measurable financial outcomes that condo investors can track. The impact is highest in the early years of ownership when accelerated deductions are most concentrated.

Benefit 1: Front-Loaded Tax Deductions That Reduce Your Tax Bill Immediately

The primary benefit is reclassifying a substantial portion of the condo's depreciable basis into 5-year property, which compresses decades of deductions into the first few years of ownership.

How this works in practice:

Components such as kitchen appliances, flooring, cabinetry, specialty lighting, and built-in fixtures are identified and separated from the building structure. Each receives a shorter depreciation life per IRS MACRS guidelines.

Why this matters:

A case study from Engineering Tax Services examined a $1.36 million residential condo in Margate, NJ. The study reclassified 39.6% of the depreciable basis to 5-year property, generating a first-year depreciation increase of over $333,000.

For a condo owner in a high tax bracket, this translates directly to tens of thousands of dollars in tax savings in a single year. Industry data shows that 20% to 40% of a residential property's components typically qualify for reclassification, concentrating deductions where they deliver maximum financial impact.

KPIs impacted:

- First-year taxable income from rental activity

- Federal income tax owed

- Effective tax rate on rental income

When this benefit matters most:

Highest impact occurs in the year of acquisition or the first year the condo is placed in service as a rental. Look-back studies for properties held for years without a cost segregation analysis remain valuable, though some time-value benefit is permanently lost.

Benefit 2: Improved Cash Flow That Can Be Reinvested Into the Next Property

Lower taxes in the early ownership years directly translate into more cash on hand. That capital stays with the investor rather than going to the IRS and can be redeployed into renovations, debt paydown, or a down payment on another property.

By shifting depreciation from future years into the present, the condo owner effectively receives an interest-free loan from the government in the form of deferred taxes. This capital advantage compounds when reinvested.

A case study by Cost Segregation Services, Inc. on a $565,000 office condo generated $30,934 in first-year tax savings, which when reinvested at an 8% rate could grow to over $456,000 in future value.

Industry benchmarks suggest cost segregation can reduce income taxes by up to $100,000 for every $1 million in building costs over the first five years.

Condo investors who delay or skip a study lose this time-value advantage permanently. Depreciation not claimed in earlier years cannot be fully recovered with equivalent financial benefit later.

KPIs impacted:

- Net cash flow after taxes

- Reinvestment capacity

- Portfolio growth rate

- Return on equity

When this benefit matters most:

Highest impact for investors actively scaling their portfolio, those with multiple condos, and short-term rental operators with strong income who need offsetting deductions to reduce passive income taxes.

Benefit 3: Bonus Depreciation Amplification for Maximum First-Year Write-Off

Cost segregation and bonus depreciation reinforce each other. Once the study identifies assets with a class life of less than 20 years (5-year and 15-year categories), those assets become eligible for bonus depreciation. As of January 2025, the One Big Beautiful Bill Act permanently restores bonus depreciation at 100%.

Instead of spreading a $200,000 reclassified component over 5 years, the condo owner deducts the entire amount in year one. This creates a substantial loss that offsets rental income or, for qualifying real estate professionals, other income streams.

Hypothetical illustration:

A $700,000 condo where 30% of the basis ($210,000) is reclassified to 5-year property. With 100% bonus depreciation, the owner deducts the full $210,000 in year one rather than $42,000 annually, a significant reduction in year-one tax liability.

The STR advantage:

Short-term rental (STR) condo owners with an average guest stay of 7 days or fewer may classify their activity as non-passive under IRS Publication 925. If the owner meets material participation tests, the large first-year depreciation losses can offset W-2 and other active income — the "STR loophole."

Even as bonus depreciation rates change with future legislation, cost segregation continues to provide value. The 5-year and 15-year reclassifications still accelerate deductions compared to the default 27.5-year baseline.

KPIs impacted:

- Year-one tax liability

- Passive vs. active loss classification

- W-2 income offset potential (for STR operators and real estate professionals)

When this benefit matters most:

Most powerful for condos placed in service after January 19, 2025 under OBBBA rules. Also critical for STR condo operators and real estate professionals who can use accelerated losses against ordinary income.

What Condo Components Typically Qualify for Accelerated Depreciation?

Not everything inside a condo qualifies for reclassification. The structural shell, load-bearing walls, and core plumbing/electrical infrastructure remain at 27.5 years. However, a surprising number of interior components do qualify and are often overlooked.

5-Year Personal Property

- Kitchen appliances (refrigerators, stoves, microwaves, dishwashers)

- Carpeting and decorative flooring

- Window treatments (blinds, drapes)

- Specialty and decorative lighting fixtures

- Dedicated electrical outlets for appliances

- Built-in entertainment or tech systems

- Security systems and equipment

Land improvements are less common for individual condo investors, but worth confirming with your engineer.

15-Year Land Improvements (When Applicable)

- Sidewalks and paving (rarely owned by individual condo owners)

- Fences and outdoor lighting (typically HOA-owned)

Remaining at 27.5-Year Real Property

- Building structure and load-bearing walls

- Core HVAC systems

- Kitchen cabinetry and countertops (typically structural)

- General interior lighting and wiring

- Core plumbing systems

One important boundary to clarify upfront: the study only applies to interior unit components owned by the condo investor. Common-area improvements (hallways, lobbies, exterior landscaping, elevators) are typically owned by the HOA and are not eligible for individual unit owner depreciation. Before commissioning a study, confirm exactly which components fall within your ownership scope — your engineer can help map this quickly.

