Introduction

Rental property owners pay taxes on rental income—but most don't realize how many legal deductions the IRS allows to reduce or even eliminate that tax burden. According to IRS Publication 527, landlords can deduct "ordinary and necessary" expenses for managing, conserving, and maintaining rental properties, from mortgage interest and repairs to depreciation strategies that can generate six-figure deductions in year one. Most rental property owners still leave significant tax savings unclaimed — particularly when it comes to accelerated depreciation strategies like cost segregation.

This guide covers the rental property tax deductions the IRS allows — including the ones most investors overlook — so you keep more of what you earn. Whether you own one single-family rental or a growing multi-family portfolio, knowing which expenses to deduct immediately versus capitalize determines how much you actually keep and whether your returns hold up under IRS scrutiny.

TLDR

- Landlords can deduct mortgage interest, property taxes, insurance, repairs, management fees, utilities, professional services, and travel costs

- Depreciation typically provides the largest single deduction, recovering the building's cost over 27.5 years

- Cost segregation accelerates depreciation by reclassifying 20–40% of property costs into shorter 5- and 15-year schedules, often generating six-figure first-year deductions

- Capital improvements must be depreciated, not immediately expensed—use the IRS BAR Test to classify expenses correctly

- Thorough recordkeeping and a qualified real estate tax professional are essential to maximize deductions and hold up under IRS scrutiny

Common Rental Property Tax Deductions You Can Write Off

The IRS standard is straightforward: deductible expenses must be "ordinary and necessary" for managing, conserving, and maintaining the rental property. This filter should guide every expense decision you make. If the cost is typical for landlords and helps operate or preserve the property, it likely qualifies.

Financing and Ownership Costs

Mortgage interest is typically the largest single ongoing deduction for most landlords. Your lender provides Form 1098 each year documenting the interest paid — only the interest portion is deductible, not the principal.

Other ownership costs that qualify:

- Mortgage points — deductible over the life of the loan, not all at once

- Property taxes — fully deductible in the year assessed

- Landlord insurance (hazard, liability, flood) — deductible in the year the premium applies

- Prepaid insurance premiums — must be allocated to the specific years of coverage, not deducted early

Operating and Management Costs

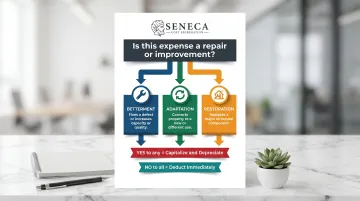

Repairs and routine maintenance are deductible in the year paid. The critical distinction is between repairs (which restore working condition) and improvements (which add value and must be depreciated).

The IRS BAR Test provides a simple framework:

- Betterment: Fixes a pre-existing defect or increases the property's capacity, strength, or quality

- Adaptation: Converts the property to a new or different use from its original purpose

- Restoration: Replaces a major structural component or rebuilds it to like-new condition

If the answer to any question is "yes," the expense is an improvement that must be capitalized and depreciated. If "no" to all three, it's a repair you can deduct immediately.

Core operating expenses deductible in the year incurred:

- Utilities paid by the landlord (water, sewer, electric, gas)

- Property management fees

- Advertising and tenant screening costs

- Professional services (attorneys, accountants, tax preparers) related to rental activity

Travel Expenses

Travel expenses related to the rental are deductible—local mileage for inspections or maintenance visits at the IRS standard rate of 70 cents per mile for 2025, and long-distance travel to manage the property. However, commuting from home to a nearby rental is generally not deductible unless the home is the principal place of business for the rental activity.

Other Allowable Deductions

Wages and fees paid to contractors, plumbers, electricians, landscapers, and property managers are all deductible in the year paid.

If you manage your rentals from a dedicated home workspace, the home office deduction applies under two methods:

- Simplified method: $5 per square foot, up to 300 square feet ($1,500 cap)

- Standard method: Proportional share of actual home expenses based on square footage

Casualty and theft losses may be deductible when property is damaged by a sudden event — fire, storm, or natural disaster — and the loss exceeds your insurance coverage. You can deduct the uncovered portion, subject to IRS rules on federally declared disaster areas.

