Introduction

Converting a primary residence into a rental property triggers a complex set of IRS depreciation rules that differ substantially from standard rental property treatment. Homeowners who make this transition often face costly tax errors: either overstating deductions by using their original purchase price as the basis, or understating them by failing to properly allocate between land and structure.

According to Treasury Regulation §1.168(i)-4(b), the depreciable basis of a converted residence is the lesser of its adjusted cost basis or its fair market value at conversion. This rule exists specifically to prevent taxpayers from deducting personal-use losses through their rental activity.

This guide is for individual homeowners and real estate investors navigating the conversion of a former primary residence to a rental property. Whether you're an accidental landlord relocating for work, a house hacker moving on to your next property, or a strategic investor building a portfolio, the depreciation rules here carry real financial stakes.

Getting them wrong can trigger IRS audits, leave legitimate deductions unclaimed, or create unexpected tax bills when you sell.

Here's what this article covers:

- How the depreciable basis is determined at the time of conversion

- How the 27.5-year MACRS schedule applies to a converted residence

- Common mistakes that lead to audits or missed deductions

- What happens to accumulated depreciation when you sell, including how depreciation recapture interacts with the Section 121 exclusion

TL;DR

- Depreciation starts when the property is placed into service as a rental, not from the original purchase date

- Your basis is the lower of adjusted cost basis or fair market value at conversion (land is always excluded)

- Residential rentals depreciate over 27.5 years using the MACRS straight-line method (approximately 3.636% annually)

- At sale, depreciation recapture is taxed up to 25%, even when the Section 121 exclusion shields other gains

- Strategic timing of improvements after conversion can directly increase your deductible basis

What Is Depreciation on a Converted Primary Residence?

Rental property depreciation is the IRS-allowed annual deduction that reduces your taxable rental income by accounting for the gradual wear and deterioration of a residential structure over its useful life. Under IRC §168(e)(2)(A), properties where 80% or more of income comes from dwelling units qualify as residential rental property and follow Modified Accelerated Cost Recovery System (MACRS) rules.

How Converted Properties Differ from Direct Rental Purchases

A converted primary residence differs from a property purchased as a rental from the start: the depreciation basis is not automatically the purchase price. The IRS applies a "lower of" rule at conversion to prevent homeowners from deducting losses that accrued during personal use.

If your home declined in value while you lived in it, that decline cannot become rental loss deductions. It's permanently lost for tax purposes.

Land Is Never Depreciable

Only the building structure and improvements are depreciable. IRS Publication 527 is explicit on this point:

"Because land isn't depreciable, you can only include the cost of the house when figuring the basis for depreciation." (IRS Publication 527)

This applies regardless of what the land was worth at purchase or conversion. To allocate correctly, most investors use the land-to-improvement ratio from their county tax assessment records or a qualified appraisal at the time of conversion.

How to Calculate Your Depreciation Basis After Conversion

Step 1: Determine Your Adjusted Cost Basis

Start with the original purchase price, then add:

- Closing costs attributable to the purchase (title fees, recording fees, legal costs)

- Capital improvements made during personal use (new roof, room additions, kitchen remodel, HVAC replacement)

Then subtract:

- Prior casualty loss deductions claimed

- Energy credits or other basis-reducing credits taken

For example, if you purchased the home for $350,000, paid $8,000 in acquisition closing costs, and invested $42,000 in a kitchen remodel and new roof during personal use, your adjusted cost basis would be $400,000 (before land allocation).

With your adjusted basis in hand, the next input you need is what the property was actually worth on the day you converted it.

Step 2: Establish Fair Market Value at Conversion

Determine the property's fair market value (FMV) on the exact date of conversion to rental use. This is typically established through:

- Professional appraisal (strongest IRS audit protection)

- Documented comparable market analysis

- Recent purchase offers or listing prices

Critical: This must be the FMV of the structure only, not the entire property including land. Securing formal documentation at the time of conversion prevents future IRS disputes over your depreciable basis.