What Happens When Condo Owners Skip a Cost Segregation Study?

Without a study, the IRS requires the entire depreciable basis of a condo to follow the 27.5-year straight-line schedule. This means owners under-depreciate in early years and over-depreciate in later years—the reverse of what maximizes tax efficiency.

Compounding consequences of inaction:

- Forfeits the time-value benefit of early deductions — a look-back study can partially catch up, but the interest-free tax deferral is gone

- Misses the window to pair cost segregation with 100% bonus depreciation, which requires action in the acquisition year

- Eliminates component-level asset records needed to claim partial asset disposition deductions when renovating

The numbers tell the story:

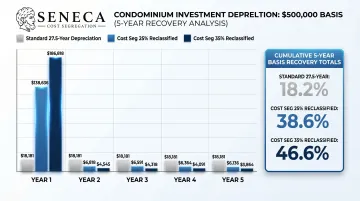

The table below compares cumulative depreciation over the first five years for a condo with a $500,000 depreciable basis:

| Depreciation Method | Year 1 | Years 2-5 (Annual) | Cumulative Years 1-5 | % of Basis Recovered |

|---|---|---|---|---|

| Standard 27.5-Year | $18,181 | $18,181 | $90,909 | 18.2% |

| Cost Seg (25% Reclassified) | $138,636 | $13,636 | $193,182 | 38.6% |

| Cost Seg (35% Reclassified) | $186,818 | $11,818 | $233,091 | 46.6% |

At a 25% reclassification, that's over $100,000 in additional deductions within five years — cash that stays in your pocket for reinvestment rather than sitting in a deferred tax account.

How to Get the Most Value from Your Condo Cost Segregation Study

Timing Matters

The study delivers the highest value when completed in the year the condo is placed in service as a rental, capturing all accelerated deductions and bonus depreciation from day one. Look-back studies (using IRS Form 3115) remain valuable for condos held for several years without a study.

Study Quality Determines Study Value

The IRS prefers engineering-based cost segregation studies prepared by qualified professionals—not rule-of-thumb estimates or spreadsheet-only approaches. Accurate component identification and cost allocation make reclassifications audit-defensible.

Seneca Cost Segregation uses an engineering-based methodology with licensed engineers on staff, AuditDefense, and a money-back guarantee — delivering IRS-compliant results in 2-4 weeks. Across more than 10,200 studies, their average first-year deduction is $171,243.

Professional Implementation Is Critical

Pair the study with a CPA or tax advisor experienced in real estate to:

- Implement results correctly on your tax return

- Maximize bonus depreciation elections

- Plan for depreciation recapture when the condo is eventually sold

Conclusion

Cost segregation studies give condo owners a proven method to legally reduce their tax burden — one that ensures IRS-accepted depreciation schedules reflect the true, shorter useful lives of interior components—rather than defaulting to a blanket 27.5 years.

The benefits — front-loaded deductions, improved cash flow, and amplified bonus depreciation — compound most powerfully when the study is done early and integrated into a broader tax strategy with qualified professional support. The sooner a study is completed, the more deductions you can capture. Firms like Seneca Cost Segregation deliver studies within 2–4 weeks and have helped investors across all 50 states unlock an average first-year deduction of $171,243 — making it one of the highest-ROI tax moves available to condo owners today.

Frequently Asked Questions

Can you do a cost segregation study on a condo?

Yes, condos qualify for cost segregation as long as they are income-producing (used as a rental, not a primary residence). Residential and commercial condos are both eligible. The study applies to the interior components owned by the investor within the unit.

What is the average cost of a cost segregation study for a condo?

Study fees typically range from $2,500 to $6,000 for smaller residential rental properties, with broader industry ranges spanning $5,000 to $15,000 depending on complexity. For most condo investors, study fees are a fraction of first-year tax savings — Seneca's clients average $171,243 in first-year deductions.

What properties qualify for cost segregation?

Any income-producing or business-use real property qualifies—including rental condos, apartment buildings, office buildings, short-term rentals, and commercial spaces. Primary residences do not qualify because they must be used for investment or business purposes.

Can you do cost segregation on a short-term (vacation) rental property?

Yes, STR condos qualify and often benefit the most. Short-term rentals with an average guest stay of 7 days or fewer may allow depreciation losses to offset non-passive income for qualifying owners. This makes cost segregation especially powerful for Airbnb and VRBO condo operators.

What are common cost segregation mistakes?

The three most costly errors are:

- Waiting too long and missing the bonus depreciation window

- Using unqualified providers who rely on rules-of-thumb rather than engineering analysis

- Ignoring depreciation recapture implications when planning to sell

What is the $2,500 de minimis safe-harbor (expense) rule?

This IRS rule allows taxpayers to immediately expense individual items costing $2,500 or less per invoice rather than capitalizing and depreciating them. It works alongside cost segregation as a complementary strategy to expense smaller condo components outright rather than depreciating them over time.