Introduction

Real estate investors face a higher audit risk than most filers — and it has nothing to do with wrongdoing. Depreciation schedules across multiple properties, rental income streams, large deductions, and strategies like cost segregation all create the kind of statistical complexity that IRS screening algorithms flag.

An audit is not an accusation of wrongdoing. It's a request for documentation. Investors who struggle through audits are almost always the ones who weren't prepared. Knowing the triggers and keeping meticulous records in advance makes all the difference.

This guide covers the specific triggers that raise red flags with IRS algorithms, the advanced strategies the IRS scrutinizes most heavily, and practical steps to reduce risk before an audit notice ever arrives.

TLDR

- Real estate investors face higher audit risk due to complex returns with high income, large deductions, and paper losses

- Common triggers: accelerated depreciation, income mismatches, repair vs. improvement classification errors, REPS and STR claims

- IRS audits returns within 3 years (6 years if significant underreporting exceeds 25%)

- Best defense: organized records, time logs, and engineering-based cost segregation studies completed contemporaneously

- CCSP-certified cost segregation studies from Seneca Cost Segregation deliver audit-ready documentation that holds up under IRS scrutiny

Why Real Estate Investors Face Higher Audit Risk

The IRS uses automated scoring systems to flag returns that deviate from statistical norms. The primary algorithm, called the Unreported Income Discriminant Function (UI DIF), mathematically scores every tax return for examination potential. Real estate investor returns routinely fall outside normal ranges due to complexity.

What Draws IRS Attention:

Returns that show $300,000 in W-2 or business income reduced to near zero by property-related deductions get flagged automatically — regardless of whether every deduction is legitimate. The algorithm doesn't evaluate intent; it scores statistical deviation.

Automated reviews are most likely when these patterns appear:

- Large Schedule E expenses that look disproportionate to reported income

- Significant depreciation deductions that offset active income

- Rental losses claimed on returns without real estate professional status

Algorithmic flags aren't the only risk. If a business partner, co-investor, or transaction counterparty is being audited, the IRS Internal Revenue Manual instructs examiners to identify and examine related returns using Form 5345-D to expand the examination. One audit in your network can pull your return into scope.

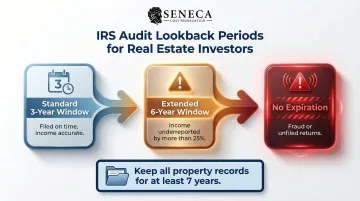

How Far Back Can the IRS Audit a Real Estate Investor?

The Standard 3-Year Window

Under IRC §6501(a), the IRS typically has 3 years from the filing date (or due date, whichever is later) to initiate an audit. This is the baseline most investors operate under.

The 6-Year Exception

If the IRS identifies that income was underreported by more than 25%, the lookback period extends to 6 years under IRC §6501(e)(1)(A). For investors with multiple income sources — rental income, capital gains, 1099 income from real estate activities — accurate income reporting becomes critical.

Practical Implications

A few rules every real estate investor should know:

- No expiration for fraud or unfiled returns — the IRS can audit these at any time, with no time limit

- Keep records for at least 7 years, including depreciation schedules, closing documents, receipts, and time logs

- Property records require longer retention — the IRS instructs taxpayers to keep property-related records until the limitations period expires for the year that property is sold

Top IRS Audit Triggers for Real Estate Investors

Income-Related Triggers

High Earnings

Audit rates scale aggressively with income. According to the IRS Data Book, examination coverage for taxpayers with Total Positive Income (TPI) of $1 million to $5 million was 1.0% in Tax Year 2020, rising dramatically to 8.8% for TPI of $10 million or more.

Real estate investors with significant W-2 income alongside rental portfolios are particularly visible because their returns combine high reported income with substantial offsetting deductions.

Mismatched Income Figures

The IRS cross-references all income reported to them — W-2s, 1099s, 1098s, and Form 1099-S from property sales — against what appears on your return. The Automated Underreporter (AUR) program automatically flags discrepancies.

Any mismatch, even an honest oversight, can auto-trigger a correspondence audit via CP2000 notice. All income sources should reconcile before filing.