Step 3: Apply the "Lower of" Rule

Treasury Regulation §1.168(i)-4(b) requires using the lesser of adjusted basis or FMV. Here's a concrete example:

Scenario A (Declining Market):

| Item | Value |

|---|---|

| Adjusted cost basis of structure (excluding land) | $210,000 |

| FMV at conversion (structure only) | $175,000 |

| Depreciable basis | $175,000 (the lower amount) |

Scenario B (Appreciating Market):

| Item | Value |

|---|---|

| Adjusted cost basis of structure | $210,000 |

| FMV at conversion (structure only) | $245,000 |

| Depreciable basis | $210,000 (the lower amount) |

The IRS illustrates this directly in the regulation: a taxpayer converts her principal residence in February 2004, when the house FMV (excluding land) is $130,000 but the adjusted depreciable basis is $150,000. The depreciable basis is $130,000; the lower figure wins.

Step 4: Allocate Between Land and Structure

The total property value must be split between land (non-depreciable) and building (depreciable). IRS-approved methods include:

- County assessor ratios: IRS Publication 527 allows you to split land and building value based on assessed values for real estate tax purposes

- Professional appraisals: Appraisals and comparable sales data from the conversion date provide the strongest documentation

Example Allocation:

- Total FMV at conversion: $400,000

- County assessor shows land at 25% of total value

- Land value: $100,000 (non-depreciable)

- Building value: $300,000 (depreciable basis)

The Declining-Value Market Trap

If your home lost value between purchase and conversion, the lower FMV basis locks in a smaller depreciation deduction and caps the loss that can ever be recognized on a future sale.

This is intentional IRS policy: personal-use losses don't become deductible just because you later rent the property. Once the lower basis is set at conversion, you cannot recover those pre-conversion losses through depreciation or a sale.

How the 27.5-Year Depreciation Schedule Works

MACRS Straight-Line Method

Residential rental property is depreciated over 27.5 years using the MACRS straight-line method under IRC §168(c). The depreciable basis is divided equally across the recovery period, resulting in approximately 3.636% deducted per year in years 2 through 27.

Example:

- Depreciable basis: $300,000

- Annual depreciation: $300,000 ÷ 27.5 = $10,909

Partial-Year Depreciation: The Mid-Month Convention

The IRS uses the mid-month convention under IRC §168(d)(2)(B), which treats property placed in service during any month as placed in service at that month's midpoint. This affects your first-year deduction.

Example: If you convert your home to a rental on July 15 (making it available for rent), the IRS treats it as placed in service on July 15. You can claim depreciation for 5.5 months (mid-July through December) in the first year, which equals approximately 1.667% of the depreciable basis.

IRS Publication 527 clarifies: "You place property in service in a rental activity when it is ready and available for a specific use in that activity. Even if you aren't using the property, it is in service when it is ready and available for its specific use." Depreciation begins when the property is ready and available for rent, not necessarily when a tenant moves in.

Strategic Timing of Improvements

Critical Planning Point: Improvements and renovations completed after the property is placed into service are added to the depreciable basis, whereas the same work done before conversion is treated as a personal expense with no current deduction.

Example:

| Timing | Description | Treatment |

|---|---|---|

| Pre-conversion remodel | $15,000 spent on flooring before listing the property | Added to adjusted basis, subject to "lower of" rule |

| Post-conversion improvement | $15,000 spent on flooring after property is available for rent | Fully depreciable addition to basis |

Completing major renovations after the property is placed in service, rather than before, can convert non-deductible personal expenses into depreciable basis, directly increasing your annual deduction.

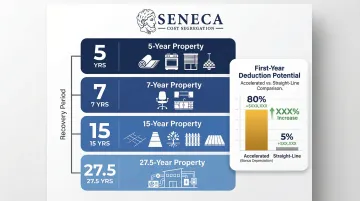

Cost Segregation Acceleration

While the standard 27.5-year schedule applies to the building structure, certain components can be reclassified into shorter depreciation lives through engineering-based cost segregation studies. The IRS Cost Segregation Audit Techniques Guide and Revenue Procedure 87-56 permit qualified studies to identify:

| Property Class | Examples |

|---|---|

| 5-year property | Carpeting, appliances (refrigerators, stoves, dishwashers), window treatments, decorative lighting |

| 7-year property | Office furniture and certain fixtures |

| 15-year property | Land improvements (parking lots, sidewalks, landscaping, fencing, decks) |

| 27.5-year property | Core building structure and permanent systems |

For a converted primary residence with a $900,000 depreciable basis, cost segregation might reclassify 20-30% of the value into these shorter categories. With 100% bonus depreciation, that translates to first-year deductions of $200,000+, compared to the standard $32,727 annual deduction under straight-line depreciation.

