Introduction

Many rental property owners spend thousands on mortgage interest, repairs, insurance, and property taxes, sometimes more than they collect in rent, yet still can't deduct those losses on their tax returns. It's a genuinely confusing situation, and it catches a lot of investors off guard.

Others see their properties generate positive cash flow while depreciation creates substantial "paper losses" on Schedule E, only to find the IRS won't let them apply those deductions against W-2 income or business earnings.

IRS passive activity rules make rental loss deductions far more complicated than most investors expect. According to IRS Publication 925, rental activities are automatically classified as passive, meaning losses can only offset passive income by default. For the typical landlord earning a salary or running an active business, that's a real tax planning problem.

This guide cuts through the complexity. You'll learn how rental losses are classified, the two key exceptions that allow deductions against ordinary income, income limits that affect eligibility, and practical strategies to maximize what you can write off, including how accelerated depreciation through cost segregation can create massive first-year deductions when deployed strategically.

TLDR:

- Rental losses are passive by default and can only offset passive income, not wages or business income

- The $25,000 special allowance lets active participants offset ordinary income if MAGI stays under $150,000

- Real estate professionals and short-term rental hosts who materially participate can bypass passive loss limits entirely

- Cost segregation with 100% bonus depreciation (reinstated for property acquired and placed in service after Jan. 19, 2025, under the One Big Beautiful Bill Act) unlocks major front-loaded deductions; the TCJA phase-down remains in effect for property acquired before January 19, 2025

- Suspended losses carry forward indefinitely and unlock fully when you sell the property

What Are Rental Property Losses?

A rental property loss occurs when your total deductible expenses (mortgage interest, property taxes, insurance, maintenance, repairs, utilities, property management fees, and depreciation) exceed the rental income you collected during the tax year.

The IRS distinguishes between two types of rental losses:

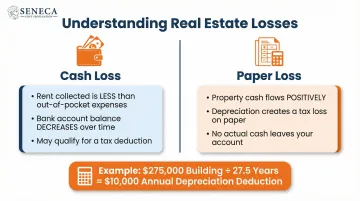

- Cash losses happen when rent doesn't cover out-of-pocket costs like mortgage payments, property taxes, and repairs. Your bank account takes a hit, but you may qualify to deduct those losses.

- Paper losses occur when your property cash flows positively, yet depreciation creates a tax loss on paper. Even profitable rentals can show a loss because depreciation reduces taxable income without any actual cash leaving your account.

That second type—the paper loss—is where real estate investors gain a significant tax edge. Under the IRS General Depreciation System, residential rental property depreciates over 27.5 years using the straight-line method. On a $275,000 building (excluding land), that's $10,000 deducted annually ($275,000 ÷ 27.5), whether or not you spent a dime. Understanding this mechanic is the first step toward using rental losses strategically rather than just absorbing them.

How the IRS Classifies Rental Losses: The Passive Activity Rules

Here's the core problem: IRC Section 469 automatically classifies rental activities as "passive activities," regardless of how actively involved you are in managing the property. This classification creates a strict limitation: rental losses can only offset passive income. They cannot reduce wages, business income, or investment income.

Passive vs. Active Income: What's the Difference?

Understanding the income classification system is critical:

| Income Type | Examples |

|---|---|

| Passive Income | Rental income from real estate; Income from businesses where you don't materially participate; Royalties from intellectual property |

| Active (Ordinary) Income | W-2 wages and salaries; Self-employment earnings; Income from businesses where you materially participate |

| Portfolio Income | Dividends and interest; Capital gains from investments; Annuity income |

The default rule is unforgiving. A landlord earning $90,000 in salary who generates a $20,000 rental loss cannot use that loss to reduce taxable wages. The loss is suspended because there's no passive income to offset.

Portfolio income doesn't help either. IRS Publication 925 explicitly excludes dividends, interest, and capital gains from the passive income category.

What Happens to Losses You Can't Deduct Right Away?

Rental losses that exceed your passive income aren't lost permanently. They're "suspended" and carried forward indefinitely. These suspended losses accumulate year after year, waiting for one of two triggering events:

Future passive income generation: If you acquire additional rental properties that produce net income or invest in other passive activities generating profits, your suspended losses can offset that income.

Property disposition: When you sell the rental property in a fully taxable transaction to an unrelated party, all previously suspended passive losses associated with that property become fully deductible in the year of sale.

If you've accumulated $50,000 in suspended losses over five years and sell the property for a $100,000 gain, those suspended losses reduce your taxable gain to $50,000. At disposition, suspended losses also offset depreciation recapture, often the steepest tax hit when exiting a rental investment.

The $25,000 Rental Loss Allowance: Who Qualifies and What Are the Limits

IRC Section 469(i) carves out a special exception to the passive loss rules: the $25,000 rental loss allowance. Qualifying taxpayers can deduct up to $25,000 of rental losses against their ordinary income each year, even without passive income to offset. Congress created this exception specifically to avoid penalizing small landlords.

Who Qualifies for the $25,000 Allowance?

