Introduction

Many real estate investors face the same cash flow problem: properties generate solid income, but federal tax obligations consume a significant portion before they can reinvest or scale. The culprit is often straight-line depreciation: a 27.5- or 39-year write-off schedule that spreads deductions so thin, the tax benefit barely moves the needle in year one.

Most investors leave substantial legal deductions unclaimed, not because the deductions don't exist, but because capturing them requires a level of engineering precision most accountants aren't trained to apply.

Engineering-based cost segregation is a tax strategy that uses licensed engineers and construction methodology to reclassify building components into shorter depreciation categories, accelerating deductions from the standard 27.5- or 39-year schedule to 5, 7, or 15 years. This isn't creative accounting; it's applied construction science that transforms how quickly you recover your property investment through the tax code.

If you've heard the term but aren't sure what separates a rigorous engineering study from a cheaper desktop alternative, or how that gap translates into real dollars, this guide breaks it down.

TLDR

- Engineering-based studies reclassify 20–40% of building costs into 5-, 7-, and 15-year depreciation categories using construction analysis

- Site inspections and document review let qualified engineers identify more qualifying property than accounting-based approaches

- IRS-quality studies require component-level cost allocation, legal authority citations, and thorough documentation

- Properties purchased, built, or renovated after 1987 with a cost basis above $300,000 typically qualify

- First-year deductions unlock immediate cash flow, backed by engineering documentation that holds up under audit

What Is Engineering-Based Cost Segregation?

Engineering-based cost segregation is a tax study conducted by licensed engineers who apply construction knowledge and cost-allocation methodology to identify which property components qualify as personal property or land improvements. Those components depreciate over 5, 7, or 15 years, rather than the full building depreciating as real property over 27.5 or 39 years.

By front-loading depreciation deductions, investors reduce taxable income in the early years of ownership, freeing up cash that would otherwise go to the IRS.

Not all cost segregation studies are equal. The IRS explicitly states in its Cost Segregation Audit Technique Guide that studies conducted by construction engineers are more reliable than those prepared by individuals without engineering or construction backgrounds. Here's how the two approaches differ:

| Study Type | Methodology |

|---|---|

| Accounting-based studies | Rely on rules of thumb, averages, and residual estimation |

| Engineering-based studies | Use actual construction data, site inspections, and component-level analysis |

Why the Engineering Approach Delivers More Tax Savings

The Technical Advantage

Engineers trained in mechanical and electrical systems can identify components that serve a business function rather than a structural building function. Only assets serving a business purpose, not the building's structure itself, qualify for shorter depreciation lives under IRS rules.

Consider these commonly reclassified components:

- Specialty HVAC circuits serving specific equipment rather than general building climate control

- Dedicated electrical systems powering business operations instead of standard building lighting

- Removable partitions that can be relocated without structural damage

- Custom millwork designed for specific business functions

- Parking lots and landscaping classified as 15-year land improvements

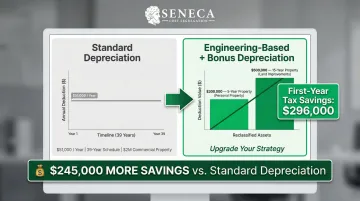

The Math That Matters

A $2 million commercial property depreciated over 39 years produces roughly $51,000 in annual deductions. Engineering analysis might identify $800,000 (40%) of that basis as qualifying for accelerated depreciation:

- $300,000 reclassified to 5-year property

- $500,000 reclassified to 15-year property

- $1,200,000 remains 39-year property

With 100% bonus depreciation (reinstated for property acquired on or after January 19, 2025, under the One Big Beautiful Bill Act), that $800,000 becomes immediately deductible in year one. At a 37% combined tax rate, this creates $296,000 in first-year tax savings, versus the $51,000 you'd receive under standard depreciation.

The Residual Estimation Gap

DIY and abbreviated studies work from industry averages. If the typical office building has 25% of its value in short-life assets, that's what you'll be assigned, regardless of whether your building actually has 18% or 35%. Engineering-based analysis is property-specific, reflecting actual installed components rather than statistical assumptions.

Data from over 8,000 engineering-based studies puts the typical reclassification rate at 20% to 30% of a property's depreciable basis into 5-year and 15-year recovery schedules.

Audit Defensibility

The IRS lists 13 quality criteria for cost segregation studies in its Audit Technique Guide. Engineering-based reports are built to meet every requirement:

- Prepared by engineers with hands-on construction expertise

- Supported by actual construction documentation, not estimates

- Calculated using unit cost take-offs and engineering-grade math

- Reconciled back to total project costs, dollar for dollar

- Identifies Section 1245 property with written legal justification

- Includes detailed methodology descriptions reviewable by the IRS

Meeting all 13 criteria is what separates a defensible study from one that creates audit exposure. Seneca Cost Segregation's engineering-based studies satisfy each requirement and include AuditDefense coverage for the entire ownership period, so if the IRS ever questions a reclassification, you're covered.