The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate |

|---|---|

| September 27, 2017 – December 31, 2022 | 100% |

| January 1, 2023 – December 31, 2023 | 80% |

| January 1, 2024 – December 31, 2024 | 60% |

| January 1, 2025 – January 18, 2025 | 40% |

| January 19, 2025 – December 31, 2030 | 100% (if acquisition date is January 19, 2025 or later) |

If acquisition date is before January 19, 2025:

- 40% bonus depreciation applies in 2025

- 20% bonus depreciation applies in 2026

An engineering-based cost segregation study documents these reclassifications using IRS-compliant methodology, giving your CPA the audit-ready support needed to claim accelerated deductions with confidence. Seneca Cost Segregation typically completes studies within 2-4 weeks and has averaged $171,243 in first-year deductions across more than 10,200 properties assessed.

Common Mistakes and Misconceptions

Misconception 1: Using Original Purchase Price as Depreciation Basis

Many homeowners assume they simply depreciate what they paid for the home, completely ignoring the "lower of" rule. This leads to either:

- Overstating deductions if the home appreciated (triggering IRS adjustments and penalties)

- Understating deductions if proper capital improvements weren't added to basis (leaving money on the table)

The IRS requires comparing adjusted cost basis to FMV at conversion and using the lower amount. No exceptions.

Misconception 2: Including Land in Depreciable Basis

Land never depreciates under any circumstances. IRS Publication 946 states: "You cannot depreciate the cost of land because land does not wear out, become obsolete, or get used up."

Failing to allocate value between land and structure is one of the most common Schedule E errors, and an unsupported allocation puts your entire depreciable basis into question during an audit. The IRS requires figures based on real-world, accurate data, not estimates.

Using the total purchase price without subtracting land value overstates depreciation, a mistake that typically requires correction with penalties and interest attached.

Misconception 3: Depreciation Is Optional

Some property owners skip depreciation to avoid recapture taxes at sale. It doesn't work that way.

IRC §1016(a)(2) requires basis reduction for depreciation "allowed or allowable," meaning the IRS calculates recapture on depreciation you could have claimed, whether or not you took the deductions. Two authoritative sources confirm this:

- IRS Publication 544: "If you did not take any deduction at all for depreciation, your adjustments to basis for depreciation allowable are figured by using the straight-line method."

- IRS FAQ on Depreciation Recapture: "You must reduce your basis in your home by the greater of the allowed or allowable depreciation."

Skipping depreciation forfeits your annual deductions while the 25% recapture tax still applies at sale.

What Happens When You Sell: Depreciation Recapture and Section 121

Depreciation Recapture at 25%

When you sell a converted primary residence at a gain, the IRS subjects all depreciation taken (or allowable) during the rental period to "unrecaptured Section 1250 gain" tax. Under IRC §1(h)(1)(E), that gain is taxed at a maximum federal rate of 25%, notably higher than the 0%, 15%, or 20% long-term capital gains rates that might otherwise apply.

Example:

| Item | Amount |

|---|---|

| Original purchase price | $300,000 |

| Depreciable basis at conversion | $250,000 (after land allocation) |

| Total depreciation claimed over 5 years | $45,455 |

| Sale price | $400,000 |

| Adjusted basis at sale | $254,545 ($300,000 - $45,455) |

| Total gain | $145,455 |

| Depreciation recapture (taxed at 25%) | $45,455 |

| Remaining capital gain (taxed at 0-20%) | $100,000 |

Section 121 Interaction: Partial Exclusion Only

The Section 121 primary residence exclusion allows taxpayers to exclude up to $250,000 (single) or $500,000 (married filing jointly) of gain from the sale of a principal residence. However, IRC §121(d)(6) contains a strict carve-out:

"Subsection (a) shall not apply to so much of the gain from the sale of any property as does not exceed the portion of the depreciation adjustments... attributable to periods after May 6, 1997."

Translation: The Section 121 exclusion can shield appreciation in value from capital gains tax, but depreciation taken after May 6, 1997 cannot be excluded; it must be recaptured and taxed separately at 25%, regardless of how long you owned or lived in the home.

The 2-Out-of-5-Year Requirement

To qualify for Section 121 exclusion on the non-depreciation portion of gain, IRC §121(a) requires ownership and use as a principal residence for at least 2 of the 5 years ending on the sale date.