Two requirements must be met:

Active participation is the first requirement. This is a lower bar than material participation—it means making meaningful management decisions such as:

- Setting rental terms and approving lease agreements

- Approving new tenants

- Deciding on repairs and capital improvements

- Arranging for property services

Physical presence isn't required. An out-of-state owner who approves tenants via email, sets rent rates annually, and authorizes major repairs qualifies—even with a property manager handling day-to-day execution. Limited partners in partnerships, however, automatically fail this test.

Ownership threshold is the second requirement: you (and your spouse if filing jointly) must own at least 10% of the property's value at all times during the tax year.

How the Phaseout Works for Higher Earners

The $25,000 allowance isn't available to everyone. It begins phasing out when your modified adjusted gross income (MAGI) exceeds $100,000, reducing by $0.50 for every dollar above that threshold. The allowance disappears entirely at $150,000 MAGI.

Phaseout Examples:

| MAGI | Phaseout Calculation | Allowance Available |

|---|---|---|

| $100,000 or less | No phaseout | $25,000 |

| $120,000 | ($120,000 - $100,000) × 0.50 = $10,000 reduction | $15,000 |

| $140,000 | ($140,000 - $100,000) × 0.50 = $20,000 reduction | $5,000 |

| $150,000+ | Fully phased out | $0 |

MAGI for this purpose starts with your adjusted gross income and adds back specific items including IRA contributions, student loan interest deductions, and certain other adjustments. IRS Publication 925 provides precise calculation guidance.

The phaseout rules tighten further for married couples filing separately. If you lived apart from your spouse the entire year, the maximum allowance drops to $12,500 and the phaseout begins at $50,000 MAGI.

If you lived together at any point during the year, you cannot claim the allowance at all when filing separately.

Two Key Exceptions to Passive Loss Rules

Beyond the $25,000 allowance, two additional exceptions can allow landlords to deduct much larger rental losses or bypass passive loss rules entirely.

Exception 1: The Real Estate Professional Status

The real estate professional (REP) exception under IRC Section 469(c)(7) completely exempts qualifying landlords from passive loss classification. REPs can deduct unlimited rental losses against any income (wages, business earnings, investment income) without restriction.

The Two-Part Qualification Test

More than 50% of working hours: Over half of your total working hours during the year must be spent in real property trades or businesses where you materially participate, including development, construction, rental operations, brokerage, or property management.

750-hour minimum: You must log more than 750 hours per year in those real property activities.

Both conditions must be met. A full-time W-2 employee working 2,000 hours annually needs at least 1,001 hours in real estate to clear the 50% threshold, which makes REP status impractical for most people with demanding day jobs. Many qualifying taxpayers are spouses who manage the couple's rental portfolio full-time.

Material Participation: The Step Most REPs Miss

Qualifying as a REP alone doesn't automatically make rental losses deductible. It only removes the "per se passive" label. You must still materially participate in each individual rental activity. The most common test requires more than 500 hours per year per property.

For multi-property owners, hitting 500 hours per property is impractical. Reg. §1.469-9(g) addresses this by allowing qualifying REPs to file a grouping election that treats all rental properties as a single activity.

This election must be made with your original tax return and is binding for all future years unless circumstances materially change. Skip it, and you'd need to prove 500+ hours for each separate property, a standard almost no one can meet.

Exception 2: The Short-Term Rental Exception

If your property's average rental period is 7 days or fewer, it's not automatically treated as a passive rental activity under Temp. Reg. §1.469-1T(e)(3)(ii)(A). Instead, it's subject to the general material participation tests, meaning qualifying hosts can offset other income with short-term rental (STR) losses.

Meeting Material Participation as an STR Host

To deduct STR losses against ordinary income, you must materially participate using one of the seven IRS tests:

| Material Participation Test | Requirement |

|---|---|

| 500-Hour Test | You participate more than 500 hours during the year |

| Substantially All Test | Your participation constitutes substantially all participation by all individuals |

| 100-Hour Test | You participate more than 100 hours AND no one else participates more |

The 100-hour test is useful for STR hosts who handle guest communications, booking management, and property oversight but hire cleaners. If you log 150 hours managing the property and your cleaning service logs 100 hours, you pass. But if you hire a full-service management company logging 200 hours while you log only 100, you fail and the activity remains passive.

Strategies to Maximize Your Rental Loss Deductions

Accelerate Depreciation Through Cost Segregation

Standard depreciation spreads your building's cost over 27.5 years. Cost segregation reclassifies components such as flooring, appliances, fixtures, landscaping, and parking lots into 5-, 7-, or 15-year MACRS categories instead.

With 100% bonus depreciation reinstated for property acquired and placed in service after January 19, 2025 under the One Big Beautiful Bill Act, those reclassified components can often be deducted in full in Year 1. The TCJA phase-down is still in effect. If a taxpayer acquired a property before January 19, 2025, and places it into service after January 19, 2025 in 2025 or 2026, they will experience 40% bonus depreciation and 20% bonus depreciation, respectively.