Significant Income Swings

A dramatic drop in reported income from one year to the next — especially without a clear economic reason — can look like underreporting to IRS algorithms. Document any major events that explain year-over-year income changes:

- Extended vacancy periods

- Major renovations that took units offline

- Property sales that shifted income recognition

- Market downturns affecting occupancy rates

Deduction-Related Triggers

Large or Disproportionate Deductions

The IRS compares deductions to industry norms. When depreciation deductions, repairs, or operating expenses are unusually large relative to income or to other investors in the same bracket, it raises a flag. This scrutiny applies directly to investors using accelerated depreciation methods like cost segregation — where first-year deductions can be substantial — making proper documentation and an engineering-based study critical for defending those positions.

Misclassified Repairs vs. Improvements

This is one of the most scrutinized areas in real estate tax returns. Under Treasury Regulation §1.263(a)-3, the IRS draws a clear distinction:

- Repairs: Maintain existing condition, deductible immediately under §162

- Improvements: Betterments, restorations, or adaptations to a new use, must be capitalized and depreciated

The IRS Capitalization of Tangible Property Audit Technique Guide directs examiners to scrutinize whether costs were improperly expensed rather than capitalized. Replacing a roof section is a repair; replacing an entire roof is typically a capital improvement.

Safe Harbor: Taxpayers can elect a de minimis safe harbor to deduct expenditures up to $2,500 per invoice or item for those without an applicable financial statement.

Home Office, Vehicle, and Lifestyle Deductions

The IRS is skeptical of home office and vehicle deductions claimed by self-employed investors, especially when amounts appear excessive relative to documented business use. Red flags include:

- Round numbers (exactly 100% business use of a vehicle)

- Home office deductions without exclusive and regular business use

- Inflated charitable donations

- Listed property deductions without adequate substantiation

Each of these deductions has specific documentation requirements. IRS Publication 587 requires home office space be used "exclusively and regularly" as a principal place of business, while Publication 946 requires detailed records for vehicle and listed property depreciation.

Advanced Tax Strategies That Draw Extra IRS Scrutiny

Real Estate Professional Status (REPS)

Under IRC §469(c)(7), rental real estate activities are non-passive if you meet two tests:

- More than half of personal services performed in all trades or businesses during the year are in real property trades or businesses in which you materially participate

- You perform more than 750 hours of services during the year in those real property trades or businesses

Why the IRS Pays Attention:

The IRS knows REPS is frequently claimed incorrectly, particularly by investors holding full-time W-2 jobs. The Passive Activity Loss Audit Technique Guide instructs examiners to request appointment books, diaries, calendars, and contemporaneous logs.

What IRS Agents Specifically Ask:

- Who monitors the properties day-to-day?

- Who collects rent and handles tenant communications?

- Does a property manager handle operations?

- Were time logs maintained contemporaneously or reconstructed later?

Tax Court Denials:

In Lucero v. Commissioner (T.C. Memo. 2020-136), REPS was denied because the taxpayer relied on a reconstructed log created during IRS Appeals. The court excluded investor activities (paying bills, preparing taxes) and commuting time, calling the log a "postevent ballpark guestimate."

Short-Term Rental (STR) Tax Strategies

Under Temp. Reg. §1.469-1T(e)(3)(ii)(A), an activity is not a "rental activity" if the average period of customer use is 7 days or less. This means STRs can generate non-passive losses.

The Catch:

You must meet material participation tests (typically more than 500 hours, or more than 100 hours and not less than any other individual). The IRS examines whether you actually managed guest communications, maintenance, and operations, or whether that was outsourced to a property manager.

Cost Segregation and Bonus Depreciation

A cost segregation study that produces an unusually large first-year depreciation deduction will draw IRS scrutiny. The agency's concern isn't whether cost segregation is legitimate — it is — but whether the methodology holds up under examination.

The IRS Cost Segregation Audit Technique Guide (Pub 5653) confirms that cost segregation is a recognized strategy. However, the guide states that a "detailed engineering approach from actual cost records" is the most methodical and accurate, whereas "rule of thumb" estimates lacking documentation are viewed with caution.

