Introduction

Many real estate investors operate under a costly misconception: if they didn't perform a cost segregation study when they acquired a property, they've permanently forfeited the right to accelerated depreciation. The reality is the IRS provides a clear correction mechanism through Form 3115 (Application for Change in Accounting Method), allowing retroactive depreciation adjustments without disturbing prior-year returns.

The real obstacle is the assumption that correcting past depreciation requires amending multiple tax returns — a process that reopens statute of limitations periods and invites scrutiny. Form 3115 eliminates that risk by consolidating all prior-year missed depreciation into a single current-year filing through what's called a Section 481(a) adjustment.

This guide covers how to use Form 3115 to claim catch-up depreciation from a cost segregation study, including:

- What documentation to prepare

- Which form sections to complete

- How to calculate the Section 481(a) adjustment

- How the filing mechanics work under the IRS's automatic change procedures

TL;DR

- Form 3115 captures all prior-year missed depreciation in one current-year deduction—no amended returns needed

- The Section 481(a) adjustment consolidates all missed deductions into your current-year return as one lump-sum deduction

- If you've used an incorrect depreciation method for two or more consecutive years, filing Form 3115 is required—not optional

- DCN 7 applies to assets still in service; DCN 107 covers assets that have already been disposed of

- Without an engineering-based cost segregation study, most investors significantly underestimate the deductions available through this process

When Should You Use Form 3115 for Catch-Up Depreciation?

Knowing when Form 3115 applies—versus when to amend a return or use a different correction method—saves time and prevents rejected filings. The rules are specific.

The Two-Year Rule

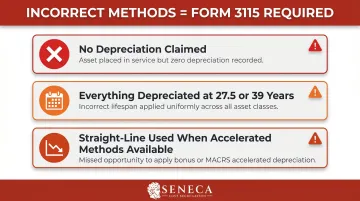

Once you've used an incorrect depreciation method for two consecutive tax years, the IRS considers that method "adopted." At that point, amending prior returns is no longer permitted—Form 3115 becomes the only correction vehicle.

An "incorrect method" includes:

- Taking no depreciation at all on a property

- Depreciating everything over 27.5 or 39 years when 5-, 7-, and 15-year components exist

- Using straight-line depreciation when accelerated methods are available

When Form 3115 Is the Right Move

Form 3115 is appropriate when:

- You acquired a building in a prior year without performing cost segregation

- You're now reclassifying components to 5-, 7-, or 15-year property for the first time

- The incorrect method has been in place for at least two consecutive filed returns

Contrast this with situations where:

- Only one year has passed (amendment still available)

- A simple math or posting error exists (correctable within statute of limitations)

- The error stems from changed facts, not a method change

When Form 3115 Cannot Be Used

The IRS explicitly prohibits Form 3115 for:

- Changing a placed-in-service date

- Making or revoking a Section 179 election

- Making or revoking bonus depreciation elections

- Changing a useful life not assigned by code or regulation

- Correcting mathematical errors or posting mistakes

Each of these situations calls for a different IRS procedure—none qualifies as an accounting method change, so Form 3115 won't help and could complicate the filing.

What You Need Before Filing Form 3115

Engineering-Based Cost Segregation Study

The cost segregation study is the technical foundation justifying your method change. It must:

- Reclassify building components into correct MACRS asset classes (5-, 7-, 15-year property)

- Include component-level documentation with supporting calculations

- Follow IRS Cost Segregation Audit Techniques Guide methodology

- Provide the numbers used to calculate the 481(a) adjustment

If your study lacks component-level detail, the IRS can challenge your 481(a) adjustment during examination. Seneca Cost Segregation's engineering-based studies are completed in 2–4 weeks and are structured to meet that documentation standard.

Complete Depreciation Schedule History

You need a depreciation schedule showing what you've actually claimed since the property was placed in service. Use it to calculate the difference between:

- Depreciation taken (what you claimed)

- Depreciation allowable (what you should have claimed)

This difference is the Section 481(a) adjustment.