These deductions cover the fundamentals, but they only capture a portion of what most rental properties can offset. Depreciation — particularly through a cost segregation study — often delivers the largest single tax reduction available to real estate investors.

Depreciation: Your Biggest Rental Property Deduction

Depreciation is the IRS allowing you to deduct the cost of the building gradually over its useful life, recognizing that the structure wears down over time. This is a non-cash deduction—it reduces taxable income without requiring you to spend money each year.

How Residential Depreciation Works

Residential rental properties are depreciated over 27.5 years under the Modified Accelerated Cost Recovery System (MACRS). This means roughly 1/27th of the building's cost basis is deductible each year. Land is never depreciable—you must subtract the land value from the purchase price to determine the building's depreciable basis.

Example: You buy a rental property for $400,000. The land is valued at $100,000, leaving a building basis of $300,000. Your annual depreciation deduction would be $300,000 ÷ 27.5 = $10,909.

Depreciation Is Not Optional

The IRS calculates depreciation recapture tax upon sale whether or not you actually claimed the deduction. Failing to take the deduction means paying tax on a benefit you never received. The recapture is based on depreciation "allowed or allowable"—what you should have claimed, not what you did claim.

Depreciating Improvements and Personal Property

Improvements to the property—new roof, HVAC system, major renovation—are also depreciated, not expensed immediately. Depreciation starts in the year the improvement is placed in service. Personal property inside the rental (appliances, carpeting, furniture) can be depreciated over a shorter 5-year schedule.

Bonus Depreciation

The One, Big, Beautiful Bill Act (OBBBA) permanently restored 100% bonus depreciation for qualified property acquired and placed in service after January 19, 2025, per IRS guidance on the provision. This allows you to immediately deduct the full cost of eligible short-lived assets rather than spreading deductions over decades.

Cost Segregation: The Most Overlooked Rental Property Tax Deduction

Cost segregation is an IRS-approved engineering study that reclassifies components of a building from the 27.5-year depreciation schedule to shorter 5-, 7-, or 15-year categories. Components like flooring, lighting, landscaping, and specialty electrical are legally reclassified, accelerating depreciation deductions into the early years of ownership.

The Financial Impact

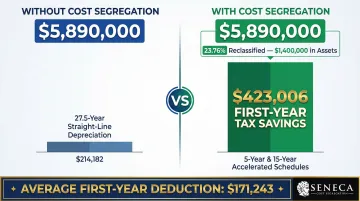

Instead of deducting a small fraction of the property's value each year, a cost segregation study can reclassify 20-40% or more of a property's cost into shorter-lived asset categories—creating significantly larger deductions in year one. Seneca Cost Segregation has completed over 10,200 property assessments, achieving an average first-year deduction of $171,243 across their client base.

Real example: A multi-family townhome property purchased for $5.89 million underwent cost segregation analysis. The study reclassified 23.76% of the property—$1,403,836 in assets—to 5- and 15-year schedules. Combined with 100% bonus depreciation, this generated $423,006 in first-year tax savings.

Who Benefits Most

Cost segregation delivers the strongest ROI for owners who meet any of these criteria:

- Properties purchased or renovated for $300,000 or more (excluding land value)

- Buildings already owned where depreciation was never accelerated ("look-back" studies)

- Investors who want to capture missed deductions from prior years without amending returns — done via IRS Form 3115

IRS Compliance Requirements

Once you've confirmed you're a good candidate, the quality of the study itself determines whether those deductions hold up under review. The IRS Cost Segregation Audit Techniques Guide explicitly warns against "rule of thumb" methods that apply fixed percentages without proper documentation — only engineering-based analysis meets the IRS standard.

Seneca Cost Segregation uses proprietary technology, licensed engineers, and an AuditDefense guarantee to ensure every study is compliant and optimized for the highest allowable deductions.