What the IRS Expects from a Cost Segregation Study:

An engineering-based study provides the technical documentation examiners look for:

- Property-by-property asset classifications

- Engineering analysis tied to actual cost records

- Supporting depreciation schedules

- Site visit documentation

Seneca Cost Segregation performs studies to this standard — CCSP-certified, engineering-based, and backed by an AuditDefense guarantee. If the IRS questions a study, investors aren't left to respond alone.

Passive vs. Nonpassive Activity Misreporting

Documentation gaps don't stop at depreciation schedules. Incorrectly categorizing income or losses as passive versus nonpassive is a documented IRS audit focus — and the errors are often procedural, not intentional.

Common errors include:

- Grouping or ungrouping properties incorrectly

- Failing to file the proper grouping election with the original return

- Missing the required election statement under Regs. Sec. 1.469-9(g) to treat all rental real estate as a single activity

Documentation gaps created by missed elections are difficult to defend retroactively, though late relief may be available under Rev. Proc. 2011-34.

How to Proactively Reduce Your Audit Risk

Emphasize Contemporaneous Documentation

Time logs for REPS and material participation, categorized receipts for repairs versus improvements, and mileage logs should be maintained throughout the year — not assembled after an audit notice arrives.

Treasury Regulation §1.469-5T(f)(4) allows participation to be established by "any reasonable means," but Tax Court precedent establishes that retroactively reconstructed records carry far less weight. In Lucero, the court rejected logs created during appeals as "postevent ballpark guestimates."

Maintain Core Documents for Every Property

Essential records every real estate investor should keep:

- Financial statements: Reconciled P&L and balance sheets for each property

- Depreciation schedules: Showing cost basis and placed-in-service dates

- Closing documents: For every acquisition and sale

- Loan documents: Mortgages, refinance paperwork

- Lease agreements: Current and historical

- Expense receipts: Categorized by property and tax year

- Time logs: Contemporaneous records for REPS or material participation claims

Digital storage organized by property and tax year makes retrieval during an audit straightforward.

Work with Specialized Professionals Year-Round

Organized records only protect you if your return positions are defensible — that's where a specialized CPA earns their fee. A CPA familiar with real estate tax law can flag high-risk positions before filing and attach voluntary disclosure statements where appropriate (Form 8275 or Form 8275-R). This ensures the return is structured to reduce scrutiny from the start.

For investors using cost segregation, Seneca Cost Segregation offers complimentary tax assessments alongside CCSP-certified studies that meet all 13 IRS principal elements for quality cost segregation reports — reviewed by senior engineers and tax professionals before delivery.

Frequently Asked Questions

What is the 3 year rule for the IRS?

The IRS has 3 years from the filing date (or due date, whichever is later) to audit a return under standard circumstances. This window extends to 6 years if income is underreported by more than 25%. Real estate investors should keep records for at least 7 years to be safe.

How does the IRS know if you sold a home?

The IRS is automatically notified through Form 1099-S, which title companies and settlement agents are required to file for real estate sales. The IRS cross-references this against the seller's return to verify proper reporting of capital gains or applicable exclusions.

What not to say during an audit?

Don't volunteer information beyond what's requested, make speculative statements without documentation, or misrepresent facts. The IRS can refer cases for criminal investigation if fraud is suspected, so let a qualified CPA handle all communication.

Does cost segregation increase the risk of an IRS audit?

Cost segregation itself does not trigger audits, but large bonus depreciation deductions can attract IRS attention. An engineering-based study with proper documentation that follows the IRS Cost Segregation Audit Technique Guide is fully defensible and unlikely to result in an adverse outcome.

What documents should real estate investors keep in case of an IRS audit?

Keep depreciation schedules, closing statements, lease agreements, expense receipts, bank statements, and contemporaneous time logs for material participation or REPS claims. Organize these digitally by property and tax year for fast retrieval during an audit.

Can the IRS audit multiple tax years at once?

Yes, the IRS can examine multiple tax years simultaneously, particularly when an issue identified in one year is likely to appear in adjacent years. This makes consistent and correct filing practices across all years especially important for real estate investors.