If you rent for more than 3 consecutive years without returning to the home, you fail the use test and lose the Section 121 exclusion entirely, not just on depreciation, but on all gain. Sell within roughly 3 years of conversion and you can still exclude appreciation, though the depreciation portion remains taxable at 25%.

Basis Adjustment on Sale

For gain calculations, your tax basis at sale equals:

Original (or Converted) Basis + Capital Improvements - All Depreciation Taken

Example:

| Item | Amount |

|---|---|

| Original purchase | $350,000 |

| Capital improvements during personal use | $50,000 |

| Adjusted cost basis | $400,000 |

| Land allocation | $100,000 |

| Depreciable basis at conversion | $300,000 |

| Depreciation claimed over 6 years | $65,455 |

| Adjusted basis at sale | $334,545 ($400,000 - $65,455) |

| Sale price | $475,000 |

| Total taxable gain | $140,455 |

Accumulated depreciation reduces your adjusted basis dollar-for-dollar, directly inflating your taxable gain. The picture changes, however, when you sell at a loss.

The "Two-Basis" Loss Scenario

A special "two-basis" rule under IRS Publication 551 governs loss sales, blocking deductions for value declines that occurred during personal use.

The rule: Calculate basis for loss starting with the smaller of your adjusted basis or the FMV at conversion, then adjust for post-conversion changes.

Three possible outcomes:

| Sale Price Scenario | Tax Outcome |

|---|---|

| Above original adjusted basis | Taxable gain, subject to Section 121 exclusion (if eligible) and 25% unrecaptured Section 1250 tax |

| Below FMV at conversion | Deductible rental loss, calculated using FMV at conversion minus post-conversion depreciation |

| Between FMV and original basis | Zero gain, zero loss: the "no man's land" where the decline during personal use is permanently non-deductible |

Example of "no man's land":

| Item | Amount |

|---|---|

| Original adjusted basis | $400,000 |

| FMV at conversion | $350,000 (home declined during personal use) |

| Depreciation taken | $50,000 |

| Sale price | $375,000 |

| Result | No reportable gain or loss (sale price is above the depreciation-adjusted FMV basis of $300,000 but below the original $400,000 basis) |

That $50,000 decline in value during personal use disappears permanently; it can never be deducted, even if the property later sells at a price that would otherwise suggest a loss. Running this calculation before you sell can prevent an unpleasant surprise at tax time.

Frequently Asked Questions

Frequently Asked Questions

How to depreciate rental property that was primary residence?

Depreciation begins when the property is placed in service as a rental (made available for rent). The basis is the lower of adjusted cost basis or fair market value at conversion, with land excluded. Residential property is depreciated over 27.5 years using the MACRS straight-line method, yielding approximately 3.636% annually.

What is the 2 out of 5 year rule?

This rule governs eligibility for the Section 121 capital gains exclusion. To qualify, you must have owned and used the property as your primary residence for at least 2 of the 5 years immediately preceding the sale.

What is the 6 year rule for main residence?

The "6-year rule" does not exist under U.S. tax law; it is a concept in Australian tax law. The relevant U.S. rule is the 3-year window after conversion during which the Section 121 exclusion may still apply, provided the 2-out-of-5-year use test was met before conversion.

When does depreciation start on a converted rental property?

Depreciation starts in the month the property is "placed in service," meaning made available for rent, not necessarily when a tenant moves in. The mid-month convention applies in the first year, treating the property as placed in service at the mid-point of that month.

Can I avoid depreciation recapture if I move back into my rental property?

Moving back in can re-qualify the property for Section 121 exclusion on future appreciation, but depreciation taken during the rental period remains subject to unrecaptured Section 1250 gain tax at up to 25%. Recapture cannot be erased by re-establishing personal use.

What is the 50% rule in rental property?

The 50% rule is a real estate investing rule of thumb (not an IRS rule) suggesting that roughly 50% of gross rent should be set aside for operating expenses (excluding mortgage). It's used to estimate cash flow and is unrelated to depreciation rules.

Converting a primary residence to a rental unlocks real depreciation benefits, provided you apply the "lower of" basis rule correctly, allocate land properly, and plan for recapture at sale. For higher-value properties, an engineering-based cost segregation study from Seneca Cost Segregation can reclassify 20–40% of your building basis into shorter-lived assets, generating first-year deductions that would otherwise be spread across 27.5 years. Getting these rules right from day one keeps your tax position defensible and your cash flow working harder.