Property Acquisition Documentation

Calculating the 481(a) adjustment accurately also depends on the original acquisition details. Form 3115 and Schedule E require:

- Placed-in-service year

- Original cost basis

- Any tax credits, grants, or subsidies received

- Business use percentage

How to File Form 3115 for Catch-Up Depreciation (Step-by-Step)

Form 3115 follows the automatic change procedures under Rev. Proc. 2015-13, and skipping or misordering steps can result in rejected filings or loss of audit protection.

Step 1: Identify the Correct DCN and Filing Type

For cost segregation catch-up, use:

- DCN 7 — "Depreciation or amortization (impermissible to permissible)" for assets still in service

- DCN 107 — Same change, but for assets already disposed of

Both fall under automatic change procedures, meaning:

- No user fee required

- No advance IRS approval needed

- Consent is granted by procedure if filing complies with requirements

You still bear full responsibility for the accuracy and completeness of every filing.

Step 2: Complete Form 3115 and Schedule E

Required sections:

| Section | What to Include |

|---|---|

| Part I | Enter DCN 7 on Line 1a |

| Part II | Property information, examination status, audit protection eligibility |

| Part IV | Section 481(a) adjustment calculation and methodology |

| Schedule E | Property description, type, placed-in-service year, business use |

Schedule E attachments must include:

- Detailed description of prior depreciation method

- Detailed description of proposed method (using cost segregation reclassification)

- Written statement supporting the reclassification under cost segregation methodology

- Year the property was placed in service

Step 3: Calculate and Enter the Section 481(a) Adjustment

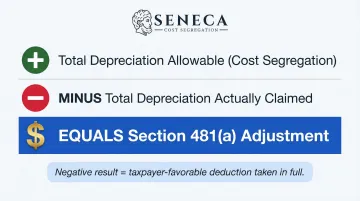

The 481(a) adjustment equals:

Total depreciation allowable under cost segregation (from placed-in-service date through end of prior year)

MINUS

Total depreciation actually claimed (over same period)

EQUALS

Section 481(a) adjustment (typically negative — meaning taxpayer-favorable)

A negative adjustment is deducted in full in the year of change, reducing taxable income immediately.

Step 4: File the Original and Duplicate Copy Correctly

Two-copy requirement (critical):

- Original: Attach to your timely filed federal income tax return for the year of change

- Duplicate: Send signed copy to IRS National Office in Ogden, UT no earlier than the first day of the year of change and no later than the return filing date

Common error: Filing only one copy. Both are required.

Ogden address:

Internal Revenue Service

Ogden Submission Processing Center

1973 N Rulon White Blvd.

Ogden, UT 84201

Step 5: Report the Deduction on the Tax Return

The negative 481(a) adjustment flows through as additional depreciation in the year of change. For investors who qualify, this deduction can offset active income — significantly increasing the tax benefit.

Two common qualifying pathways:

- Real Estate Professional Status (REPS) under IRC §469(c)(7)

- Short-Term Rental (STR) exception — average customer use ≤7 days with material participation

How to Calculate the Section 481(a) Adjustment

The Foundational Logic

The Section 481(a) adjustment prevents taxpayers from either double-deducting or permanently losing deductions when accounting methods change. It captures the cumulative difference from the property's placed-in-service date through the last day before the year of change.

Calculation Sequence

Step 1: Determine total depreciation allowable under cost segregation

Using component reclassification, calculate what depreciation would have been from placed-in-service date through end of prior year.

Step 2: Determine total depreciation actually claimed

Sum all depreciation deductions taken under the prior method over the same period.

Step 3: Calculate the adjustment

Allowable minus actual = Section 481(a) adjustment

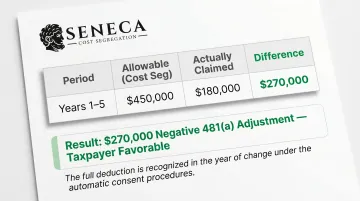

Example:

| Period | Allowable (Cost Seg) | Actually Claimed | Difference |

|---|---|---|---|

| Year 1-5 | $450,000 | $180,000 | $270,000 |

Result: $270,000 negative 481(a) adjustment (taxpayer-favorable)

The "Allowed or Allowable" Rule

Under IRC §1016(a)(2), the IRS reduces your property's basis by depreciation "allowed or allowable", even if you never claimed it. This means:

- If you don't claim depreciation, you still lose basis

- When you sell, recapture is calculated on what you could have claimed

- You get taxed on deductions you never took

Form 3115 with DCN 7 offsets this penalty by allowing catch-up deductions for corrected assets, so you recover the deductions you were already losing basis on.