The Bonus Depreciation Factor

The One Big Beautiful Bill Act reinstated 100% bonus depreciation for qualified property acquired on or after January 19, 2025. That matters because bonus depreciation had been phasing down under the TCJA, as shown in the timeline below, leaving many investors uncertain about year-one deduction potential.

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | TCJA original rate |

| January 1, 2023 – December 31, 2023 | 80% | TCJA phase-down |

| January 1, 2024 – December 31, 2024 | 60% | TCJA phase-down |

| January 1, 2025 – January 18, 2025 | 40% | TCJA phase-down |

| January 19, 2025 – December 31, 2030 (acquisition date on or after January 19, 2025) | 100% | OBBBA reinstatement |

| 2025 (acquisition date before January 19, 2025) | 40% | TCJA phase-down applies |

| 2026 (acquisition date before January 19, 2025) | 20% | TCJA phase-down applies |

For property with an acquisition date on or after January 19, 2025, if a property's engineering study identifies $800,000 in short-life assets, that $800,000 is immediately deductible in year one at 100% bonus depreciation: not 60%, not 80%, all of it. That's the combination that produces the $296,000 first-year savings figure in the example above.

How an Engineering-Based Cost Segregation Study Works

The study progresses through five distinct phases, each building the documentation your CPA needs to apply accelerated depreciation correctly and defend it under IRS review.

Step 1: Initial Assessment and Qualification

The process begins with a review of your property's purchase price, construction cost, year placed in service, and property type to determine whether a study will produce beneficial returns.

Key evaluation factors include:

- Cost basis (typically $300,000 minimum depreciable basis)

- Property type and construction characteristics

- Tax situation and ability to use passive losses

- Holding period expectations

Many qualified engineering firms, including Seneca, offer this pre-study analysis at no cost. Seneca has assessed over 10,200 properties nationwide, with clients averaging $171,243 in first-year deductions.

Step 2: Document Collection and Blueprint Review

Engineers collect comprehensive documentation to understand how the building was actually constructed and what each component cost:

- Cost basis documentation and closing statements

- Construction contracts and change orders

- Architectural drawings and engineering plans

- Tax depreciation schedules

- Property appraisals separating land from building value

With actual construction records in hand, engineers can allocate costs precisely, rather than relying on square footage estimates or comparable property assumptions, before the site inspection confirms what's on the ground.

Step 3: Site Inspection and Component Identification

During the 1-2 hour property inspection (virtual or on-site), engineers verify:

- Whether fixtures are bolted to structural walls or can be removed without damage

- Specialty systems that serve a specific business function rather than the building overall

- Land improvements such as paving, fencing, and landscaping

- Whether actual site conditions match what the construction documents show

Engineers document findings through hundreds of photographs, detailed measurements, and construction material identification, creating the evidentiary foundation for component classification.

Step 4: Cost Allocation and Asset Classification

The core technical work involves assigning each identified component to the correct depreciation category:

| Recovery Period | Examples |

|---|---|

| 5-year property: | Carpeting, appliances, removable fixtures |

| 7-year property: | Office furniture, specialized equipment |

| 15-year property: | Parking lots, sidewalks, exterior landscaping |

| 27.5/39-year property: | Structural building components |

This requires simultaneous application of engineering knowledge (understanding building systems) and tax law knowledge (applying IRS asset class guidance and legal precedents like the Hospital Corporation of America functional allocation test).

Step 5: Report Preparation and Implementation

The completed engineering report contains:

- Asset lists by depreciation class with detailed descriptions

- Cost allocation reconciliation tying back to total purchase price

- Legal authority citations including revenue rulings, court cases, and IRS guidance

- Supporting documentation including photographs, blueprints, and engineering calculations

- Ready-to-file tax forms (Form 4562 for current-year studies, Form 3115 for look-back studies)

The report goes directly to your CPA for implementation. Seneca delivers most studies within 2-4 weeks, using in-house technology built by engineers to ensure accurate component classifications and consistent documentation across all 50 states.

Which Properties and Investors Qualify

Property Eligibility

Most investment properties meet the basic qualification criteria:

- Placed in service after December 31, 1987

- Depreciable cost basis above $300,000 (excluding land value)

- Expected holding period of 3+ years

Both current acquisitions and properties owned for years qualify. Look-back studies allow you to claim missed depreciation from prior years through a Form 3115 accounting method change, without amending past returns.

Which Building Types Benefit Most

Engineering-based cost segregation applies across diverse property categories:

Commercial Buildings:

- Office buildings and professional centers

- Retail stores and shopping centers

- Hotels and hospitality properties

- Restaurants and entertainment venues

Industrial Facilities:

- Warehouses and distribution centers

- Manufacturing plants

- Self-storage facilities

Residential Investment:

- Multi-family apartment complexes

- Single-family rentals with sufficient cost basis

- Short-term rental properties

| Property Type | Typical Reclassification Rate |

|---|---|

| Mobile home parks | 80-85% |

| Manufacturing facilities | 30-60% |

| Medical buildings | 25-43% |

Investor Profile

Cost segregation delivers the most value to investors in the 32%+ federal tax bracket who can apply accelerated depreciation in the year it's generated. Whether those deductions are immediately usable depends on how you navigate passive activity loss rules under IRC Section 469.