What You Cannot Deduct on Rental Property

Many rental property owners claim deductions they're not entitled to — triggering IRS scrutiny and unexpected tax bills. Knowing where the line is keeps your returns clean.

Capital Improvements

Costs that add value to the property, extend its useful life, or adapt it to a new use cannot be expensed immediately. Examples include:

- New addition or major expansion

- Roof replacement

- Full kitchen or bathroom remodel

- New HVAC system

- Structural repairs

These must be capitalized and recovered through depreciation over the appropriate recovery period.

Personal Expenses

Personal expenses are never deductible, even when tied to the property. Mixed-use properties are the common trap: if you use a rental for personal purposes more than 14 days — or more than 10% of rental days — you must split expenses between rental and personal use. Only the rental share qualifies.

Other Non-Deductible Items

- Local benefit taxes: Assessments for street improvements, sidewalks, or water lines that increase property value must be added to your cost basis instead

- Commuting costs: Travel from home to nearby rental properties is not deductible unless your home is your principal place of business

- Prepaid expenses: Costs covering future tax years beyond the current filing period cannot be deducted now

How to Maximize Your Rental Property Tax Deductions

Keep Meticulous Records

Retain receipts, invoices, bank statements, mileage logs, and Form 1098 for every deductible expense. Without documentation, valid deductions won't hold up in an IRS audit. Records relating to property basis and improvements must be kept until the period of limitations expires for the year you dispose of the property.

Work With a Real Estate Tax Professional

Tax laws change regularly, including bonus depreciation phasedowns, SALT cap updates, and new IRS regulations. A CPA or tax advisor familiar with rental property can identify deductions that general tax software misses. Seneca Cost Segregation offers complimentary tax assessments to help investors evaluate their full tax picture, not just cost segregation opportunities.

Use the De Minimis Safe Harbor

Landlords can elect to immediately expense items costing $2,500 or less per item (or $5,000 with an applicable financial statement) rather than depreciating them. This simplifies accounting for smaller purchases like appliances, tools, or minor fixtures. To claim this election:

- Expense threshold is $2,500 per item (or $5,000 with an applicable financial statement)

- Applies to smaller purchases such as appliances, tools, and minor fixtures

- Attach a statement titled "Section 1.263(a)-1(f) de minimis safe harbor election" to your timely filed return

Frequently Asked Questions

What can you write off for rental property?

Landlords can deduct mortgage interest, property taxes, insurance, repairs and maintenance, depreciation, management fees, utilities, professional services, and travel expenses—provided these costs are ordinary and necessary for the rental activity.

Can you write off repairs and maintenance on a rental property?

Yes, repairs are fully deductible in the year paid. However, improvements that add value or extend the property's life must be capitalized and depreciated. Use the IRS BAR Test (Betterment, Adaptation, Restoration) to determine the correct classification.

What is the $2,500 expense rule for rental property?

The IRS De Minimis Safe Harbor election allows rental property owners to immediately deduct items costing $2,500 or less per item (rather than depreciating them). This simplifies recordkeeping for smaller purchases like appliances or minor fixtures.

How does the new $6,000 tax deduction work for rental property?

No federal tax provision grants a blanket "$6,000 rental property deduction" — this figure likely stems from confusion with other legislative proposals. Landlords must rely on actual documented expenses and MACRS depreciation rules. Confirm any new deduction with your tax advisor.

How can I maximize deductions for a rental property?

Keep thorough records of all expenses, work with a real estate-savvy tax professional, and consider a cost segregation study to accelerate depreciation deductions. These steps can significantly increase first-year write-offs and improve long-term cash flow.

What is the most overlooked tax deduction for rental property?

Depreciation acceleration through cost segregation is the most commonly missed strategy. Most landlords default to straight-line depreciation over 27.5 years, leaving tens of thousands of dollars on the table by not reclassifying assets into shorter depreciation schedules.