Spread Period Rules

Negative adjustment (taxpayer-favorable):

Deducted entirely in the year of change.

Positive adjustment (IRS-favorable, rare in cost segregation):

Generally spread ratably over four tax years, unless under $50,000—then you may elect to recognize it all in the year of change.

Depreciation Recapture on Future Sale

Understanding the spread period matters because it affects your tax position heading into a sale. When you eventually sell the property:

- Section 1245 recapture applies to personal property components (5/7-year assets)

- Section 1250 recapture applies to real property (27.5/39-year assets)

Recapture is based on "allowed or allowable" depreciation whether or not you claimed the deductions. Since recapture applies either way, claiming the catch-up deduction now means you get the tax benefit without taking on additional recapture exposure.

Best Practices for Using Form 3115 Effectively

Engage a Qualified Cost Segregation Firm First

The quality of your cost segregation study directly determines:

- Accuracy of the 481(a) adjustment

- Strength of audit protection

- CPA willingness to sign the return

Engineering-based studies with component-level documentation are far more defensible than rule-of-thumb estimates. ASCSP-certified providers like Seneca Cost Segregation deliver studies built to IRS documentation standards—with licensed engineers on staff and AuditDefense backed by a money-back guarantee.

File Proactively, Not Reactively

Form 3115 must be filed by the due date of your return (including extensions) for the year of change. Missing that window creates real problems:

- Filing after your return is submitted eliminates access to automatic consent procedures

- Filing after an IRS examination begins removes audit protection entirely

Plan ahead to allow time for the cost segregation study (typically 2–4 weeks) and CPA coordination.

Maintain Thorough Documentation

Retain the complete chain:

- Cost segregation study report with all schedules

- Depreciation schedules for all prior years

- Filed Form 3115 with all attachments

- Proof of duplicate copy filing (certified mail receipt or fax confirmation)

The IRS does not send acknowledgment for automatic change requests—you must maintain your own proof of timely submission.

Frequently Asked Questions

How to calculate catch-up depreciation?

Catch-up depreciation equals total depreciation allowable under cost segregation (from placed-in-service date forward) minus depreciation actually claimed. This difference becomes the Section 481(a) adjustment, deducted in full in the current year.

Can you catch-up on missed depreciation?

Yes, the IRS allows retroactive catch-up through Form 3115 (Application for Change in Accounting Method). No amended returns are needed—the entire cumulative missed deduction is taken in the current tax year via a Section 481(a) adjustment.

What is the accelerated depreciation rule?

Accelerated depreciation allows certain asset classes (5-, 7-, or 15-year property identified through cost segregation) to be depreciated faster than the standard 27.5- or 39-year straight-line method. This front-loads deductions, reducing taxable income by a material amount in the early years of ownership.

Do I need to amend prior tax returns to claim missed depreciation from a cost segregation study?

No amendments are needed. Once you've used an incorrect depreciation method for two or more consecutive years, Form 3115 is the correct vehicle — all missed deductions are captured in a single current-year filing.

What is the Section 481(a) adjustment?

The Section 481(a) adjustment is the cumulative accounting correction that appears on your tax return in the year the method change takes effect. For cost segregation catch-up, it's typically a negative (favorable) adjustment reducing taxable income by the full amount of previously unclaimed accelerated depreciation.

What happens to depreciation recapture if I file Form 3115 and later sell the property?

Depreciation recapture applies upon sale regardless of whether deductions were actually taken—the IRS reduces basis by "allowed or allowable" depreciation. Claiming catch-up via Form 3115 doesn't increase tax burden on sale; it ensures you receive the benefit you'll be taxed on either way.