Bonus Depreciation Timeline

| Period | Bonus Depreciation Rate | Notes |

|---|---|---|

| September 27, 2017 – December 31, 2022 | 100% | — |

| January 1, 2023 – December 31, 2023 | 80% | — |

| January 1, 2024 – December 31, 2024 | 60% | — |

| January 1, 2025 – January 18, 2025 | 40% | — |

| January 19, 2025 – December 31, 2030 | 100% | Applies if acquisition date is January 19, 2025 or later |

| 2025 (property acquired before January 19, 2025) | 40% | TCJA phase-down applies |

| 2026 (property acquired before January 19, 2025) | 20% | TCJA phase-down applies |

Engineering-based cost segregation studies identify which components qualify for accelerated treatment and provide IRS-compliant documentation. Seneca Cost Segregation's studies have delivered an average first-year deduction of $171,243—giving investors paper losses they can deploy through the $25,000 allowance, REP status, or STR material participation rules.

Manage Your AGI to Preserve the $25,000 Allowance

If your MAGI hovers near the $100,000–$150,000 phaseout range, strategic AGI management preserves your rental loss deduction:

| AGI Reduction Method | How It Works |

|---|---|

| SEP-IRA contributions (Schedule 1, Line 16) | Directly reduces AGI for self-employed taxpayers |

| Deferring bonuses or consulting income to the following year | Lowers current-year AGI |

| Harvesting investment losses | Offsets capital gains |

| HSA contributions | Reduces AGI dollar for dollar |

Example: An investor with $140,000 AGI and $25,000 in rental losses faces a $20,000 phaseout penalty, leaving only $5,000 deductible. A $20,000 SEP-IRA contribution drops AGI to $120,000, cutting the phaseout to $10,000 and preserving $15,000 of rental loss deductions, a $10,000 improvement.

File a Grouping Election for Multiple Properties

Beyond AGI management, real estate professionals with multiple properties can simplify participation tracking with a grouping election under Reg. §1.469-9(g). Treating all properties as a single rental activity lets you aggregate hours across the portfolio rather than tracking each property separately, making the 500-hour material participation test much easier to satisfy. This election must be filed with your original return and requires a formal statement.

Recordkeeping: How to Prove Your Rental Losses

The IRS requires thorough documentation to support rental losses. The following records apply to each property:

| Documentation Category | Required Items |

|---|---|

| Expense Documentation | Receipts for all repairs, maintenance, and improvements; Bank and credit card statements showing rental-related transactions; Mortgage interest statements (Form 1098); Property tax bills and payment records; Insurance policy documents and premium receipts; Utility bills for landlord-paid services; Property management agreements and fee invoices; Depreciation schedules and cost segregation study reports |

| Income Documentation | Lease agreements for all tenants; Rent rolls showing payments received; Records of vacancy periods; Documentation of uncollected rent or evictions; Security deposit accounting |

Time Logs for REP or Material Participation Claims

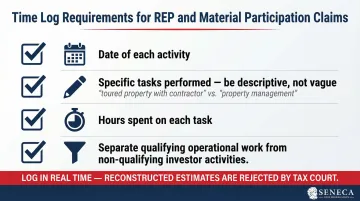

Beyond income and expenses, one documentation gap consistently derails audits: time. If you're claiming REP status or material participation in short-term rentals, the IRS will ask for contemporaneous time logs, and it routinely challenges hours claims. Despite Temp. Reg. §1.469-5T(f)(4) allowing "any reasonable means" to prove participation, Tax Court has repeatedly rejected post-event estimates and reconstructed logs.

Detailed records include:

- Date of each activity

- Specific tasks performed (e.g., "toured property with contractor to assess roof repair" not "property management")

- Hours spent on each task

- Separation of qualifying operational work from non-qualifying investor activities (reviewing financial statements, researching investments)

Contemporaneous time logs created in real time provide stronger documentation; vague hour estimates created after the fact won't hold up in Tax Court.

Frequently Asked Questions

What is the limitation of rental loss deduction?

Rental losses are subject to passive activity loss rules under IRC Section 469. By default, losses can only offset passive income. A $25,000 exception allows active participants earning under $150,000 MAGI to deduct losses against ordinary income, with unlimited exceptions available for qualifying real estate professionals.

What is the $25,000 rental loss allowance?

The $25,000 rental loss allowance lets landlords who actively manage their rental property and have MAGI below $100,000 deduct up to $25,000 in rental losses against ordinary income each year. The benefit phases out between $100,000 and $150,000 MAGI and disappears entirely above that threshold.

How to prove loss of rental income?

Expense receipts, bank statements, rent rolls, lease agreements, and vacancy records document cash losses. Depreciation schedules and cost segregation reports cover non-cash deductions. For real estate professional or material participation claims, contemporaneous time logs showing the work performed and when it was performed are required.

What happens to suspended rental losses when I sell my property?

All suspended passive losses tied to a rental property are released and become fully deductible in the year you sell the property in a fully taxable transaction to an unrelated party. This can offset capital gains and depreciation recapture from the sale.

Can a real estate professional deduct unlimited rental losses?

Yes. Taxpayers who qualify as real estate professionals under IRS rules (750+ hours in real property businesses, more than 50% of working time) and materially participate in their rental activities (typically 500+ hours or through a grouping election) can deduct unlimited rental losses against any type of income, including W-2 wages.