Deductions become immediately useful if you:

- Qualify as a Real Estate Professional (750+ hours annually in real property trades, materially participating)

- Operate short-term rentals with average stays of 7 days or less and materially participate

- Have substantial passive income from other sources to offset

If your situation doesn't fit neatly into one of these categories, Seneca offers complimentary tax assessments that analyze your specific property, bracket, and passive income profile, so you know before committing whether a study pencils out.

Common Misconceptions That Cost Investors Money

"I'm Already Getting All My Depreciation"

Many investors assume their CPA's standard depreciation schedule captures everything available. In reality, without a cost segregation study, the entire structure is typically depreciated as one asset over 27.5 or 39 years, a legally conservative approach that leaves substantial accelerated deductions unclaimed.

Standard depreciation treats your building as a single asset. A component-level analysis separates it into 50–200+ distinct components, each with its own appropriate recovery period, unlocking deductions that standard schedules never surface.

"It's Aggressive or Risky"

Cost segregation is explicitly recognized by the IRS in its Audit Technique Guide and has been validated by decades of tax court cases and Treasury guidance. The risk isn't in conducting a study; it's in conducting a poorly documented one.

The IRS acknowledges that field-verified, engineer-led studies are more reliable than accounting-based alternatives. With proper documentation meeting the 13 quality criteria, audit risk is minimal. Seneca's AuditDefense program provides complete audit support for your entire ownership period at no additional charge.

"My CPA Can Handle This"

CPAs can prepare cost segregation studies, but IRS guidance recognizes that professionals with construction engineering knowledge produce more accurate, audit-ready results. A CPA without that background typically relies on the same residual estimation method as DIY tools.

The strongest studies combine both disciplines:

- Engineers identify and classify individual components with field-verified precision

- CPAs implement the findings and integrate them into your broader tax strategy

Your CPA doesn't get replaced; they get better data to work with.

"Only Big Commercial Properties Benefit"

While large commercial assets have historically dominated cost segregation, the strategy applies across property types. Multi-family properties, short-term rental portfolios, and even high-value single-family rentals generate meaningful deductions when cost basis exceeds $300,000 in depreciable improvements.

The real threshold is simple math: study cost vs. tax savings. When a study costing a few thousand dollars unlocks $30,000–$50,000+ in first-year deductions—a 10:1 return or better—the investment justifies itself regardless of property type.

Frequently Asked Questions

What is engineering based cost segregation?

Engineering-based cost segregation is a tax study conducted by licensed engineers who use construction methodology and property-specific analysis to identify and reclassify building components into accelerated depreciation categories, unlike accounting-based approaches that rely on industry averages and statistical estimates.

How does an engineering based cost segregation study affect my taxes?

The study increases depreciation deductions in the early years of property ownership, reducing taxable income and federal tax liability. Combined with 100% bonus depreciation for property acquired on or after January 19, 2025, identified short-life assets may be fully expensed in the year placed in service.

Who qualifies for engineering based cost segregation?

Most commercial, industrial, and investment residential properties with depreciable cost basis above $300,000 placed in service after 1987 qualify. The benefit is strongest for investors who can actively use the resulting deductions against their income through Real Estate Professional Status or the short-term rental exception.

Who performs engineering based cost segregation studies?

Studies are typically performed by professionals who combine construction engineering expertise with tax law knowledge, such as licensed engineers or Certified Cost Segregation Professionals (CCSPs). The IRS Audit Technique Guide notes that engineering-based preparers produce more reliable studies than those without construction backgrounds.

Are engineering based cost segregation studies worth it?

For most investment properties above the qualifying threshold, study costs are small relative to the tax savings generated — typical returns range from 10:1 to 25:1. ROI depends on property value, tax bracket, and ability to use passive losses. Pre-study analyses confirm viability before you commit.

How much does an engineering based cost segregation study cost?

Fees vary based on property type, size, and complexity but typically range from $5,000-$15,000. The fee is proportional to savings: a $10,000 study generating $150,000+ in first-year deductions represents substantial ROI. Many providers offer free benefits analysis upfront to establish economic viability before proceeding.

Ready to find out what your property's depreciation is actually worth? Seneca Cost Segregation offers complimentary preliminary assessments to determine your property's qualification and projected savings. With over 12 years of experience, 10,200+ completed studies, and an average first-year deduction of $171,243, their veteran-owned team delivers engineering-based analysis backed by AuditDefense for your entire ownership period.

Contact Seneca at +1 530-797-6539 or info@senecacostseg.com to schedule your no-obligation consultation.